Australia’s exchange-traded product market has grown from $185 billion at the end of 2024 to over $230 billion by mid-2026, and with more than 370 funds now listed across the ASX and Cboe, the selection problem has become as real as the opportunity. For investors in their 30s, the challenge is not access to ETFs. It is making the three or four structural decisions that will determine whether the next three decades of compounding work for them or against them.

This guide covers the decisions that matter most: how to select a core ETF allocation, why fees compound against a portfolio with the same force they compound in its favour, and why adding more ETFs often makes a portfolio worse rather than better. Each section is built for an investor who has moved past the basics and is ready to get the structure right.

ASIC Regulatory Guide 282 sets out the operational and disclosure obligations that govern exchange-traded products listed on Australian markets, establishing the framework within which the more than 370 funds now available to investors must operate.

Why your 30s are the moment that determines most of your wealth outcome

Investors in their 30s occupy a position no other age group shares. Seven to ten years of professional earnings have typically produced a meaningful capital base. Superannuation, while growing, remains inaccessible for roughly 30 more years. And the investment horizon stretching ahead is long enough that small structural improvements, a fee reduction of 0.3 percentage points, a better allocation split, compound across decades rather than years.

That arithmetic matters. A 0.3% annual fee difference on a $200,000 portfolio, compounded over 30 years at a 7% gross return, produces a gap of tens of thousands of dollars. The improvement is invisible in any single year. Over a full horizon, it is not.

The competing pressures on this cohort make the stakes sharper. Investors in their 30s are often managing several financial obligations simultaneously:

- Mortgage repayments on property purchased at elevated valuations

- Childcare costs or early education fees

- Private school tuition, which can reach $100,000 per year per family and require approximately $140,000 in pre-tax income for higher earners

- Superannuation that is growing but locked away until preservation age

With after-tax capital under pressure from every direction, the capital that does reach a brokerage account needs to be allocated well. There is no room for structural waste.

When big ASX news breaks, our subscribers know first

The fee you barely notice is quietly the most expensive decision you make

A management fee of 0.04% per annum sounds like nothing. It is $40 per year on a $100,000 balance. The instinct to dismiss it as irrelevant is understandable, and it is wrong.

Fees compound negatively over time in exactly the same mechanical way that returns compound positively. A fee is not a one-off charge deducted from a static balance. It is deducted from a growing balance, every year, for the life of the holding. The damage accelerates in later decades, precisely when the balance is largest and the compounding is doing its most visible work.

The compounding fee advantage is only part of the picture: ETF structure and tax mechanics, including the CGT discount for units held beyond 12 months and the legal separation of fund assets from the issuer’s balance sheet, shape after-tax returns in ways that are just as durable as the fee differential itself.

The practical range of the problem is wider than most investors realise. The lowest-cost Australian equity ETFs charge a fraction of the market average, while some thematic or active ETFs sit well above it.

| ETF Ticker | Fund Name | Asset Class | Fee (p.a.) |

|---|---|---|---|

| A200 | BetaShares Australia 200 ETF | Australian Equities | 0.04% |

| VAS | Vanguard Australian Shares Index ETF | Australian Equities | 0.07% |

| BGBL | BetaShares Global Shares ETF | International Equities | 0.08% |

| VGS | Vanguard MSCI International Shares Index ETF | International Equities | 0.18% |

| DHHF | BetaShares Diversified All Growth ETF | All-in-One (Growth) | 0.19% |

| VDHG | Vanguard Diversified High Growth Index ETF | All-in-One (High Growth) | 0.27% |

The average management fee across the Australian ETF market is estimated at 0.40%-0.50% p.a., meaning a core holding at 0.04% costs roughly one-tenth of the market average. Over a 30-year horizon, that difference is not marginal. It is structural.

Because fees apply to the entire balance and recur every year, they inflict the greatest damage on the largest, longest-held positions. For most passive investors, those positions are core index ETFs. The implication is direct: the core of the portfolio is where fee discipline matters most, not at the margins.

What a core allocation actually means, and how to build one

A core allocation is the broad, low-cost foundation that accounts for the majority of a portfolio, typically 70%-80% of total holdings. It tracks well-known market indices that hold hundreds or thousands of underlying companies, and its purpose is to deliver the return of the market at the lowest possible cost.

The term sounds abstract until it meets a specific question: how much should be in Australian shares, and how much in global shares?

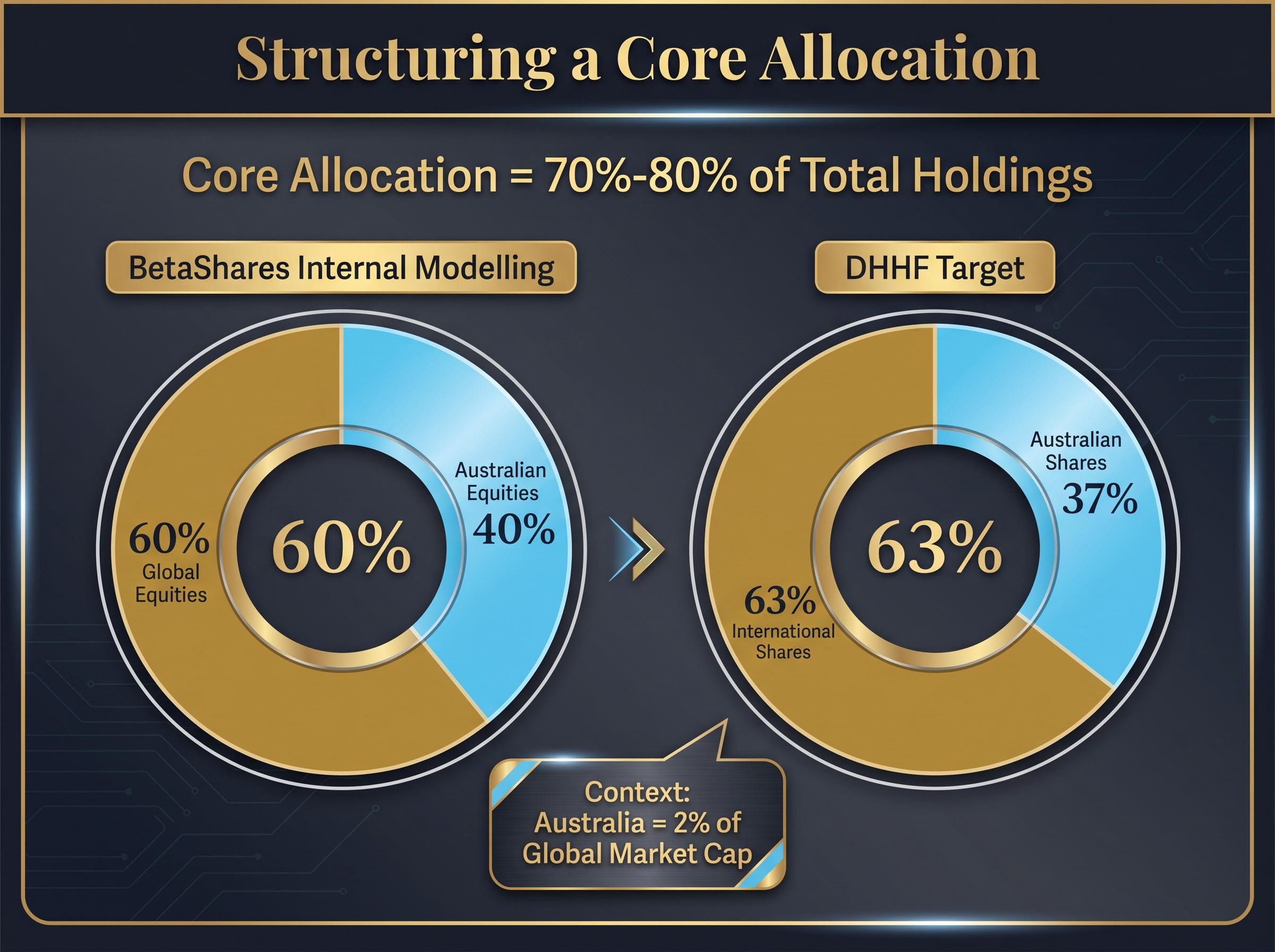

Australia represents approximately 2% of global market capitalisation. An investor who holds only Australian equities is concentrating their entire portfolio in a narrow slice of the global economy, one dominated by financials, materials, and industrials. BetaShares internal modelling suggests approximately 60% global and 40% Australian equities as a risk-adjusted split, and this figure aligns with the allocation embedded in products like DHHF, which targets roughly 63% international and 37% Australian shares.

Cap-weighted domestic ETF concentration is a structural feature that most investors underestimate: the top 10 ASX 200 companies hold approximately 48.6% of a broad domestic ETF, meaning nearly half of local equity exposure lands in banks and miners before any deliberate allocation decision is made.

The case for retaining a meaningful Australian allocation, despite the small global share, rests on two factors. First, Australian equities offer sector diversification against US markets that are heavily technology-weighted. Second, franking credits provide an additional return benefit in taxable accounts that is not available from international holdings.

Two-ETF core versus all-in-one: what each approach actually involves

There are two valid paths to building a core allocation, and neither is universally superior.

The two-ETF approach pairs an Australian equity ETF (such as A200 or VAS) with a global equity ETF (such as BGBL or VGS). The investor controls the split, can adjust it over time, and may achieve a lower aggregate fee.

The all-in-one approach uses a single diversified ETF (such as DHHF or VDHG) that holds both Australian and international equities internally. Rebalancing is managed by the fund, the fee is slightly higher, and the investor makes one purchase rather than two.

The key differences:

- Control: Two-ETF allows the investor to tilt the allocation deliberately; all-in-one locks the ratio

- Rebalancing: Two-ETF requires periodic manual adjustment; all-in-one rebalances internally

- Fees: Two-ETF can be cheaper in aggregate (e.g., A200 at 0.04% plus BGBL at 0.08%); all-in-one carries a single, slightly higher fee

- Behavioural friction: All-in-one removes the temptation to tinker; two-ETF requires the discipline not to

The right choice depends on whether the investor values control or simplicity. Both deliver a diversified core at low cost.

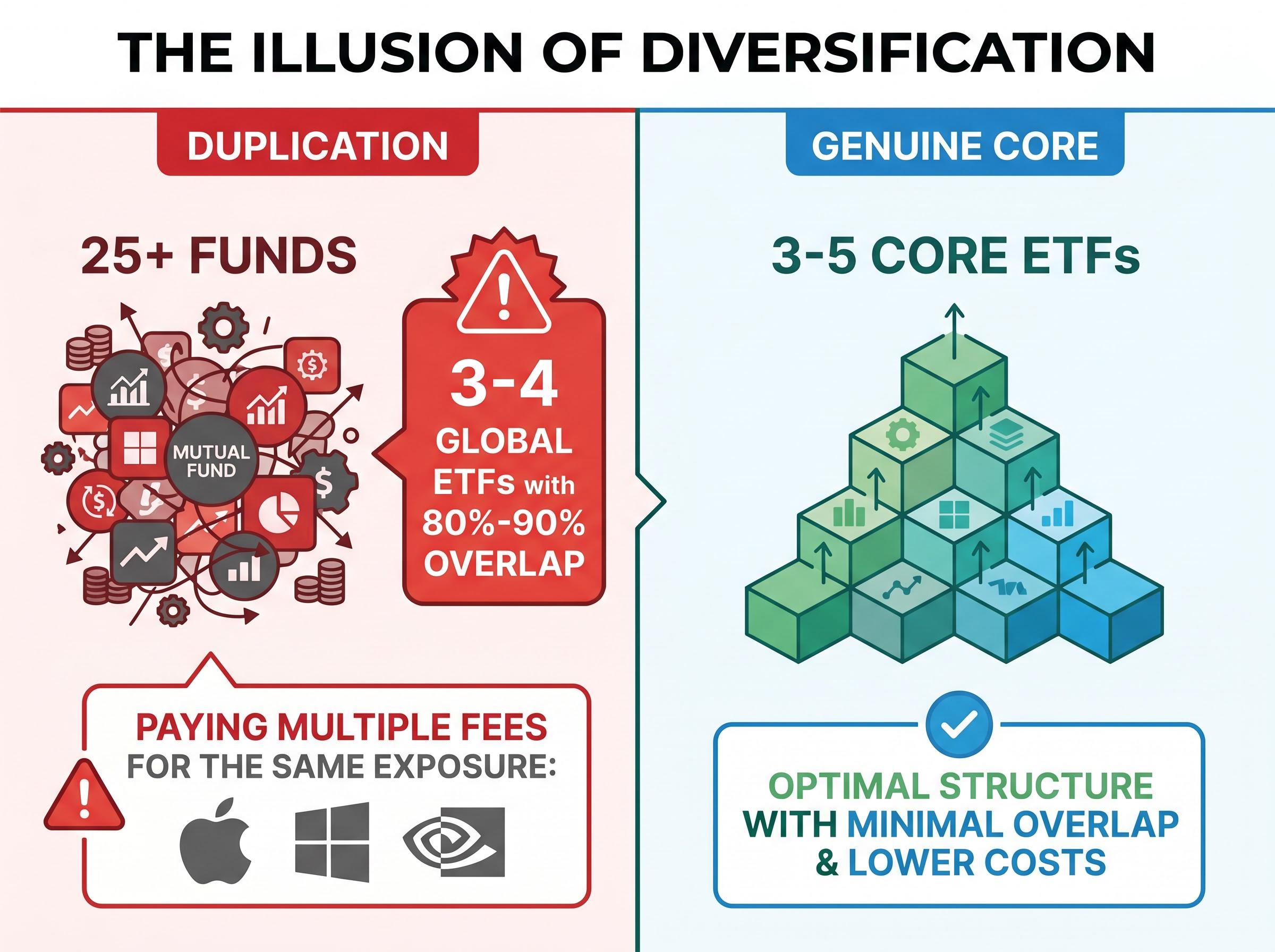

Why holding more ETFs often makes your portfolio less diversified, not more

Diversification requires exposure to genuinely different return drivers, not simply more fund names on a brokerage screen. A portfolio holding five global equity ETFs that track different indices but share 80%-90% of the same underlying mega-cap technology stocks is not diversified. It is duplicated.

According to Morningstar’s Adam Fleck, investors are “creating portfolios of 15-20 ETFs that mostly own the same underlying stocks.”

The overlap problem is well-documented. James Marlay, co-founder of Livewire Markets, reported in March 2025 that advisers are seeing young investors holding 25+ funds, with three or four global equity ETFs that are 80%-90% overlapped. Cameron Gleeson of BetaShares has noted that “holding multiple broad-market ETFs tracking similar indexes can result in unnecessary duplication and higher aggregate fees.”

Ben Nash, financial adviser at Pivot Wealth, has stated that “three or four well-chosen ETFs is enough for most accumulation investors.” Across sources from 2024 and 2025, a portfolio of 3-5 core ETFs is the most commonly cited range for a well-constructed accumulation portfolio.

The practical cost is not just complexity. Each additional ETF adds its own management fee to the aggregate, meaning duplication is not merely redundant but actively corrosive to returns over time.

A simple diagnostic test can reveal whether a portfolio has genuine breadth or cosmetic complexity:

- List every ETF currently held

- Note the top-10 underlying holdings for each fund

- Identify which company names appear across multiple funds

- Assess whether the overlap serves a deliberate purpose (such as a conscious overweight) or is accidental

If the same names, Apple, Microsoft, Nvidia, appear across three or four holdings, the portfolio is paying multiple fees for a single exposure.

How much defensive allocation do investors in their 30s actually need?

The conventional wisdom is straightforward: a 30-year-plus horizon supports 80%-100% growth assets, and bonds are for retirees. The arithmetic supports this view. Over long periods, equities have delivered higher returns than fixed income, and a young investor has time to recover from drawdowns.

The counter-argument is not about arithmetic. It is about behaviour.

James Gerrish, portfolio manager at Market Matters, typically runs 70%-85% growth for clients in their 30s, with the remainder in investment-grade bond ETFs and cash. The reason, as he described in January 2025 on Livewire, is that “a small allocation to bond ETFs can stop clients from panicking during equity sell-offs.” The investor who holds through drawdowns because their portfolio did not fall as far ultimately achieves a better outcome than the investor who was theoretically correct but sold at the trough.

The data suggests younger investors are listening. According to Morningstar’s Annika Bradley, investors aged 25-39 doubled their allocations to bond ETFs between 2022 and 2024, though from a low base. Fixed income ETFs attracted approximately $6.4 billion in net inflows in 2024, their strongest year on record, according to BetaShares.

Morningstar’s Australian ETF market data covering the 2024-2025 period confirms that fixed income ETF inflows reached record levels while broad-market equity ETFs remained the dominant allocation for investors under 40, reinforcing the behavioural pattern that simpler, diversified portfolios attract consistent capital across volatility episodes.

Not all defensive instruments are genuinely defensive. Distinguishing between the two categories matters:

- Genuinely defensive: Investment-grade government bonds, short-duration bond ETFs, cash ETFs. These tend to hold value or appreciate when equities sell off.

- Equity-like characteristics: Floating rate credit, infrastructure funds, high-yield corporate bonds. These may carry “defensive” labels but often fall alongside equities during stress periods.

Short-duration bond ETFs and cash ETFs have attracted particular attention in 2026 as investors navigate a stagflationary environment where supply-shock inflation and rising bond yields are occurring simultaneously, a combination that challenges the assumption that all fixed income behaves defensively during equity drawdowns.

Matching defensive allocation to your actual risk tolerance, not the textbook version

A 10%-30% defensive allocation is the range most commonly cited across 2024-2025 sources, with the key variable being individual risk tolerance and income stability.

The honest question is whether the investor has experienced, or can realistically simulate, a 20%-30% portfolio drawdown without selling. Investors with high fixed obligations, a mortgage, private school fees, regular childcare costs, have a practical argument for some defensive allocation independent of equity market theory. A portfolio that generates predictable cash flow from bond coupons can reduce the likelihood that a volatile equity market forces a sale at the worst possible time.

During the April 2025 tariff-related sell-off, ETF outflows were less than 0.3% of total assets, and investors under 40 were net buyers of A200 and VAS, according to the Australian Financial Review. A balanced 50/50 portfolio outperformed growth-heavy equivalents over certain trailing periods, offering context that defensive allocation is not always a pure return drag.

The simplest portfolio that works is usually the right one

The three structural lessons of this guide, low-cost core allocation, fee discipline, and diversification without duplication, converge on a single principle: the portfolio that a 30-something investor will actually maintain through volatility is worth more than the theoretically optimal one they will abandon.

The evidence from 2025 supports this. Across multiple volatility episodes, younger investors on Australian platforms were consistently net buyers of broad-market ETFs, not sellers.

The structural shift in Australian ETF allocation toward international equities is accelerating: in April 2026, international equity ETFs captured approximately $2.6 billion of the $5.2 billion in total industry net inflows, reflecting a sustained decline in the home bias that once kept most Australian retail portfolios concentrated in domestic shares.

According to Morningstar’s Annika Bradley, “set-and-forget ETF investors appear to be sticking to their plans,” with net flows to diversified and broad-market ETFs remaining positive across all major 2025 volatility episodes.

A 3-5 ETF portfolio represents the practical outer limit for most accumulation investors, per Canstar, Morningstar, and Livewire sources. For investors who genuinely prefer not to manage allocation themselves, a single all-in-one ETF such as DHHF or VDHG is a legitimate and complete solution.

The next step is a portfolio review that takes less than an hour:

- List current holdings and their fees. If any holding charges more than 0.30% p.a. for broad-market exposure, question whether it belongs in the core.

- Check for overlap in top-10 holdings. If the same companies appear across multiple funds, the portfolio is paying for duplication.

- Confirm the allocation split is deliberate. The ratio of Australian to global equities, and of growth to defensive assets, should reflect a conscious decision rather than the accumulated result of individual purchases made at different times.

The Australian ETP market, with over $230 billion in assets and more than 370 listed products, provides the infrastructure for any level of portfolio complexity. For most investors in their 30s, the best use of that infrastructure is the simplest one that meets their goals.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.