Why Short Squeezes Send Stocks Parabolic and Then Collapse

7 mins ago

Takeover premiums in Australian small-cap acquisitions typically run 20% to 40% above pre-bid trading prices, yet most retail investors only learn about a deal after the share price has already moved. The gap between those who capture that premium and those who chase it comes down to one thing: understanding why deals happen, which companies attract them, and how to act at each stage of the process.

The mid-2026 Australian market is running an active gold and resources merger and acquisition cycle alongside technology sector consolidation, making small-cap M&A a live and immediately relevant topic. What follows is a structural framework for reading these cycles, identifying high-probability targets before a bid lands, and making the correct hold, arbitrage, or redeployment decision at each stage of a deal. Three recent Australian case studies put the framework to work with real numbers.

Takeovers are not random events. They cluster into sector-specific waves, and those waves are driven by three structural forces that, when they converge, make deal activity not just likely but close to inevitable.

The 2024-26 period is a convergence moment. Falling rates, significant PE dry powder, and historically wide small-cap valuation discounts to large caps are all pointing in the same direction. Small caps have historically outperformed during monetary easing and early-cycle recoveries, and those same periods coincide with higher M&A activity.

The commodity supercycle thesis underpinning the current gold and resources M&A wave rests on four demand pillars: AI data centre copper intensity, grid expansion, EV adoption, and defence spending on rare earths; major mining companies currently trade at roughly 7-8x EV/EBITDA compared to approximately 14x during the 2008-2010 boom, a valuation gap that institutional capital has been closing at pace and that sustains the financing conditions for further consolidation.

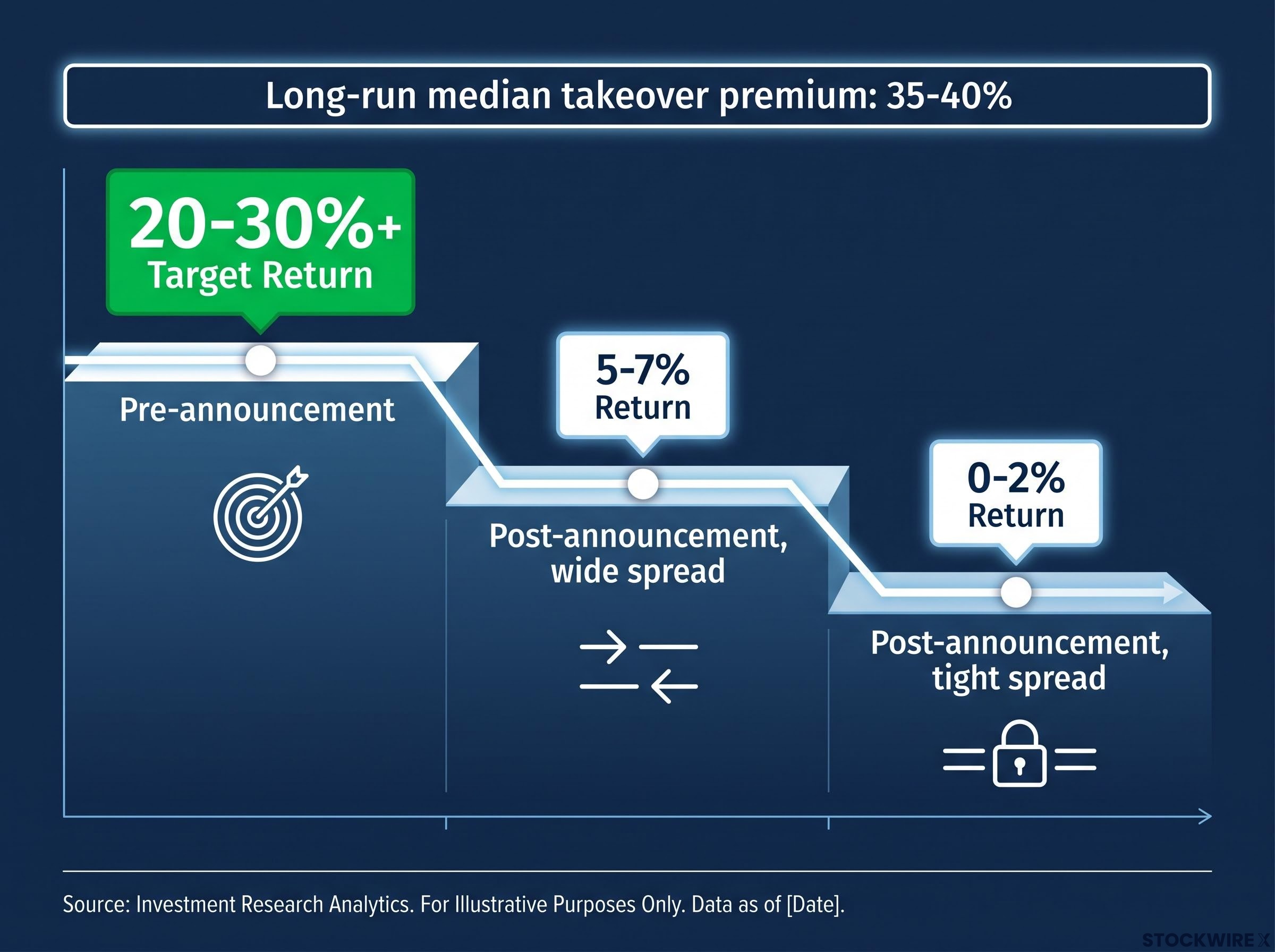

The long-run median takeover premium for Australian small caps sits around 35-40% over pre-bid trading prices, anchoring the structural case for why pre-bid positioning generates returns that post-announcement arbitrage cannot replicate.

Understanding these three drivers shifts M&A from an unpredictable event to a structurally anticipatable one. The rest of this framework builds on that foundation.

Within a single resource bull market, deal activity does not arrive all at once. It cascades down the capitalisation spectrum in a consistent and observable sequence:

This pattern is not theoretical. It is visible in real time.

The Australian gold cycle has already moved through its upper tiers. De Grey Mining and Gold Road Resources were acquired at the Tier 1 level. Genesis Minerals acquiring Magnetic Resources and the Volant-Regus merger of equals represent mid-cap consolidation. The wave is now at the junior developer stage.

The Regis and Vault merger, an all-scrip deal creating Australia’s third-largest ASX gold producer at over 700,000 ounces per year, illustrates the mid-cap consolidation phase in real time: Regis shares fell roughly 14% within 48 hours of announcement, consistent with the acquirer sell-off pattern that frequently emerges when the synergy logic is sound but the market prices in execution risk and scrip dilution ahead of deal close.

BHP and Rio Tinto positions in comparable portfolios were reported up approximately 35-40% as of early June 2026, consistent with ongoing commodity market strength that sustains the conditions for further deal activity. In tin, Metals X produces approximately 11,000 tonnes per year (around 4% of estimated global supply), providing the operational scale that makes junior tin developers logical acquisition targets.

The investor edge is positional. Recognising where the wave currently sits, at the junior developer stage, identifies where the next tranche of premiums will be captured before the bids arrive.

Knowing that a sector is in an active M&A cycle is necessary but not sufficient. The question that converts macro awareness into stock selection is: which specific company actually gets taken over?

A high-conviction M&A setup typically requires three conditions working together:

The screening criteria differ by sector.

| Resources Targets | Technology Targets |

|---|---|

| Proximity to existing mills or smelters operated by logical acquirers | Recurring revenue above 70%, serving government or institutional clients |

| Sub-scale producers with identifiable larger neighbours | Recent de-rating driven by sector-wide concerns, not company-specific deterioration |

| Development capital requirements creating incentive for processing deals | Founder-led businesses with disclosed strategic reviews or inbound interest |

One additional signal warrants attention: a strategic stake of 10-20% or more by a logical buyer. This validates the thesis and signals acquirer interest, but it also carries a limitation. A blocking stake can deter competing bidders, reducing the probability of a competitive auction and potentially capping the final offer price.

Most investors treat M&A investing as a single activity. It is not. There are three distinct stages, and each demands a fundamentally different decision framework.

| Stage of Deal | Key Decision | Target Return Profile |

|---|---|---|

| Pre-announcement | Size position for timing and price uncertainty | 20-30%+ if thesis pays off |

| Post-announcement, wide spread | Assess deal risk against available spread | Single-digit return, high IRR if time to close is short |

| Post-announcement, tight spread | Treat as cash equivalent; redeploy capital | 0-2% remaining; focus on opportunity cost |

Pre-bid positioning targeting 20-30% or more is a structurally different activity from merger arbitrage on a 5-7% narrow spread. Conflating the two leads to either overpaying for a deal already announced or exiting too early on a wide spread that was worth holding.

One structural feature of Australian M&A reinforces this distinction. When an acquirer structures a deal as a scheme of arrangement rather than an off-market takeover bid, the offer price is typically higher.

Schemes of arrangement require 75% approval by votes cast plus a majority of shareholders by number. Acquirers pay up for the certainty and clean execution a scheme provides, which is why scheme offers consistently exceed takeover bid prices for the same target.

ASIC Regulatory Guide 60 on schemes of arrangement sets out the Commission’s role in reviewing scheme documents, the matters it considers before issuing a no-objection statement, and the shareholder approval thresholds that apply under Part 5.1 of the Corporations Act 2001, providing the formal regulatory basis for the premium pricing that scheme structures consistently attract.

Understanding which stage of the deal lifecycle a position occupies determines whether the correct action is to hold, to capture the spread, or to redeploy.

Stellar Resources is developing what is classified as the highest-grade undeveloped tin project in Australia (and the third-highest globally), located approximately 18 kilometres from the Metals X-operated Renison processing facility. The synergy logic is specific: Stellar’s ore could be processed through the existing Renison mill rather than requiring a standalone facility, which would be highly capital-intensive.

In April 2026, Metals X acquired a strategic stake in Stellar via a placement at approximately 3.3 cents per share. The thesis was validated. The position was exited.

RPM Global, an Australian mining software company, was acquired by Caterpillar in a transaction announced in October 2025 and closed in February 2026. During the post-announcement period, shares traded at approximately $4.70 against a $5.00 offer price.

The rationale for holding through close was straightforward: no competing bidder would realistically challenge Caterpillar’s financial scale, making deal risk low and the spread worth capturing. Once the share price narrowed to within a few cents of the offer price, the position was liquidated and capital redeployed.

ReadyTech (ASX: RDY) operates mission-critical software platforms serving TAFEs, education institutions, government, and legal sectors. The takeover thesis proved directionally correct: a subsidiary of Constellation Software (Topicus/Total Specific Solutions) announced an offer in late May/early June 2026, structured at approximately $1.75 per share via takeover bid or $2.00 via scheme of arrangement.

The offer came in below expectations. A February earnings result had disappointed the market, with no meaningful contract progress reported, and the stock’s illiquidity amplified the negative price reaction. As of June 2026, the share price was trading below the stated offer price, and the ReadyTech board had rejected the initial offer.

For investors wanting to understand why Constellation Software was the logical acquirer of ReadyTech rather than a domestic ASX peer, our deep-dive into the Constellation Software acquisition model examines how the company contacts up to 100,000 vertical market software businesses annually, why its decentralised approval structure lets it close deals faster than competitors, and how that engine is now expanding into larger transactions.

A correct thesis with wrong position sizing produces the same outcome as a wrong thesis. In illiquid small-cap names, both entry and exit can move the price materially, creating a structural asymmetry that demands more conservative sizing and a larger margin of safety than equivalent positions in liquid names.

The ReadyTech earnings miss is a live illustration. In a more liquid stock, the same result would have produced a measured decline. In ReadyTech’s thin trading volumes, the reaction was amplified, compounding losses on a position where the underlying takeover thesis was ultimately validated.

Practical rules for M&A position sizing:

A tight-spread position earning 1-2% competes directly against the next pre-bid setup targeting 20-30%. The opportunity cost of holding through close when the spread has collapsed is real and measurable.

The macro conditions for small-cap M&A in mid-2026 are structurally supportive. Falling rates are reducing acquisition financing costs for both PE and strategic buyers. PE funds are deploying accumulated dry powder. Small caps continue to trade at wide valuation discounts to large caps across multiple sectors.

Two active fronts are visible.

The gold and tin M&A cycles have moved through their Tier 1 and mid-cap phases. The wave is now at the junior developer stage, where the remaining valuation gaps are widest and the pre-bid positioning premiums are available. The Metals X stake in Stellar Resources is a live example of this stage in motion: the strategic logic is established, the blocking position is acquired, and the question is timing rather than whether consolidation occurs.

Falling rates are also catalysing PE-driven M&A in software and services. The high-probability target profile mirrors the ReadyTech setup: recurring revenue above 70%, mission-critical platforms serving government and institutional clients, and recent de-rating driven by sector-wide concerns (interest rate sensitivity, AI disruption) rather than company-specific deterioration. The Constellation Software bid for ReadyTech is a live example of this consolidation trend.

CGT reform timing creates an additional seller-side incentive that is compressing deal windows in the technology sector: with the 50% CGT discount being replaced by cost-base indexation and a 30% minimum rate from 1 July 2027, founder-controlled software businesses face meaningfully higher exit tax burdens after that date, adding urgency to strategic sale processes that would otherwise have extended over a longer horizon.

The framework built in this article exists to identify the next Stellar, the next RPM Global, the next ReadyTech, before the announcement rather than after.

The six questions that constitute a pre-investment M&A checklist:

M&A premiums close valuation gaps that organic re-ratings fail to deliver. A long-run median premium of 35-40% is not an anomaly; it is the structural price of speed, certainty, and synergy that acquirers pay and that pre-bid positioning captures. That is why the edge is real, persistent, and worth building a disciplined framework around.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding M&A activity and market conditions are speculative and subject to change based on market developments and company performance.

Australian small cap M&A refers to merger and acquisition activity involving smaller listed companies on the ASX. These companies attract takeover premiums of 20% to 40% above pre-bid prices because acquirers pay for speed, certainty, and the synergy value that organic growth cannot deliver as quickly.

Rising commodity prices generate strong cash flows and elevated scrip values for major miners, which then fund acquisitions that cascade down the capitalisation spectrum: Tier 1 assets are acquired first, followed by mid-cap bolt-ons, and finally junior developers, where the widest valuation gaps and largest pre-bid premiums are found.

The three key conditions are a clear synergy rationale for a specific acquirer, a constrained buyer universe of one or two logical bidders, and a realistic path to closing given board dynamics and regulatory environment. Sector-specific screens differ: resources targets are assessed on proximity to existing mills, while technology targets are assessed on recurring revenue above 70% and mission-critical client exposure.

A scheme of arrangement requires 75% approval by votes cast plus a majority of shareholders by number, and acquirers typically pay a higher price for that certainty and clean execution. The ReadyTech case illustrates this directly, with Constellation Software offering approximately $1.75 via takeover bid versus $2.00 via scheme of arrangement, a $0.25 structural premium for the scheme structure.

Pre-bid positions should be sized to reflect both timing uncertainty (no guarantee of when or whether a bid arrives) and liquidity risk (the inability to exit without moving the price), with a minimum expected return threshold of 20% to 30% to compensate for those risks. Post-announcement tight-spread positions earning 1% to 2% should be treated as near-cash and redeployed into higher-returning setups.