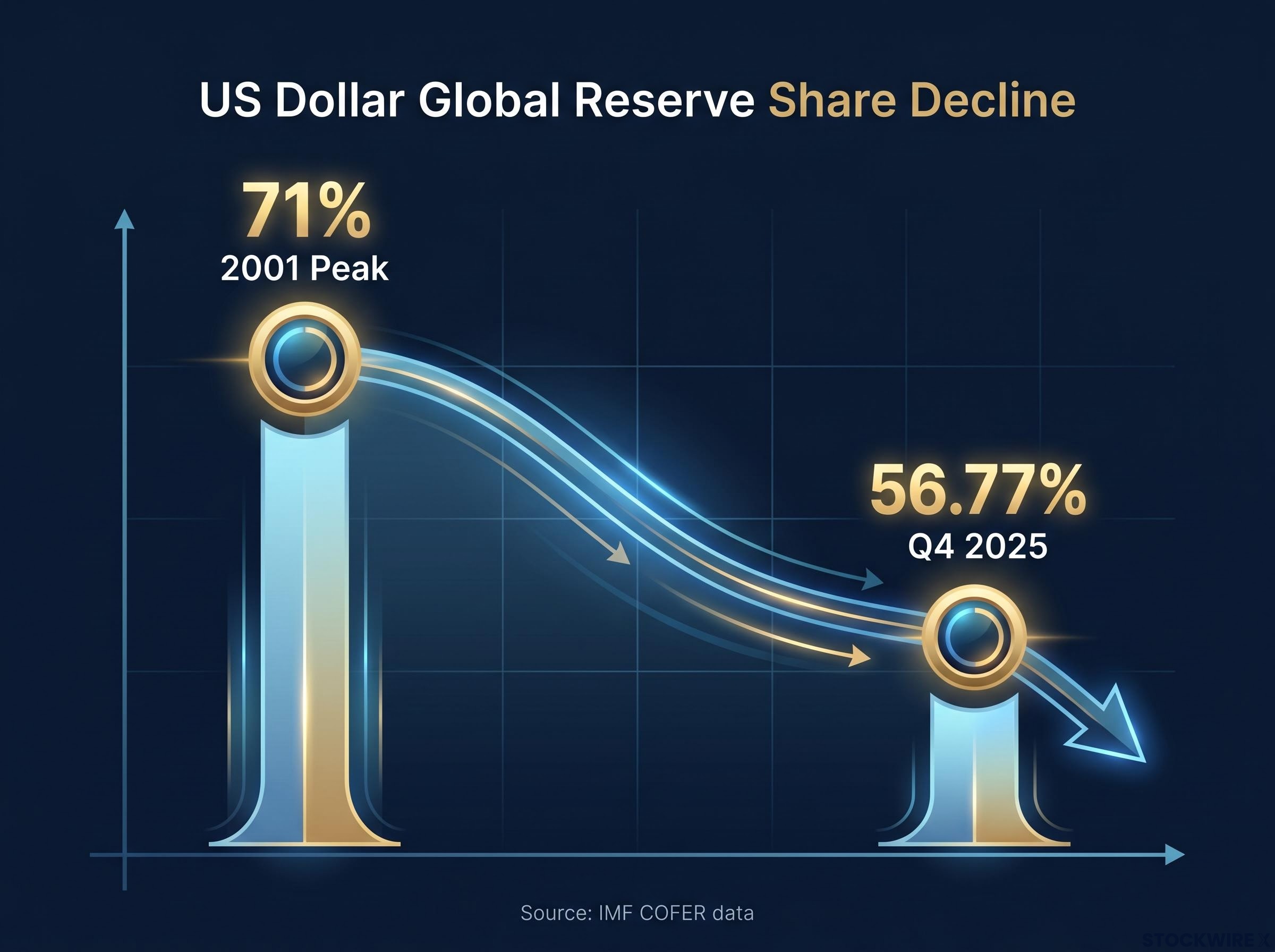

The US dollar’s share of global central-bank reserves has fallen from roughly 71% in 2001 to 56.77% in Q4 2025, according to IMF COFER data. This is not a forecast of collapse. It is a measured, multi-decade decline that shows no sign of reversing, and it is being actively accelerated by sovereign actors, including China’s 18-consecutive-month gold accumulation programme and multiple nations reducing their US Treasury holdings. For Australian investors, the implications are specific: heavy domestic concentration in assets correlated with US financial conditions creates a version of this risk that few have mapped. This guide covers the geopolitical forces behind the de-dollarisation trend, why Australian portfolios carry particular exposure, and the defensive strategies, including physical gold, Swiss franc holdings, and hard commodities, that some family offices are already deploying.

The slow retreat of the dollar from centre stage

The dollar’s decline as the world’s dominant reserve currency did not begin with a single event. It has unfolded across more than two decades, from a peak share of approximately 71% in 2001 to 56.77% as of Q4 2025, per the IMF’s Currency Composition of Official Foreign Exchange Reserves (COFER) database.

IMF COFER Data, Q4 2025: The US dollar’s share of allocated global central-bank reserves stood at 56.77%, continuing a multi-decade decline from its 2001 peak.

Three structural forces are driving this erosion:

- Central-bank diversification: Sovereign reserve managers across Asia, the Middle East, and Latin America have been steadily reallocating away from dollar-denominated assets, increasing holdings in euros, yuan, gold, and other currencies.

- Japan’s repatriation dynamics: Rising domestic interest rates in Japan are creating financial incentives to bring capital home, reducing one of the largest traditional sources of demand for US Treasuries.

- Yuan internationalisation: China is actively building a network of bilateral trade agreements settled in yuan, reducing the dollar’s role as the default medium for international commerce.

No specific collapse timeline exists. This is a tail-risk framing: low probability in any given year, high consequence if realised, and already shifting the behaviour of the world’s largest sovereign capital pools. The trend direction is what matters. It has been consistent for 25 years, and the pace of decline appears to be accelerating rather than stabilising.

The IMF COFER reserve composition data, published quarterly, provides the primary statistical basis for tracking this decline, recording the dollar’s share at 56.77% in Q4 2025 and offering sovereign wealth managers and retail investors alike a common benchmark for measuring how rapidly the trend is progressing.

When big ASX news breaks, our subscribers know first

What de-dollarisation actually means for a portfolio in Sydney or Melbourne

De-dollarisation, in plain terms, is the process by which the US dollar loses its role as the primary medium for international trade, reserve holdings, and commodity pricing. When that role erodes, the value of assets denominated in or correlated with the dollar comes under pressure, not just in the United States, but in every economy whose financial system is tightly linked to American markets.

For Australian investors, this linkage is direct. A significant downturn in US equities or the US housing market has historically produced corresponding declines in Australian equities and property values, reflecting the deep trade and financial connections between the two economies. The contagion mechanism does not require Australia to have its own crisis; it only requires the US to have one.

The four Australian asset categories most exposed to this contagion scenario are:

- Domestic equities, which tend to track US market downturns with a lag measured in days rather than weeks

- Residential property, where valuations are sensitive to shifts in global credit conditions and investor confidence

- AUD-denominated cash, which loses purchasing power if the Australian dollar weakens in sympathy with broader risk-off moves

- Concentrated brokerage infrastructure, where operational dependence on a single provider amplifies liquidity risk

The operational infrastructure risk most Australian investors overlook

Concentration risk extends beyond asset class diversification. It includes the operational infrastructure that underpins how investments are held and settled.

A meaningful share of Australian SMSFs and retail investors rely on Macquarie cash management accounts as their primary brokerage settlement infrastructure. Named data on Macquarie’s precise share of this market is not publicly confirmed, and no formal regulatory concern on record was identified in available research. The structural dependency, however, is worth understanding.

If a confidence event were to affect a single provider with this degree of penetration, the consequences would extend beyond what a typical institutional failure would imply. Liquidity access, settlement processing, and cash management for a disproportionate segment of Australian retail investors could be disrupted simultaneously.

This is not a prediction. It is an observation about concentration. Most Australian investors have diversified their asset classes but have not mapped the operational dependencies that sit underneath those assets.

Why China’s gold stockpile is the most watched number in global finance

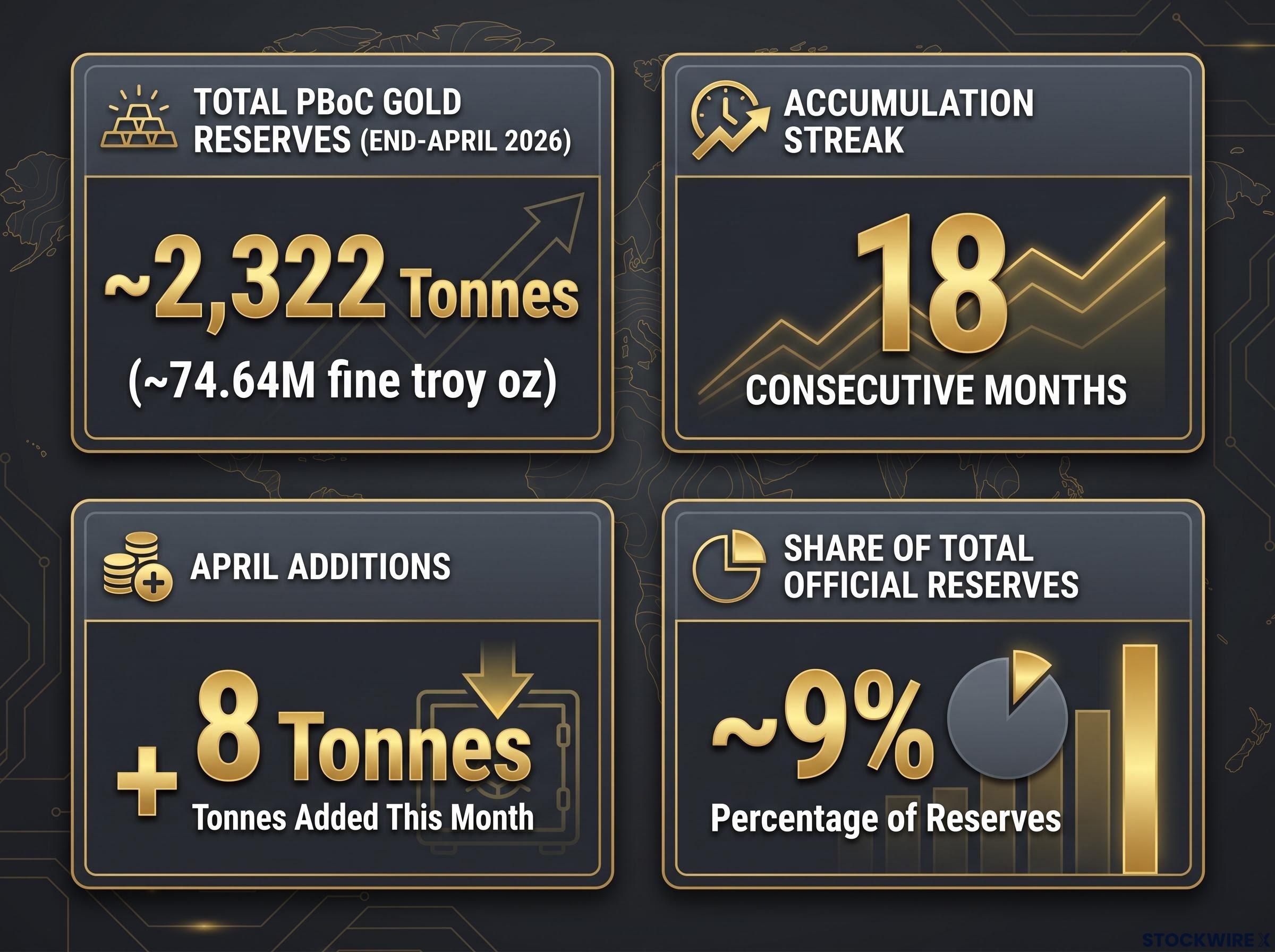

By end-April 2026, the People’s Bank of China held approximately 2,322 tonnes (roughly 74.64 million fine troy ounces) of gold, representing at least 18 consecutive months of purchases. Gold now comprises approximately 9% of China’s total official reserves, a figure that has climbed steadily as Beijing adds to its position month after month.

18 consecutive months. Through April 2026, the PBoC has purchased gold every single month for at least a year and a half, adding an estimated 8 tonnes in April alone.

The strategic logic is straightforward. China holds substantial US Treasury bond positions and faces potential losses if the US bond market deteriorates. Reducing dollar exposure while building a gold-backed credibility case for the yuan serves two objectives simultaneously: it hedges against dollar weakness and positions the yuan as a viable alternative reserve currency.

This financial accumulation has a diplomatic complement. China is actively recruiting nations into a yuan-transacting bloc, with Russia, Indonesia, India, and North Korea among those being drawn into bilateral trade arrangements settled outside the dollar system. The process of transitioning the yuan to reserve currency status is acknowledged as multi-year, but the monthly PBoC data confirms it is already underway.

| Metric | Figure | Source |

|---|---|---|

| PBoC gold reserves | ~2,322 tonnes (~74.64M fine troy ounces) | PBoC / State Administration of Foreign Exchange, end-April 2026 |

| Accumulation streak | At least 18 consecutive months | PBoC monthly reserve updates |

| Gold share of total reserves | ~9% | World Gold Council / PBoC data, 2026 |

| Nations in yuan bloc recruitment | Russia, Indonesia, India, North Korea | Widely reported in 2026 financial coverage |

China’s gold accumulation is not speculative commentary. It is reported monthly by the PBoC. Retail investors can observe the same data that sovereign wealth managers are watching, and draw their own conclusions about what sustained central-bank buying at this scale signals about the direction of global reserve composition.

Institutional price targets ranging from $5,400 to $6,350 per ounce reflect a broad consensus that sovereign gold demand, driven by central bank accumulation at a pace not seen in decades, has established a structural price floor that rate-differential models alone cannot explain.

Physical gold, Swiss francs, and Swiss property as defensive anchors

The strategies being deployed by family offices and high-net-worth investors share a common thread: they seek assets that sit outside the dollar-linked financial system and cannot be diluted by monetary policy.

Physical gold is the foundational position. It cannot be printed, it carries no counterparty risk when held directly, and it is particularly suited to capital preservation rather than income generation. The current price environment provides context for entry-point evaluation.

Gold price, June 2026: approximately US$4,300-4,500 per troy ounce, near record nominal levels after sustained appreciation across 2024-2026.

Gold at these levels reflects the cumulative effect of central-bank buying and reserve diversification. The price trajectory confirms that sovereign actors have been positioning ahead of retail investors on this theme.

Swiss franc exposure represents a second pillar. The franc’s safe-haven status is underpinned by Switzerland’s well-funded government and a long institutional tradition of fiscal discipline. At least one Australian family office has reportedly been converting holdings into Swiss francs and purchasing Swiss property as a protective measure, treating both as hard-currency alternatives to dollar-denominated assets.

Bitcoin is a supplementary consideration, not a primary one. The case rests on its fixed supply schedule, which means it cannot be artificially inflated. Its volatility profile and shorter track record, however, make it categorically different from gold or the Swiss franc as a defensive vehicle. It may warrant a small allocation for investors with appropriate risk tolerance, but it does not replace either of the primary hedges.

| Asset | Key Characteristic | Australian Access Method | Relevant Consideration |

|---|---|---|---|

| Physical gold | No counterparty risk; cannot be printed | ASX-listed bullion-backed ETFs (GOLD, QAU, NUGG, GLDN, PMGOLD) | Near record nominal price; suited to preservation, not income |

| Swiss franc | Safe-haven currency; well-funded sovereign backing | International broker platforms; currency ETFs | Limited direct ASX access; may require offshore accounts |

| Swiss property | Hard asset in hard-currency jurisdiction | Direct purchase (requires international legal and tax advice) | Illiquid; high entry cost; suited to high-net-worth investors |

| Bitcoin (supplementary) | Fixed supply; cannot be inflated | Australian crypto exchanges; ASX-listed crypto ETPs | High volatility; shorter track record; not a primary hedge |

Understanding why specific asset classes are being chosen, and not just that they are being chosen, allows Australian investors to evaluate whether the underlying logic applies to their own risk tolerance and time horizon.

How Australian retail investors can actually access these strategies

The most accessible entry point for Australian investors is physical gold through ASX-listed, bullion-backed exchange-traded products. Five confirmed options are currently available:

Australian access to gold, currency, and commodity strategies has been transformed by the growth of exchange-traded products: as of end-2025, 2.69 million Australians held ETFs representing $330.6 billion in funds under management, giving retail investors and SMSF trustees direct access to asset classes that previously required institutional-scale capital or offshore brokerage arrangements.

- GOLD (Global X Physical Gold ETF)

- PMGOLD (Perth Mint Gold)

- QAU (BetaShares Gold Bullion ETF)

- NUGG (VanEck Gold Bullion ETF)

- GLDN (iShares Physical Gold ETF)

Each of these is backed by physical gold bullion, which distinguishes them from gold-mining equities. Mining stocks carry operational, jurisdictional, and management risk that means they do not replicate bullion price performance directly. Investors seeking a pure hedge against dollar weakness should understand this distinction before allocating.

Beyond the five bullion-backed products listed above, ASX commodity ETFs covering mining equities and platinum have delivered 85% to 132% returns over the past 12 months, though investors should understand that mining equity ETFs embed operational leverage, meaning they can fall harder than the underlying commodity if gold prices plateau or cost inflation compresses margins.

Swiss franc and commodity exposure: what to look for

Accessing Swiss franc exposure from an Australian brokerage account is more complex. Specific CHF-exposure products on the ASX were not confirmed in available research, meaning investors seeking direct Swiss franc positions may need to explore:

- International broker platforms that offer currency trading or foreign-denominated accounts

- Currency ETFs listed on US or European exchanges, which introduces foreign exchange conversion costs and additional complexity

- Consultation with a financial adviser to assess whether offshore currency positions are compatible with superannuation or SMSF structures

Hard commodities represent a third diversification category. Dollar-priced commodities such as copper tend to appreciate in nominal terms when the dollar weakens, providing a natural hedge for investors positioned in these assets. ASX-listed commodity ETFs tracking copper or broader commodity indices offer the most accessible route for retail investors not in a position to hold physical commodities. Specific product names should be verified against current ASX listings, as product availability changes over time.

The honest disclosure is worth repeating: Swiss franc and commodity ETF product availability on the ASX was not confirmed in current research. Investors should verify specific product options through their broker or financial adviser before acting.

Building a portfolio that can survive a scenario most Australians are not positioned for

The appropriate response to a low-probability, high-impact scenario is not to restructure an entire portfolio. It is to ensure some meaningful allocation to assets that are genuinely uncorrelated with the dollar-linked system.

Tail-risk positioning is about proportionate preparation, not prediction. The goal is not to bet on a dollar collapse. It is to ensure that if one occurs, the portfolio is not entirely exposed.

A practical starting hierarchy:

- Audit existing gold exposure and consider allocating to one or more ASX-listed bullion-backed ETFs (GOLD, QAU, NUGG, GLDN, or PMGOLD) if current holdings are limited or absent.

- Investigate Swiss franc or hard-currency diversification channels, recognising that direct ASX access is limited and may require an international brokerage arrangement.

- Map brokerage and cash management concentration risk, particularly if a single provider handles settlement, cash management, and trading activity across multiple accounts.

Investors converting Australian dollar holdings into Swiss francs or hard commodities should map the current AUD/USD technical resistance levels before initiating currency conversion: the pair is pinned below 0.7280 resistance with 0.7160 as near-term support, and a break of that level reopens downside toward the 50-day moving average near 0.7040, which would alter the effective cost of acquiring offshore assets denominated in US dollars or Swiss francs.

A complementary measure: reducing exposure to high-debt and speculative leveraged positions. Leverage amplifies downside in any stress scenario, and reducing it is a risk-management step that costs little in the current environment.

The IMF COFER data shows the dollar at 56.77% of global reserves and falling. Family offices are already acting on these themes. The strategies outlined above provide a framework for Australian retail investors and SMSF trustees to evaluate whether proportionate defensive action fits within their own risk profile.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements are speculative and subject to change based on market developments and geopolitical conditions. Past performance does not guarantee future results.

The dollar’s retreat is already underway. The question is when Australian portfolios catch up.

The de-dollarisation trend is not speculative. It is measurable in IMF reserve data published quarterly and PBoC gold reserve reports published monthly. The only genuine uncertainty is pace and severity.

That uncertainty is precisely why proportionate hedging is more rational than either full portfolio repositioning or complete inaction. The cost of holding a measured allocation to gold, hard currencies, and uncorrelated assets is modest. The cost of having no exposure at all, in the scenario where the trend accelerates, could be substantial.

As central banks continue accumulating gold and reducing dollar exposure, the defensive strategies outlined here are likely to move from niche family office behaviour toward mainstream portfolio consideration. The shift has been underway for 25 years. The question for Australian investors is not whether the trend is real, but whether their portfolios reflect it.

A practical first step: review current gold and currency exposure, map brokerage concentration, and consult a financial adviser about how tail-risk positioning fits within an overall strategy and risk profile.

—