When 85% Growth Isn’t Enough: AI Stocks Priced for Perfection

54 mins ago

Westpac has decommissioned 27 legacy systems in just over a year, reduced its product set by roughly 70%, and simplified more than 700 internal processes. Yet it still carries a cost-to-income ratio approximately 3.7 percentage points above the major bank peer average. That gap is precisely why the UNITE programme exists.

Released alongside Westpac’s 1H FY26 results on 5 May 2026, the latest UNITE update confirmed $287 million invested in the first half alone, with full-year guidance reaching $850-900 million. The programme is the most significant structural commitment Westpac has made in years, and it is now deep enough into execution that progress can be evaluated against its original promises.

What follows is an explanation of what UNITE is, how it works in practice, which milestones have already been reached, and what the programme’s trajectory means for Westpac’s competitive position among Australia’s major banks.

Westpac’s cost-to-income (CTI) ratio, the percentage of revenue consumed by operating expenses, stood at 51.7% (excluding notable items) at 1H FY26. That figure sits approximately 3.7 percentage points above the major bank peer average based on FY25 data.

Westpac’s CTI ratio gap: approximately 3.7 percentage points above the major bank peer average, a persistent structural disadvantage rather than a cyclical one.

The gap is not new. Decades of acquisitions and organic growth left Westpac operating multiple overlapping technology stacks, customer systems, and product sets simultaneously. The duplication was not abstract; it was specific and measurable:

Westpac’s 1H26 financial results confirmed the UNITE effect is beginning to show in the income statement, with operating expenses falling 6% and pre-provision profit growing 4% to $5.5 billion, figures that sit behind the CTI ratio improvement the programme is designed to accelerate.

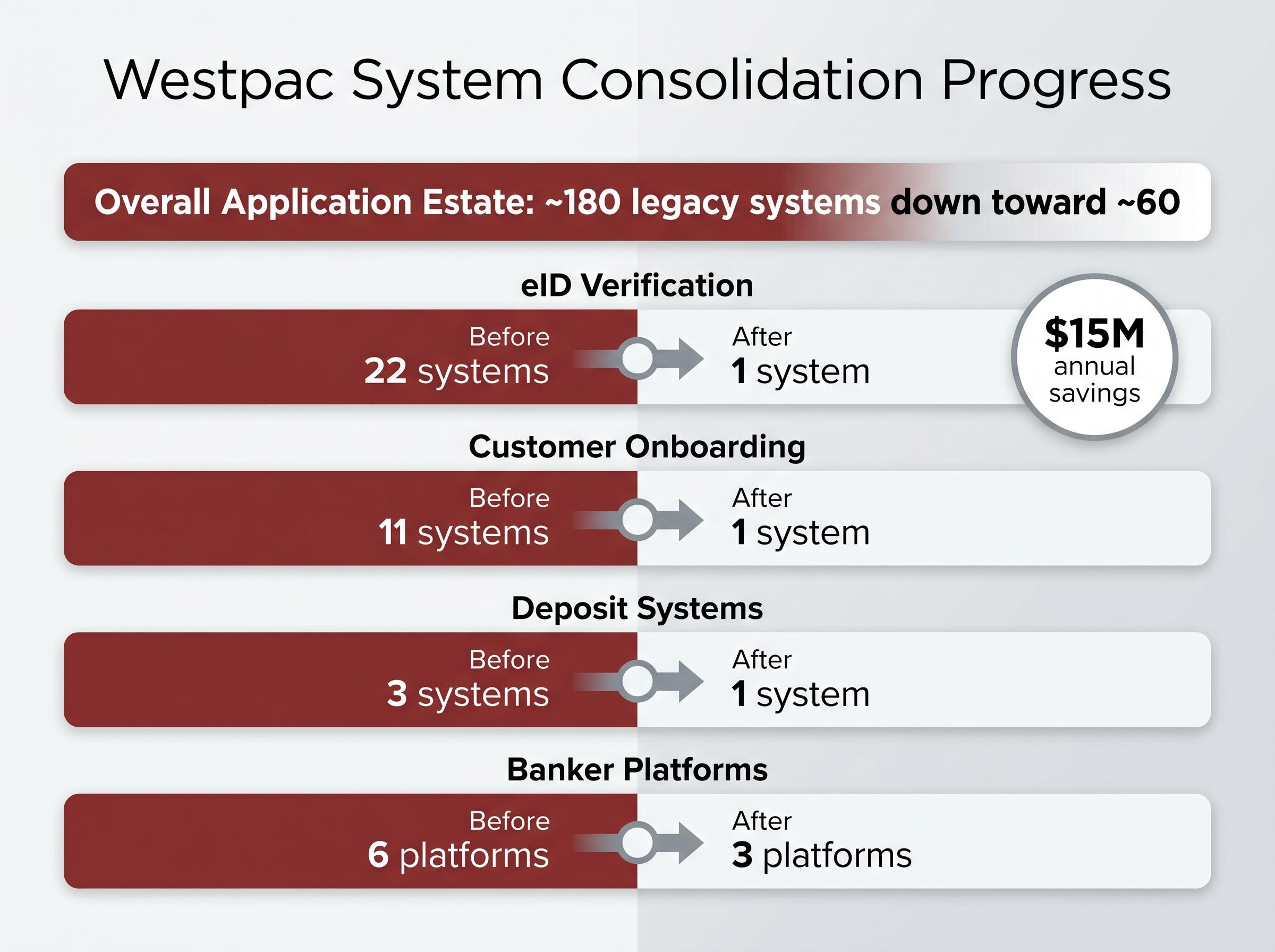

Each duplicated system carried its own maintenance cost, its own vendor contracts, and its own staff. Multiply that pattern across an application estate of approximately 180 systems, and the mechanism linking legacy infrastructure to the CTI ratio gap becomes clear. Every redundant system was a line item pulling the ratio further from peers.

The programme’s target: reduce that estate from approximately 180 systems down toward approximately 60.

UNITE is a sequenced, multi-year simplification initiative running from 2024 through to 2029. Rather than a single technology migration, it is a coordinated portfolio of initiatives designed to consolidate systems, reduce products, and eliminate process duplication across three business segments in deliberate order.

The programme originally comprised 85 separate initiatives. As planning matured and workstreams were merged or completed, that figure consolidated:

That decline from 85 to 57 reflects programme maturation rather than scope reduction. Completed workstreams exit the count, and related initiatives are merged as execution reveals natural overlaps.

The three business segments are addressed in a specific sequence. Consumer simplification, where systems are more standardised and migration volumes are higher, comes first. Business and wealth follows. Westpac Institutional Bank (WIB), where product complexity and bespoke client requirements are greatest, comes last.

| Segment | Focus area | Sequencing priority | Key timeline marker |

|---|---|---|---|

| Consumer | Onboarding, eID, deposits, customer master records | First | Multiple workstreams completed by 1H FY26 |

| Business / Wealth | Commercial platform consolidation, BT Panorama migration | Second | One Commercial Bank targeted December 2027 |

| WIB | Institutional platform rationalisation | Third | Mortgage simplification targeted FY29 |

UNITE accounts for approximately 40% of Westpac’s roughly $2 billion annual group investment envelope, making it the single largest allocation within the bank’s capital expenditure framework. Full-year FY26 investment guidance sits at $850-900 million.

The RAMS mortgage portfolio sale, confirmed as on track for 2H26 completion via a Pepper Money, KKR, and PIMCO consortium, is a related but distinct strand of Westpac’s broader simplification effort, one that reduces balance sheet complexity rather than technology stack duplication.

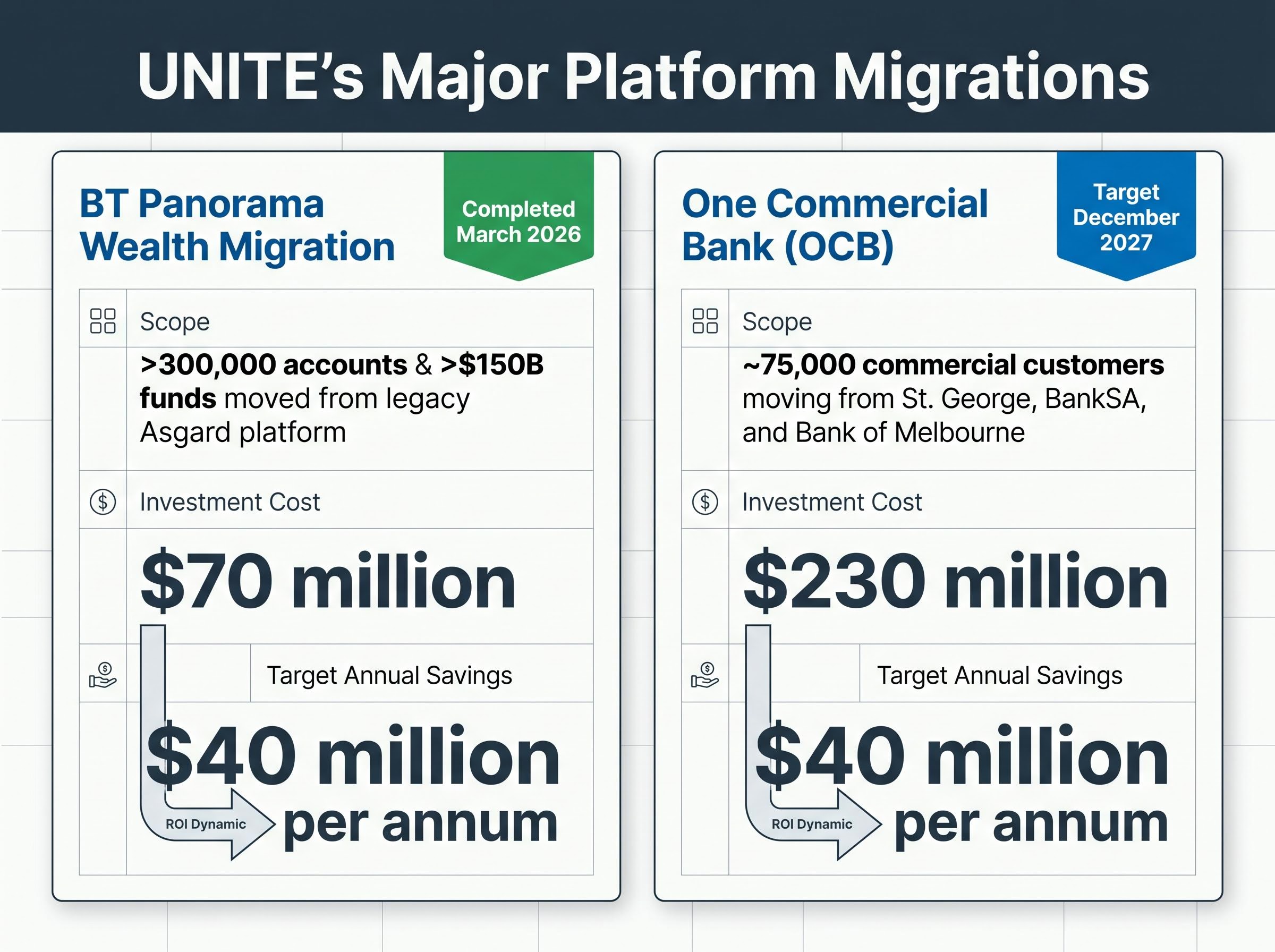

Eight of the programme’s 57 initiatives are now complete. The largest and most consequential is the BT Panorama wealth migration.

Completed in March 2026, the migration moved more than 300,000 accounts and more than $150 billion in funds under administration from the legacy Asgard platform onto BT Panorama. The workstream cost $70 million and is expected to generate $40 million per annum in savings once the Asgard platform is fully decommissioned.

The retail consumer consolidations form a second cluster of completed work. Taken together, they illustrate the pattern UNITE is designed to repeat across the broader estate:

| System category | Before | After | Annual savings |

|---|---|---|---|

| eID verification | 22 systems | 1 system | $15 million |

| Customer onboarding | 11 systems | 1 system | Not separately disclosed |

| Deposit systems | 3 systems | 1 system | Not separately disclosed |

| Banker platforms | 6 platforms | 3 platforms | Not separately disclosed |

| BT Panorama migration | Asgard + Panorama | Panorama only | $40 million |

Across the broader programme, 27 legacy systems have been decommissioned to date, including 9 in 1H FY26 alone.

Total productivity benefits realised to date: more than $550 million.

That aggregate figure is the clearest available signal that the programme is translating planning into operating results. Whether the pace of realisation accelerates from here depends on the workstreams now in motion.

The largest single initiative currently underway is One Commercial Bank (OCB), formally announced in March 2026 and reported by the Australian Financial Review on 23 March 2026.

OCB will migrate approximately 75,000 commercial customers from legacy platforms operated under three subsidiary brands onto a single Westpac commercial banking platform. The three brands involved:

The workstream carries a cost of $230 million and a target completion date of December 2027. Upon completion, it is expected to deliver $40 million per annum in ongoing savings.

OCB investment: $230 million. Expected annual savings upon completion: $40 million per annum.

Westpac has characterised the migration as requiring minimal action from affected customers, with the focus on delivering consistent experiences and expanded digital capabilities across the consolidated platform.

The return profile mirrors the pattern established by the BT Panorama migration: a large upfront capital commitment followed by a recurring annual savings stream that, if sustained, recovers the investment over approximately six years. OCB’s December 2027 target makes it the clearest near-term test of whether Westpac can execute complex, customer-facing migrations on schedule and within budget.

If the full programme delivers, Westpac has stated its aspiration is to reach top-decile efficiency by 2029. That target would represent a structural reset of the bank’s cost base, not simply an incremental improvement.

APRA’s quarterly ADI performance statistics provide the official cost-to-income benchmarks against which Australia’s major banks are measured, confirming that the efficiency gap Westpac is working to close is a sector-wide structural metric rather than an internally constructed target.

The remaining execution stages, in approximate sequence:

Alongside the system work, more than 700 processes have been simplified and the product set has been reduced by approximately 70%. These figures represent the broader organisational decluttering that accompanies the technology consolidation.

Technology transformation programmes of this scale typically require sustained investment before savings accumulate. The BT Panorama migration illustrates the dynamic precisely: $70 million in upfront cost, followed by $40 million per annum in savings. The investment is discrete; the savings are recurring. It takes time for the latter to overtake the former.

At the programme level, Westpac invested $287 million in 1H FY26 alone, with FY26 guidance at $850-900 million. Total productivity benefits realised to date stand at more than $550 million. The net position remains in investment-leading territory, meaning cumulative spend still exceeds cumulative savings.

This is structurally expected. The heaviest investment years for a programme of this kind precede the heaviest savings years, because systems must be built, migrated, and decommissioned before their maintenance costs disappear. The question is not whether the lag exists but whether the savings trajectory is accelerating quickly enough to justify the ongoing capital commitment.

With roughly 10% of targeted application decommissioning achieved as of 1H FY26, the majority of the programme’s savings potential remains unrealised. The most capital-intensive workstreams, OCB and mortgage simplification, are also the ones with the longest lead times.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Westpac’s situation is not unique. Every major Australian bank that grew through acquisition carries some version of the same problem: overlapping systems inherited from absorbed institutions, each with its own technology stack, product architecture, and process layer.

Several parallels extend beyond Westpac specifically:

Market reaction has been mixed. Westpac shares rose 1% to $40.83 following the March 2026 UNITE briefing, with coverage highlighting the decommissioning progress and product reduction figures as tangible evidence. Shares subsequently fell 2.26% to $37.62 on 5 May 2026 following the 1H FY26 results, suggesting that the broader earnings context, rather than UNITE progress alone, drove the session’s pricing.

The market’s mixed reaction to UNITE progress reflects a broader tension: Morgans issued an analyst sell rating on Westpac in April 2026 with a $34.04 price target, implying the programme’s structural promise has not yet been sufficient to justify the share price’s 12-month re-rating at a trailing P/E of 21.39.

UNITE is a real-time test case: whether an incumbent Australian financial institution can engineer its way out of a structural cost disadvantage through technology, without disrupting customers, losing competitive ground, or exceeding its own budget. The answer will take years to arrive in full.

Eight initiatives complete. Forty-nine ongoing. More than $550 million in productivity benefits realised. Roughly 10% of the targeted application decommissioning achieved. Those figures describe a programme that has demonstrated it can execute on discrete workstreams, particularly in the consumer and wealth segments where the early wins were concentrated.

The tension sits in the distance still to travel. The One Commercial Bank migration, at $230 million, is the most capital-intensive workstream in motion, with a December 2027 target that will test execution capability on complex, customer-facing consolidation. Mortgage simplification, the longest-dated workstream, extends to FY29. The top-decile efficiency aspiration attached to that same year remains an ambition rather than a forecast.

What the track record to date provides is a basis for evaluating execution quality: milestones met, savings confirmed, systems decommissioned. The milestones to watch in FY27 are whether OCB progresses on schedule, whether the decommissioning pace accelerates from its current 10% baseline, and whether the cumulative savings trajectory begins to close the gap on cumulative investment. Those markers will determine whether UNITE delivers on the structural promise its early results have suggested.

For investors wanting to connect UNITE’s progress to Westpac’s headline financial performance, our full explainer on Westpac’s 1H26 profit result breaks down the statutory net profit, dividend, ROE, and capital ratio figures that frame the transformation programme’s commercial context.

These forward-looking statements regarding UNITE’s targets and projected outcomes are subject to change based on market developments and programme execution.

The Westpac UNITE program is a multi-year technology simplification initiative running from 2024 to 2029, designed to consolidate legacy systems, reduce the bank's product set, and eliminate process duplication across its consumer, business, and institutional banking segments.

Westpac invested $287 million in the first half of FY26 alone, with full-year FY26 guidance set at $850-900 million, representing approximately 40% of the bank's roughly $2 billion annual group investment envelope.

The UNITE program has realised more than $550 million in total productivity benefits to date, decommissioned 27 legacy systems, reduced the product set by approximately 70%, and simplified more than 700 internal processes.

One Commercial Bank is a $230 million workstream targeting completion in December 2027, which will migrate approximately 75,000 commercial customers from St. George, BankSA, and Bank of Melbourne legacy platforms onto a single Westpac commercial banking platform, expected to deliver $40 million per annum in ongoing savings.

The BT Panorama migration was the largest completed UNITE initiative, moving more than 300,000 accounts and over $150 billion in funds under administration from the legacy Asgard platform at a cost of $70 million, with expected annual savings of $40 million once Asgard is fully decommissioned.