The S&P 500 is hovering near all-time highs in late May 2026, yet some of the world’s most recognisable consumer brands are trading at meaningful discounts to what Morningstar analysts believe they are worth. A confluence of forces has driven investors away from consumer-facing equities and toward AI-related names: China’s prolonged luxury spending slump, geopolitical uncertainty, sticky inflation, and rising cost-of-living pressures. That rotation has left a cluster of wide-moat consumer brands, including LVMH, Burberry, and Nike, looking attractively priced relative to intrinsic value estimates, according to Morningstar analysis. What follows is an examination of the investment case Morningstar is building around these three stocks, an explanation of what economic moat ratings mean for long-term investors, and an assessment of how undervalued consumer stocks fit into a diversified Australian portfolio at a time when the traditional 60/40 construction is under strain.

Why the market has soured on consumer brands at exactly the wrong time

The conditions driving investors away from consumer discretionary are precisely the conditions that have historically created the best long-term entry points. AI sector enthusiasm and macro anxiety are working in concert to depress valuations, producing a bifurcated market where capital chases momentum in one direction and abandons quality in another.

Consider Nvidia’s Q1 FY2027 earnings: 85% year-on-year profit growth, data centre revenue of approximately $75 billion. A year ago, those numbers would have sent the stock surging. The market reaction was muted. When even blockbuster AI results stop moving prices the way they once did, the question of where that capital rotates next becomes unavoidable.

Ameya Hattangadi, Associate Portfolio Manager at Morningstar Investment Management Australia, has characterised the current S&P 500 levels as a potential disconnect from the underlying economic picture.

Morningstar Investment Management Australia views S&P 500 levels near all-time highs as a potential disconnect relative to prevailing macroeconomic uncertainties, creating a relative value argument for out-of-favour consumer names.

For Australian investors with heavy exposure to US tech or domestic equities, the current rotation away from consumer stocks may represent a mispriced opportunity rather than a justified de-rating. The rest of this analysis examines whether that thesis holds.

When big ASX news breaks, our subscribers know first

The macro headwinds battering consumer stocks (and why they may be temporary)

Four headwinds are bearing down on consumer-facing equities simultaneously. Geopolitical tensions, including Iran-related supply-side risks, have elevated uncertainty across global markets. Sticky inflation continues to compress discretionary spending budgets. Rising cost-of-living pressures are hitting middle-income consumers hardest; and China’s luxury demand slowdown has removed the single most important growth engine for premium consumer brands.

The weight of these headwinds is real. The question Morningstar analysts are posing is whether they impair long-term brand value or temporarily suppress reported earnings. That distinction separates a buying opportunity from a value trap.

US-China trade tensions have added a geopolitical layer to the luxury demand equation that sits beneath the headline spending figures, with the May 2026 Beijing summit producing a preliminary consensus on tariffs and procurement commitments while leaving the critical details of implementation timelines and sectoral exposures formally unresolved.

What China’s luxury slump actually signals

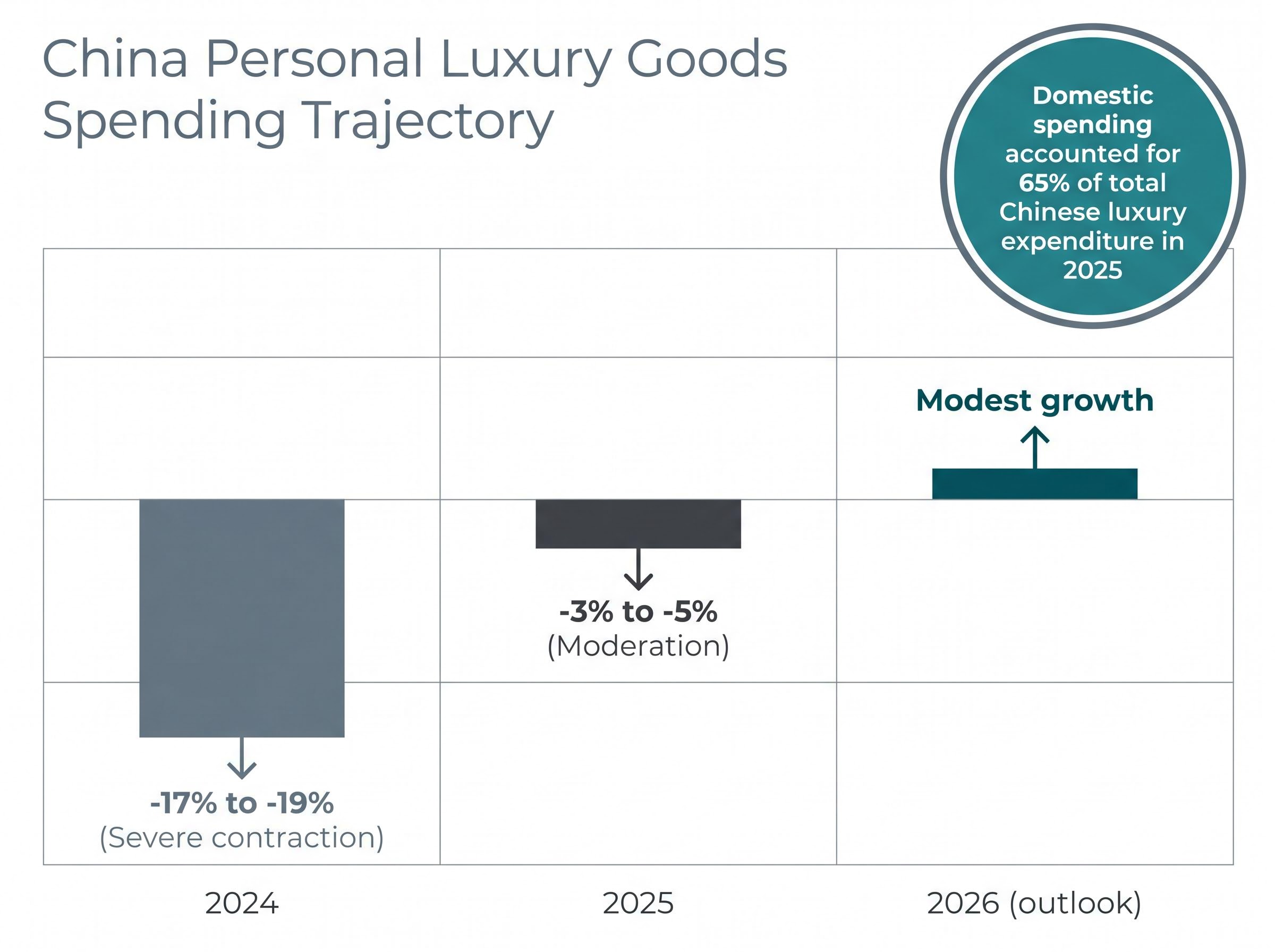

The China luxury contraction has been severe. According to Bain & Company and Altagamma’s January 2026 report, mainland personal luxury goods spending fell 17-19% in 2024, moderating to a 3-5% decline in 2025. The 2026 outlook calls for modest expansion, though Bain characterises the recovery as fragile and uneven.

Bain & Company’s January 2026 luxury market report confirms that mainland China personal luxury goods spending contracted 3-5% in 2025, a significant moderation from the 17-19% decline recorded in 2024, with the recovery characterised as fragile and unevenly distributed across brand tiers.

| Year | Change (%) | Characterisation |

|---|---|---|

| 2024 | -17% to -19% | Severe contraction; post-pandemic normalisation, property stress |

| 2025 | -3% to -5% | Moderation; stabilisation signals from Q3 onward |

| 2026 (outlook) | Modest growth | Fragile, uneven recovery (Bain & Company projection) |

A two-speed dynamic is emerging. Top-tier brands with strong pricing power are better positioned to capture recovering demand, while aspirational and accessible luxury names face continued pressure. Domestic Chinese luxury spending accounted for 65% of total Chinese luxury expenditure in 2025, and that domestic component is stabilising faster than overseas spending. For brand-specific recovery timelines, where a company sits on the pricing-power spectrum matters as much as the headline figures.

What economic moat ratings mean and why they matter for beaten-down stocks

When a stock falls sharply, the first question is whether it is genuinely undervalued or simply cheap for good reason. Morningstar’s economic moat framework provides one structured approach to answering that question.

An economic moat is a structural competitive advantage that allows a company to earn returns above its cost of capital for an extended period. Morningstar assigns three ratings:

- Wide Moat: A durable advantage expected to persist for at least 20 years

- Narrow Moat: A competitive advantage expected to persist for at least 10 years

- No Moat: No meaningful structural advantage identified

For consumer brands specifically, three moat sources are most relevant:

- Intangible assets: Brand value and pricing power that allow a company to charge premium prices without losing customers

- Switching costs: The financial, practical, or emotional cost to a consumer of changing brands or suppliers

- Scale advantages: Cost efficiencies that smaller competitors cannot replicate, particularly in manufacturing and distribution

The reason moat ratings matter most during cyclical weakness is that a wide-moat company’s intrinsic value is driven by long-term earnings power, not a single year of depressed results. A bad quarter does not erode a decades-old brand franchise.

Morningstar’s framework identifies five sources of competitive advantage that qualify as genuine moats: intangible assets, switching costs, network effects, cost advantage, and efficient scale, with companies possessing multiple reinforcing sources considered meaningfully more durable than those relying on a single driver. For readers wanting a structured way to apply this framework beyond the three stocks discussed here, our dedicated guide to economic moat investing covers each source with ASX examples and explains why moat trajectory — whether an advantage is widening or eroding — matters as much as the initial classification.

| Company | Moat Rating | Uncertainty | Key Moat Source | Primary Risk |

|---|---|---|---|---|

| LVMH | Wide | Medium | Brand intangibles (Louis Vuitton, Dior); pricing power | China demand recovery timing |

| Burberry | Narrow | High | Brand heritage; outerwear identity | Repositioning execution risk |

| Nike | Wide | High | Brand intangibles; distribution scale | Turnaround timing and magnitude |

For Australian investors unfamiliar with Morningstar’s framework, this distinction transforms what follows from a list of discounted stocks into a replicable methodology for evaluating quality businesses during market dislocations.

The valuation gap: how far each stock is trading below fair value

Start with LVMH. Morningstar’s Fair Value Estimate sits at approximately €620 per share, with a Medium Uncertainty rating. Recent trading has ranged between approximately €472 and €507, placing the stock at a material discount to that estimate. The normalised P/E of roughly 21-22x is reasonable for a luxury conglomerate anchored by the Fashion and Leather Goods division, which generates over half of group profits.

Burberry presents a more nuanced picture. The Fair Value Estimate of GBX 1,370 carries a High Uncertainty rating, and the normalised P/E of approximately 59-60x is elevated relative to peers. That multiple reflects expectations of earnings recovery from the ongoing brand repositioning, not current profitability. If the repositioning succeeds, the current valuation may appear reasonable on a forward basis. If it does not, the multiple compresses.

Then there is Nike. The Fair Value Estimate ranges between $102 and $117. Recent trading has been around $44-$45. The implied discount is the largest of the three, and the High Uncertainty rating acknowledges that the turnaround’s timing and magnitude remain genuinely uncertain.

| Company | Fair Value Estimate | Approx. Current Price | Moat Rating | Uncertainty |

|---|---|---|---|---|

| LVMH | ~€620/share | €472-€507 | Wide | Medium |

| Burberry | GBX 1,370 | Below FV estimate | Narrow | High |

| Nike | $102-$117 | ~$44-$45 | Wide | High |

All fair value estimates cited above are Morningstar analytical figures and have not been independently verified by this publication. Fair value estimates represent long-term intrinsic value calculations, not short-term price targets. The timeframe for convergence between market price and estimated fair value is genuinely uncertain.

Knowing the size of each discount, and the uncertainty rating accompanying it, allows investors to calibrate position sizing and risk tolerance rather than treating all three stocks as equivalent opportunities.

Where these stocks fit in an Australian investor’s portfolio right now

The traditional 60/40 portfolio relied on a negative correlation between bonds and equities: when stocks fell, bonds rallied, cushioning portfolio drawdowns. That relationship has broken down. The simultaneous bond and equity sell-offs of 2022, and again earlier in 2026, demonstrated that during inflation or stagflation episodes, both asset classes can decline together.

Ameya Hattangadi and the Morningstar Investment Management Australia team have recommended broadening diversification beyond traditional equity-bond allocations, with real assets and alternatives referenced as complementary holdings.

Portfolio diversification beyond domestic equities becomes more urgent when the bond-equity correlation breaks down, because Australian investors who rely on the ASX for equity exposure are simultaneously concentrating in banks and miners, which account for approximately 52% of the S&P/ASX 200, while assuming bond holdings will cushion drawdowns that 2022 and early 2026 demonstrated they may not.

Against that backdrop, quality consumer brands trading at discounts to intrinsic value offer a potential source of differentiated return. But they introduce portfolio-level considerations that individual stock analysis does not capture.

Currency and concentration risks Australian investors should account for

Three specific risks warrant attention:

- Correlation risk: The breakdown in bond-equity correlation means adding international equities without considering their correlation profile may not deliver the diversification benefit investors assume

- China concentration: Owning LVMH, Burberry, and Nike together amplifies rather than diversifies China macro exposure; the thematic overlap is not visible from any single stock’s fact sheet

- Currency exposure: Unhedged positions introduce AUD/EUR variability for LVMH and AUD/USD variability for Nike, adding a layer of return uncertainty that compounds the underlying equity risk

These are not reasons to avoid the stocks. They are reasons to size positions deliberately and to understand what the aggregate portfolio looks like after adding them.

The long-term case: patience, volatility, and the return to fundamentals

Morningstar’s framing treats current volatility as normal market behaviour, not evidence of structural impairment to these brands.

Morningstar Australia has characterised volatility as a normal feature of investing that long-term investors should expect rather than fear, particularly when owning wide-moat businesses purchased at discounts to fair value.

For the bull case to play out, three conditions need to materialise:

- China’s luxury recovery gains traction, supported by government stimulus measures and gradually improving consumer confidence

- Nike’s turnaround under CEO Elliott Hill delivers earnings normalisation, with improving wholesale relationships and inventory management

- Burberry’s repositioning succeeds in rebuilding margin, with May 2026 earnings showing early signs of improving comparable sales

If geopolitical tensions worsen, inflation re-accelerates, or the China recovery stalls, the timeline to fair value convergence extends materially. Mark LaMonica, CFA, Director of Personal Finance at Morningstar Australia, has positioned luxury stocks as long-term buying opportunities in publications dating from September 2025 through 2026, though with consistent acknowledgement that patience is a prerequisite.

This opportunity suits investors with time horizons long enough to absorb further near-term drawdowns and genuine conviction in the moat durability of these brands. It does not suit investors who need near-term price appreciation to validate the thesis.

Quality at a discount: what history says about buying beaten-down brands

The investment case for LVMH, Burberry, and Nike rests not on a prediction that macro conditions will improve quickly, but on the durability of their competitive advantages relative to the prices currently available. The S&P 500 sits near all-time highs, AI sector earnings are producing diminishing market reactions, and a cluster of wide-moat consumer brands is trading at discounts that Morningstar analysts believe are inconsistent with long-term intrinsic value.

Identifying undervalued assets during periods of maximum pessimism is analytically sound but emotionally difficult. The current environment is testing both.

Contrarian positioning in consumer names has historical precedent on its side: the dot-com bust and the GFC both produced episodes where consumer defensives entered from similarly depressed relative valuations and went on to outperform over 3-5 year horizons, a pattern that managers including Magellan, Platinum, and Orbis are now explicitly referencing in their positioning rationale.

The practical next step for Australian investors is to review whether current portfolio construction accounts for the changed bond-equity correlation environment, and whether any allocation to quality consumer brands at current valuations is consistent with long-term objectives. That assessment is personal, not universal, and it requires honest appraisal of time horizon, risk tolerance, and conviction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.