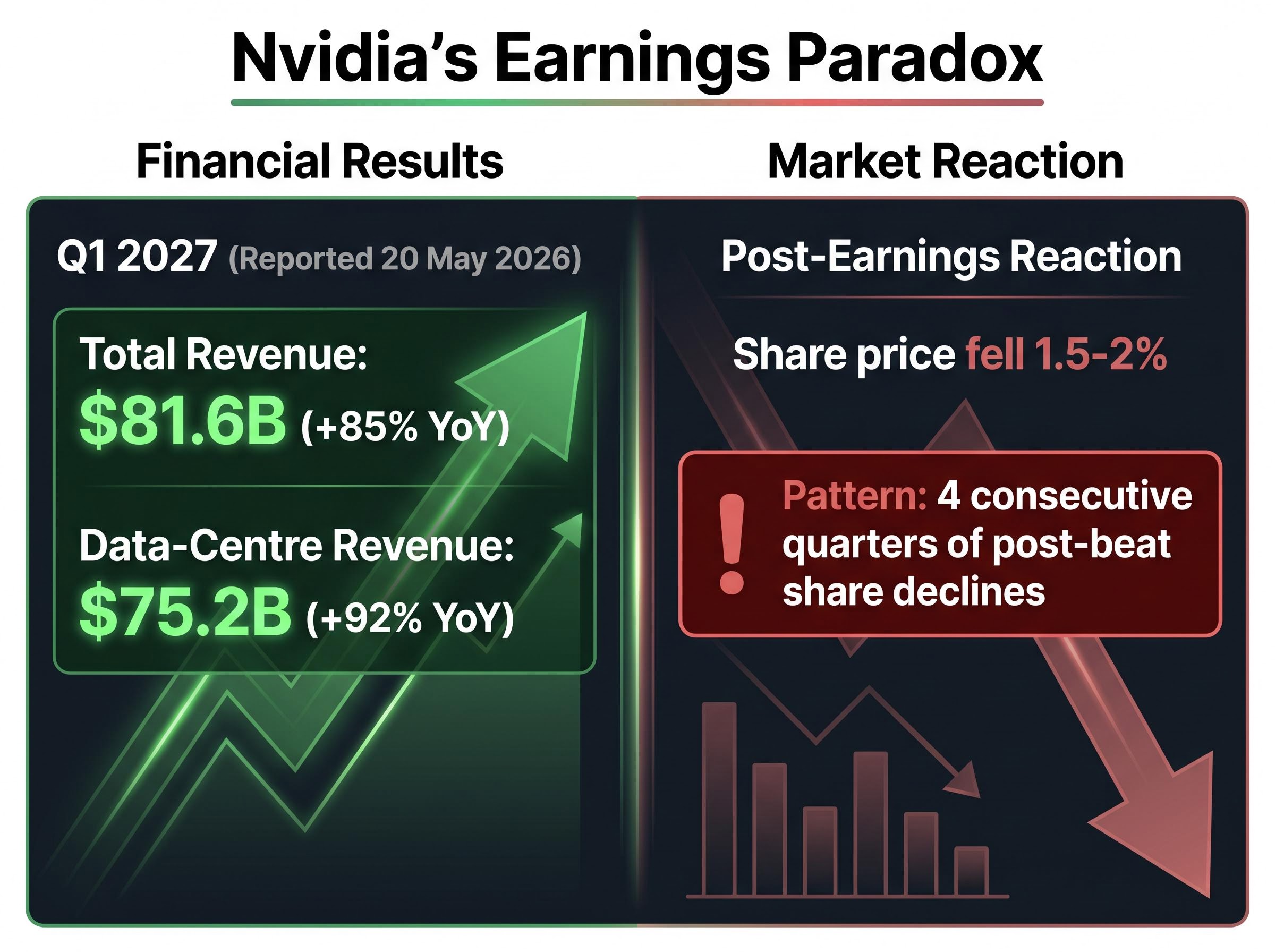

Nvidia just reported 85% earnings growth and $75.2 billion in data-centre revenue for the quarter ending May 2026. Its share price fell roughly 1.5-2% in the sessions that followed.

That gap between the strength of the result and the weakness of the reaction is the story. For Australian investors with exposure to global AI-linked equities, whether through direct holdings, ETFs, or ASX-listed infrastructure proxies, understanding why markets responded this way is now a practical allocation question. This article breaks down the mechanics behind the muted reaction, examines what institutional analysts say about where AI stock valuations actually sit, and identifies what the divergence between mega-cap AI leaders and smaller names means for Australian investors positioning their AI exposure in the second half of 2026.

Record results, subdued price action: reading Nvidia’s post-earnings signal

The headline numbers from Nvidia’s fiscal Q1 2027 results, reported on 20 May 2026, were unambiguous:

- Total revenue: $81.6 billion, up 85% year-over-year

- Data-centre revenue: $75.2 billion, up 92% year-over-year

- Earnings beat consensus expectations for the fourth consecutive quarter

Shares responded positively intraday before reversing, closing down approximately 1.5-2% in the sessions following the release. The intraday fade was not a one-off.

Wolfe Research had flagged ahead of the release that another double beat could prompt investors to exit rather than build positions, a pattern consistent with the prior two years of results; analysts at William Blair separately identified a guidance threshold for a genuine beat at $90 billion in Q2 revenue, meaning anything short of that number would read as a miss regardless of the headline figures.

Nvidia has now recorded four consecutive quarters in which shares declined after beating earnings expectations, a pattern that speaks less to the quality of the business than to the price the market had already assigned it.

That distinction matters. A stock that falls after delivering record results is sending a signal about its valuation, not its fundamentals. For Australian investors holding Nvidia directly or through global technology ETFs, the question is no longer whether AI is growing. It is whether the growth is surprising relative to what the share price already assumes.

When big ASX news breaks, our subscribers know first

How expectations get baked into prices: the mechanics of “priced for perfection”

The confusion is reasonable. How does 85% revenue growth fail to move a stock higher?

The answer sits in a concept that Morningstar Australia has applied directly to the US AI complex: parts of this market are “priced for perfection.” Ameya Hattangadi, Associate Portfolio Manager at Morningstar Investment Management Australia, and Mark LaMonica, Director of Personal Finance at Morningstar Australia, have both characterised individual earnings announcements as having less influence on market movements than previously observed. The implication is that the market has already embedded exceptional future performance into share prices.

When a stock’s valuation already reflects analysts’ most optimistic projections, even a genuine beat provides no upside surprise. The result confirms what the price assumed. There is no new information to reprice.

Consider two scenarios:

- A stock priced conservatively beats expectations. The market reprices upward because the beat reveals something the price did not yet reflect. The share price rises.

- A stock priced for perfection beats expectations. The result confirms what the price already assumed. There is no new information to reprice. The share price moves sideways or falls as some holders take profits.

What “priced for perfection” actually means in practice

In plain terms, a stock priced for perfection has already absorbed the best-case scenario into its current price. There is no room for positive surprise, only room for disappointment.

This dynamic is amplified for long-duration growth stocks like Nvidia, where a significant portion of the valuation depends on earnings projected years into the future. Those distant earnings are more sensitive to changes in interest rates and investor risk appetite. When the discount rate shifts even modestly, the present value of those future cash flows compresses, making the stock more vulnerable regardless of near-term results.

Mega-caps versus the rest: a widening AI valuation divide

“AI stocks” is no longer a single category. The performance and valuation gap between mega-cap AI leaders and smaller or pure-play AI names has widened materially through 2025 and into 2026, with capital flows and total returns heavily skewed toward the largest names.

America’s technology giants, including Nvidia, Microsoft, Apple, and Google, now account for approximately 40% of S&P 500 value, according to ABC News Australia reporting from the 2025-2026 period. The S&P 500 sat at or near all-time highs as of late May 2026, but those gains are concentrated in a handful of mega-caps rather than distributed broadly.

The Reserve Bank of Australia has flagged US technology concentration as a macro-financial concern, with some observers cited in ABC News Australia coverage characterising the AI boom as “starting to resemble a bubble.”

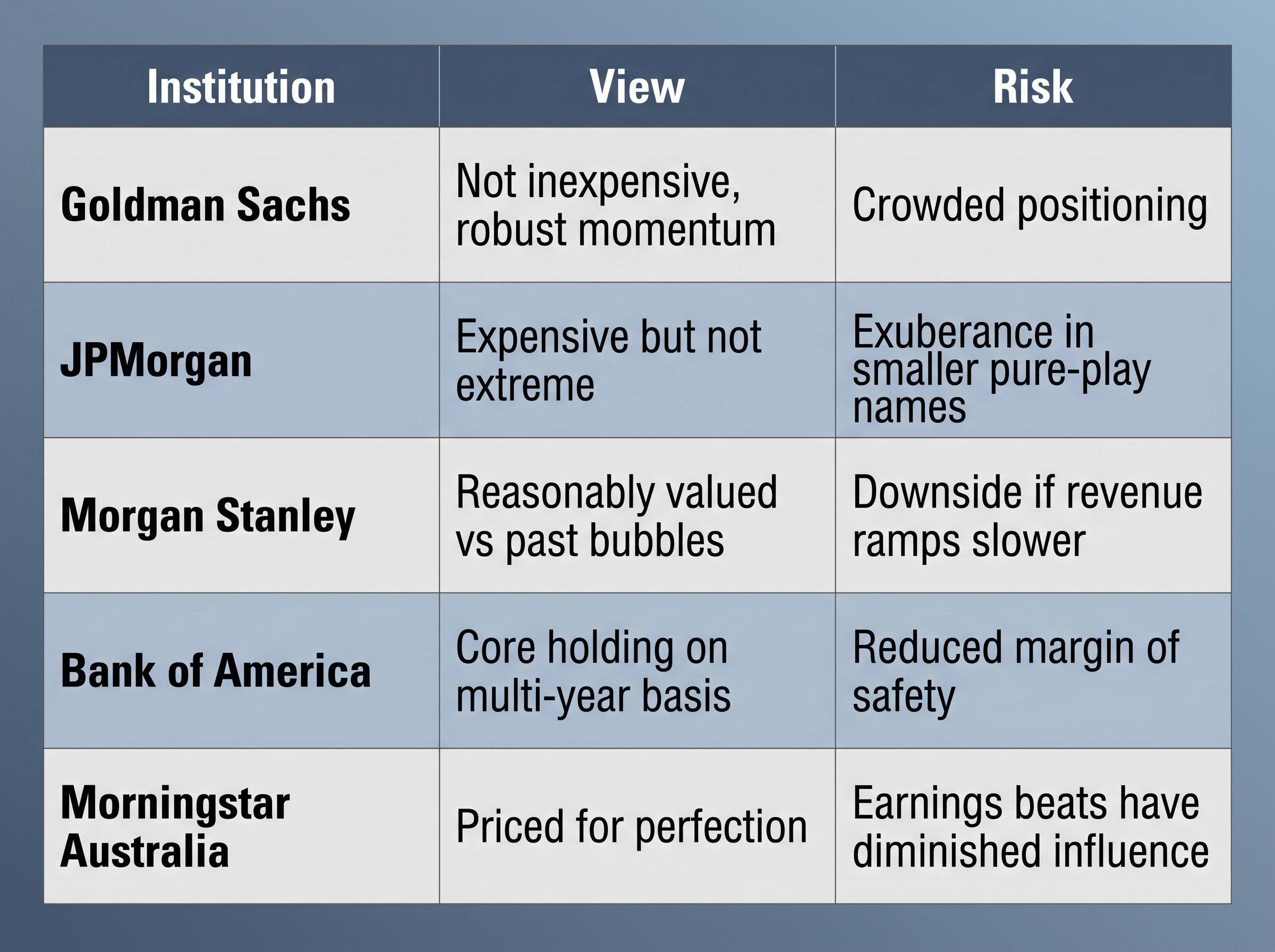

How the major institutions characterise AI mega-cap valuations varies in tone but converges on the same core message:

| Institution | Mega-cap AI valuation view | Key caveat |

|---|---|---|

| Goldman Sachs | Not inexpensive, but supported by robust earnings momentum | Crowded positioning is the primary concern |

| JPMorgan | Expensive but not extreme | Pockets of exuberance in smaller, pure-play AI names |

| Morgan Stanley | Reasonably valued on forward earnings relative to past bubbles | Meaningful downside risk if AI revenue ramps slower than expected |

| Bank of America | Core portfolio holdings on a multi-year earnings basis | Reduced margin of safety at current levels |

| Morningstar Australia | Overvalued to fairly valued; priced for perfection | Individual earnings beats have diminished pricing influence |

The shared conclusion: the greatest valuation risk is not in the mega-caps themselves but in high-multiple smaller or pure-play AI names. For Australian investors, this distinction matters directly. An AI-themed ETF holding smaller names carries a different risk profile than an index fund dominated by mega-caps, and the blended label “AI stocks” obscures that difference.

Three independent valuation frameworks, including the Buffett Indicator sitting at 223.6% and well above dot-com bubble peaks, an unfavourable equity earnings yield versus Treasury yield spread, and a near-absence of margin-of-safety buying opportunities, have converged simultaneously on the same overvaluation conclusion, providing the broader market-level context within which Nvidia’s priced-for-perfection dynamic sits.

JPMorgan Asset Management’s 2026 equity valuation outlook advises investors to consider reducing concentration in overvalued sectors, a position that reinforces the broader institutional consensus that crowded positioning in high-multiple technology names carries asymmetric downside risk even when underlying earnings remain strong.

The macro backdrop that makes AI valuations harder to read right now

AI equity valuations do not exist in isolation. Three distinct macro risk channels are actively distorting the valuation signal:

- US interest rate path: The “higher for longer” stance from the Federal Reserve directly compresses the present value of long-duration growth stocks, making the Fed’s trajectory a co-determinant of AI stock prices alongside earnings.

- Geopolitical inflation risk: Ongoing uncertainty around Iran and the Middle East creates potential supply-side inflation pressure. ABC News Australia reported that markets were effectively “betting that war in the Middle East will soon be over,” with a ceasefire described as on “shaky ground.” If conflict escalates, the resulting inflationary impulse would worsen the interest rate outlook and further pressure high-multiple equities.

- Domestic RBA policy: The Reserve Bank of Australia continues to flag persistent inflation risk, with Assistant Governor Sarah Hunter outlining how the RBA uses its frameworks to respond to inflation and growth data in remarks to the Bloomberg Forum for Investment Managers.

The interaction between Fed rate decisions and mega-cap earnings has become increasingly difficult to separate as a valuation signal: with the 10-year Treasury yield near 4.64-4.65% and derivative markets pushing the next anticipated rate cut to late 2027, even a strong earnings beat from a long-duration growth stock faces an immediate headwind from the discount rate that partially offsets the fundamental good news.

Ameya Hattangadi at Morningstar Investment Management Australia has characterised the near-term outlook as presenting an “unusually broad range of potential scenarios,” with the favourable case being a return to AI-earnings-driven markets as geopolitical concerns recede. That breadth of outcomes makes any single valuation reading less reliable.

How Australian rate and policy dynamics add a local layer

RBA policy decisions, shaped by domestic inflation and growth data, affect the Australian dollar and local investor appetite for high-growth global equities. A persistently cautious RBA, combined with an active stance monitoring US mega-cap concentration risk, creates a compounding headwind for Australian investors overweighted in AI-linked global holdings. When both global rate expectations and domestic policy lean hawkish, the cost of maintaining concentrated high-multiple positions rises from both directions.

What Australian investors are actually doing with AI exposure

The abstract valuation debate has already produced a pragmatic shift in how Australian investors are accessing AI themes. ABC News Australia reporting from the 2025-2026 period shows local investors gaining AI exposure primarily through ASX-listed data-centre infrastructure and property names, specifically Goodman Group and Infratil, rather than through direct Nvidia or US software equity ownership.

Morningstar Australia has reinforced this approach with a four-point portfolio framework:

- Assess valuations against fair value, not just earnings growth rates

- Favour AI-adjacent infrastructure over highest-multiple pure plays

- Widen diversification beyond equity-bond pairs, given that the conventional bond-equity offset has become less reliable (both asset classes declined simultaneously in 2022 and again in earlier 2026, according to Morningstar analysis)

- Focus on quality and cash flow in an elevated-rate environment

Morningstar has also cited selected consumer names such as LVMH, Burberry, and Nike as undervalued diversification candidates for portfolios overconcentrated in growth themes.

The case for AI-adjacent infrastructure over direct chip exposure

Data-centre REITs and infrastructure names like Goodman Group benefit from AI capital expenditure growth without carrying the same valuation premium as the chipmakers and software platforms driving that spending. They collect rent and service fees from the AI buildout regardless of which specific AI company wins the revenue race.

The trade-off is real. Lower valuation risk comes with lower upside if AI earnings continue to beat expectations at the mega-cap level. But in an environment where even Nvidia’s record quarter failed to lift its share price, the risk-adjusted case for infrastructure exposure has strengthened.

One quarter’s results do not resolve a structural valuation question

Nvidia’s four consecutive post-beat share price declines are not a market malfunction. They are a rational response from a market that has already priced in exceptional performance and is now being pulled in multiple directions by macro uncertainty.

The forward question for Australian investors is not whether AI is growing. It clearly is. The question is whether the growth rate is surprising relative to what is already embedded in prices, and whether the macro environment is stable enough for those price levels to hold.

The key investor question is not whether AI is working but whether markets already know it is.

Morningstar Australia’s framework of quality, cash flow, diversification, and AI-adjacent infrastructure exposure over high-multiple direct positions represents a defensible approach in the current environment. Australian investors who frame their allocation decisions around the right question will be better positioned than those evaluating AI stocks purely on revenue growth rates.

For Australian investors wanting to implement an infrastructure-tilted AI allocation through ASX-listed ETFs rather than individual stocks, our dedicated guide to AINF and IFRA compares Global X’s concentrated data-centre equipment fund against VanEck’s broader infrastructure fund with its AUD currency hedge, including year-to-date return data, management expense ratios, and entry-point guidance for each.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.