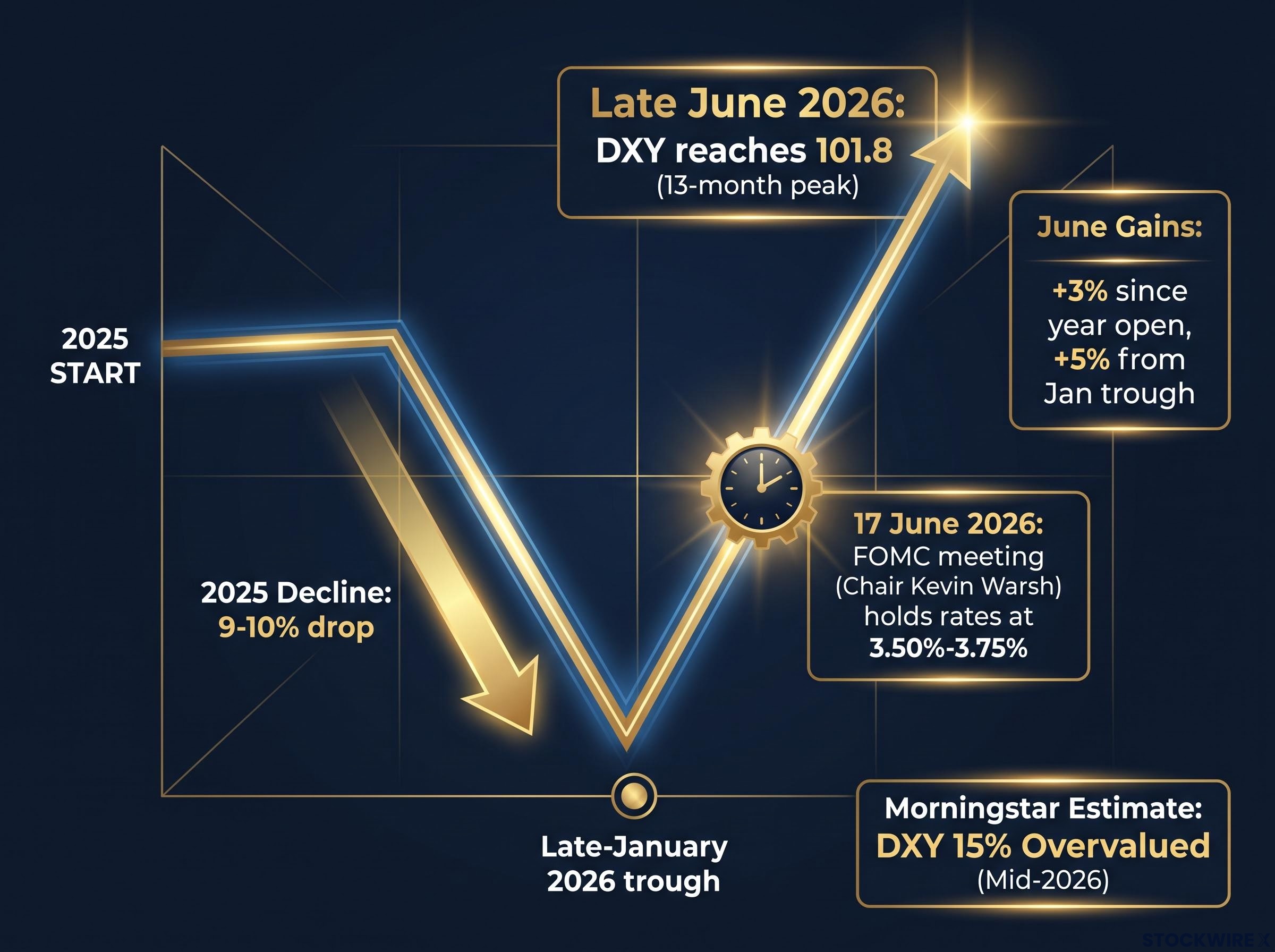

The greenback’s first-half performance in 2025 ranked among the worst on record for any comparable period, while the Dollar Index (DXY), which tracks the US currency against a basket of six major global currencies, shed roughly 9-10% across the year. Then, in late June 2026, that same index reached 101.8, marking a 13-month peak. The whipsaw is not a contradiction. It is the same set of forces, flipped.

That reversal matters whether or not you think of yourself as a currency investor. If you hold international equities, currency-hedged funds, or any US-denominated asset, the dollar’s direction is already shaping your returns. It is not an abstract macro question; it is a line item in your portfolio performance.

Here is what this piece gives you: a clear read on which drivers are actually doing the work right now, why Morningstar’s valuation model raises a serious flag even as the dollar hits multi-month highs, and which five signals to watch rather than which single forecast to follow. The analyst landscape is genuinely split, and the most useful thing is a map through it, not another prediction to add to the pile.

From historic low to 13-month high: what actually changed

The 2025 dollar decline was driven by three forces that reinforced each other:

- Expectations of continued Fed rate cuts, which compressed US yield advantages over other major currencies

- Rising concerns over US fiscal deficits and political instability

- Perceived risks to Federal Reserve independence, which eroded institutional confidence in the dollar

Together, these pushed DXY down approximately 9-10% for the year, its sharpest annual drop in eight years. Through the first six months of 2025, the dollar put in its poorest opening-half showing in over fifty years.

Then the mirror image arrived. The Fed stopped cutting. US economic data came in stronger than expected, powered by artificial intelligence investment and fiscal stimulus. Markets began repricing toward higher-for-longer rates rather than the steady easing path they had assumed throughout 2025.

The decisive turning point came at the 17 June 2026 Federal Open Market Committee (FOMC) meeting, the first presided over by incoming Fed Chair Kevin Warsh. Policymakers kept rates on hold at 3.50%-3.75% and released a dot plot that carried a distinctly hawkish tone, prompting an immediate repricing across markets.

FOMC internal divisions were already visible before Warsh’s arrival: the April 2026 meeting produced a historic four-way dissent, with hawks outnumbering the lone dove three to one, confirming that the hawkish pivot reflected genuine committee conviction rather than a single chair’s rhetorical preference.

Reuters described the dollar heading into the second half of 2026 “on a high,” driven by bets on higher US rates and strong demand for US assets.

By late June 2026, the index had advanced 3% since the year’s opening and 5% from its late-January trough, arriving at 101.8 for a 13-month peak. The speed and scale of that reversal tells you something important: currency markets are not pricing fundamentals so much as repricing expectations. The next shift in Fed tone could move the dollar just as sharply in reverse.

When big ASX news breaks, our subscribers know first

The three pillars holding up the dollar right now

Three forces are supporting the dollar’s current strength, but they are not equal. Understanding which one is doing the heavy lifting tells you which leading indicator matters most.

| Pillar | Primary mechanism | Key institutions citing it | Durability |

|---|---|---|---|

| Interest-rate differentials | Higher US yields attract global capital inflows into Treasuries and money-market instruments, lifting demand for dollars | JPMorgan, LPL, Invesco Fixed Income (Robert Waldner), MUFG (Lee Hardman) | Cyclical; entirely Fed-dependent |

| Relative growth expectations | US GDP outperformance (AI investment, fiscal stimulus) draws equity and bond flows; exchange rates discount future growth as much as present conditions | Morgan Stanley, LPL, multiple institutional desks | Cyclical; subject to global convergence |

| Reserve-currency and safe-haven demand | Central banks, sovereign wealth funds, and global investors hold dollar assets as primary safe-haven instruments; the dollar’s role in trade invoicing, commodity pricing, and cross-border finance limits downside | US Bank, broad institutional consensus | Structural |

The rate-differential pillar is doing the most work right now. JPMorgan explicitly ties recent dollar strength to the Fed’s tighter policy pivot. Robert Waldner, chief strategist and head of macro research at Invesco Fixed Income, and Lee Hardman, senior currency analyst at MUFG, both track rate-differential dynamics as the primary driver.

That matters because pillar one can reverse on a single dot plot. Pillar two is subject to global growth convergence as European and Asian economies normalise. Only pillar three, the reserve-currency role, is genuinely durable, and it was already there before the rally started. If you are watching Fed communications more closely than anything else, you are watching the right variable.

The PCE inflation trajectory is the most direct input into that rate-differential pillar: May 2026 core PCE held at 3.4% year-over-year, its highest reading since October 2023, and the FOMC responded not with a rate move but with a hardening of guidance language that repriced cut timelines more decisively than any actual hike would have.

When valuation and momentum point in opposite directions

Here is the surface-level paradox: the dollar is at a 13-month high and simultaneously flagged as significantly overvalued. Both statements are true, and understanding why requires separating two different ways of pricing a currency.

Morningstar’s currency valuation model estimates the DXY is approximately 15% overvalued as of mid-2026.

Muhammad Hamza Saleem, currency research analyst at Morningstar, views the dollar’s current strength as predominantly cyclical in nature, driven by rate differentials and a degree of risk premium rather than any genuine shift in the currency’s underlying fair value. His outlook calls for the dollar to hold firm through the remainder of 2026 before drifting gradually lower into 2027 as those cyclical tailwinds fade.

The distinction comes down to what each camp is measuring. Current pricing reflects cyclical factors:

- Interest-rate differentials favouring the US

- A risk premium driven by policy uncertainty

- Short-term growth outperformance

Fair value, by contrast, reflects structural factors:

- Purchasing power parity across economies

- Long-run trade flows and current account balances

- Structural demand for dollar reserves

US Bank makes a similar point: long-term currency trends reflect economic strength and stability across multiple years, not just one or two years of rate differentials. And deVere highlights that US trade and industrial policy has at least some intent to limit dollar strength by encouraging currency diversification, a headwind that does not show up in short-term momentum but matters over longer horizons.

The 15% overvaluation figure is not a sell signal for tomorrow. It is a clear statement that anyone with significant dollar exposure at current levels is paying a cyclical premium that requires the current rate and growth narrative to hold indefinitely in order to justify itself. For an investor deciding whether to hedge currency exposure in international holdings or increase dollar-denominated asset weighting, that gap is the most important single data point in this analysis.

What the bulls and bears are each getting wrong

Both camps have identifiable blind spots, and recognising them is more useful than picking a side.

- Over-extrapolation of Fed hawkishness. Many bullish arguments treat the current rate stance as a new permanent regime rather than a data-dependent posture. LPL explicitly identifies this risk: the biggest threat to its own bullish dollar thesis would be a shift in the Fed’s tone toward neutrality or renewed easing. If energy-related inflation continues to ease and core measures moderate, the Fed will face growing pressure to prioritise growth and employment. The hawkish stance is itself cyclical.

- Underestimation of global growth convergence. Bearish forecasts from late 2025 assumed US exceptionalism would fade quickly. Bullish forecasts now assume it will last indefinitely. Both underweight the evidence that European and Asian growth is normalising as earlier energy shocks dissipate. A Reuters analysis from December 2025 emphasised structural dollar weakness as global growth picked up, and that backdrop has not fully disappeared. Morgan Stanley projects the dollar bear market ends in the second half of 2026, with the index around 100 and possible further gains in 2027, but that is a transition scenario, not a secular bull market.

The US growth exceptionalism narrative supporting pillar two rests on aggregate spending data that may be less durable than it appears: April 2026 consumer spending was largely funded by savings drawdowns rather than income gains, and the K-shaped distribution of fuel cost burdens means the aggregate numbers overstate the breadth of underlying demand.

- Insufficient weight on valuation and political risk. Day-to-day FX commentary is dominated by momentum and carry trades. Morningstar’s 15% overvaluation estimate and deVere’s point about US policy explicitly targeting dollar limitation are underweighted in mainstream consensus. A Reuters survey in early 2026 found most currency strategists expect the rebound to be short-lived, yet market positioning has not fully reflected that view.

Central bank reserve diversification is the structural headwind that deVere’s US policy argument points toward but does not fully quantify: the OMFIF Global Public Investor survey released 30 June 2026 recorded the first instance on record of net dollar-reduction intent outnumbering net dollar-increase intent among sovereign institutions, a shift that operates independently of the cyclical rate and growth factors currently supporting DXY.

LPL notes that the biggest downside risk to its bullish dollar thesis is a shift in Fed tone toward neutrality or renewed easing.

The practical takeaway is not that one camp is right. It is that the most dangerous position is the one that has picked a camp and stopped monitoring the conditions that would invalidate it.

The next major ASX story will hit our subscribers first

Five signals that will tell you whether the rally holds

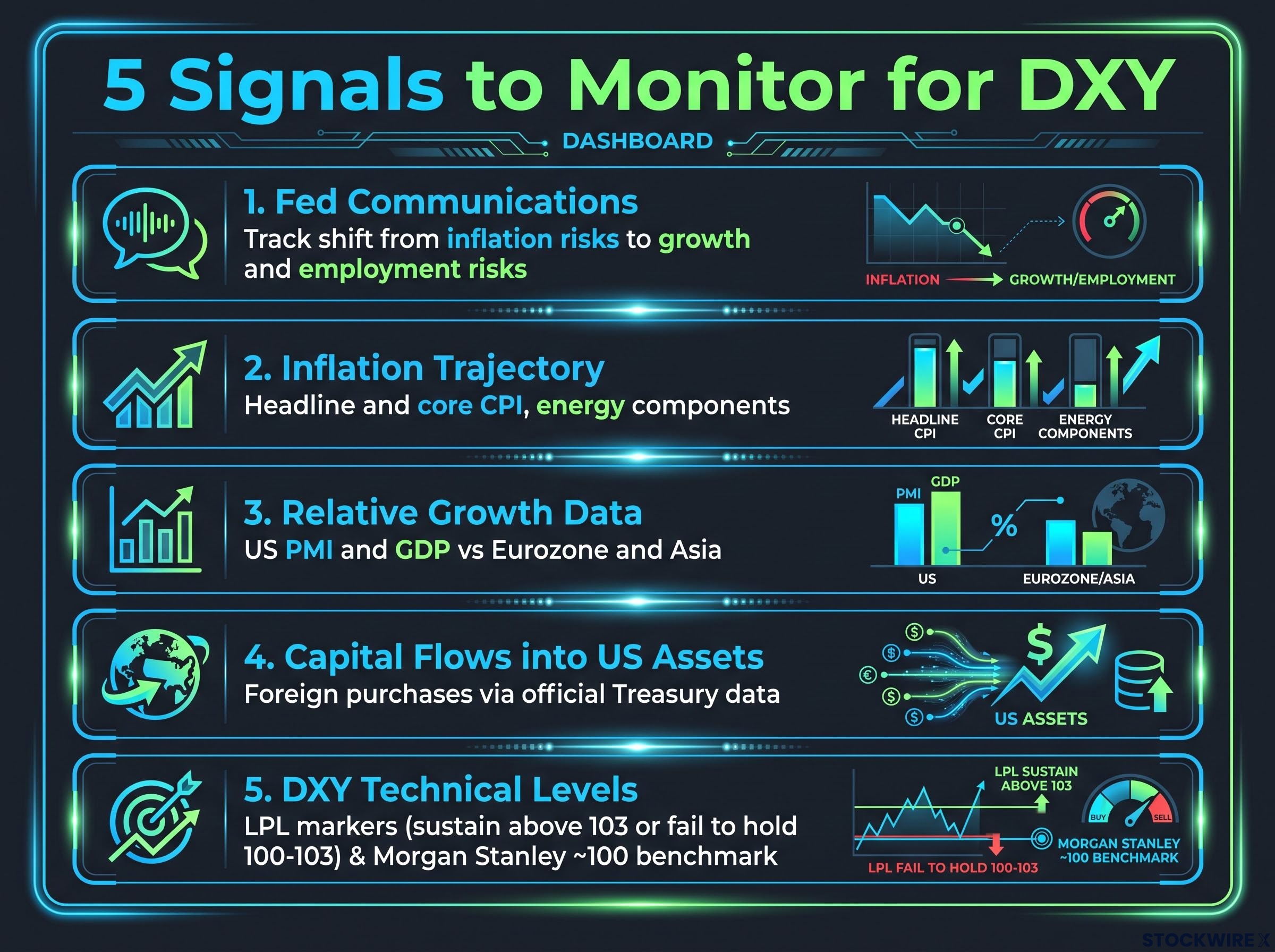

Each of these maps directly to a specific pillar of dollar strength or a blind spot identified above. Watching all five gives you a real-time diagnostic rather than a passive exposure to whatever happens next.

- Fed communications and dot plots. This is the single most important variable. Track whether the Fed’s language remains focused on “inflation risks” or starts to emphasise “growth and employment risks.” That shift in framing would signal that the rate-differential pillar is weakening. Any pivot toward neutrality or rate cuts would compress the yield advantage that is doing most of the work right now.

- Inflation trajectory. Watch headline and core CPI, especially energy components. Core inflation is already being driven lower by falling energy costs and diminishing prior-year tariff effects. A sustained decline removes the justification for higher-for-longer rates and brings the Fed’s hawkish stance under pressure.

- Relative growth data. Compare US purchasing managers’ index (PMI) readings, GDP revisions, and earnings trends with eurozone and Asian equivalents. Evidence of growth convergence would undermine the exceptionalism narrative supporting pillar two.

- Capital flows into US assets. Official Treasury data on foreign purchases of US assets tracks whether institutional and sovereign investors are still chasing yield and growth in the US or starting to diversify. This is your instrument for monitoring reserve and institutional demand in real time.

The Treasury International Capital data published monthly by the US Department of the Treasury provides the most granular publicly available record of foreign purchases of US assets, covering Treasuries, equities, and agency securities, giving investors a direct window into whether sovereign and institutional demand for dollar assets is holding or beginning to rotate.

- DXY technical levels. LPL specifically identifies a sustained break above approximately 103 as the marker confirming a durable bullish phase. Failure to break and hold the 100-103 range would signal a failed rally. Price action around these thresholds helps distinguish between a cyclical bounce and something more durable. Morgan Stanley’s projection of the index around 100 in the second half of 2026, with potential further gains in 2027, provides the benchmark bullish scenario against which to assess incoming data.

This framework converts a complex multi-variable macro debate into five concrete, publicly available data points. You do not need access to a proprietary FX desk to monitor them.

Current dollar strength is a priced-in bet, not a new equilibrium

The weight of independent evidence points in one direction. Morningstar’s estimate that the DXY is approximately 15% overvalued, the Reuters strategist survey showing most expect the rebound to be short-lived, and the identified blind spots in bullish commentary all suggest a cyclical rebound rather than a structural shift.

The dollar’s current level is a priced-in bet on Fed hawkishness and US growth exceptionalism holding together simultaneously. That is a meaningful risk to carry passively without a monitoring plan. Morgan Stanley frames the second half of 2026 as a transition period, not the beginning of a new secular bull market.

The historical parallel reinforces the point. The 2025 slump was faster and deeper than most forecasters predicted. That is precisely the reason to take valuation signals seriously even when momentum disagrees. When the first of those five signals breaks, the dollar’s direction will likely shift faster than consensus expects, for the same reason the 2025-to-2026 reversal caught most positioning off guard.

Investors who treat current strength as a temporary cyclical phase rather than a new equilibrium will position their currency hedges, international equity allocations, and fixed income exposures differently, and more defensively, than those who extrapolate the current rally forward. That distinction may not matter this quarter. Over the next twelve months, it likely will.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.