How Wesfarmers Buys, Builds, and Exits to Create Value

2 hrs ago

Australians hold billions in savings accounts earning headline rates of up to 5.90% per annum, and it is easy to see why the number feels reassuring. But the most recent ABS data, published 27 May 2026, shows annual inflation running at 4.2% for the year to April 2026. That gap between what savers think they are earning and what their money can actually buy is far narrower than most people realise, and it narrows further once tax enters the equation.

With the Reserve Bank of Australia raising the cash rate to 4.35% on 6 May 2026 and inflation still well above the 2-3% target band, the tension between nominal interest and real purchasing power has become one of the most practically important personal finance questions in the country. Most savings account marketing focuses on the headline rate. This article focuses on what that rate actually delivers: how much purchasing power Australian cash savings are gaining (or losing) in real terms, why the brain makes this easy to overlook, and what the numbers look like once the Australian Tax Office takes its share.

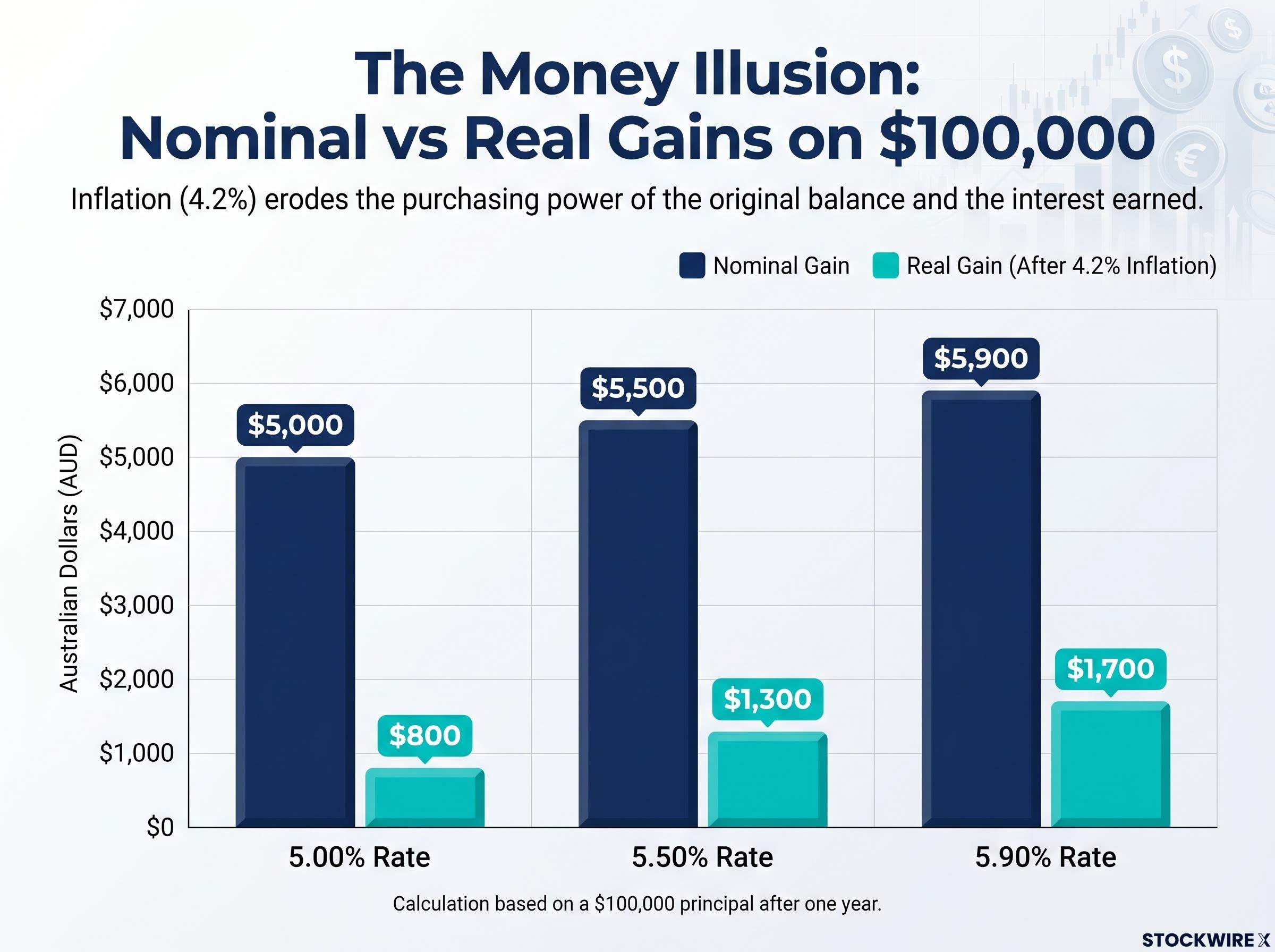

Start with the number most savers trust: the headline rate. A savings account paying 5.00% on $100,000 generates $5,000 in nominal interest over a year. That figure appears in the account balance. It is real money. And it is almost entirely misleading.

Inflation, measured by the ABS at 4.2% for the year to April 2026, erodes the purchasing power of both the original balance and the interest earned. After adjusting for that erosion, the actual gain in what the money can buy is approximately $800 per year, not $5,000.

The 4.2% figure comes from the ABS monthly CPI indicator, which tracks a basket of goods and services weighted to reflect typical household spending; how CPI is calculated, and why the trimmed mean and the headline rate can diverge by more than a full percentage point, determines whether any given savings rate is truly outpacing the prices a specific household actually faces.

The ABS Consumer Price Index release for the year to April 2026 confirmed annual inflation at 4.2%, the official benchmark that underpins every real-return calculation in this article and the figure savers should use when assessing whether their current savings rate is keeping pace with rising prices.

On $100,000 at 5.00% nominal, the real purchasing power gain after 4.2% inflation is roughly $800 per year. The other $4,200 simply keeps pace with rising prices.

The arithmetic is not complicated. Subtract the inflation rate from the nominal interest rate to get a rough real return. At 5.00% minus 4.2%, that real return is 0.8%. At 5.50%, it rises to 1.3%, producing approximately $1,300 in real gain on $100,000 before tax, according to Canstar analysis from February 2026. Even at 5.90%, the top of the current market, the real gain is $1,700 before tax.

| Nominal rate | Inflation rate | Nominal gain on $100,000 | Real gain on $100,000 |

|---|---|---|---|

| 5.00% | 4.2% | $5,000 | $800 |

| 5.50% | 4.2% | $5,500 | $1,300 |

| 5.90% | 4.2% | $5,900 | $1,700 |

That table is the single most important reference point for evaluating any savings account. Without it, every comparison based on headline rates is comparing the wrong number.

If the arithmetic is this straightforward, why do so many savers overlook it? The answer sits in two well-documented psychological forces that quietly shape how people think about money:

The share market drop is visible in real time on a screen. Inflation’s damage is felt only gradually, at the checkout, at the petrol pump, in the rent bill. The brain treats these two forms of financial loss as fundamentally different events, even when the dollar impact is equivalent. Recognising this is not about self-criticism. It is about understanding why the instinct to stay in cash, while natural, is systematically incomplete as a financial strategy.

The real cost of cash hoarding is documented across two decades of Australian asset class returns: over 20 years, residential property delivered 9.16% annualised returns and Australian shares returned 7.55%, while cash produced a negative real return after inflation, a finding that frames the current high-rate environment as an exception rather than a structural argument for staying in savings accounts indefinitely.

The pattern is not hypothetical. An RBA Bulletin paper from September 2024 found that Australian households built large cash buffers during COVID and were slow to draw them down even as real deposit rates turned negative. The paper cited precautionary saving motives and loss aversion as contributing explanations.

The Grattan Institute, in an April 2024 analysis, made the connection explicit: households prefer “a guaranteed small gain in nominal terms” over a “risky but higher expected payoff,” linking this directly to Kahneman and Tversky’s prospect theory.

An AustralianSuper research note from July 2025 found that a significant proportion of pre-retiree members held high cash allocations driven by “fear of market volatility and a strong desire to avoid seeing balances fall.” These were not unsophisticated savers. Many held substantial balances. The behaviour was widespread across income levels.

The good news is that the top of the Australian savings market is genuinely competitive. Rabobank leads with a promotional rate of 5.90% per annum for new customers on balances up to $250,000, and UBank offers 5.85% on an introductory or bonus basis. ING’s Savings Maximiser pays 5.50% for customers who meet monthly deposit, balance growth, and transaction conditions. Macquarie offers approximately 5.35% with no monthly conditions attached, making it the strongest unconditional rate in the market.

These are real rates, available now, and they produce meaningful nominal interest.

| Institution | Account | Rate | Conditions | Reverts to |

|---|---|---|---|---|

| Rabobank | High Interest Savings | 5.90% | New customers, up to $250k, 4-month promo | 4.00% |

| UBank | Save Account | 5.85% | Introductory/bonus; $200/month deposit, withdrawal limits | 5.10% (ongoing conditional) |

| ING | Savings Maximiser | 5.50% | $1,000/month deposit, balance growth, 5+ card transactions | Base rate (lower) |

| Macquarie | Savings Account | ~5.35% | None | N/A (ongoing variable) |

| ANZ | Plus Save | ~4.90% | None | N/A (ongoing variable) |

| CBA/Westpac/NAB | Bonus savings accounts | 4.50-4.65% | Monthly deposit, no withdrawals | Base rate (lower) |

The problem is that most savers are not earning these rates. The big four trail market leaders by 60-140 basis points on their best conditional products. Many customers at the major banks sit on older legacy rates well below even the advertised maximum, as the Australian Financial Review reported in November 2025.

As ABC News reported in January 2026: “On average transaction and savings accounts, households are still earning less than inflation.”

For savers on legacy rates of 3.5% or 4.0%, the real return calculation is not a story of thin margins. It is a story of outright purchasing power loss.

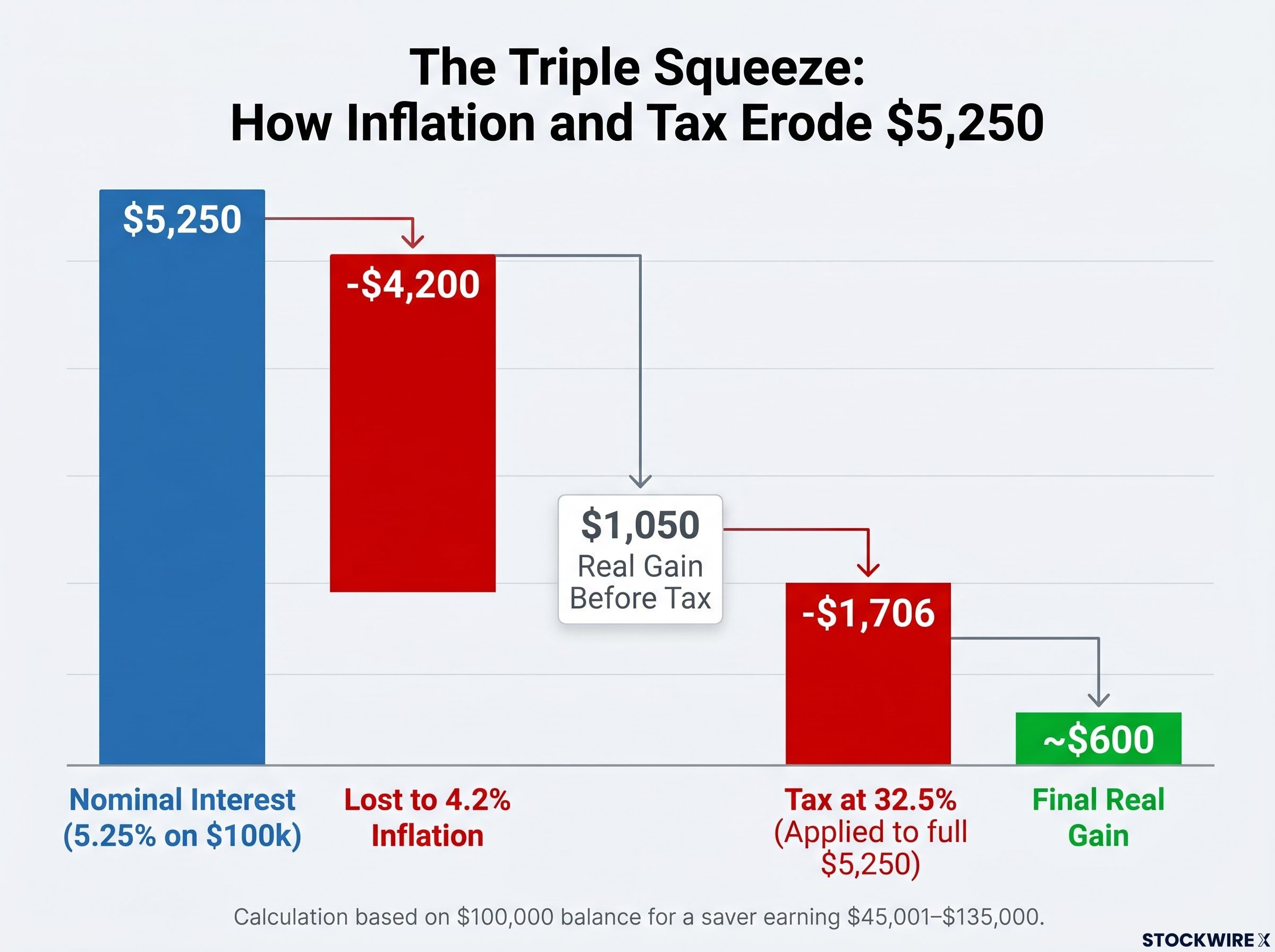

Even where a saver has secured a competitive rate, there is a second layer of erosion. Savings account interest is taxed as ordinary income in Australia, at the saver’s marginal rate. For someone earning between $45,001 and $135,000, a bracket covering a large proportion of full-time workers, that marginal rate is 32.5% (plus the 2% Medicare levy).

The calculation works in three steps:

According to AFR analysis from February 2026, that $600 figure is the honest return for a saver in this tax bracket earning a rate slightly above the current top-market average. Steve Mickenbecker, Canstar Group Executive, put it plainly: at 5.5% nominal with inflation around 4%, “some people will see their real return vanish” after tax.

Sally Tindall, RateCity Research Director, noted that the “sliver of real return” at 5% versus 4.2% inflation “can quickly disappear after tax, especially for higher-income savers.”

The tax system does not distinguish between nominal interest and real interest. It taxes the whole figure. That mechanical fact turns a marginal real gain into something close to zero for many Australians.

The annual figures above capture a single year’s erosion. The picture changes materially when viewed across a realistic savings horizon, because inflation’s effect on purchasing power compounds.

The RBA’s current outlook, set out in the May 2026 Statement on Monetary Policy, expects inflation to have peaked around mid-2026 before easing gradually. But the central forecast has inflation remaining above the 2-3% target band for some time. This is not a problem confined to a single quarter.

The RBA’s May 2026 monetary policy decision confirmed the cash rate increase to 4.35% and noted that inflation had picked up in the second half of 2025, with the Board’s updated forecasts anticipating a gradual easing from mid-2026 but no near-term return to the 2-3% target band.

The headline CPI figure of 4.2% is itself only part of the story; trimmed mean inflation rose to 3.4% in April 2026, above the RBA’s 2-3% target band and trending upward since its trough in June 2025, suggesting the underlying price pressures relevant to a saver’s long-run real return calculation are not easing as quickly as the headline suggests.

Consider $100,000 held in a savings account at 5.00% nominal for three years, against sustained average inflation of 4.00%. Over that period, the account generates approximately $15,000 in cumulative nominal interest. The saver sees the balance approach $115,000 and feels wealthier.

But after adjusting for compounding inflation at 4% over three years, the real purchasing power gain is closer to $3,000 before tax. The remaining $12,000 in nominal interest simply offsets the rising cost of goods and services. The RBA Bulletin’s September 2024 finding is relevant here: households were slow to draw down COVID-era cash buffers despite real erosion, underscoring how inertia compounds the cost of staying in cash over multiple years.

These are illustrative figures, not precise forecasts; actual inflation will vary. But they make visible a cost that annual snapshots tend to hide.

None of this is an argument against holding cash. Emergency funds, short-term savings goals, and capital stability are legitimate purposes that a savings account serves well. The argument is narrower: most savers misread what cash is doing for them, and that misread has a dollar cost.

The risk-return tradeoff across asset classes looks different in 2026 than at almost any point in the last decade: high-interest savings accounts paying up to 5.65% have unusually compressed the traditional return premium of shares over cash, narrowing but not eliminating the long-run case for holding growth assets alongside a cash buffer.

Closing the gap starts with three steps:

MoneySmart, the Australian Government’s financial guidance service, advises savers to “consider inflation when comparing returns on savings and investments.”

The arithmetic in this article is not complex. The gap between nominal and real returns is something any saver can calculate in under a minute, once they know to look for it.

Even at the top of the market, Australian savers are earning real returns measured in hundreds of dollars per year on $100,000, not thousands. Once tax is applied at the 32.5% marginal rate, the real gain can shrink to roughly $600 or less. For savers on legacy rates at the major banks, the real return is likely negative.

Cash savings are not a poor financial tool. But they are a tool being systematically misread by most people who hold them, and that misread has a measurable dollar cost. Knowing the actual rate, checking it against the best available market rate, and running the real-return arithmetic with the current 4.2% CPI figure are the three actions most likely to close the gap between what savers believe they are earning and what their money can actually buy.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. The calculations presented are illustrative and subject to change based on prevailing inflation rates, interest rates, and individual tax circumstances.

At a nominal rate of 5.00% and annual inflation of 4.2% (as of April 2026), the real purchasing power gain on $100,000 is approximately $800 per year. Even at the top market rate of 5.90%, the real gain before tax is only around $1,700.

Savings account interest is taxed as ordinary income in Australia. For someone on the 32.5% marginal tax bracket, a nominal interest payment of $5,250 on $100,000 is reduced by approximately $1,706 in tax, leaving a real after-inflation, after-tax gain of roughly $600 per year.

As of 2026, Rabobank leads with a promotional rate of 5.90% for new customers on balances up to $250,000 (reverting to 4.00% after four months), followed by UBank at 5.85% and Macquarie at approximately 5.35% with no monthly conditions attached.

Subtract the current CPI figure from your savings account rate to estimate your real return. With inflation at 4.2% as of April 2026, a rate of 5.00% produces a real return of approximately 0.8%, or around $800 per year on $100,000 before tax.

Research from the RBA and the Grattan Institute points to money illusion and loss aversion as key factors. People focus on the rising nominal balance in their account rather than what that balance can actually buy, making inflation's gradual erosion of purchasing power easy to overlook.