How Wesfarmers Buys, Builds, and Exits to Create Value

3 hrs ago

The Canada Strong Fund, unveiled alongside the Spring Economic Update on 28 April 2026, commits $25 billion in federal seed capital over three years to a new Crown corporation designed to take equity stakes across six domestic sectors, while giving individual Canadians the option to invest directly alongside the government. Yet as of 12 May 2026, no enabling legislation has been tabled, no chief executive has been named, and the fund’s retail investment terms remain entirely undefined. Prime Minister Mark Carney has framed the vehicle as a generational institution for national wealth-building. Whether that framing holds depends on three tests this article works through: whether the fund is necessary, whether it can remain politically independent, and whether Canada’s fiscal position gives it enough room to succeed.

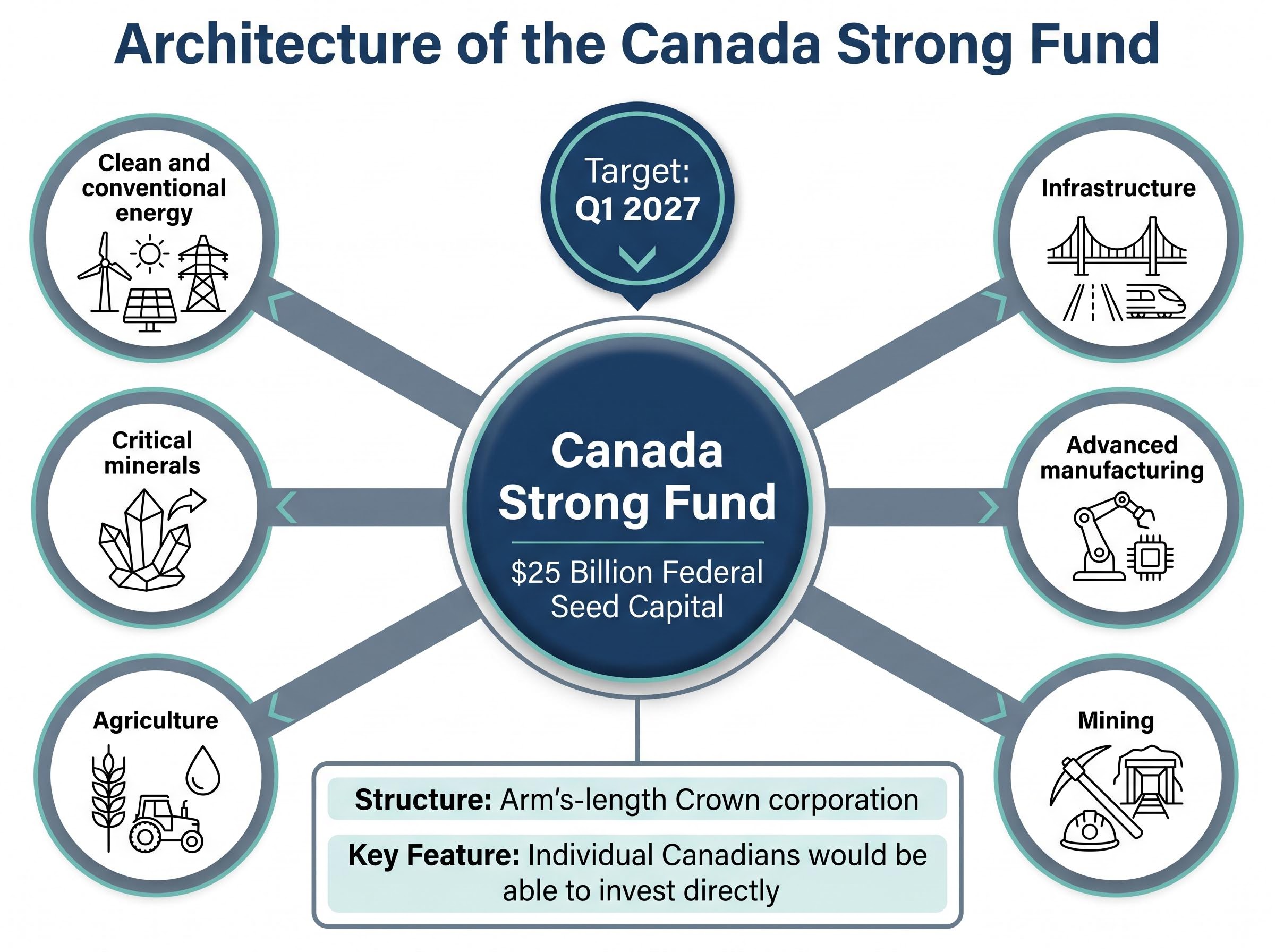

The fund’s architecture marks a deliberate departure from Canada’s existing federal investment vehicles. Structured as a new arm’s-length Crown corporation reporting to the Minister of Finance, with an independently appointed chief executive and board, the Canada Strong Fund is designed to take equity ownership stakes in domestic projects rather than provide loans or guarantees. That distinction is structural, not semantic; equity ownership means the fund retains upside in the assets it backs, and it bears downside risk alongside private co-investors.

The fund carries a dual mandate: generate commercial returns for public benefit while advancing domestic economic development, spanning jobs, innovation, and strategic industry capacity.

The $25 billion federal seed contribution represents approximately 1.4% of annual federal expenditure and under 1% of Canada’s GDP. Target sectors include:

The fund’s most distinctive feature is its retail participation component. Individual Canadians would be able to invest directly alongside government and institutional capital, a structure absent from every major sovereign wealth fund currently operating. A Transition Office has been announced to finalise governance, mandate, and retail product design, with operationalisation targeted for Q1 2027.

Three federal investment vehicles now sit on the landscape, and conflating them produces a misreading of both the new fund’s ambitions and its risks. The distinctions are structural.

The Canada Infrastructure Bank (CIB) provides loans and equity for infrastructure projects. As of 2025, it had deployed approximately 20% of its $35 billion mandate, a deployment pace that drew enough criticism for the House of Commons Standing Committee on Transportation, Infrastructure, and Communities to recommend dissolving the CIB in 2022. The Canada Growth Fund targets private capital mobilisation for decarbonisation, with a narrower sectoral lens and no retail access.

No existing Canadian federal entity combines equity ownership across multiple sectors, a commercial return mandate, and direct retail investor participation in the same structure. That combination is what makes the Canada Strong Fund genuinely new, and it is also what makes its execution risk genuinely untested.

| Fund | Structure | Investment Approach | Retail Access |

|---|---|---|---|

| Canada Strong Fund | Arm’s-length Crown corporation | Equity ownership across six sectors | Yes (planned) |

| Canada Infrastructure Bank | Crown corporation | Loans and equity for infrastructure | No |

| Canada Growth Fund | Federal investment vehicle | Private capital mobilisation for decarbonisation | No |

Understanding what a mature sovereign wealth fund looks like in practice is the necessary precondition for evaluating what Canada is proposing.

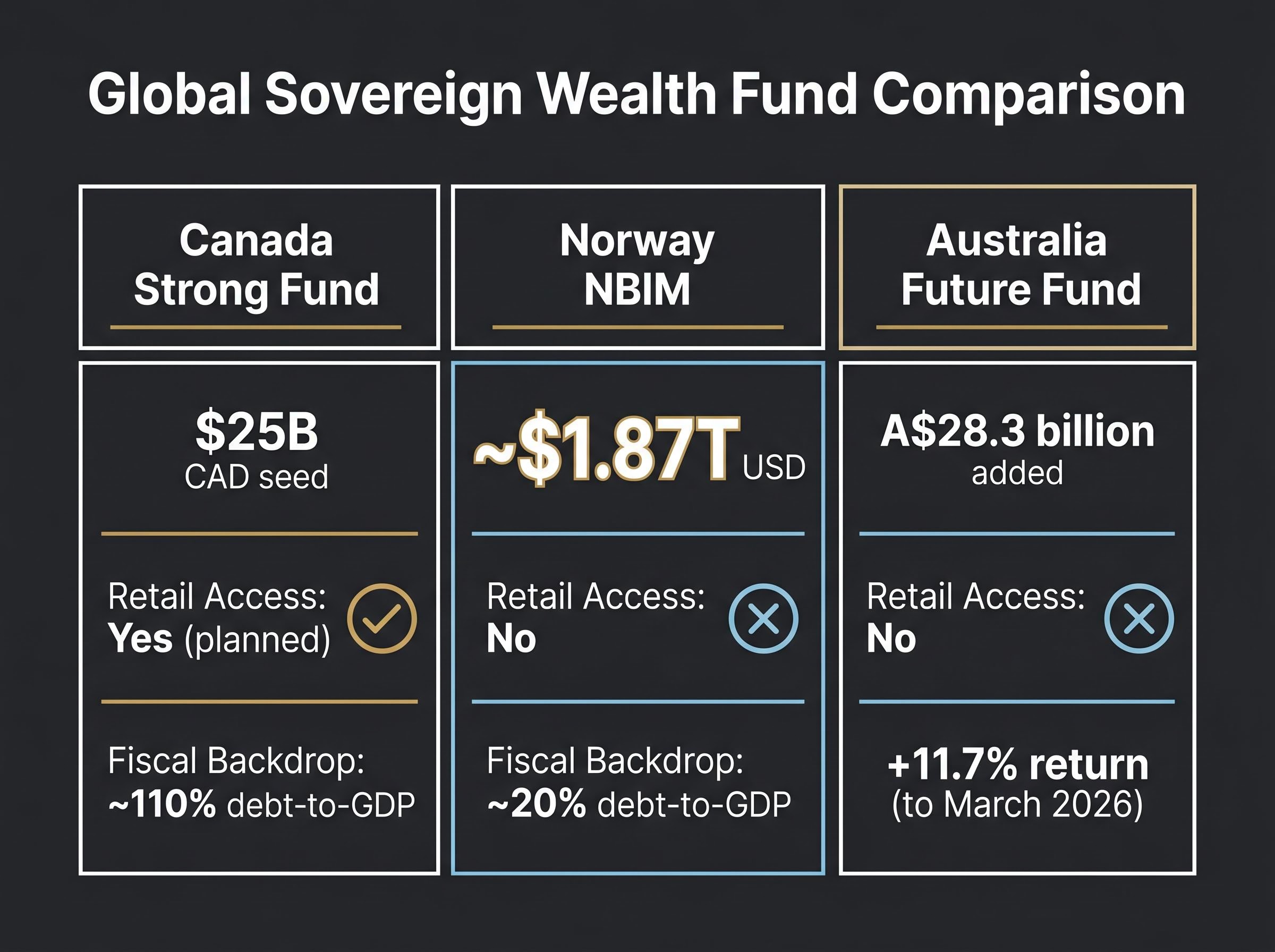

Norway’s NBIM manages approximately $1.87 trillion USD and covers up to 25% of annual government expenditure. It invests globally, not domestically, and was seeded by government-owned oil production revenue, a mechanism unavailable to Canada given its privately owned oil sector and provincially accruing royalties. Norway’s fiscal backdrop is approximately 20% debt-to-GDP. The Australia Future Fund returned +11.7% for the 12 months to March 2026, adding A$28.3 billion, with five-year growth exceeding A$96 billion. It is purely government-owned, with no retail component.

NBIM’s Q1 2026 key figures confirm the fund’s scale and global diversification, providing the most direct benchmark against which Canada’s domestically concentrated, deficit-seeded proposal must be measured.

FT Alphaville characterised Canada’s timing as “Ambitious but late, Canada’s debt-to-GDP lags Norway’s ~20%.”

Canada is not alone in launching sovereign wealth vehicles during 2025-2026. Indonesia’s Danantara launched with a $20 billion seed in January 2026. Brazil expanded its PNB fund to over $100 billion with an energy focus. India is considering a $10 billion vehicle. Global sovereign wealth fund assets grew approximately 8% year-over-year to $12 trillion, according to the International Forum of Sovereign Wealth Funds (IFSWF, May 2026).

Canada’s proposed fund is smaller than its peers and uniquely structured with its retail participation feature. The structural gap that matters most, however, is fiscal. Canada’s 10-year Treasury yield sits at approximately 3.5%, against a 10-year average sovereign wealth fund return of approximately 6.3%. That 2.8 percentage point spread is the margin within which a deficit-funded sovereign wealth fund must justify its existence.

| Fund | AUM / Seed Capital | Retail Access | Investment Focus | Fiscal Backdrop |

|---|---|---|---|---|

| Canada Strong Fund | $25B CAD (seed) | Yes (planned) | Domestic (energy, minerals, infrastructure) | ~110% debt-to-GDP |

| Norway NBIM | ~$1.87T USD | No | Global (equities, bonds, real estate) | ~20% debt-to-GDP |

| Australia Future Fund | A$28.3B added in 12 months | No | Mixed (domestic and global) | Moderate |

The fund’s credibility rests on three tests. Each reveals a different layer of structural challenge, and together they produce a calibrated assessment rather than a binary verdict.

The fund’s $25 billion seed is deficit-financed. Canada’s projected federal deficit for FY 2025-26 stands at $67 billion (approximately 2.1% of GDP), and general government debt-to-GDP exceeds 110%. The arithmetic is straightforward: the government borrows at approximately 3.5% (10-year Treasury yield) and needs the fund to return more than that to create net value.

The limitations of debt-to-GDP as a fiscal metric are relevant here: the ratio compares a stock of accumulated obligations to an annual flow of economic output rather than to government revenue, and international precedent shows Japan has sustained debt above 200% of GDP and Canada itself above 113% without sovereign crises, which is why credit agencies focus on interest-to-revenue ratios and yield dynamics rather than the headline number alone.

The 10-year average sovereign wealth fund return of approximately 6.3% suggests the spread is achievable, but that global average reflects diversified portfolios investing across geographies. A domestically concentrated fund operating in a single national economy carries different risk characteristics.

One partial reassurance: no credit rating agency has issued downgrades or negative watches in connection with the fund as of May 2026. S&P, Moody’s, and DBRS all maintain Canada’s AAA rating with stable outlooks.

The case for necessity is grounded in a genuine productivity crisis. Canada ranks last in the G7 for investment in machinery, equipment, and intellectual property. Business investment per Canadian worker declined from 2014 to 2025. The Major Projects Office pipeline carries over $126 billion in referred projects, signalling a demand for coordinated federal capital deployment.

The counter-argument is institutional overlap. Multiple Crown corporations already operate in adjacent spaces, and the CIB’s 20% deployment rate raises the question of whether a new vehicle is needed or whether existing ones need better execution. The C.D. Howe Institute’s 29 April 2026 analysis raised precisely this point, citing CIB underperformance as a cautionary precedent.

Alberta’s Heritage Savings Trust Fund provides the most relevant Canadian precedent. The fund’s balance remained flat from 2007 to 2017 despite a 10-year investment return of 7.7%, because the provincial government withdrew earnings to cover budget shortfalls. The lesson is direct: arm’s-length governance structures protect against political capture only if governments respect them under fiscal pressure.

The Canada Strong Fund’s design includes an independently appointed board and CEO. Prime Minister Carney’s own background (a blind trust arrangement and prior Brookfield Asset Management affiliation) has drawn scrutiny from opposition parties. Conservative Leader Pierre Poilievre labelled it “a $25B slush fund for Liberal cronies” in the House of Commons on 6 May 2026. Whether the governance structure can withstand that level of political pressure over a multi-decade horizon is an open question.

Design intentions are one dimension of evaluation. Canada’s track record with major federal projects is another, and the numbers speak plainly.

The Trans Mountain Pipeline expansion is the primary case study. The federal government acquired the pipeline from Kinder Morgan for CAD $4.5 billion in 2018. By 2024, the total expansion cost had reached approximately CAD $34 billion, roughly six times the original estimate. BlackRock Canada cited Trans Mountain directly in a May 2026 note as precedent for caution on the new fund’s execution risk.

BlackRock Canada (May 2026) flagged execution risk as a material concern, citing historical Canadian mega-project cost overruns including Trans Mountain.

The connection to the Canada Strong Fund is structural, not merely anecdotal. A globally diversified fund can absorb project-level failures across geographies and sectors. A domestically concentrated fund with equity stakes in Canadian infrastructure projects cannot offset underperformance the same way. Every cost overrun compresses returns directly.

Mining capex overruns follow a recognisable pattern: Wood Mackenzie estimates that cost blowouts of 40-50% are typical for critical minerals projects, meaning the Canada Strong Fund’s exposure to a tungsten mine, an LNG terminal, and an EV battery plant carries sector-wide structural risk that project-level due diligence cannot fully eliminate.

The Major Projects Office pipeline provides a concrete picture of what the fund might actually invest in. Of 15 referred projects (6 in active development), 4 target Final Investment Decisions by end-2026, and 3 have been identified as potential Canada Strong Fund candidates:

The MPO’s 2-year maximum regulatory timeline is the structural reform that must succeed for the fund’s investment thesis to hold. Canada’s commercial construction sector also carries moderate-to-high corruption and organised crime risk, an additional variable that project-level due diligence will need to address.

The retail participation component is what makes this fund genuinely different from its global peers. It is also the least defined element of the entire proposal.

Infrastructure investments typically operate on timelines of a decade or more. Retail investors generally expect meaningfully higher liquidity than that. In the United States, retail-accessible private market funds have imposed withdrawal restrictions during periods of high redemptions, a precedent that illustrates the structural tension between illiquid assets and retail access.

Many Canadians already hold disproportionate domestic exposure in their portfolios. Additional allocation to a Canada-only fund compounds concentration risk, a consideration that the fund’s design does not currently address.

As of 12 May 2026, the following terms remain entirely undefined:

Bloomberg polling from May 2026 showed approximately 60% positive sentiment on the fund’s strategic direction. Sentiment, however, does not substitute for defined terms.

For Canadians who are weighing the retail participation component but are uncertain how an equity-based government fund fits within a broader personal portfolio, our dedicated guide to investment vehicles and risk profiles covers how to match account wrappers, fee structures, and concentration risk considerations to different financial goals, including the specific impact of tax-advantaged account eligibility on long-term net returns.

The Indigenous participation gap adds a governance dimension with both ethical and practical implications. Assembly of First Nations National Chief Cindy Woodhouse Nepinak stated on 29 April 2026 that “No First Nations distinctions-based funding” has been committed. The NDP called for explicit Indigenous allocations, but official fund documents have not addressed the issue. For projects requiring community support for regulatory approvals, particularly in mining and energy, this gap carries practical consequences beyond governance optics.

The Canada Strong Fund addresses a real problem. Canada’s productivity crisis, its last-place G7 ranking in business investment per worker, and the absence of a federal vehicle combining equity ownership with retail participation all constitute a legitimate case for institutional innovation.

What remains unresolved as of May 2026 is substantial: no legislation, no chief executive, no retail terms, no Indigenous allocation commitment, and a fiscal backdrop that provides meaningfully less margin for error than Norway or Australia enjoyed at equivalent fund launch stages. The CIB’s deployment record and Trans Mountain’s cost trajectory are not arguments against the fund’s existence, but they are evidence that ambition and execution have diverged before in this specific institutional context.

The Fall 2026 Economic Statement and the Q1 2027 operationalisation target are the next meaningful information checkpoints. Until legislation is tabled, governance is formalised, and retail terms are defined, the Canada Strong Fund remains a policy commitment with considerable structural questions outstanding.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Forward-looking statements regarding the fund’s returns, timeline, and operational structure are subject to change based on legislative developments, market conditions, and government policy decisions.

—

The Canada Strong Fund is a proposed Canadian federal Crown corporation announced on 28 April 2026, seeded with $25 billion in government capital over three years to take equity stakes in six domestic sectors including clean energy, critical minerals, agriculture, infrastructure, advanced manufacturing, and mining. It is uniquely structured to allow individual Canadians to invest directly alongside government and institutional capital.

The Canada Infrastructure Bank primarily provides loans and equity for infrastructure projects and has no retail investor access, while the Canada Strong Fund is designed to take equity ownership stakes across six sectors and will offer a direct retail participation component. No existing Canadian federal entity combines equity ownership across multiple sectors, a commercial return mandate, and direct retail investor participation in the same structure.

As of 12 May 2026, retail investors do not yet know whether principal guarantees will apply, what the tax treatment will be (including TFSA or RRSP eligibility), how long capital must remain committed, or what withdrawal restrictions may apply during periods of market stress. These terms are expected to be defined ahead of the Q1 2027 operationalisation target.

Canada is launching the fund with general government debt-to-GDP exceeding 110% and a projected federal deficit of approximately $67 billion for FY 2025-26, whereas Norway launched its sovereign wealth fund from a fiscal backdrop of approximately 20% debt-to-GDP. This means Canada's fund must generate returns exceeding its borrowing cost of roughly 3.5% (10-year Treasury yield) to create net value for taxpayers.

Alberta's Heritage Savings Trust Fund saw its balance remain flat from 2007 to 2017 despite a 10-year investment return of 7.7%, because the provincial government withdrew earnings to cover budget shortfalls. This precedent illustrates that arm's-length governance structures only protect a sovereign fund from political interference if governments consistently respect them under fiscal pressure.