When two of the most disciplined value investors in the United States study the same stock at the same time and arrive at opposite conclusions, that tension is worth understanding. The Q1 2026 13F filings, reflecting positions as of 31 March 2026 and filed with the SEC on 15 May 2026, from Berkshire Hathaway, Pershing Square, Baupost Group, and Akre Capital reveal a quarter defined as much by divergence as by consensus. Berkshire tripled its Alphabet stake while Bill Ackman liquidated his entirely. Berkshire exited Visa while Seth Klarman initiated a new position in it. These are not random contrarian signals. They are the output of rigorous, independent analytical processes arriving at different conclusions from the same public information. What follows maps the moves from each manager’s latest filing, explains the strategic logic behind them, and draws out the single most important lesson for any investor who uses 13F data as part of their research process.

What the Q1 2026 filings reveal at a glance

The scale differences across these four portfolios shape how each position change should be interpreted. A 1% reallocation inside Berkshire’s $263.1 billion, 29-holding portfolio represents a fundamentally different conviction signal than a 15% new position inside Ackman’s $13.7 billion, 11-holding fund.

| Manager | Fund | Approx. Portfolio Value | Holdings | Headline Q1 2026 Move |

|---|---|---|---|---|

| Warren Buffett / Greg Abel | Berkshire Hathaway | ~$263.1B | 29 | Alphabet position tripled |

| Bill Ackman | Pershing Square | ~$13.7B | 11 | Alphabet fully exited |

| Seth Klarman | Baupost Group | Not disclosed | Not disclosed | Amazon expanded ~47% |

| Chuck Akre | Akre Capital | Not disclosed | Not disclosed | New positions in ServiceNow, Salesforce, FICO |

All four filings share the same structural characteristics:

- Positions reported as of 31 March 2026 (quarter-end)

- Filing deadline and release: 15 May 2026 (45 days post-quarter)

- Publicly accessible at no cost through SEC EDGAR

Q1 2026 also marked the first full reporting period under Greg Abel as Berkshire’s Chief Executive Officer, lending additional analytical weight to every portfolio move attributed to Berkshire’s team.

When big ASX news breaks, our subscribers know first

Berkshire’s Alphabet bet and the exits that followed

The Alphabet expansion

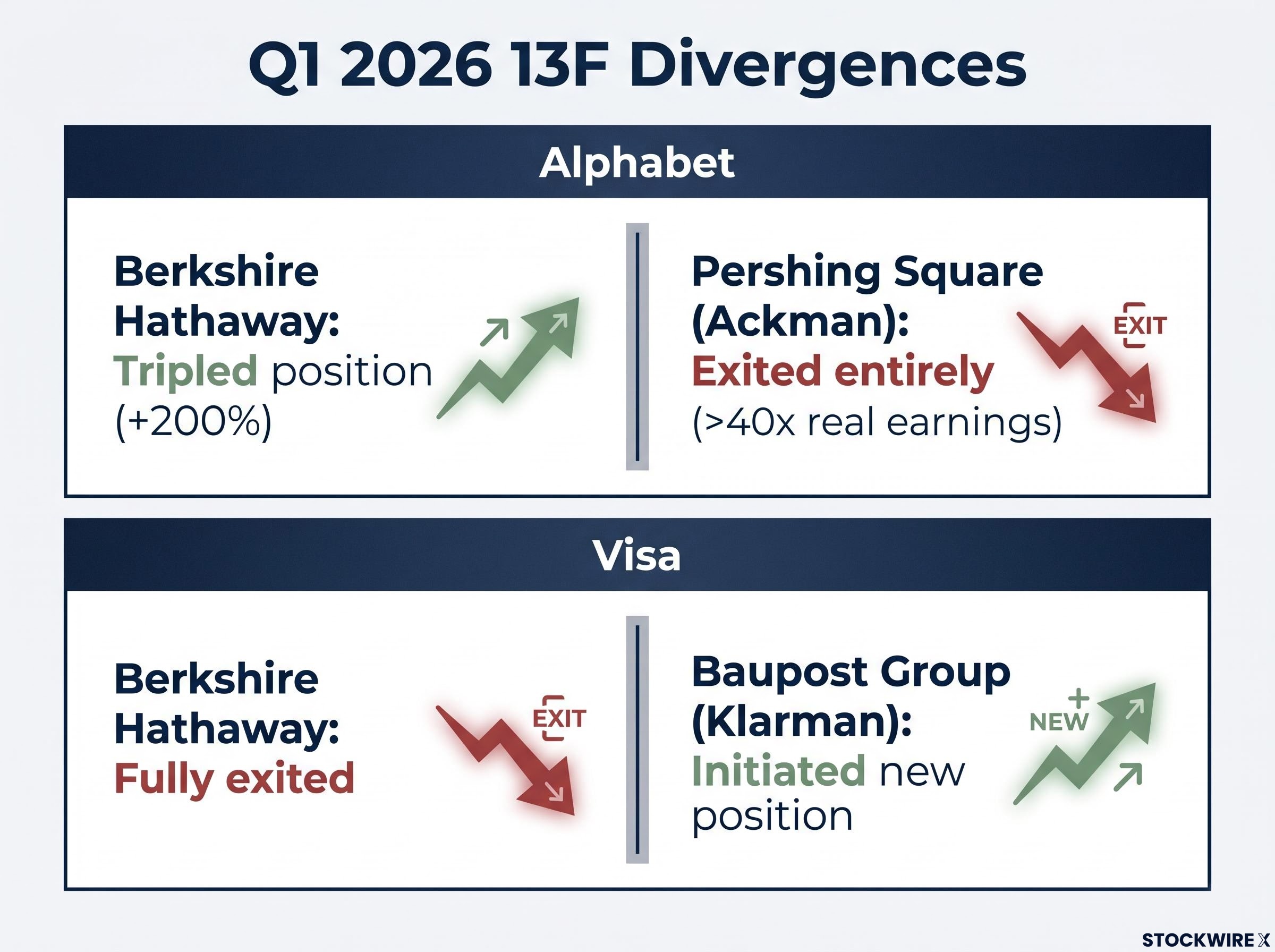

Berkshire increased its Alphabet position by approximately 200% during Q1 2026, effectively tripling the stake. The move draws particular attention given Warren Buffett’s prior acknowledgement that he and the late Charlie Munger had missed the stock earlier. Under Abel’s stewardship, the decision to triple down on a large-cap technology name signals a deliberate expansion of Berkshire’s willingness to hold concentrated positions in businesses with durable competitive advantages in cloud computing and digital advertising.

The timing matters. This was not a tentative addition to an existing toehold. A 200% increase, executed within a single quarter inside a $263.1 billion portfolio, represents a meaningful reallocation of capital.

Exiting Visa, Mastercard, and United Health

In the same quarter, Berkshire fully exited its positions in Visa, Mastercard, and United Health. According to the original source, these exits are connected to the departure of portfolio manager Todd Combs, who is understood to have managed those financial sector positions within Berkshire’s portfolio. It should be noted that this attribution has not been independently verified through public documentation available as of June 2026.

The distinction matters for any investor reading these exits as bearish signals on the underlying businesses.

Securities may be purchased for one primary reason, a positive fundamental thesis, but sold for a wide variety of unrelated reasons, including portfolio manager departures, position sizing decisions, or capital reallocation. This asymmetry makes sell signals from 13F filings particularly difficult to interpret without additional context.

Without knowing whether Berkshire’s Visa exit reflects a fundamental concern or an internal portfolio management change, drawing a bearish conclusion can be actively misleading.

Ackman’s Alphabet exit and the capital that replaced it

During the same quarter that Berkshire tripled its Alphabet stake, Bill Ackman sold his entire position. The logic, when traced through Ackman’s own framework, reads as internally coherent rather than contradictory to Berkshire’s move.

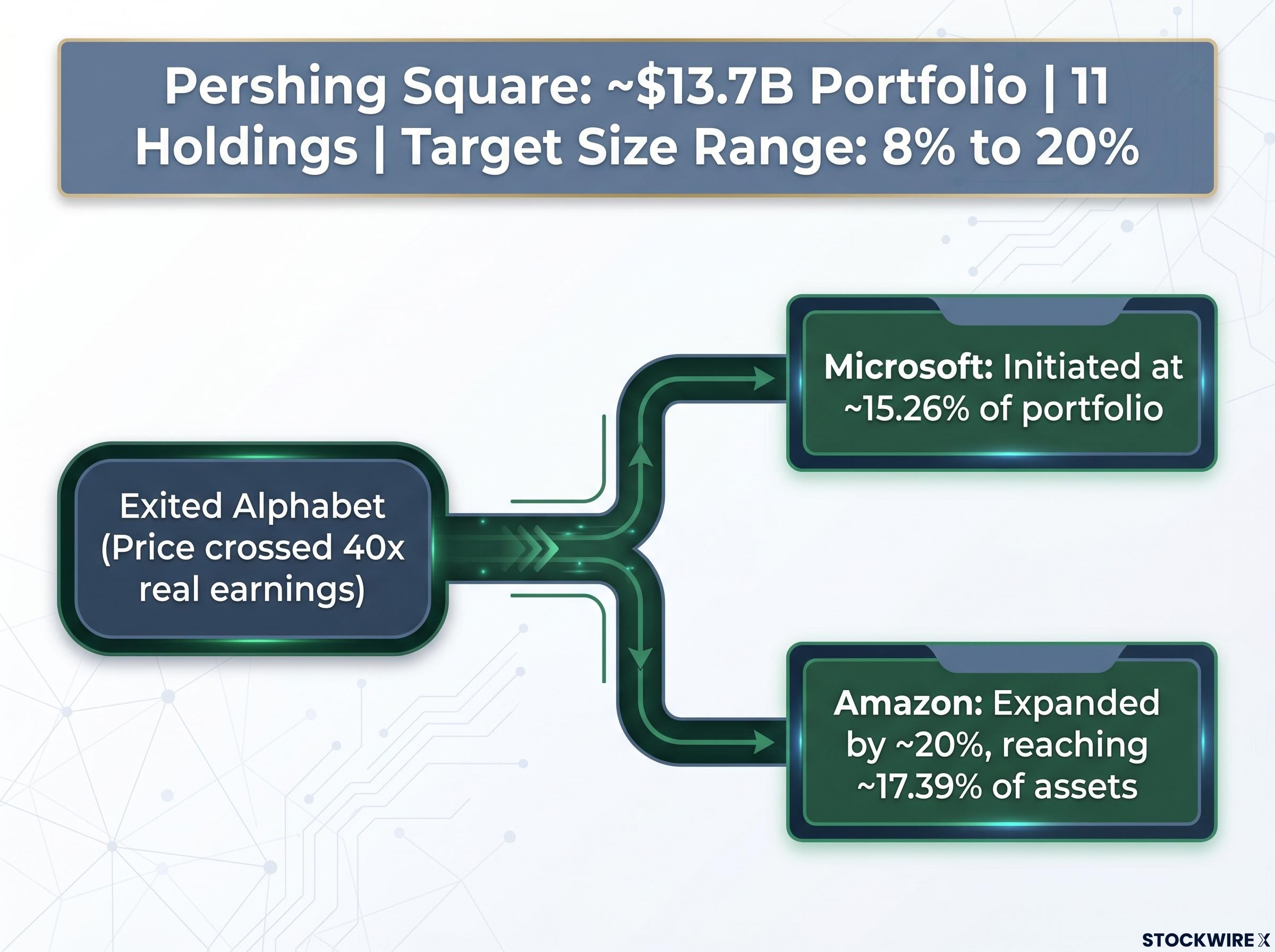

Ackman judged Alphabet to be trading above 40 times what he described as real earnings, a threshold that made the risk-adjusted return inferior to his alternatives.

Ackman’s 40x real earnings threshold is a form of the same logic that underpins price-to-earnings and free cash flow screens in systematic value analysis; the difference is that Pershing Square applies those thresholds to a concentrated 11-holding portfolio where a single valuation call carries 15-17% of total capital, making the hurdle rate significantly higher than a diversified screen would require.

That valuation assessment drove a three-step capital reallocation:

- Identify the valuation threshold exceeded: Alphabet’s price relative to Ackman’s definition of real earnings crossed the 40x boundary, signalling that the margin of safety had compressed below Pershing Square’s required hurdle.

- Assess relative attractiveness of alternatives: Microsoft and Amazon, both large-cap technology names with what Ackman has described as durable competitive advantages, offered superior risk-adjusted return profiles at prevailing prices.

- Redeploy capital at higher conviction-adjusted weight: Microsoft was initiated as a new position at approximately 15.26% of the portfolio. Amazon was expanded by roughly 20%, reaching approximately 17.39% of assets.

These weights are not incidental. Pershing Square’s characteristic position sizing range sits between 8% and 20% for highest-conviction ideas, meaning both Microsoft and Amazon entered the portfolio at or near maximum conviction. Across 11 total holdings and $13.7 billion in assets, every percentage point of allocation reflects a deliberate capital allocation judgement based on relative valuation, not absolute price levels.

What 13F filings actually are, and what they cannot tell you

Form 13F-HR requires investment firms managing more than $100 million in qualifying assets to disclose their holdings quarterly. Positions are reported as of quarter-end, with filings due within 45 days. All filings are publicly accessible at no cost through SEC EDGAR.

The regulatory framework provides visibility into what prominent managers hold. It does not provide visibility into why.

Three structural limitations govern how 13F data should be interpreted:

- Timing lag: The gap between when positions are established and when filings become public means investors cannot replicate trades at the same entry price. Q1 2026 positions were established by 31 March but not disclosed until 15 May.

- No rationale disclosure: The specific reasoning behind each transaction is absent. Two managers can hold the same stock for entirely different reasons, and neither filing reveals which thesis is in play.

- Sell-signal ambiguity: The buy-sell asymmetry principle holds that securities are purchased for one primary reason but may be sold for a wide variety of unrelated reasons, making exits the least reliable signals in any filing.

The correct use case for 13F data follows a structured sequence:

Reading earnings reports with the same depth that Klarman and Ackman apply when reconstructing a thesis requires moving well beyond the EPS headline: free cash flow divergences from net income, non-GAAP adjustment trends, and metrics that quietly disappear from quarter to quarter are often where the substantive valuation signal sits.

- Identify the position change. What did the manager buy, sell, or adjust?

- Form an independent thesis. What would an investor need to believe about this business to find it attractive at the current price?

- Assess fit with personal portfolio and risk profile. Does the thesis hold under independent scrutiny, and does the position make sense within the investor’s own framework?

Readers who approach filings with this structure will generate better investment ideas and avoid the common mistake of mechanically replicating trades without an independent thesis.

Klarman and Akre: where the deep-value and compounder frameworks converge

Klarman’s capital-preservation lens on tech and financials

Seth Klarman expanded Baupost’s Amazon position by approximately 47% during Q1 2026, making it the fund’s single largest holding at roughly 12.7% of the portfolio. For a manager whose philosophy centres on purchasing assets only when the market price offers a meaningful cushion below estimated intrinsic value, a double-digit portfolio weight in a large-cap technology name signals a conviction that Amazon’s price still provides that margin of safety.

Baupost also initiated new positions in two high-quality, fee-based financial businesses:

- Visa: A direct philosophical counterpoint to Berkshire’s simultaneous full exit

- AON: An insurance brokerage with recurring revenue characteristics

The Visa initiation is the clearest illustration of the divergence principle at work. Two managers with aligned value-investing frameworks, studying the same security in the same quarter, reached opposite conclusions.

Akre’s compounder criteria applied to enterprise software

Chuck Akre’s firm added new or expanded positions in three enterprise software and analytics names during Q1 2026. Specific share counts and primary source documentation for these positions are drawn from the original source and have not been independently sourced from a named public document.

- ServiceNow (NOW): Fits Akre’s requirement for durable high returns on capital, with subscription-based revenue providing earnings visibility

- Salesforce (CRM): Aligns with the management integrity criterion, with improving profitability metrics under disciplined capital allocation

- Fair Isaac Corporation (FICO): Satisfies the reinvestment runway test, with durable pricing power in credit scoring and recurring analytics revenue

Each position maps to Akre’s three-part framework: durable high returns on capital, management teams with integrity and long-term orientation, and the ability to reinvest earnings at attractive rates for extended periods.

Akre’s three-part framework, centred on durable competitive advantages, management integrity, and reinvestment runway, maps closely to the Morningstar moat taxonomy that formalised Buffett’s original concept into five distinct sources: intangible assets, switching costs, network effects, cost advantage, and efficient scale.

| Security | Manager | Direction | Approx. Weight or Change |

|---|---|---|---|

| Amazon | Klarman (Baupost) | Expanded | +~47%, now ~12.7% of portfolio |

| Visa | Klarman (Baupost) | New position | Not disclosed |

| AON | Klarman (Baupost) | New position | Not disclosed |

| ServiceNow (NOW) | Akre Capital | New/expanded | Not disclosed |

| Salesforce (CRM) | Akre Capital | New/expanded | Not disclosed |

| Fair Isaac (FICO) | Akre Capital | New/expanded | Not disclosed |

The overlapping accumulations by Klarman and Akre in adjacent parts of the technology and financials space suggest both managers see durable compounding potential in high-quality, fee-based business models, even as valuations in the sector remain elevated.

The divergence principle as the article’s real takeaway

Two divergences from the same filing period carry the analytical weight of this entire exercise.

Alphabet: Berkshire tripled its position (approximately +200%) while Ackman exited entirely on the basis that the stock exceeded 40 times real earnings.

Visa: Berkshire fully exited while Klarman initiated a new position in the same quarter.

Both pairs of investors operate within value-investing frameworks. Both had access to the same public financial statements, the same earnings calls, the same macroeconomic data. Both arrived at opposite conclusions.

The same public information, applied through independent analytical frameworks, should produce different conclusions among disciplined investors. Divergence is not a contradiction. It is the expected output of independent analysis.

This is the principle that transforms how 13F data should be read. Instead of asking “who is right?”, the more productive question becomes: “What would I have to believe about this business to reach either conclusion?” That question is where real analytical work begins.

The 13F cycle as a recurring research prompt, not a trading signal

The next quarterly cycle will produce Q2 2026 filings, reflecting positions as of 30 June 2026, with disclosures due in mid-August 2026. All filings will be publicly accessible through SEC EDGAR.

The correct relationship between 13F filings and independent research remains constant across every cycle. Filings identify the what. Independent analysis must establish the why before any capital commitment. Each position change should prompt three questions:

The Berkshire, Ackman, and Klarman accumulations in Alphabet, Microsoft, and Amazon sit within a broader institutional pattern: aggregate hedge fund tech exposure reached an all-time high as of late May 2026, with Goldman Sachs Prime Brokerage data showing the fastest net buying pace in nearly three months concentrated in semiconductors and AI-linked software, suggesting the conviction signals in these 13F filings are part of a wider institutional rotation rather than isolated contrarian bets.

- What is the business? Understand the company’s revenue model, competitive position, and capital allocation before evaluating any manager’s decision to buy or sell.

- Why might this manager find it attractive at this price? Reconstruct the thesis that could justify the position, using the manager’s known framework as a starting point.

- Does that thesis hold under independent scrutiny? Test the thesis against publicly available data, valuation metrics, and the investor’s own risk tolerance.

The most valuable output from studying these four portfolios is not a list of stocks to buy. It is a set of analytical questions worth pursuing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.