A bank’s licence cancellation is a rare event in Australia. When the Australian Prudential Regulation Authority (APRA) formally revoked in1Bank’s authorised deposit-taking institution (ADI) licence on 4 May 2026, it marked the bureaucratic full stop on a wind-down process that had already returned every depositor’s funds. The revocation was orderly, the financial system absorbed it without disruption, and the Financial Claims Scheme (FCS) was never activated. But the mechanics behind that outcome, and the pattern of neobank-style ADI exits it extends, deserve closer examination. This article explains what in1Bank’s licence revocation involved, how depositor protections operated in practice, and what the departure of another small ADI signals about structural pressures facing digital-first banks in Australia.

What APRA’s revocation of in1Bank’s licence actually means

APRA cancelled in1Bank’s ADI licence on 4 May 2026 under the Banking Act 1959, formally removing the institution from its public register of authorised deposit-taking institutions. The register is the definitive record of which entities hold the legal right to accept deposits from the Australian public, and its update confirmed what had been settled months earlier at the depositor level.

The distinction matters. This was not an emergency intervention triggered by a sudden failure. It was the administrative conclusion of a structured wind-down that APRA had overseen from January 2026.

A rare but significant regulatory action. Industry observers characterised the revocation in those terms, noting APRA’s escalating enforcement posture toward smaller ADIs that struggle to meet ongoing capital and liquidity requirements.

For depositors at any Australian bank, the case illustrates that a licence revocation can follow an orderly, pre-planned process rather than the systemic crisis scenario many associate with a bank losing its licence.

When big ASX news breaks, our subscribers know first

How in1Bank’s depositors were repaid before the licence was cancelled

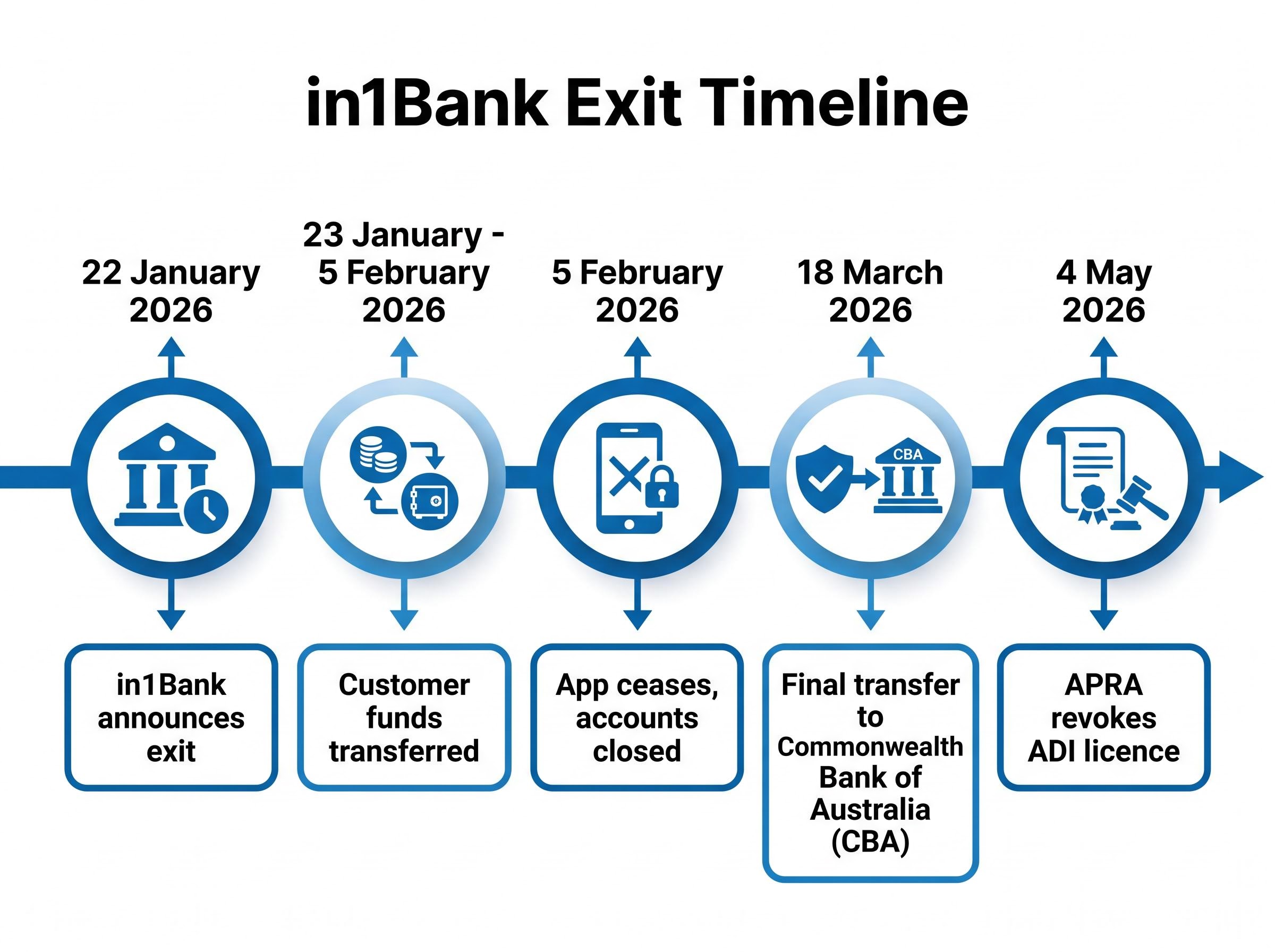

The timeline tells the story. By the time APRA formally revoked the licence, depositor protection had already been completed for months.

| Date | Event |

|---|---|

| 22 January 2026 | in1Bank announces exit from banking and begins return of deposits (ROD) process |

| 23 January – 5 February 2026 | ROD period; customer funds transferred to alternate accounts |

| 5 February 2026 | in1Bank app ceases operation; all accounts closed |

| 18 March 2026 | Final transfer of remaining deposits to Commonwealth Bank of Australia (CBA) |

| 4 May 2026 | APRA formally revokes ADI licence |

The FCS was not activated. Instead, APRA approved a managed voluntary transfer under the Financial Sector (Transfer and Restructure) Act 1999 and the Banking Act 1959, with CBA serving as the receiving institution for remaining deposits. The revocation on 4 May was confirmation of a process already complete, not the trigger for one.

The depositor protection mechanics that kept every in1Bank account holder whole are worth examining in detail, particularly the interaction between APRA’s managed transfer powers and the $250,000 FCS threshold that was never required here, because those same mechanisms would apply if another small ADI faced a similar wind-down.

Key points on FCS coverage for context:

- The FCS protects up to $250,000 per account holder at each APRA-regulated ADI

- It activates when a failed ADI cannot return deposits through normal means

- It was not required here because the managed transfer returned all funds before the licence was formally cancelled

Understanding how Australia’s deposit protection system actually works

In1Bank’s case provides a practical illustration of how Australia’s layered deposit protection framework operates. The FCS, administered by APRA, is the backstop mechanism, designed to activate when an ADI fails and deposits cannot be returned through an orderly process. It covers up to $250,000 per account holder per ADI.

Three conditions generally precede FCS activation:

- The ADI has failed or is unable to meet its obligations to depositors

- No viable managed transfer or structured wind-down can return deposits

- APRA determines that FCS activation is necessary to protect depositors’ interests

In1Bank’s case met none of those conditions. The institution’s wind-down was structured, deposits were returned voluntarily, and a receiving institution (CBA) absorbed the remainder. This is the preferred regulatory pathway when circumstances permit.

An ADI licence authorises an institution to accept deposits from the public, and holding one subjects the institution to APRA’s full suite of prudential standards covering capital adequacy, liquidity, and governance. APRA’s supervisory remit extends across approximately $9.8 trillion in total assets.

When APRA uses managed transfers instead of the FCS

The Financial Sector (Transfer and Restructure) Act 1999 provides the legislative basis for managed transfers. APRA favours this mechanism when the wind-down is solvent, sufficient notice has been provided to depositors, and a viable receiving institution is available to accept the transferred deposits. In1Bank’s case satisfied all three conditions, with CBA receiving the final tranche of deposits on 18 March 2026.

The neobank pattern: why smaller ADIs keep exiting the Australian market

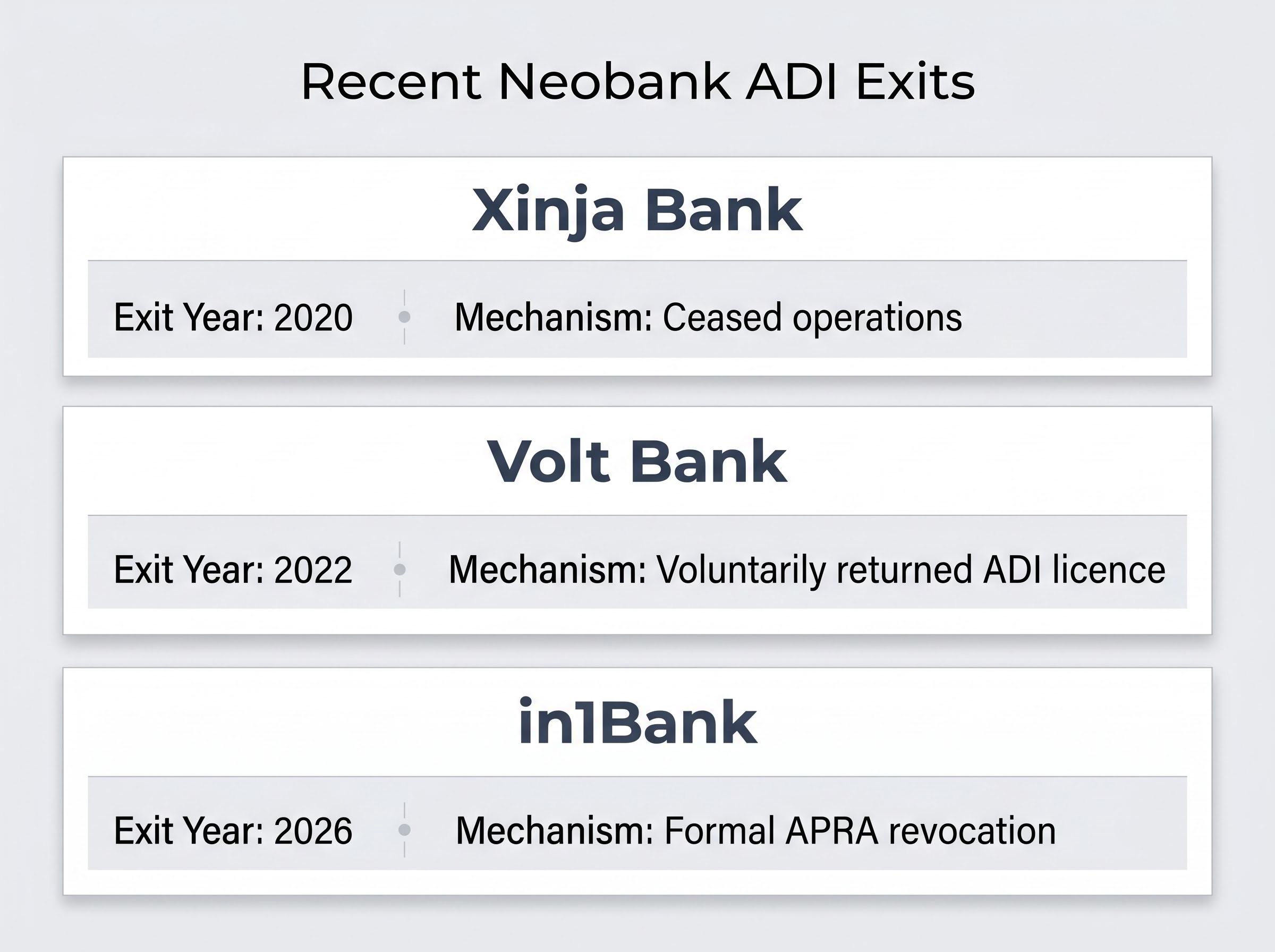

In1Bank is not an isolated case. It is the third notable neobank-style ADI to exit the Australian market in six years.

| Institution | Exit Year | Exit Mechanism |

|---|---|---|

| Xinja Bank | 2020 | Ceased operations |

| Volt Bank | 2022 | Voluntarily returned ADI licence |

| in1Bank | 2026 | Formal APRA revocation |

The sequence is difficult to dismiss as coincidental. The APRA ADI register shows a gradual decline in neobank-style registrations over this period, and each exit followed a similar trajectory: an inability to achieve the deposit and lending scale needed to sustain operations under APRA’s prudential standards.

Volt, Xinja, and the limits of the Australian neobank model

Xinja Bank ceased operations in 2020 after failing to build a sustainable lending business. Volt Bank voluntarily returned its ADI licence in 2022, a process characterised as a “successful failure” in regulatory terms because depositors were repaid without FCS activation, paralleling the in1Bank approach.

The common structural factor across all three is persistent difficulty meeting APRA’s capital adequacy and liquidity requirements without the revenue base that comes from scale. The regulatory framework is designed for institutional resilience; whether it is calibrated in a way that makes the neobank model structurally unviable in Australia remains an open question.

The capital adequacy standards that proved difficult for neobank-scale institutions to sustain are themselves subject to ongoing APRA review, with the regulator currently reassessing its ECAI recognition guidelines alongside broader Basel III implementation and CPS 230 amendments, a pattern that suggests deliberate framework modernisation rather than isolated policy changes.

APRA’s oversight footprint and why even small ADI exits matter

APRA supervises a financial system encompassing approximately $9.8 trillion in total assets on behalf of Australian depositors, policyholders, and superannuation members.

Approximately $9.8 trillion in assets fall under APRA’s supervisory remit as of May 2026.

That remit spans a broad range of regulated entities:

- Banks and mutual institutions

- General insurers and reinsurers

- Life insurers

- Private health insurers

- Friendly societies

- The majority of the superannuation sector

In1Bank’s departure is small in absolute terms relative to this system. Yet APRA’s handling of it demonstrates something that matters at any scale: consistent enforcement of entry and exit standards across the ADI register. The public register itself functions as a transparency mechanism, allowing depositors to verify which institutions hold current licences and are subject to APRA’s prudential oversight.

Confidence in the deposit-taking system depends on that consistency applying regardless of institution size.

APRA’s supervisory posture has sharpened considerably across multiple fronts in 2026, with the regulator issuing a blunt April letter holding boards explicitly accountable for AI governance gaps in banks, insurers, and superannuation trustees, a signal that its willingness to escalate scrutiny extends well beyond ADI entry and exit standards.

The orderly exit as a regulatory template, not an exception

In1Bank’s licence revocation was the final administrative act in a process that had already protected every depositor. The FCS was never activated. Deposits were transferred to CBA through a managed process under the Financial Sector (Transfer and Restructure) Act 1999. APRA’s exit framework functioned as designed.

The pattern of neobank-style ADI exits, from Xinja in 2020 through Volt in 2022 to in1Bank in 2026, does raise a legitimate question about whether Australia’s prudential standards are calibrated in a way that makes the neobank model structurally unviable, and what that means for competition in the retail banking sector.

For readers tracking which institutions currently hold ADI licences, APRA’s public register of authorised deposit-taking institutions remains the authoritative source.

APRA’s public register of authorised deposit-taking institutions is updated to reflect each revocation and new licence grant, providing depositors with a real-time reference to confirm which entities hold the legal right to accept deposits under Australian prudential oversight.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.