Why a Rising AUD Is Quietly Eroding Your International ETF Returns

3 hrs ago

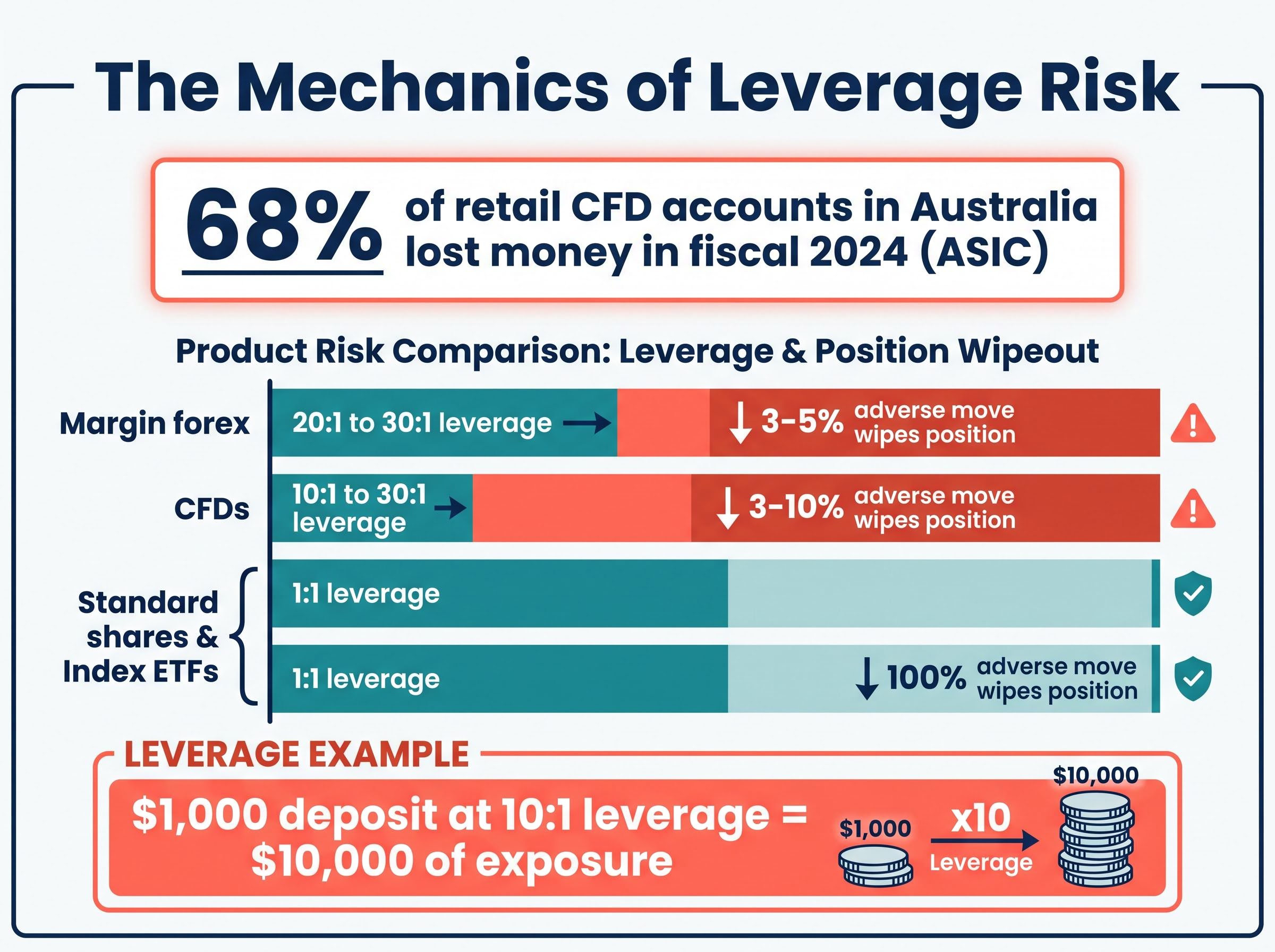

Approximately 68% of retail CFD accounts in Australia lost money in fiscal 2024, according to ASIC’s published enforcement data. That figure is not an outlier. It sits comfortably alongside the 70-80% loss rates reported by UK and European regulators for the same product category. The number is striking, but more instructive is what it represents: a predictable outcome, not a statistical anomaly.

Most new investors do not lose money because markets are inherently unfair. They lose money because they repeat a short list of behavioural and structural mistakes that experienced investors learned to avoid years ago. In the current Australian market environment, where social media finfluencers promote ASX stock tips to audiences with no financial training, where AI-themed hype cycles move penny stocks in single sessions, and where commission-free trading apps have reduced the barrier to entry without raising financial literacy alongside it, the conditions for beginner losses have rarely been more favourable.

This article names six common beginner investor mistakes that drain portfolios, explains the mechanism behind each loss, and provides a concrete corrective action for every one.

The 68% loss rate is not a reflection of bad timing or poor stock selection. It is a structural feature of the product itself.

Contracts for difference (CFDs) use leverage, meaning a trader controls a large position with a small deposit. At 10:1 leverage, a $1,000 deposit controls $10,000 of exposure. That ratio works identically in both directions. A 10% favourable move doubles the capital. A 10% adverse move eliminates it entirely.

ASIC data (fiscal 2024): Approximately 68% of retail CFD accounts in Australia lost money, a figure directionally consistent with the 70-80% retail loss rates reported by the UK’s FCA and the EU’s ESMA.

ASIC’s Product Intervention Order, in effect since 2021, restricts leverage ratios, mandates negative balance protection, and prohibits certain inducements for retail CFD products. The order was not a precautionary measure. It was a regulatory response to documented, sustained retail losses at scale.

The loss rate figures become less surprising once you understand how CFDs actually work: a CFD is a price agreement between a trader and a broker, not a purchase of any underlying asset, so the trader holds no ownership rights and bears the full amplified impact of every adverse price move against their margin deposit.

ASIC REP 828 on CFD distribution practices, published in January 2026, found that 133,674 retail clients lost money trading CFDs in FY2024 alone, with net losses exceeding $458 million including $73 million in fees, a scale of harm that underlies the regulator’s ongoing scrutiny of how CFD issuers target retail audiences.

| Product type | Typical leverage | Adverse move to wipe position | ASIC regulated? |

|---|---|---|---|

| CFDs | 10:1 to 30:1 | 3-10% | Yes (restricted since 2021) |

| Margin forex | 20:1 to 30:1 | 3-5% | Yes (restricted since 2021) |

| Standard shares | 1:1 | 100% | Yes |

| Index ETFs | 1:1 | 100% | Yes |

The corrective action is straightforward: beginners should defer leveraged products until they have at least 60-90 days of paper trading experience with them and can articulate the specific risk of ruin at the leverage ratio they intend to use.

Most beginners attribute their losses to picking the wrong stock. The research points elsewhere. The underlying engine behind the majority of beginner losses is behavioural bias, a set of psychological patterns that produce the same result regardless of which stock is involved: buying high and selling low.

Three biases account for the bulk of the damage.

FOMO (fear of missing out) drives investors to chase a stock after it has already moved. The ASX AI stock hype through 2024 and into 2025 provided a textbook illustration: by the time social media had amplified the narrative, much of the price move had already occurred, and latecomers were absorbing downside risk with limited remaining upside.

The disposition effect is FOMO’s mirror image. Research from Morningstar Australia (published July 2025) documents its prevalence among retail investors: the tendency to hold losing positions too long (hoping for recovery) while selling winners too early (locking in small gains). Both behaviours produce the same net outcome.

Panic selling completes the pattern. Investors who sold during sharp ASX corrections and missed the subsequent recovery crystallised a loss that the market eventually recovered from on their behalf. Loss aversion research indicates that losses feel approximately three times heavier than equivalent gains, which explains why the impulse to sell during drawdowns is so strong and so consistently value-destroying.

The connection between cognitive bias and market volatility is well-documented: the S&P 500 fell 10.5% across two days during the April 2025 tariff shock before delivering a 16.39% full-year return, and investors who sold during the decline converted a temporary drawdown into a permanent loss.

Each of these biases operates on the same mechanism: an emotional impulse overrides a rational plan. The corrective for all three is the same in principle, which is to make the decision before the emotion arrives.

Pre-set entry and exit rules remove FOMO from the equation. A fixed review cadence prevents daily price checking from triggering the disposition effect. A written drawdown commitment made in calm conditions is harder to break than a mental note made during a sell-off.

The shift from internal biases to external threats follows a logical path: once a beginner recognises their own behavioural vulnerabilities, paid signal groups and trading courses offer what appears to be a solution. Many of them are not.

ASIC and the ACCC have issued repeated thematic warnings about the growth of investment education scams in Australia, particularly Telegram-based signal groups and social media trading courses targeting 18-35 year olds. These products frequently operate without an Australian Financial Services Licence (AFSL), promise specific return percentages, and charge recurring subscription fees (often $49.99/month or more) that compound quietly while delivering content available for free elsewhere.

ASIC’s finfluencer crackdown, announced in June 2025, targeted operators inviting consumers to join closed communities or forums to copy trades, the same model used by many unlicensed Telegram signal groups that charge recurring subscription fees while operating outside the Australian Financial Services Licence framework.

Free verified resource: ASIC’s Moneysmart website (moneysmart.gov.au) provides comprehensive, regulator-approved investment education at no cost, covering topics from share investing basics to superannuation and tax.

A two-minute check before purchasing any course or signal service can prevent the majority of these losses:

The distinction matters: legitimate financial education exists and has value. The screening process above separates it from the predatory products that thrive on beginner urgency.

A stock surges 20% in a single session. The notification arrives. Social media fills with screenshots of the gain. The instinct to buy is immediate and visceral.

That instinct is the trap.

Stocks that move 20% or more in a single day have, in most cases, already priced in the catalyst that drove the move. The buyer who enters after the spike is absorbing all of the remaining volatility risk with little of the upside that the earlier participants captured. Liquidity thins after extreme moves, which amplifies price swings further against any new entrant attempting to build or exit a position.

The pattern operates in both directions. Beginners buy after surges (FOMO) and also buy after crashes, reasoning that a stock that has fallen 20% “can only go back up.” Both instincts are structurally unsound without additional due diligence, because neither addresses the question of whether the catalyst has been fully absorbed into the price.

A senior London broker quoted in industry research estimated that acting on post-move tips cost approximately $1 million over the course of a career. The prices had already moved before the tip arrived.

ASX penny stocks are particularly susceptible to this dynamic, where pump-and-dump schemes amplify the initial move through coordinated social media promotion, and latecomers absorb the subsequent reversal.

ASX pump-and-dump schemes follow a repeatable structure: a coordinated social media promotion inflates a small-cap price, latecomers absorb the move after the bulk of the gain has been captured by earlier participants, and the subsequent reversal arrives faster than most retail investors can react.

Before entering any stock after a large single-day move, three signals are worth evaluating:

For most Australians, superannuation will be their single largest lifetime investment. A beginner who spends hours analysing ASX stock picks while ignoring super and tax structure is optimising the smallest component of their net wealth.

The scale of the opportunity cost becomes clear when the numbers are modelled: the tax advantage of investing inside super means a 35-year-old investing $100,000 at the same gross return could accumulate roughly $230,000 more by age 60 inside super than in a personal share portfolio, purely due to the 15% earnings tax rate versus marginal rates of up to 47% outside it.

Multiple superannuation accounts are the most common and most quietly destructive mistake. Each additional account carries its own administration fees and default insurance premiums, silently eroding balances that should be compounding. Remaining in a default conservative investment option, particularly for investors under 40, costs decades of growth at the wrong risk setting relative to the investor’s time horizon.

| Beginner mistake | Corrective action |

|---|---|

| Multiple super accounts with duplicate fees | Consolidate into a single fund via myGov or the fund directly |

| Default conservative investment option | Review and select an option aligned with age and risk tolerance |

| Selling shares before the 12-month CGT threshold | Hold for at least 12 months to access the 50% CGT discount |

| Excluding brokerage from CGT cost base | Include all brokerage fees in cost base calculations at purchase and sale |

| Poor record-keeping for tax purposes | Maintain a spreadsheet of all trades including dates, prices, and fees from day one |

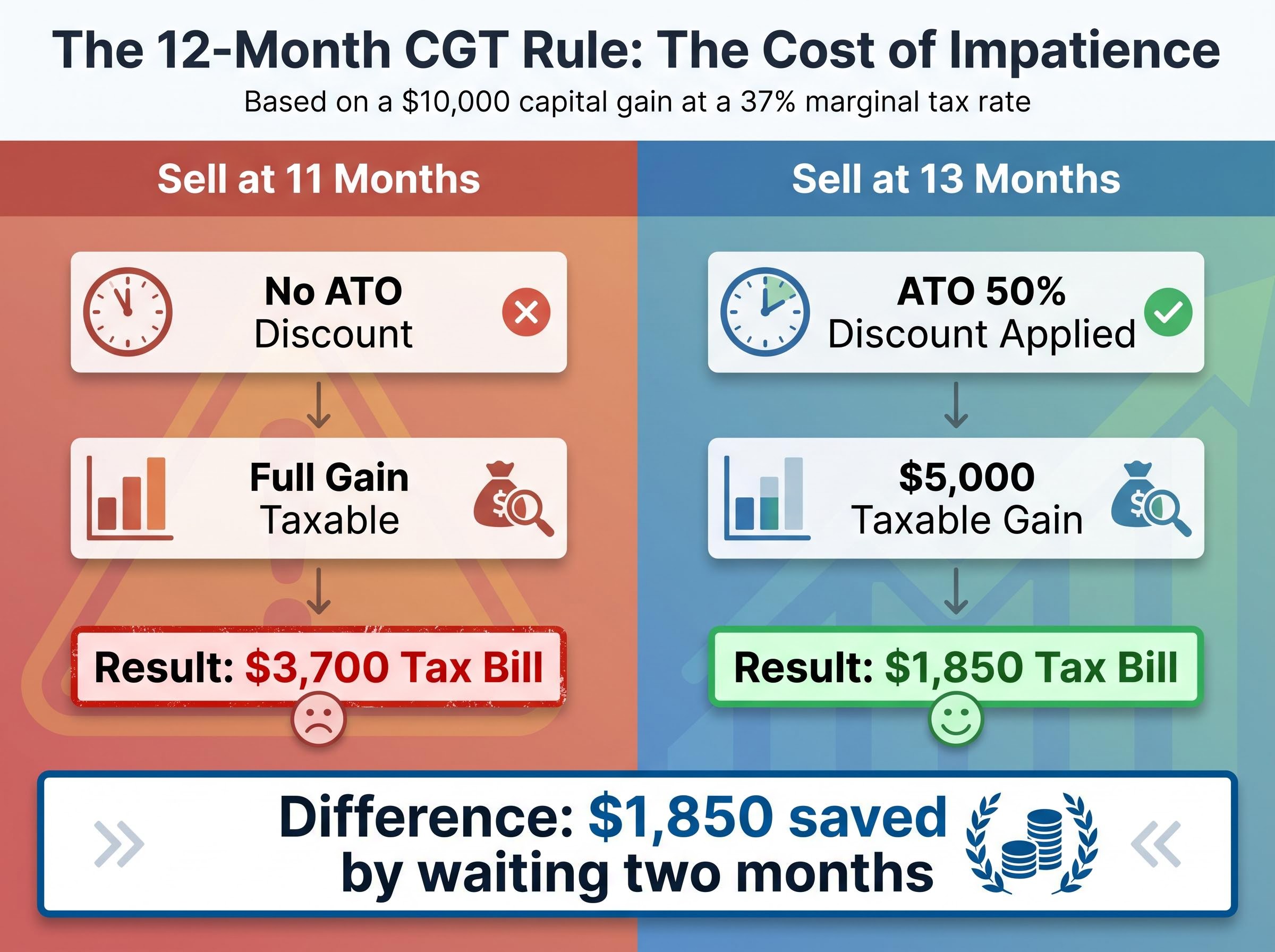

The Australian Tax Office (ATO) provides a 50% capital gains tax discount for assets held for 12 months or more. Beginners who panic-sell before that threshold do not just crystallise a market loss; they also forfeit the discount.

A worked example: an investor realises a $10,000 capital gain on a share trade. At a 37% marginal tax rate, selling at 11 months produces a tax bill of $3,700 (the full gain is taxable). Selling at 13 months triggers the 50% discount, reducing the taxable gain to $5,000 and the tax bill to $1,850. The difference, $1,850, is the cost of two months’ impatience.

Brokerage costs are also frequently excluded from CGT calculations. Brokerage paid at purchase increases the cost base, and brokerage paid at sale reduces the capital proceeds, both lowering the taxable gain. Missing these deductions means overpaying tax on every trade.

The six mistakes above share a common thread: they are all avoidable with preparation. The corrective is not caution; it is practice.

Paper trading is not a watered-down substitute for real investing. It is the standard method professionals use to test a strategy before committing capital. Two verified platforms available to Australian beginners offer this at no cost:

The realistic first-year benchmark for any beginner is worth stating plainly.

Finishing year one with the same capital you started with is a genuine success metric, not a consolation prize.

Loss aversion research confirms why this matters: because losses feel approximately three times heavier than equivalent gains, undercapitalised real-money trading is psychologically destructive for learners. Paper trading removes that weight while preserving the educational value.

One final trap deserves mention. The opposite of FOMO is analysis paralysis: the beginner who researches indefinitely and never starts. This is also a cost, measured in opportunity foregone, inflation erosion, and compounding years lost.

A practical starting framework:

These six mistakes are not random or unlucky outcomes. They are predictable patterns with documented loss mechanisms and known corrective actions. Every beginner who recognises them in advance holds a structural advantage over one who does not.

Two actions carry the highest return for the lowest effort: check a provider’s AFSL before paying for any course or signal service, and open a demo account before trading any leveraged product. Both cost nothing and take minutes.

Investing is a long-term intellectual pursuit, not a short-term extraction exercise. The beginners who treat it accordingly, who build skills before risking capital and who understand the behavioural patterns that produce losses, are the ones most likely to still be investing a decade from now.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The most common beginner investor mistakes include trading leveraged CFD products without understanding the risks, acting on behavioural biases like FOMO and panic selling, paying for unlicensed signal groups or trading courses, chasing stocks after extreme single-day price moves, and ignoring superannuation and capital gains tax rules that significantly affect net returns.

Approximately 68% of retail CFD accounts in Australia lost money in fiscal 2024, according to ASIC data, because leverage amplifies losses just as much as gains, meaning even a small adverse price move can wipe out an entire deposit before a trader can react.

The ATO provides a 50% capital gains tax discount on assets held for 12 months or more, so a beginner who sells shares before that threshold at a 37% marginal tax rate could pay up to $1,850 more in tax on a $10,000 gain compared to waiting just two additional months.

Beginners should search ASIC Connect to verify the provider holds an Australian Financial Services Licence (AFSL), check the ASIC Investment Warning List, look for a physical Australian address and named staff, and treat any promise of guaranteed returns or specific win rates as an automatic red flag under Australian financial services law.

Paper trading involves practising buy and sell decisions using virtual funds rather than real capital, allowing beginners to test strategies and understand risk mechanics without financial loss; ASIC-regulated platforms like IG Australia offer free demo accounts specifically for this purpose.