A 35-year-old earning $95,000 a year with $41,000 in net worth looks financially stable from the outside. By Thomas Stanley’s measure, that figure sits at roughly 12% of where it should be. Stanley spent nearly two decades studying actual American millionaires for The Millionaire Next Door (1996) and found that genuine wealth and the appearance of wealth are almost perfectly inversely correlated. His expected net worth formula gives anyone a fast, objective read on which side of that line they occupy.

This guide explains how the formula works, how to apply it accurately, where it breaks down and why, and what a reader who scores poorly should do about it. The result is a number, a classification, and a clear next step.

What the Thomas Stanley net worth formula actually measures

The formula is a behavioural diagnostic first and a mathematical exercise second. The number it returns is not a savings target. It is a mirror showing whether wealth is scaling appropriately with earning years, or whether income is being consumed faster than it accumulates.

The formula’s behavioural logic becomes sharper when set against a second reality: inflation erodes purchasing power silently across the same earning years the formula measures, meaning a household that fails to accumulate also loses real value on whatever it does hold.

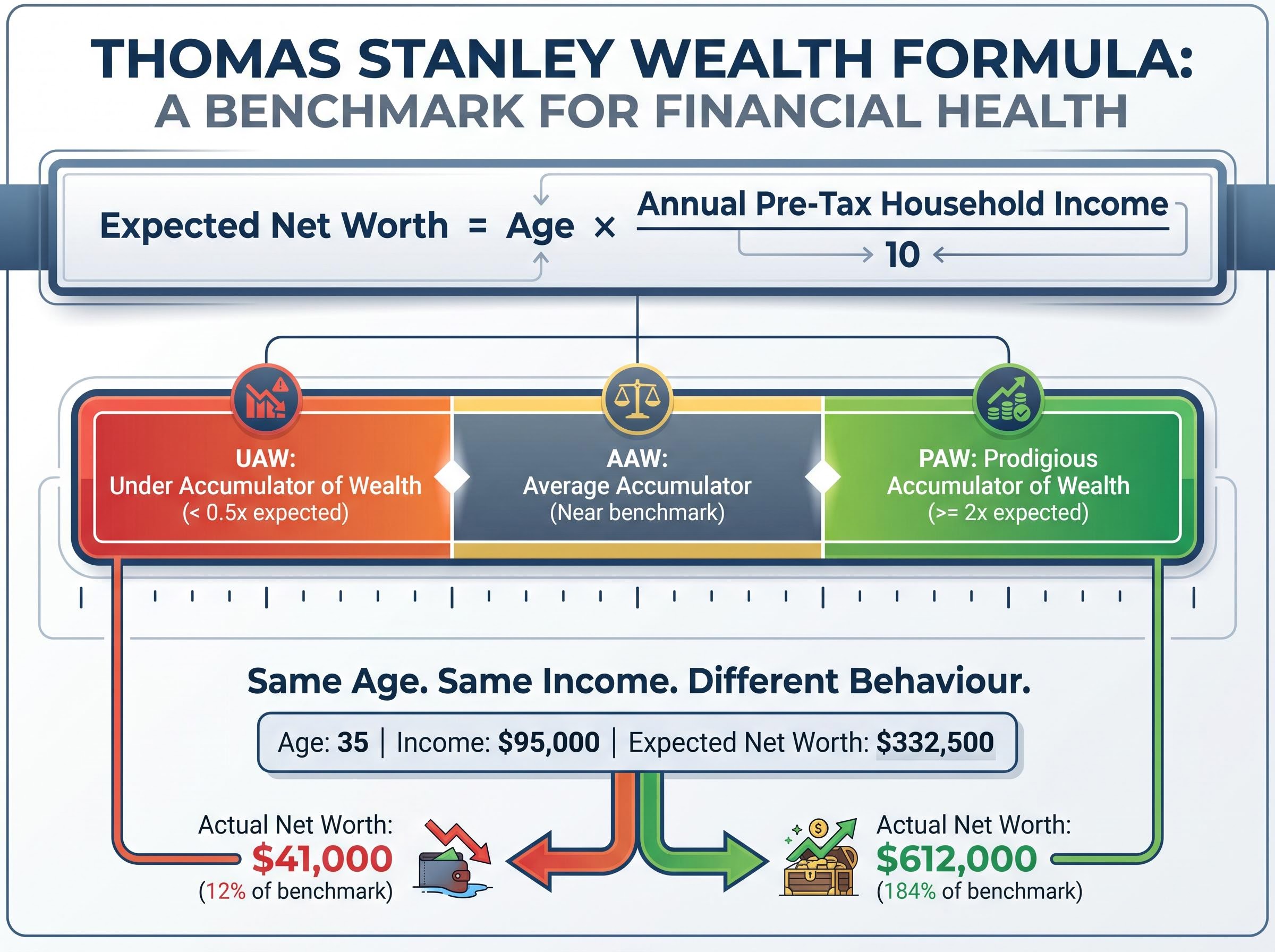

Expected Net Worth = Age x Annual Pre-Tax Household Income / 10

The calculation takes three steps:

- Multiply current age by annual pre-tax household income.

- Divide the result by 10.

- Compare the output to actual net worth and classify the result.

Stanley created three classifications based on how actual net worth compares to the expected figure. A Prodigious Accumulator of Wealth (PAW) holds actual net worth at or above 2x the expected number. An Average Accumulator of Wealth (AAW) falls somewhere near the benchmark. An Under Accumulator of Wealth (UAW) holds actual net worth below 0.5x of the expected figure.

The classifications matter because they separate earners from accumulators. A 35-year-old earning $95,000 has an expected net worth of $332,500. At $41,000 actual, that is approximately 12% of the benchmark, placing them deep in UAW territory. At $612,000 actual, that same person sits at roughly 184% of the benchmark, a solid PAW. Same age, same income. The difference is entirely behavioural.

Most people carry an intuitive sense of whether they are “doing okay” financially, but that sense is heavily contaminated by peer comparison and lifestyle signals. The formula replaces intuition with a number anchored in income and time, the two variables that actually determine how much wealth a person has the capacity to build.

When big ASX news breaks, our subscribers know first

How most Americans actually score against the benchmark

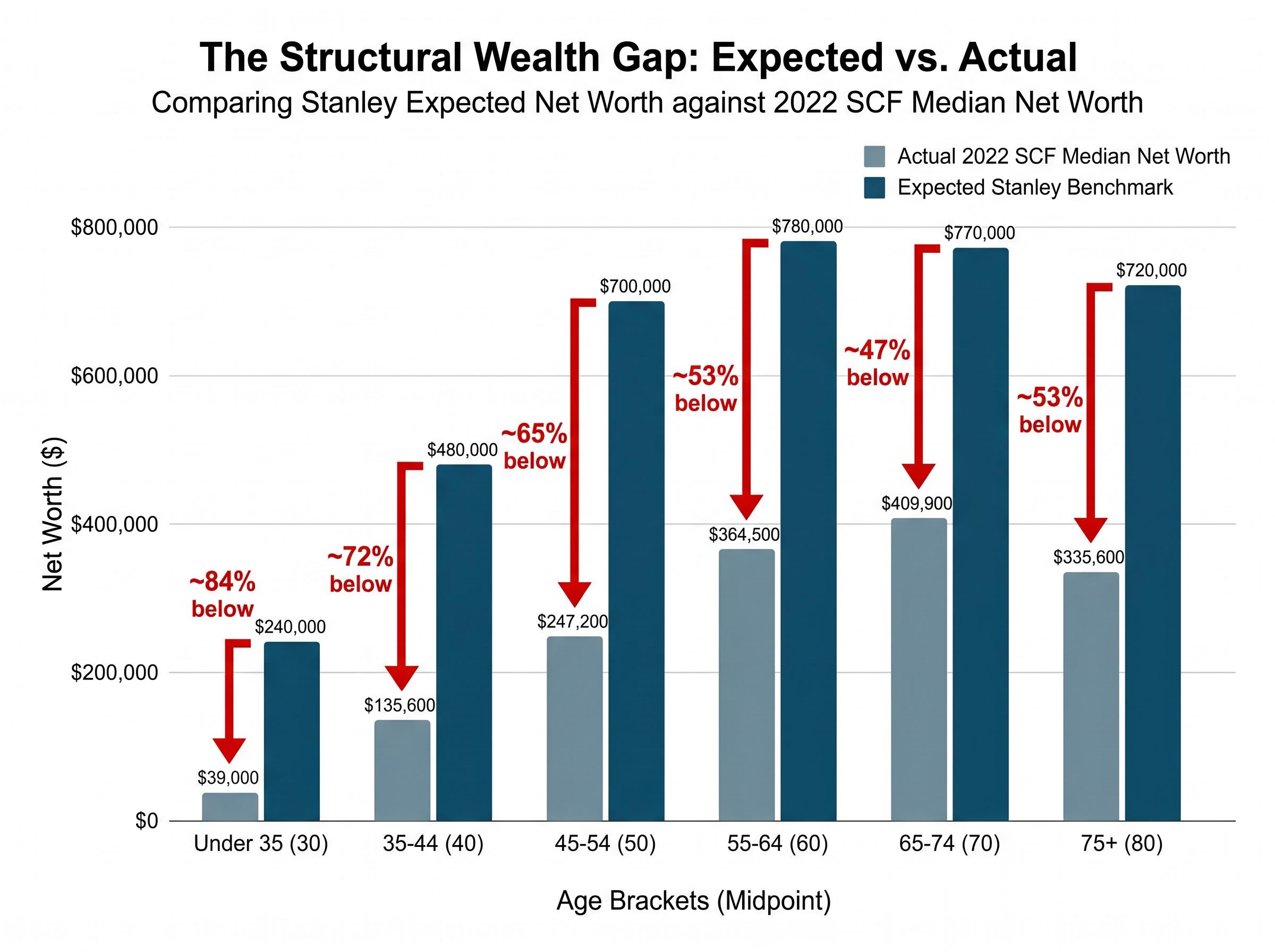

The 2022 Survey of Consumer Finances (SCF), published by the Federal Reserve in October 2023, provides the most authoritative snapshot of household wealth in the United States. When median net worth figures from that survey are placed alongside the Stanley expected benchmarks for each age bracket, the gap is not a close miss.

The Federal Reserve Survey of Consumer Finances, conducted every three years and last published in October 2023 covering 2022 data, is the primary source for household wealth distribution in the United States, capturing assets, liabilities, income, and demographic characteristics across a nationally representative sample.

It is structural.

| Age Bracket | Age Midpoint | 2022 SCF Median Net Worth | Stanley Expected Net Worth | Gap |

|---|---|---|---|---|

| Under 35 | 30 | $39,000 | $240,000 | ~84% below |

| 35-44 | 40 | $135,600 | $480,000 | ~72% below |

| 45-54 | 50 | $247,200 | $700,000 | ~65% below |

| 55-64 | 60 | $364,500 | $780,000 | ~53% below |

| 65-74 | 70 | $409,900 | $770,000 | ~47% below |

| 75+ | 80 | $335,600 | $720,000 | ~53% below |

Medians run 47-84% below the Stanley benchmarks across every age group. The youngest cohort, under 35, faces the widest gap. Even the best-performing bracket, ages 65-74, still falls nearly half short.

According to the 2022 SCF, approximately 49% of US households lacked sufficient liquid assets to cover three months of expenses.

These gaps reflect population-wide patterns, not individual failure. Median net worth did rise approximately 37% from 2019 to 2022, driven largely by housing appreciation and equity market gains. But context does not change the conclusion: falling short of the Stanley benchmark is common. Common, however, is not the same as acceptable for anyone whose goal is financial independence.

Why high earners are often the worst accumulators

Income and wealth accumulation are weakly correlated once income passes a threshold. The reason is mechanical: higher income attracts higher fixed costs and higher-status peer groups, and both exert constant upward pressure on spending.

Stanley identified three specific mechanisms that drain wealth from high-earning households:

- Lifestyle inflation after raises: Each income increase, when converted to higher monthly spending, creates a permanent obligation that resets the baseline cost of living upward.

- Oversized homes: Carrying $1,200 per month in excess housing costs (maintenance, taxes, insurance, utilities) over 30 years totals approximately $432,000 in additional expenses, with estimated foregone investment growth exceeding $1 million.

- Financed or leased vehicles: A $650 monthly vehicle lease over a 40-year career amounts to approximately $312,000 in cumulative payments. The same amount directed to an S&P 500 index fund could produce an estimated $2-$3 million at retirement.

Physicians and attorneys illustrate the compounding problem. With median incomes around $300,000, they possess enormous earning power. But a late career start (age 30-35 after training) combined with high peer-group lifestyle expectations creates compounded underaccumulation that the formula captures precisely.

The lifestyle inflation trap

Two profiles make the mechanism concrete. Both begin at age 25 earning $95,000 in the same city. Over ten years, the high-expense profile’s vacations escalate from $2,000 to $9,000 annually. Home size grows from roughly 1,800 to 3,200 square feet. Vehicle cost climbs from $35,000 to $75,000.

Each upgrade converts a temporary income gain into a permanent monthly obligation.

At year ten, the high-expense profile holds approximately $41,000 in net worth. The wealth-building profile, operating on the same income trajectory, holds approximately $612,000. That is a 15x difference driven entirely by behavioural choices, not earnings.

This pattern is income-agnostic. Professional athletes experiencing bankruptcy operate through the same mechanism at higher dollar amounts. The trap is not about how much flows in. It is about how much flows out, and whether the outflow ratchets upward with every raise.

The behavioural gap between PAWs and UAWs maps directly onto the mechanics of long-term wealth accumulation: compounding equity returns require both time in market and a savings rate high enough to fund the initial position, which is precisely what lifestyle inflation prevents.

How to apply the formula to your own situation (and where to be careful)

The self-assessment process takes four steps:

- Calculate expected net worth: Multiply current age by annual pre-tax household income, then divide by 10.

- Add up actual net worth: Sum all assets (home equity, investment accounts, retirement accounts, business equity) and subtract all liabilities (mortgages, auto loans, student loans, credit card balances).

- Compute the ratio: Divide actual net worth by expected net worth.

- Identify classification: A ratio of 2.0 or higher is PAW. A ratio below 0.5 is UAW. Everything between is AAW.

That gives the number. The harder task is interpreting it honestly.

Adjustments that are legitimate versus convenient

The formula has documented blind spots. Knowing which adjustments are conceptually defensible, versus which ones function as rationalisation, determines whether the exercise is useful.

Legitimate adjustments include:

- Late career starters: A physician who finished residency at 32 might use (Age minus 10) rather than raw age, acknowledging that a decade of training produced debt rather than income.

- High-cost-of-living areas: Some practitioners divide by 15 instead of 10 for households in coastal metros where housing costs genuinely constrain accumulation.

- Very high earners: For incomes well above $200,000, the formula can produce benchmarks that understate the genuine difficulty of wealth accumulation in the same geographic and peer context.

Rationalisation red flags include citing expensive-city residence without evidence that housing costs, rather than elevated lifestyle standards, explain the gap. Inherited wealth or parental financial transfers also inflate the net worth figure without reflecting accumulation behaviour, something the formula cannot distinguish.

Subtracting non-productive training years is a defensible structural correction. Explaining away the entire gap with circumstance is not.

Beyond the benchmark: alternative frameworks and what they add

Stanley’s formula is a starting point, not the final word. Each alternative framework captures something the original misses.

The FI Number (Financial Independence Number) anchors the target to expenses rather than income. The formula is straightforward: 25x to 33x annual expenses, derived from the 4% safe withdrawal rate. A household spending $80,000 per year targets a portfolio of $2,000,000 to $2,640,000.

The key contrast is sharp. A frugal household earning $200,000 and spending $60,000 needs far less than Stanley’s formula suggests. A high spender earning $200,000 and spending $180,000 needs far more. The FI Number rewards low spending directly; Stanley’s formula does not.

The FI Number framework connects directly to a related question most Stanley PAWs eventually face: the capital needed to live off dividends is substantially higher than most investors assume, with a portfolio tracking the S&P 500 at current yields producing only around $11,000 a year per million dollars invested.

For readers who want to know where they stand relative to peers rather than against a formula, DQYDJ.com offers a net worth percentile calculator based on 2022 Federal Reserve SCF data. It is descriptive rather than prescriptive: it shows positioning without judging it.

| Framework | Basis | Best For | Key Limitation |

|---|---|---|---|

| Stanley Formula | Age x Income / 10 | General benchmark, income earners | Ignores HCOL, late starters, spending |

| FI Number (25x) | Annual expenses x 25 | FIRE community, frugal high earners | Ignores age trajectory |

| SCF Percentile (DQYDJ) | Peer comparison data | Realistic benchmarking | Descriptive, not prescriptive |

| Ramsey Baby Steps | Behavioural stages | Debt-heavy households | Not a net worth formula |

Different frameworks answer different questions. Stanley’s asks whether wealth is scaling with earning years. The FI Number asks whether wealth is scaling toward actual freedom from work. A reader who understands both asks better questions about their own financial situation.

What to do when the formula reveals an underaccumulation problem

The formula produces a number. These three steps produce the behavioural change that moves the number.

- Audit three months of recurring expenses and classify each one as a cash flow contributor or a cash flow extractor. Pay specific attention to subscriptions and automatic charges that have been normalised. Most individuals completing this audit are expected to identify at least three liabilities presenting as assets, recurring costs that feel like standard living but function as wealth drains.

- Apply Stanley’s formula and classify the result honestly. Use any legitimate adjustments identified above, but resist the temptation to adjust until the answer is comfortable. The point of the exercise is diagnosis, not reassurance.

- Write a defined lifestyle ceiling before the next income increase. Specify the maximum monthly cost structure the household will maintain regardless of earnings growth. The wealth-building profile from the earlier comparison operated on exactly this principle: a one-bedroom apartment, a paid-off reliable vehicle, and approximately $700 per month in discretionary spending.

“A written lifestyle ceiling is the most consequential personal finance document most people never create.”

Without a written ceiling, every future income increase is statistically likely to be absorbed by spending expansion. The wealth-building profile’s $612,000 in assets at year ten is estimated to approximately double every decade without additional contributions, based on historical market compounding rates. The behavioural decision made in year one is what unlocked that trajectory.

The number the formula produces matters less than the behaviour it reveals

Stanley’s formula is not a precise financial model. It is a behavioural mirror. The score it returns reflects spending and saving decisions compounded over years, not circumstances beyond a person’s control. Two individuals with identical starting conditions, same age, same income, same city, produced a 15x difference in net worth outcome at year ten ($41,000 versus $612,000) driven entirely by behavioural choices.

The formula has real limitations. Late starters, high-cost geographies, and student debt burdens can suppress the score below what a person’s behaviour alone would produce. Those adjustments are warranted when they are honest. They become rationalisation when they exist solely to soften the verdict.

Stanley’s core finding holds: among the millionaires he studied, genuine wealth and the appearance of wealth were almost perfectly inversely correlated. The practical payoff of genuine accumulation is not a larger house or a newer car. It is financial optionality: the ability to quit, take risk, relocate, or stop working. That freedom is invisible to outside observers by design, and it belongs disproportionately to those whose score reflects years of deliberate, quiet accumulation.

For PAW-status readers whose written lifestyle ceiling has produced a meaningful cash surplus above monthly obligations, our full explainer on deploying capital during a market correction examines how valuation signals, including the Buffett Indicator and Shiller P/E, can inform the timing and sizing of opportunistic equity purchases when market conditions shift.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced in this article are subject to market conditions and various risk factors.

—