What GQG’s 12.4% Dividend Yield Isn’t Telling You

54 mins ago

GQG Partners delivered a negative 25% total shareholder return over the twelve months to July 2026. For a business whose entire value proposition is generating investment returns, that figure is more than a bad year. It is the market’s verdict on a conviction call that has not yet paid off.

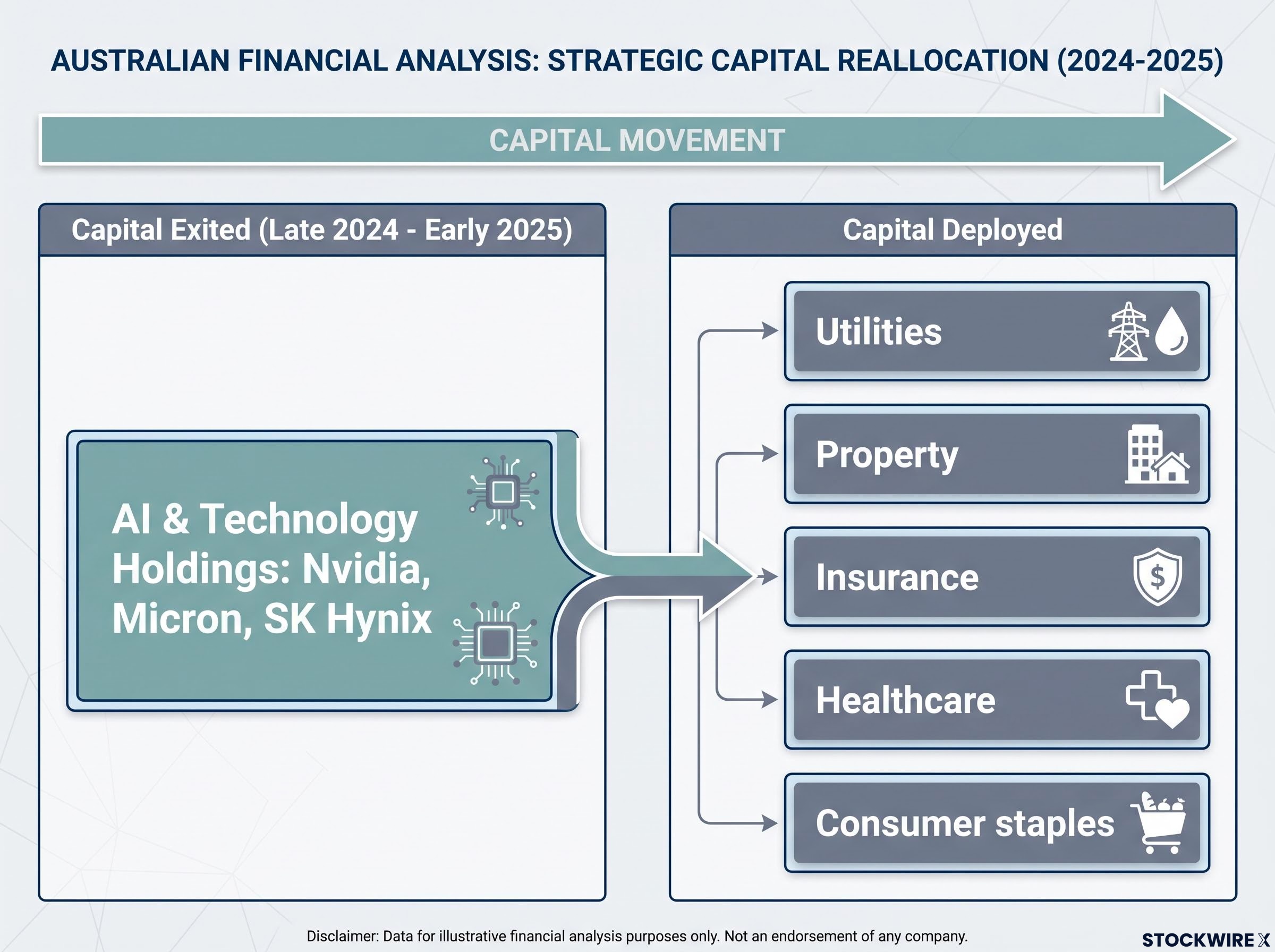

The underperformance is not random. It traces directly to a single, documented strategic decision: GQG sold down its AI and technology holdings through late 2024 into early 2025, moving that capital into defensive areas including utilities, property, insurance, and healthcare. The firm’s CIO, Rajiv Jain, cited tariff concerns and stretched valuations. The AI rally continued without them. What followed was a chain reaction: poor relative performance across all four flagship funds, US$3.9 billion in net client outflows, and a share price that has stagnated for roughly two years.

What the GQG sequence makes clear is how quickly a single positioning conviction can work backwards through an active manager’s entire value proposition. The anatomy of that propagation, from portfolio decision through performance damage to fund flows and share price, gives you a framework for evaluating any active manager whose track record is under pressure.

GQG began trimming AI-linked holdings from late 2024 into early 2025. According to Macquarie Research (July 2026), the firm’s avoided or substantially reduced positions included Nvidia, Micron, and SK Hynix, three names at the centre of the AI infrastructure build-out. The capital went into a different part of the market entirely.

The replacement sectors, each chosen for its defensive characteristics:

Rajiv Jain publicly cited tariff risk and macro uncertainty as the rationale for the rotation. The firm’s own CIO communications for late 2025 went further, making the cost of the decision explicit.

“Our decision to cut back risk, particularly in the artificial intelligence theme, cost us significant relative performance in 2025.”

The conviction behind the call is what matters here. This was not a gradual drift or a passive underweight. GQG actively sold its highest-momentum positions and redeployed into sectors that were, by design, unlikely to keep pace with an AI-driven equity rally. That structural mismatch is the origin point for everything that followed, and it explains why the underperformance compounded rather than self-corrected as the year progressed.

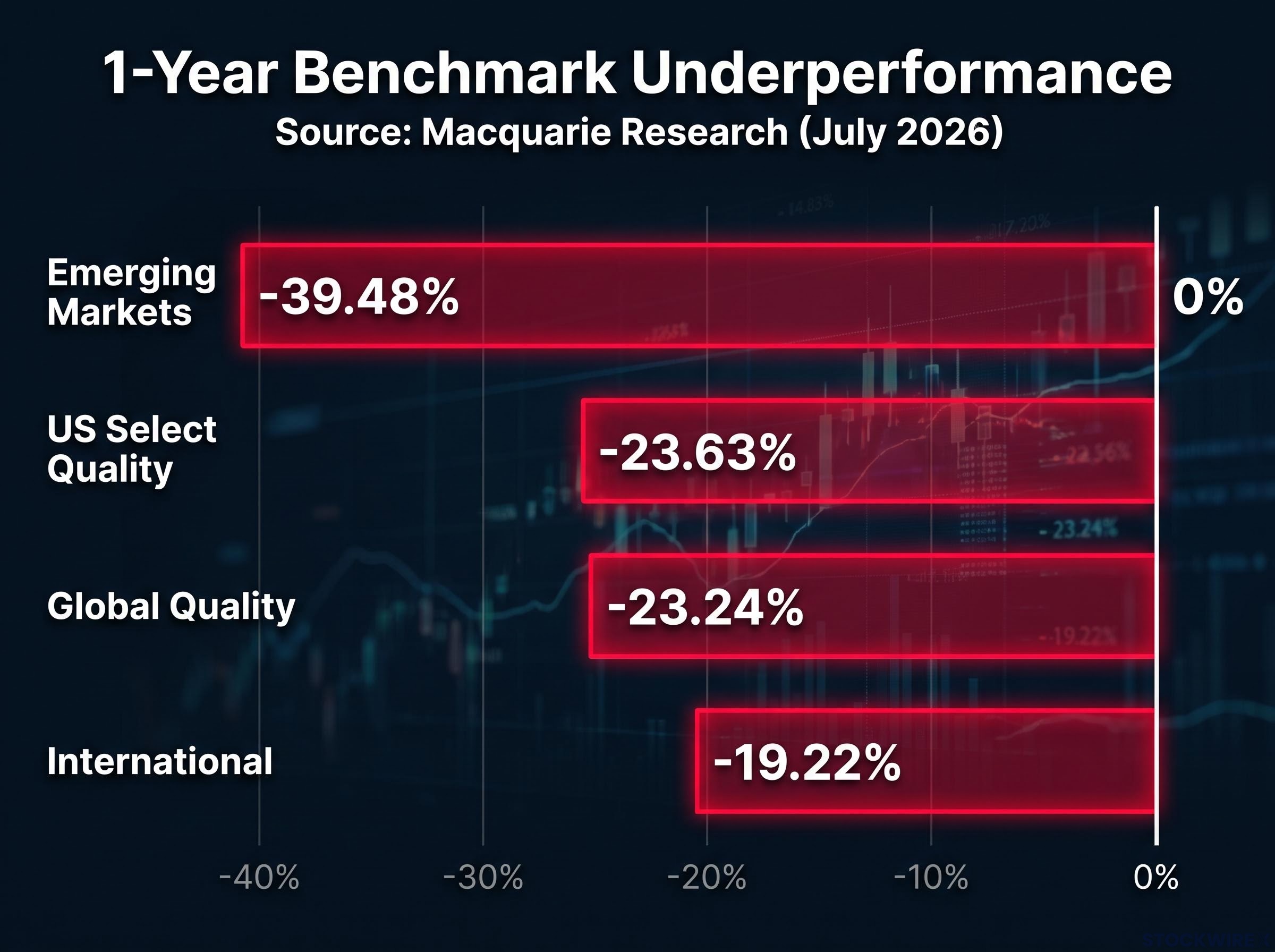

The performance damage was not confined to a single strategy or a single time horizon. Macquarie Research (July 2026) published benchmark underperformance figures across all four of GQG’s flagship funds, and the spread tells you this was a house-wide positioning outcome, not a stock-picking problem.

| Fund | 1 Month | 3 Months | 6 Months | 1 Year | 3 Years |

|---|---|---|---|---|---|

| Emerging Markets | -12.35% | -11.45% | -22.46% | -39.48% | -10.83% |

| Global Quality | -6.31% | -11.34% | -7.37% | -23.24% | -9.29% |

| International | -5.90% | -5.96% | -9.76% | -19.22% | -4.30% |

| US Select Quality | -6.46% | -14.69% | -5.16% | -23.63% | -8.78% |

Figures represent underperformance versus respective benchmark indices. Source: Macquarie Research, July 2026.

The one-year column is where the damage concentrates. Emerging Markets trailed its benchmark by 39.48%. US Select Quality lagged by 23.63%. Global Quality underperformed by 23.24%, a figure independently confirmed by the fund’s own returns: the Global Quality Equity Fund lost approximately 6.1% over the year to 30 November 2025, while its MSCI ACWI ex-Tobacco benchmark gained approximately +17.3%.

The Global Quality Fund lost approximately 6.1% over the year to 30 November 2025, against a benchmark gain of approximately +17.3%, a shortfall of roughly 23 percentage points.

The three-year column shows the bruise spreading further. Every fund is negative versus its benchmark across every measured horizon. That multi-fund, multi-horizon pattern raises a specific due-diligence question for anyone allocating to GQG: how much of the pre-2025 outperformance was the quality process, and how much was the AI sector weight that has since been removed?

The multi-fund, multi-horizon underperformance table raises precisely the due diligence issue that professional frameworks address when screening funds before performance figures are used as the primary evaluation lens: whether the people, process, and parent quality dimensions signal durability or structural fragility in the strategy.

One qualification matters here. Independent research notes that at least one GQG global strategy had regained a performance edge by early 2026 and maintained a competitive record since inception in 2019. The longer-term picture is not destroyed. But the 2025 year was clearly and comprehensively poor.

A listed active fund manager earns revenue as a percentage of the assets it manages. This is funds under management, or FUM, the total value of client money in the firm’s strategies. When a manager underperforms its benchmark, the business takes damage through two channels simultaneously, and understanding the mechanics matters because headline FUM can mask what is actually happening underneath.

GQG reported approximately US$3.9 billion in net outflows during 2025, including approximately US$2.1 billion in December alone. CIO Rajiv Jain acknowledged the firm’s positioning error directly, noting that GQG had exited the AI trade too early in 2025 and had maintained an overly defensive stance during a period when a return to risk-on would have served clients better.

The December acceleration matters as a forward signal. Institutional allocators typically review and rebalance on quarterly or annual cycles, meaning the December spike likely reflects decisions made following full-year 2025 performance reviews. If the performance gap persists, further redemption pressure in subsequent quarters is a real possibility. For a reader assessing GQG as a business, the headline FUM gain masks the underlying flow damage: the trend in client behaviour is pointing in a direction that the investment returns must reverse to arrest.

The equity market’s verdict on GQG synthesises the fund-level performance, the outflow trajectory, and the uncertainty about whether the macro thesis will pay off before further client attrition erodes the earnings base. That synthesis is visible in three figures:

Total shareholder return over twelve months as of July 2026: negative 25%, according to Macquarie Research and ASX data.

The elevated dividend yield that GQG currently carries deserves context. A high yield on a fund manager stock can signal distress, but GQG’s situation is better characterised as a prolonged period of slow deterioration across roughly two years, rather than any sudden or acute balance-sheet shock. The yield reflects the gap between a maintained dividend level and a depressed share price driven by sustained underperformance and client outflows, not a balance-sheet crisis.

For Australian investors holding GQG shares directly on the ASX, the negative 25% TSR translates the fund-level performance story into the language of their own portfolio outcome. A manager whose own shareholders lost a quarter of their capital in a year when markets performed strongly is a business where the investment process and the shareholder experience have diverged sharply.

GQG’s public language on AI is neither hedged nor apologetic. The firm has characterised the AI market as a “stock market bubble” and compared it to a “dotcom bubble on steroids”, citing capital expenditure running well ahead of any monetisation pathway. As of mid-2026, some strategies maintain near-zero technology exposure.

The analytical basis the firm offers rests on historical pattern recognition:

Whether the AI stock bubble framing GQG has adopted proves prescient depends in part on which analytical lens is applied: Minsky cycle analysis, Kindleberger’s displacement-to-revulsion sequence, and Shiller CAPE valuation metrics each reach different interim conclusions about whether current AI equity pricing represents speculative excess or earnings-justified expansion.

Understanding the conviction matters because it determines the conditions under which GQG’s performance would recover. The firm is not positioning the AI exit as a mistake. It is maintaining the call.

There is a distinction between being wrong on direction and being wrong on timing. GQG may still prove correct that AI equity valuations will correct significantly. But each quarter the correction fails to materialise, the performance gap widens and the redemption risk increases.

This is the core unresolved tension. A thesis that has cost the manager nearly two years of relative performance has to eventually pay off at a scale that justifies the accumulated drag. That payoff horizon is currently unknowable. For you, the practical implication is straightforward: GQG’s performance is unlikely to recover against AI-heavy benchmarks until either a significant technology correction occurs or the firm reconstitutes exposure. Both scenarios carry meaningful uncertainty about timing.

The GQG experience raises a question that institutional allocators reviewing the firm’s history are almost certainly asking: whether the outperformance from 2019 to 2024 reflected a repeatable quality process or was substantially driven by the AI and technology sector weight that has since been unwound.

That question has no definitive answer yet. The longer-term record provides some defence: at least one GQG strategy maintained a competitive record versus the MSCI ACWI and category averages from 2019 to 2026, even while trailing the ACWI Growth index by approximately one percentage point. The damage is concentrated, not terminal. But the question will influence redemption decisions for as long as the underperformance persists across multiple evaluation horizons.

The broader lesson applies to any active manager under performance pressure. When evaluating a manager whose track record includes a period of strong outperformance followed by a style-driven reversal, three steps sharpen the assessment:

Active manager underperformance in Australia is not limited to single-thesis conviction calls: SPIVA data shows 74% of Australian equity general fund managers failed to beat the S&P/ASX 200 in 2025 even in conditions described as unusually favourable for stock selection, suggesting the GQG episode sits within a broader structural pattern rather than as an isolated outlier.

This is a genuine analytical scenario, not a dismissal. If AI equities correct significantly, GQG’s defensive positioning would provide meaningful relative advantage. The performance gap would compress, the flow trajectory would likely reverse, and the share price would re-rate.

The counterargument to GQG’s position is that AI stock valuation risk is genuinely elevated: Goldman Sachs’ May 2026 assessment found that AI-related technology spending as a share of US GDP has surpassed the late-1990s dot-com peak, and index-level calm is masking distributional divergence between individual AI winners and losers that passive investors may be underweighting.

The practical constraint is that vindication requires both the correction and GQG’s portfolio remaining in position to capture it. Neither is assured as of mid-2026. A manager who reconstitutes technology exposure just before a correction misses the payoff. A correction that arrives after client attrition has permanently impaired the fee base changes the magnitude of the recovery.

Three variables will determine whether the GQG story becomes a cautionary tale about conviction risk or a contrarian vindication of patient positioning:

The position today is a business with a live and testable macro thesis, a clear set of conditions under which performance would recover, and a commercial window that narrows with each additional quarter of underperformance and outflow. Macquarie’s Neutral rating and $1.35 price target, as of July 2026, reflect that tension: not a business in structural distress, but one whose growth trajectory depends on a thesis the market has not yet validated.

The elevated dividend yield offers income to shareholders while they wait. The roughly two-year stagnation means they have been waiting for some time already. Whether the reader holds GQG as a fund investor, an ASX shareholder, or an allocator benchmarking active managers, the case provides something concrete: a framework for assessing a manager whose conviction is intact but whose clock is ticking.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

GQG Partners is a listed active fund manager, trading on the ASX, that runs four flagship equity strategies: Emerging Markets, Global Quality, International, and US Select Quality. The firm's value proposition is generating investment returns that beat benchmark indices through concentrated, high-conviction stock selection.

GQG's underperformance traces directly to a deliberate decision by CIO Rajiv Jain to sell AI and technology holdings, including Nvidia, Micron, and SK Hynix, from late 2024 into early 2025, rotating into defensive sectors like utilities, property, and insurance. The AI rally continued without them, leaving all four flagship funds behind their benchmarks across every measured time horizon.

According to Macquarie Research in July 2026, GQG's Emerging Markets fund trailed its benchmark by 39.48% over one year, US Select Quality underperformed by 23.63%, Global Quality by 23.24%, and International by 19.22%. Every fund was negative versus its benchmark across every measured horizon from one month to three years.

GQG reported approximately US$3.9 billion in net client outflows during 2025, including around US$2.1 billion in December alone. The December acceleration is significant because it likely reflects institutional allocators acting on full-year 2025 performance reviews, signalling further redemption pressure is possible if the performance gap persists.

GQG's performance gap would compress if AI equities correct significantly, since the firm's defensive positioning would then provide meaningful relative advantage; the article also notes that recovery requires GQG's portfolio to remain in position to capture any correction, and that further institutional redemptions narrow the commercial window within which a rebound can restore the business trajectory.