What Trading Expectancy Reveals About Your Strategy’s Edge

3 hrs ago

Most options traders start with a simple premise: pick a direction, buy a call or put, and profit when the market moves as expected. The problem is that being right about direction is often not enough. Time decay silently erodes the value of every long options position, meaning a trader can correctly call the market’s direction and still lose money if the move arrives too slowly or falls short of the required magnitude. This tension between directional conviction and time’s constant erosion pushes more experienced traders toward credit spreads, a strategy that restructures the relationship between time and probability entirely. What follows is a ground-up explanation of how credit spreads work, what gives them a statistical edge over directional positions, and what the honest trade-off looks like in practice. By the end, readers will have a clear framework for understanding why professional traders prioritise probability management over chasing large individual wins.

A new options trader typically begins by buying calls or puts based on a thesis about where a stock or index is heading. The logic feels straightforward: if the stock goes up, the call goes up. If the stock goes down, the put goes up.

What the logic omits is that profitability is not a one-variable problem. It is a two-variable problem at minimum, and often three. For a basic long call or long put to deliver a profit, three conditions must align simultaneously:

Consider a trader who buys a call option expecting a stock to rise. Over the following three weeks, the stock climbs modestly, exactly as predicted. Yet when the trader checks the position, it has lost value. The reason is theta decay, the daily erosion of the option’s time value, which outpaced the modest price gain. The direction was right. The trade still lost money.

This experience is not an edge case. A flat or slowly moving asset punishes the long options holder continuously, even when their eventual directional read proves correct. The premium paid at entry begins decaying the moment the trade is opened, and that decay accelerates as expiration approaches. Understanding why this happens is the first step toward understanding why credit spreads exist.

An option’s premium is composed of two components. Intrinsic value measures how far in the money the option currently sits; it is the portion of the price that reflects real, tangible value if the option were exercised immediately. Time value is everything else: the portion of the premium that reflects the possibility that the option could become more valuable before it expires.

Time value is what decays. And it decays at an accelerating rate, behaving less like a slow leak and more like a countdown that speeds up in its final stages. Professional educators consistently recommend the 30-45 days to expiration (DTE) window for capturing this acceleration, because it is during this period that theta decay is most pronounced while premiums remain workable.

Option buyers pay time decay; option sellers collect it. Every day that passes without a significant move in the underlying asset works in the seller’s favour.

Theta is the Greek that quantifies daily time value erosion. It is expressed as a dollar amount per day per contract. A long option with a Theta of -0.05 loses approximately $5 per day per contract in time value, all else being equal.

For a seller, the sign flips. Positive Theta means each passing day adds to the position’s theoretical profit. The seller does not need the underlying asset to move in a particular direction. The seller needs it to not move too far in the wrong direction. This is a structurally different relationship with time, and it is the mechanical foundation underneath every credit spread.

A credit spread is built from two simultaneous options trades. The first leg is a sale: the trader sells an option to collect premium. The second leg is a purchase: the trader buys a further out-of-the-money option of the same type, same expiration, to cap the maximum possible loss.

The bought option is not a cost to be minimised. It is a structural necessity. Without it, the sold option is “naked,” carrying theoretically unlimited loss exposure. With it, the position becomes defined-risk: the maximum loss is fixed and known before the trade is entered.

Two common configurations serve opposite directional biases:

| Spread Type | Market Outlook | Short Leg (Sell) | Long Leg (Buy) |

|---|---|---|---|

| Bull put spread | Neutral to bullish | Put below current price | Lower-strike put for protection |

| Bear call spread | Neutral to bearish | Call above current price | Higher-strike call for protection |

The net credit received is the difference between the premium collected on the short leg and the premium paid for the long leg. Before entering any credit spread, four numbers must be calculated:

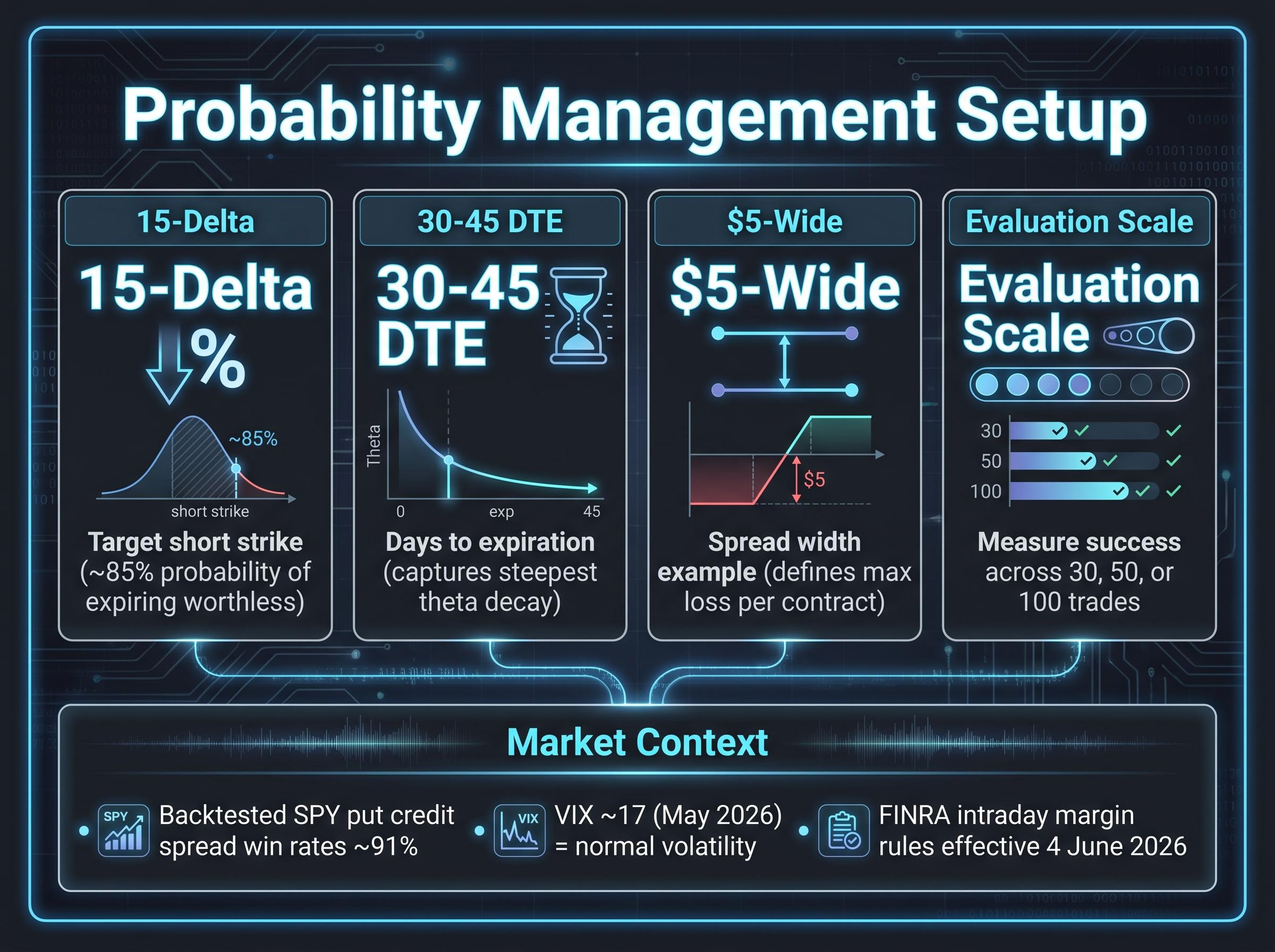

An illustrative setup might use a 15-delta short strike, a $5-wide spread, and 30-45 DTE. These parameters, drawn from professional educator recommendations, encode specific probability assumptions into the trade before it is even placed.

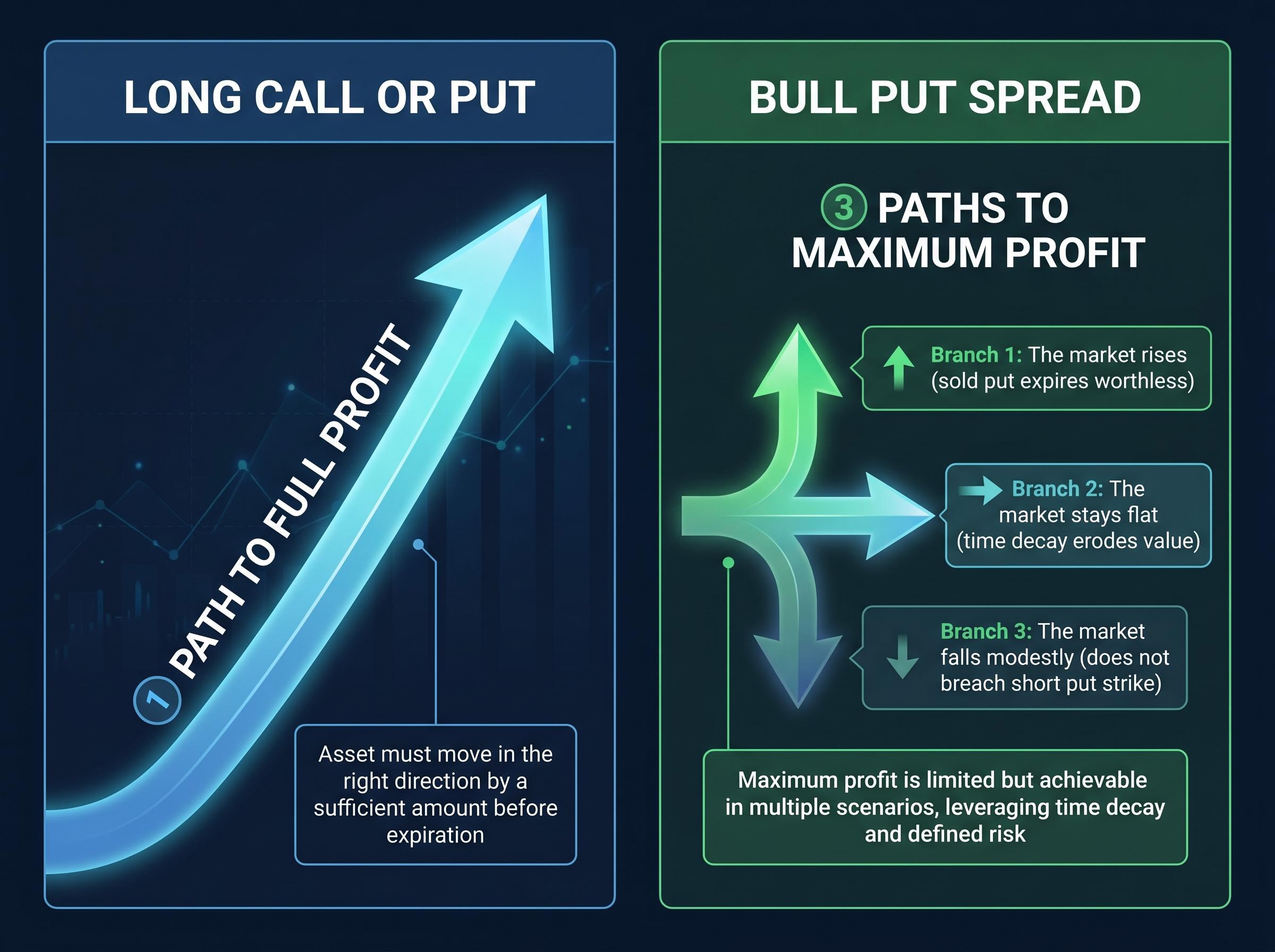

A long call or long put has exactly one path to full profit: the underlying asset must move in the right direction by a sufficient amount before expiration. If it moves the wrong way, stays flat, or moves too slowly, the position loses.

A bull put spread has three paths to maximum profit:

The short strike placement is the variable that determines how wide this profitability zone stretches. By positioning the sold strike outside the asset’s expected movement range, the trader constructs a position that profits in the majority of plausible outcomes rather than requiring a single specific outcome.

Backtested SPY put credit spread strategies have shown win rates approaching 91% in some analyses. These are historical figures and not guarantees of future performance, but they illustrate the structural probability advantage the strategy is designed to capture. With the VIX at approximately 17 as of May 2026, the current environment represents a normal volatility regime in which credit spreads remain viable with moderate premiums and steady theta decay benefits.

Consistent profitability comes from managing probability across many trades, not from maximising the return on any single one.

Professional traders favour this structure not because individual trades generate spectacular returns. They favour it because the probability of winning on any given trade is structurally higher than it is for a directional long option.

The elevated probability of profit in a credit spread comes at a specific cost: an inverted risk-reward ratio. The amount at risk on any single trade is structurally larger than the maximum gain.

Consider a concrete example. A trader collects $1.50 in net credit on a $5-wide spread. The maximum loss is $3.50 per share (spread width minus credit received), multiplied by 100 per contract. That is roughly a 2.3-to-1 risk-reward ratio working against the trader on every individual position.

This ratio is not a flaw. It is the price the strategy charges for its probability advantage. Consistent profitability depends on winning a high enough percentage of trades to overcome the occasional maximum loss, which is why disciplined stop-loss adherence and position sizing matter as much as trade selection.

Volatility context shapes how attractive this trade-off is at any given time:

| Volatility Environment | Typical Premium Quality | Impact on Risk-Reward Ratio |

|---|---|---|

| Low (VIX below ~15) | Thin premiums, compressed credits | Ratio worsens; max loss is a larger share of potential reward |

| Normal (VIX ~17, current) | Moderate premiums, steady theta decay | Ratio is workable with disciplined sizing |

| Elevated (VIX above ~25) | Rich premiums, larger credits | Ratio improves; greater margin for error |

When the VIX spiked above 60 in April 2025, credit spreads produced significantly richer credits with wider margins for error. In contrast, low-volatility periods compress premiums and make the already unfavourable ratio even less attractive. Margin for a credit spread is calculated as (strike difference multiplied by 100) minus net premium received, making it capital-efficient relative to naked short options, but traders must still manage three risk disciplines:

Implied volatility signals in derivatives markets encode the market’s collective expectation of future price movement, not direction, meaning a credit spread entered when IV is elevated relative to a stock’s historical average captures richer premium for the same probability profile than the same spread entered in a compressed-IV environment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Professional traders using credit spreads do not ask whether a specific trade will win. They ask whether their process, applied across many trades, produces a statistical edge. Each position is treated as one instance in a long series, not as an isolated event whose outcome determines success or failure.

The combination of a high win rate and a fixed maximum loss creates a framework where outcomes are predictable in aggregate. A 15-delta short strike selection means the sold option has approximately an 85% probability of expiring worthless at entry. That figure is not a guarantee on any individual trade, but across 50 or 100 trades, it describes the expected distribution of wins and losses with reasonable accuracy.

This is why the setup parameters introduced earlier are not arbitrary rules. A 15-delta short strike, 30-45 DTE, and $5-wide spread are expressions of probability management. Each parameter encodes a specific assumption about the balance between premium collected, risk accepted, and the statistical likelihood of the trade expiring profitably.

The mindset shift, from outcome focus to process focus, is what separates traders who use credit spreads successfully from those who abandon the strategy after a string of losing trades. A trader who measures success trade by trade will inevitably encounter a maximum loss and question the strategy. A trader who measures success across 30 or 50 trades will recognise that the occasional maximum loss is the cost of operating a system designed to win more often than it loses.

Five setup parameters encode this probability management into each trade:

FINRA’s new intraday margin standards, effective 4 June 2026, may improve capital efficiency for credit spread traders by potentially reducing margin tie-up, representing the most significant recent regulatory change affecting options spread strategies.

FINRA’s intraday margin requirements, updated effective June 2026, directly affect how credit spread positions are margined during the trading day, with potential implications for the capital efficiency calculations traders use when sizing spread positions relative to account equity.

Credit spreads do not eliminate risk. They restructure it, shifting the trader from needing a precise directional prediction to needing a disciplined, repeatable process. The strategy offers three structural advantages: a defined maximum loss known at entry, a probability of profit across multiple market conditions, and a Theta advantage that works with time rather than against it.

What the strategy demands in return is equally specific: consistent position sizing that prevents any single loss from threatening the account, honest stop-loss adherence that caps losses before they reach the theoretical maximum, and the patience to let probability play out across many trades rather than measuring success by any individual outcome.

Readers interested in implementing credit spreads should consider beginning with paper trading or very small position sizes to internalise the mechanics before committing meaningful capital. Brokerage educational resources and publications from the Options Industry Council offer deeper guidance on Greeks, margin requirements, and strategy variations beyond the scope of this framework.

The Options Industry Council credit spread resources cover bull put spreads, bear call spreads, and iron condors in detail, providing the Greeks breakdowns and margin treatment explanations that serve as a practical complement to the probability framework described here.

These statements are informational and not a recommendation to trade options. Options involve risk of loss and are not suitable for all investors.

A credit spread is an options strategy involving the simultaneous sale of one option and purchase of a further out-of-the-money option of the same type and expiration, generating a net premium credit while capping the maximum possible loss to the width of the spread minus the credit received.

Theta measures the daily erosion of an option's time value; sellers of credit spreads hold positive theta, meaning each passing day without a large adverse move in the underlying asset adds to the position's theoretical profit, giving sellers a structural time advantage over option buyers.

Credit spreads carry an inverted risk-reward ratio by design; for example, collecting $1.50 credit on a $5-wide spread means the maximum loss is $3.50 per share, roughly a 2.3-to-1 ratio against the trader, which is offset by the structurally higher probability of the trade expiring profitably.

Professional traders commonly target a 15-delta short strike, which encodes approximately an 85% probability of the sold option expiring worthless, combined with a 30-45 days to expiration window to capture the steepest portion of the theta decay curve.

Higher VIX levels produce richer premiums and wider margins for error, improving the risk-reward ratio; when the VIX spiked above 60 in April 2025 credits were significantly larger, while low VIX environments below 15 compress premiums and make the already unfavourable ratio less attractive.