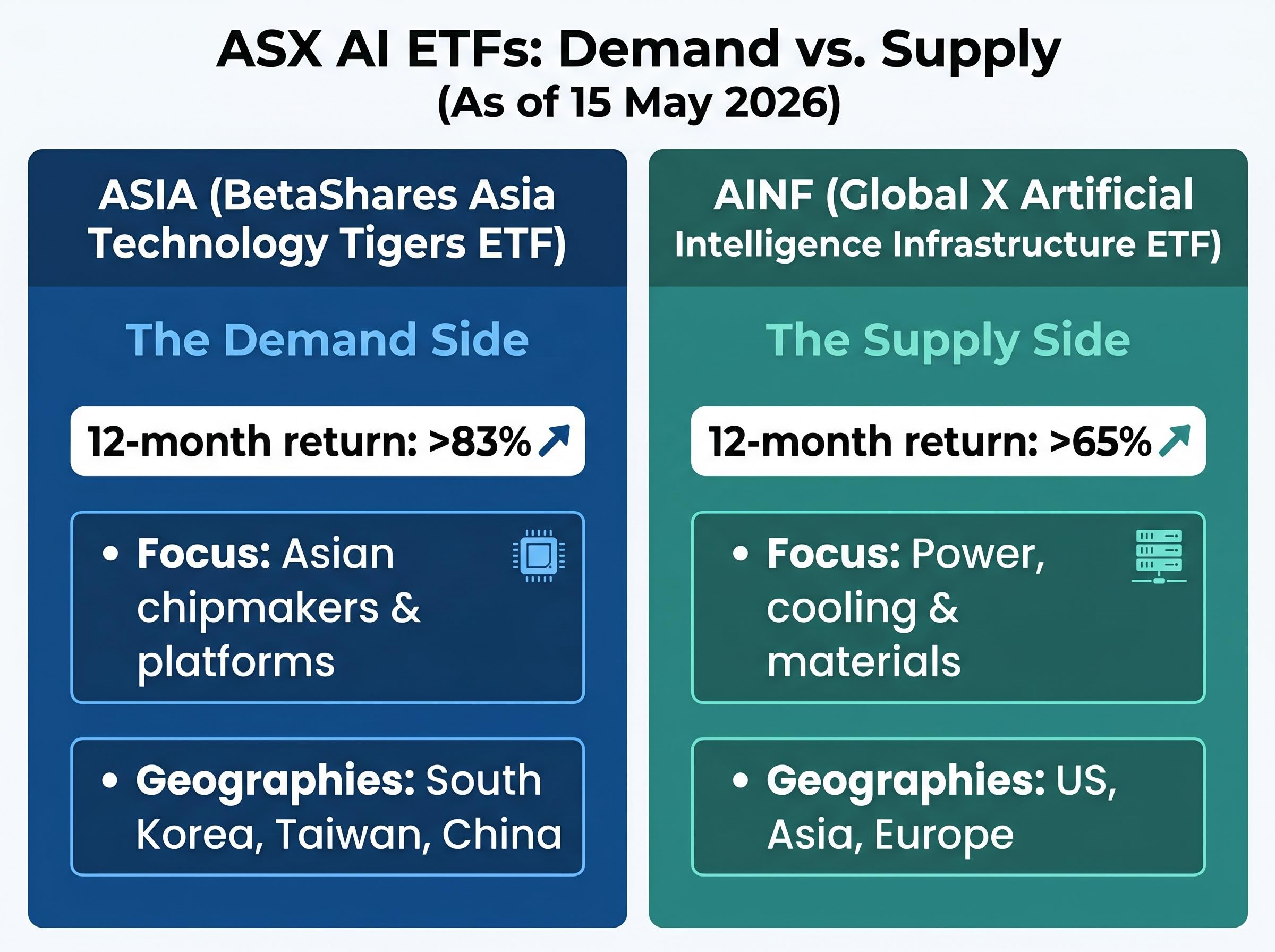

Two of the ASX’s most distinctive thematic ETFs closed at all-time high prices on Thursday 15 May 2026, marking a rare dual milestone for Australian investors tracking artificial intelligence exposure. The BetaShares Asia Technology Tigers ETF (ASIA) approached $21 per unit during the session, while the Global X Artificial Intelligence Infrastructure ETF (AINF) extended a rally that has delivered more than 65% over the prior 12 months. The records arrive as the Australian ETF industry sits at A$330.6 billion in assets under management, with 2025 inflows of A$53 billion representing a 76% increase on 2024. These are not two versions of the same bet. ASIA captures Asian semiconductor and platform leaders on the demand side of AI. AINF targets the physical power, cooling and materials infrastructure making AI workloads possible. What follows is a breakdown of what each fund holds, what produced their exceptional returns, and what the risks are for investors considering whether to act on the momentum.

Australian ETF industry growth has accelerated sharply beyond the A$330.6 billion figure cited at end-2025: assets reached A$346 billion by April 2026, with thematic and international equity products capturing a disproportionate share of the A$5.2 billion in net inflows that made April the third-highest single month on record.

Two thematic ETFs just hit simultaneous all-time highs on the ASX

Five ASX-listed ETFs hit record or 52-week highs in the week of 15 May 2026. Two of them, ASIA and AINF, both reached all-time prices on the same session.

That is not a coincidence. It reflects investor conviction building simultaneously across two distinct layers of the AI investment chain: the companies designing and manufacturing the chips, and the companies supplying the power, cooling and raw materials those chips consume at scale.

The two funds diverge sharply in what they own and where they own it:

- ASIA: Asian equity exposure; tracks approximately 50 large-cap semiconductor, e-commerce and internet companies listed in Asia ex-Japan; 12-month return exceeding 83%; geographic concentration in South Korea, Taiwan and China.

- AINF: Global infrastructure exposure; targets electric utilities, data-centre thermal management, copper and uranium producers supplying the physical AI build-out; 12-month return exceeding 65%; diversified across the US, Asia and Europe.

For Australian investors evaluating which thematic ETFs have earned recent attention, the simultaneous records provide a concrete starting point, but the funds serve fundamentally different theses and carry different risks.

When big ASX news breaks, our subscribers know first

What the Betashares Asia Technology Tigers ETF actually holds, and why it returned 83% in a year

ASIA tracks the Solactive Asia ex-Japan Technology and Internet Tigers Index, a basket of approximately 50 of the largest Asian technology and online retail companies outside Japan. Its NAV stood at $20.46 as of 13 May 2026, and the fund’s verified one-year return was 71.60% to 30 April 2026, according to the BetaShares factsheet. The acceleration through May pushed that figure above 83% by session close on 15 May.

The return is large, but the portfolio composition explains it.

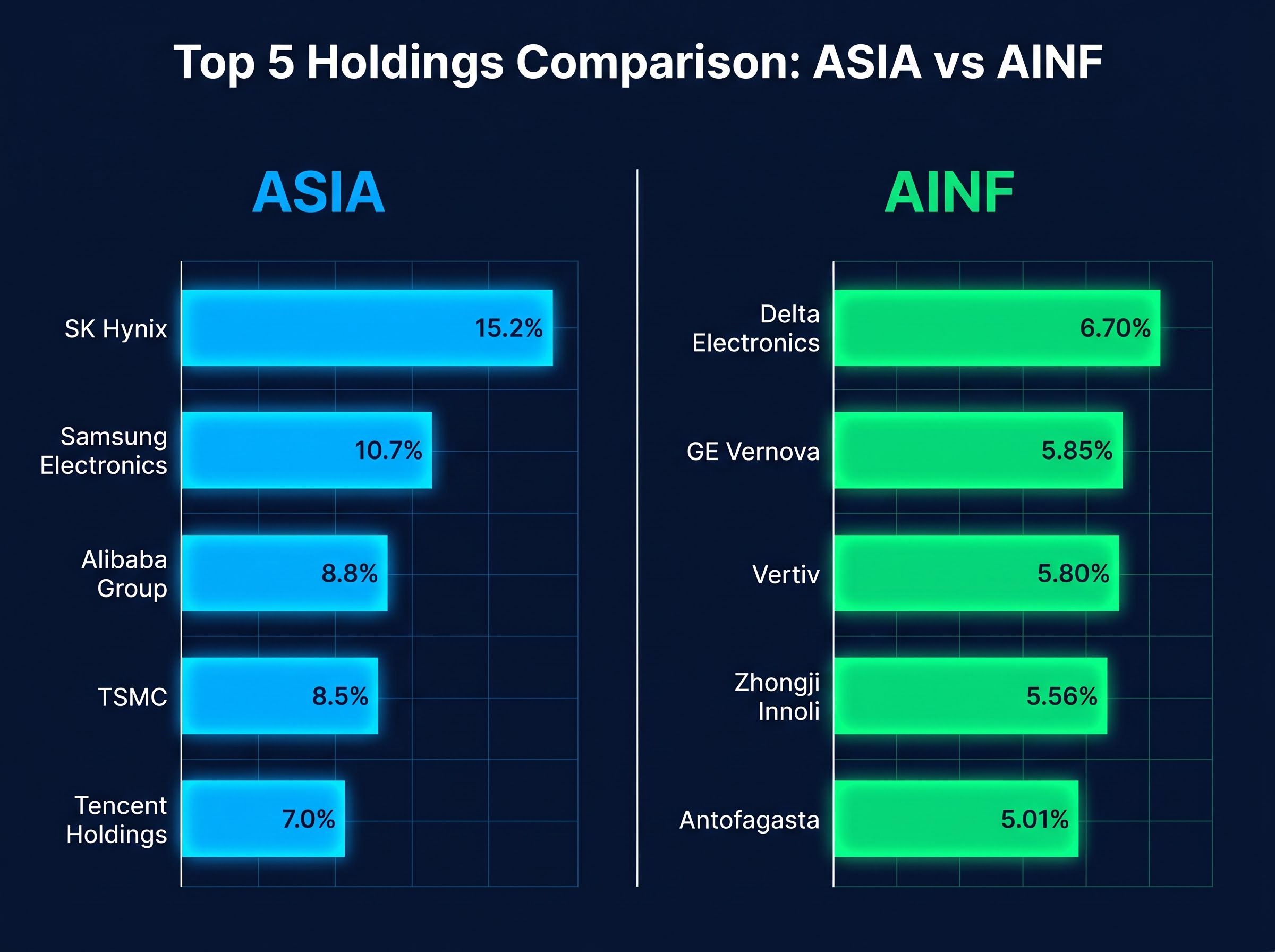

| Holding | Approximate Weight | Primary Performance Driver |

|---|---|---|

| SK Hynix | 15.2% | AI memory chip demand surge |

| Samsung Electronics | 10.7% | Advanced node and memory cyclical recovery |

| Alibaba Group | 8.8% | Chinese regulatory thaw; earnings stabilisation |

| TSMC | 8.5% | Global AI chip fabrication dominance |

| Tencent Holdings | 7.0% | Platform monetisation recovery; Beijing policy moderation |

More than 34% of the fund sits in three chipmakers whose fortunes are directly tied to AI hardware demand cycles and, in TSMC’s case, Taiwan’s geopolitical stability. The remaining weight is concentrated in Chinese internet and e-commerce platforms that benefited from Beijing moderating its regulatory stance through 2025.

MarketIndex’s ChartWatch analysis, published 5 May 2026, cited ASIA as displaying a “persistent pattern of higher highs and higher lows,” with strong relative strength versus the ASX 200.

The return is explicable rather than extraordinary: it is the product of a cyclical memory recovery, an AI chip demand surge, and a Chinese regulatory reprieve arriving simultaneously across the fund’s three largest sector exposures.

What powers the AI infrastructure thesis, and why AINF is a different kind of AI bet

Most investors hearing “AI ETF” assume a portfolio of chipmakers and software platforms. AINF is deliberately built to avoid that assumption.

The Global X Artificial Intelligence Infrastructure ETF targets companies supplying the physical and energy backbone of AI workloads. Its verified one-year return was 66.12% as of 13 May 2026, with the figure exceeding 65% by the 15 May session. The fund is positioned around what Australian commentators have described as the “picks and shovels” of AI: companies supplying power, cooling, networking and raw materials for data-centre expansion.

| Holding | Approximate Weight | Sector Category |

|---|---|---|

| Delta Electronics | 6.70% | Information Technology (power management) |

| GE Vernova | 5.85% | Utilities / Industrials (power generation) |

| Vertiv | 5.80% | Information Technology (thermal management) |

| Zhongji Innoli | 5.56% | Information Technology (data-centre equipment) |

| Antofagasta | 5.01% | Materials (copper production) |

The fund’s three main sector exposures map directly onto the AI infrastructure supply chain:

- Information Technology: Data-centre equipment makers and thermal management specialists providing the cooling systems that keep AI compute clusters operational.

- Utilities and Industrials: Electric utilities and power infrastructure companies supplying the energy AI data centres consume at scale.

- Materials: Copper and uranium producers furnishing the raw material inputs for power generation and electrical wiring in new facility construction.

Global X positions this as potentially more durable earnings visibility than pure chip plays. Infrastructure capex commitments are multi-year in nature and less sensitive to single-quarter fluctuations in chip demand. For investors seeking AI exposure without concentrating in a single chipmaker or a single country’s regulatory environment, AINF offers a structurally different entry point.

The macro forces converging behind both funds in 2025 and 2026

The all-time highs are not accidental. They are the product of three macro drivers arriving simultaneously, each mapping onto the two funds in distinct ways.

What drove ASIA’s Asian semiconductor and platform rally

AI-driven demand for advanced chip fabrication pushed earnings revisions for TSMC and Samsung into positive territory from 2024 onwards. A cyclical upturn in memory and smartphone demand reinforced the semiconductor recovery. Separately, Beijing’s moderation of its regulatory crackdown on large internet platforms through 2025 stabilised earnings expectations for Alibaba and Tencent, lifting valuations from distressed multiples in 2022-2023 toward growth multiples in 2025-2026.

A weaker Korean won during periods of 2025 also enhanced Korean exporter competitiveness, amplifying AUD-denominated returns for ASIA holders.

What drove AINF’s infrastructure capex rally

Multiple US earnings seasons through 2025 and into 2026 showed hyperscalers committing aggressively to AI-related capital expenditure, particularly into power, cooling, networking and data-centre capacity. These multi-quarter spending commitments flowed directly into earnings upgrades for the infrastructure suppliers AINF holds.

Hyperscaler capex commitments for 2026 sit in the $600-$805 billion range, a figure that contextualises why infrastructure suppliers held by AINF have received sustained earnings upgrades: the spending cycle is operating at a scale that exceeds every prior technology investment peak, including both the dot-com era and the cloud buildout period.

Livewire and ETF-platform commentary described AI infrastructure ETFs as “crowded but still underrepresented in Australian retail portfolios,” noting strong inflows from self-directed investors through 2025. Infrastructure names offered more durable contract visibility than the more volatile chip-cycle exposure powering ASIA’s returns.

The risks Australian investors should weigh before chasing the momentum

Returns of 83% and 65% in 12 months demand a proportionate risk assessment. These are high-return, high-risk funds that have already delivered the bulk of their multi-year gains in a compressed period.

ASIA-specific risks:

- Geopolitical tail risk on Taiwan. TSMC is the fund’s fourth-largest holding at 8.5%. Strategists acknowledge that risk premia on Taiwan assets remain elevated, with cross-strait tensions a structural feature of the fund’s risk profile.

- US export controls. Ongoing restrictions on advanced chip and equipment sales to China continue to pressure parts of the Asian supply chain, even as they entrench non-Chinese fabs as critical suppliers.

- Historical volatility. Motley Fool Australia noted in May 2026 that ASIA experienced large drawdowns in 2021-2022 before its current recovery, consistent with the fund’s high-beta character.

AINF-specific risks:

- Earnings sensitivity to capex expectations. Australian financial media has flagged that earnings for infrastructure suppliers remain sensitive to whether AI capex spending “meets the lofty expectations currently priced in.”

- Liquidity constraints. As a more niche ETF, AINF carries lower ASX trading volumes and wider bid-ask spreads relative to broad-market funds, and advisers suggest using limit orders during volatile sessions.

Both funds carry currency exposure across USD, KRW, TWD and CNY, which can either amplify or dampen returns for Australian investors depending on AUD movements.

For investors considering whether the momentum in ASIA and AINF represents a buying signal or a peak, our dedicated guide to thematic ETF timing risk details how the ARK Innovation ETF reported a +233% time-weighted return while the typical investor experienced approximately -35%, a gap driven by concentrated inflows near peak valuations that is directly relevant to any thematic ETF trading at all-time highs.

Funds delivering 50-80% over 12 months have historically experienced drawdowns of 30-50% in prior cycles. Investors who enter now are buying momentum, not value, and the risk management framework should reflect that reality.

Simultaneous records signal a market no longer treating AI as speculative

The dual all-time highs in ASIA and AINF reflect a market that has moved from treating artificial intelligence as a speculative theme to pricing it as a structural, multi-year infrastructure investment cycle. Five ASX ETFs hitting record or 52-week highs in the same week of 15 May 2026 reinforces that this is broad thematic momentum, not isolated fund performance.

The dot-com era lessons for AI investors remain directly applicable here: being correct about a transformative technology did not translate into correctly identifying the winning companies, and the funds that survived the 2000-2002 drawdown were overwhelmingly those that spread exposure across the value chain rather than concentrating in the most-hyped individual names.

Australian investors now have ASX-listed access to both sides of the AI trade: the demand side through Asian chipmakers and platforms via ASIA, and the supply side through power, cooling and materials via AINF. The two funds serve different risk profiles and time horizons.

Investors considering either fund should weigh their own concentration tolerance, a time horizon of five-plus years (as recommended by most commentators), and whether they are entering a momentum trade or committing to a structural thesis. In an ETF market now exceeding A$330.6 billion, the signal is clear. The risk-reward calculation for new entrants, by definition, is at its most complex.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.