How Hormuz Closure at $104 Oil Is Reshaping Every Asset Class

7 hrs ago

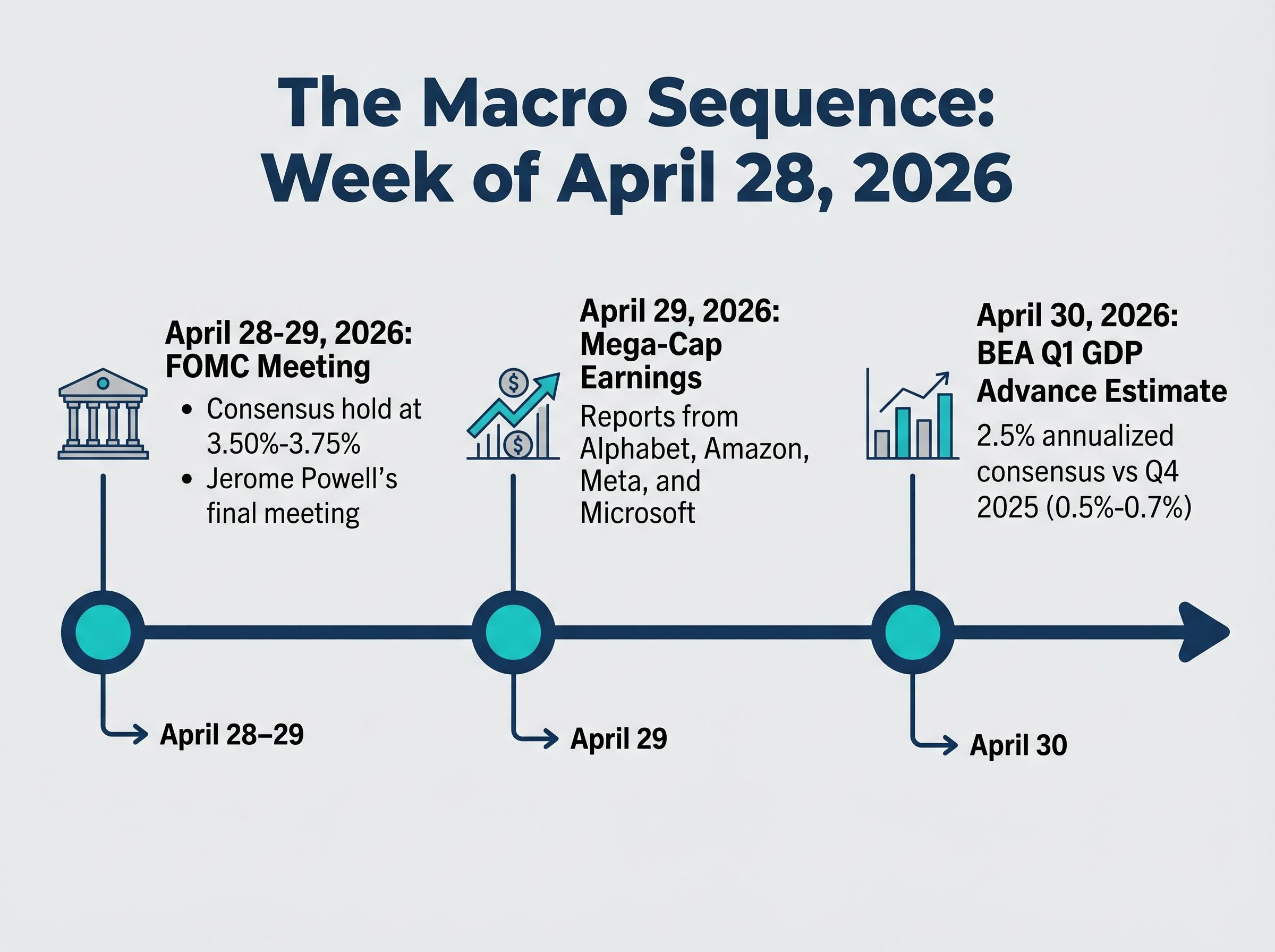

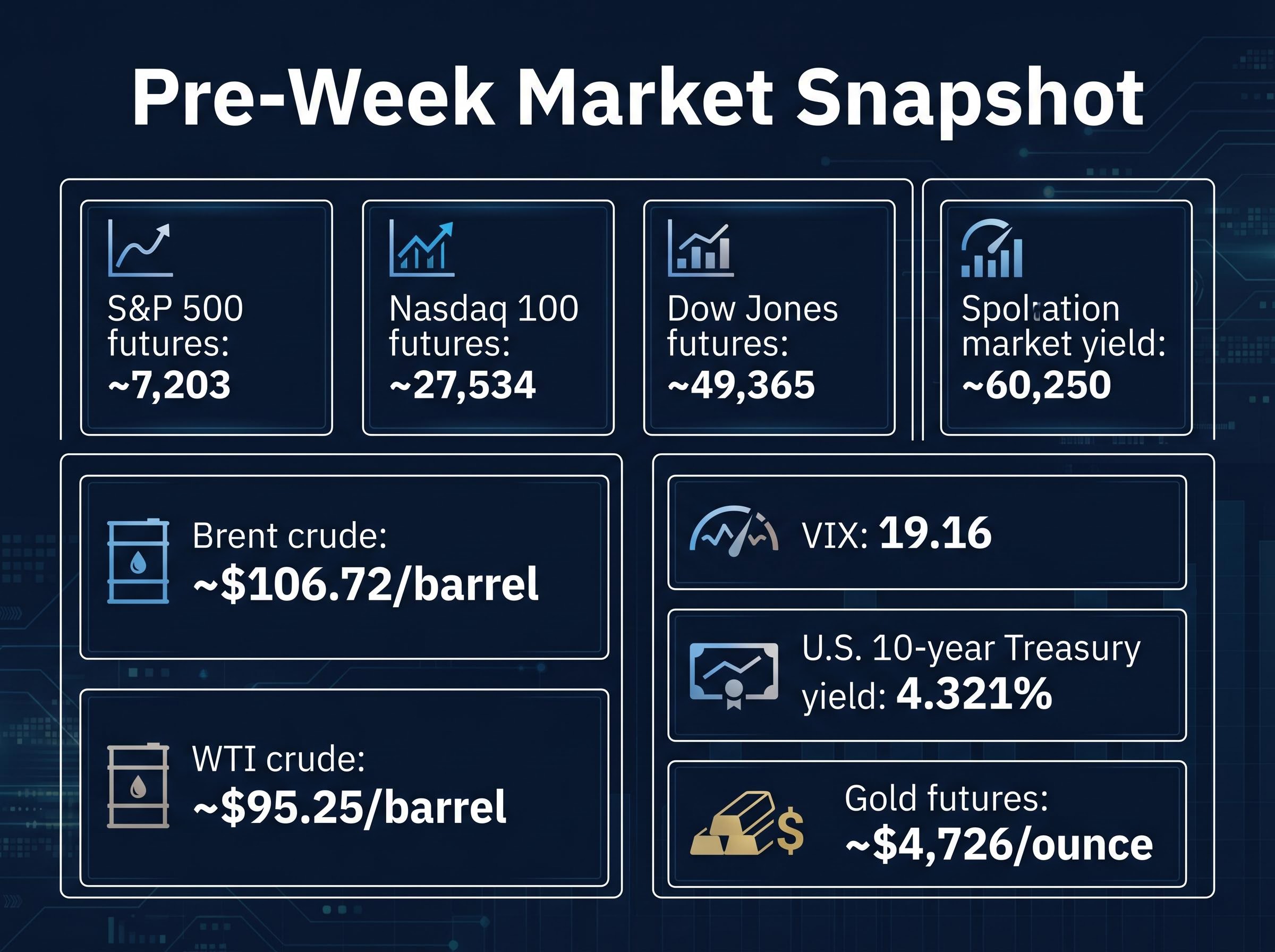

“`json { “fact_checked_full_article”: “Four of the world’s largest companies report earnings on the same afternoon. The Federal Reserve delivers its final rate decision under Jerome Powell. The Q1 GDP advance estimate lands the following morning. All of this happens in a single week, and the stock market this week faces perhaps the most consequential convergence of catalysts on the 2026 calendar.\n\nThe week of April 28, 2026 arrives with S&P 500 futures pointing toward approximately 7,203, just above the index’s last confirmed close of roughly 7,194 on April 25. The VIX sits at a moderate 19.16, a reading that suggests caution rather than alarm. Yet beneath that calm surface, Brent crude trades above $101 per barrel, driven higher by U.S.-Iran tensions over the Strait of Hormuz, and the geopolitical pressure shows no signs of easing before Wednesday’s triple collision of earnings, monetary policy, and forward guidance.\n\nWhat follows is a breakdown of each major event, what markets appear to be pricing in, the range of outcomes for each, and how the combined weight of these catalysts could define the direction of U.S. equities heading into summer.\n\n## Markets enter the week on edge as oil and geopolitics cloud the setup\n\nFutures positioning tells one story; oil prices tell another. Heading into Monday, the major indices are signalling cautious optimism:\n\n- S&P 500 futures: approximately 7,203 (above the April 25 close of roughly 7,194)\n- Nasdaq 100 futures: approximately 27,534\n- Dow Jones futures: approximately 49,365\n- Brent crude: approximately ~$106.72/barrel (up more than 2%)\n- WTI crude: approximately ~$95.25/barrel (up roughly 2%)\n- VIX: approximately 19.16 (up 2.41%)\n- U.S. 10-year Treasury yield: approximately 4.321%\n- Gold futures: approximately $4,726/ounce\n\nThe gap between a VIX below 20 and the sheer density of event risk ahead is striking. A VIX at 19 would be unremarkable in a quiet week. In a week carrying four distinct market-moving catalysts plus an active geopolitical flashpoint, it suggests investors are either positioned for a benign outcome or underpricing the tail risk.\n\nThe Strait of Hormuz remains the primary source of that tail risk. President Trump cancelled an envoy trip to Islamabad, and Iran reportedly offered to reopen the Strait in exchange for delaying nuclear programme discussions. The proposal has not been met with confidence.\n\n> Goldman Sachs analyst Rich Privorotsky expressed scepticism around the Iranian proposal, suggesting markets should not treat it as a resolution.\n\nWith Brent above $101 and the Brent-WTI spread widening on regional supply risk, the oil overlay is not background noise. It is the variable that sets the margin for error on everything else this week.\n\n## What the mega-cap earnings collision on Wednesday actually means\n\nOn April 29, 2026, four companies with enormous combined weight in both the S&P 500 and Nasdaq 100 report results in the same session: Alphabet, Amazon, Meta, and Microsoft. This is structurally unusual. In most earnings seasons, mega-cap technology names are staggered across multiple weeks, giving markets time to digest each result before the next arrives.\n\nThis time, there is no stagger. The market receives four signals simultaneously, and the question is whether that concentration amplifies upside, amplifies downside, or creates a binary event that index-level hedging cannot efficiently manage.\n\n

| Company | Report Date | EPS Consensus | Revenue Consensus | Index Relevance |

|---|---|---|---|---|

| Alphabet | 29 April 2026 | ~$2.62 | ~$92.22B | Top 5 S&P 500 / Nasdaq 100 weight |

| Meta | 29 April 2026 | ~$6.67 | Not independently verified | Top 10 S&P 500 / Nasdaq 100 weight |

| Amazon | 29 April 2026 | Not independently verified | Not independently verified | Top 5 S&P 500 / Nasdaq 100 weight |

| Microsoft | 29 April 2026 | Not independently verified | Not independently verified | Top 5 S&P 500 / Nasdaq 100 weight |

\n

\n\nFor Amazon and Microsoft, full consensus estimates were not independently verified at the time of writing; FactSet or Bloomberg terminals provide the most current aggregated figures.\n\n> These four companies collectively represent a substantial portion of both the S&P 500 and Nasdaq 100 by market capitalisation, meaning Wednesday’s after-hours session could functionally reprice the U.S. large-cap equity market in a single afternoon.\n\nGeneral analyst sentiment heading into the week leans optimistic. That optimism itself carries risk. When expectations are high, technically strong results can still produce a \”sell the news\” reaction if forward guidance disappoints or if AI capital expenditure commentary falls short of buy-side hopes. For any investor with broad U.S. equity exposure, Wednesday is not a peripheral event.\n\n## Understanding the Federal Reserve’s role this week (and why Powell’s exit matters)\n\n### What the Fed is expected to do\n\nThe Federal Open Market Committee (FOMC), the Federal Reserve’s policy-setting body, meets on April 28-29, 2026. The consensus expectation is a hold at the current federal funds target range of 3.50%-3.75%. The CME FedWatch tool provides the most precise live probabilities, but as of the weekend, a rate change at this meeting would be a significant surprise.\n\nA hold, however, is not a non-event. Traders will parse specific variables from Wednesday’s statement and press conference:\n\n- The rate decision itself (hold expected)\n- Forward guidance language on the pace and timing of future cuts\n- Any references to tariff-driven inflation pressures\n- The tone around labour market conditions\n- The number and nature of dissenting votes\n\n### What traders will be watching beyond the rate decision\n\nThis is Jerome Powell’s final FOMC meeting as Federal Reserve Chair, and that institutional context adds an interpretive layer that a routine hold would not normally carry.\n\nPowell’s departing language may be read as more than a current policy statement. Markets could treat it as a transition signal, an implicit commentary on what the incoming leadership inherits and what constraints the current data places on future action. Q4 2025 GDP came in at just 0.5%-0.7% annualised, providing context for why the Fed has been in a holding pattern rather than cutting aggressively.\n\nEvery word Powell chooses this week will carry extra interpretive weight, not because the rate decision itself is uncertain, but because the audience knows it is his last opportunity to shape the narrative before handing over the chair.\n\n## The Q1 GDP release and what it tells us about where the economy actually stands\n\nThe Bureau of Economic Analysis (BEA) releases the advance estimate for Q1 2026 real GDP on April 30, 2026, the morning after both the Fed decision and mega-cap earnings. The consensus forecast sits at 2.5% annualised growth.\n\n> The magnitude of the expected acceleration is itself a data point worth scrutiny: from 0.5%-0.7% annualised in Q4 2025 to 2.5% in Q1 2026. That is a sharp rebound that, if confirmed, would signal a meaningful shift in economic momentum.\n\nThe interpretive range on this print, however, is genuinely ambiguous. Three scenarios illustrate why:\n\n1. Strong beat (above 2.5%): Validates economic resilience and supports the earnings growth narrative, but simultaneously complicates the case for near-term rate cuts by removing the urgency for monetary easing. Equity markets may rally initially, then recalibrate as rate-cut timelines extend.\n2. In-line (near 2.5%): Confirms consensus expectations without forcing a repricing in either direction. The market reaction likely depends more on how Wednesday’s events landed than on the GDP figure itself.\n3. Miss (below 2.0%): Introduces recession-adjacent language into the market conversation, potentially triggering a dovish repricing of Fed expectations while simultaneously raising questions about whether the mega-cap earnings strength (if delivered) is sustainable in a slowing economy.\n\nThe same strong print can validate the Fed’s caution and raise questions about whether policy is already too tight. GDP this week is not a clean bullish or bearish signal; it is a number whose meaning depends entirely on what Wednesday established.\n\n## How these events interact, and why the sequence matters as much as the outcomes\n\n### The sequencing problem\n\nEvaluating mega-cap earnings, the Fed decision, and GDP as three independent events misses the analytical point. They arrive in a sequence that creates a compounding interpretation dynamic.\n\nWednesday afternoon delivers earnings and the Fed within hours of each other. If all four mega-caps beat and Powell’s tone reads as dovish, markets enter Thursday morning priced for optimism. A strong GDP print then confirms the narrative. But if earnings disappoint from even one name while the Fed holds with hawkish-leaning guidance, Thursday’s GDP arrives into a market already recalibrating. A strong GDP print in that context does not confirm anything; it complicates the picture by suggesting the economy is too resilient for the rate cuts the market may suddenly want.\n\nThe three primary tail-risk scenarios for the week:\n\n- Geopolitical escalation in the Strait of Hormuz that overwhelms any equity-positive signal from earnings or GDP\n- Earnings disappointment from one or more mega-cap names, compounded by index concentration risk\n- A GDP miss that triggers recession concern and reframes the Fed’s caution as insufficient rather than prudent\n\n### The oil wildcard no one is fully pricing\n\nThe Iran situation is the variable that operates independently of corporate fundamentals.\n\n> The CBOE Oil Volatility Index (OVX) sits at approximately 76, down from a peak of 121 on 11 March 2026, according to Citi strategist Stuart Kaiser. The decline reflects reduced hedging demand, but the absolute level remains elevated by historical standards.\n\nThe Brent-WTI spread already embeds a regional supply risk premium, meaning any further escalation would not begin from a neutral baseline. An oil shock of sufficient magnitude transmits directly into inflation expectations and consumer spending projections, the two inputs the Fed weighs most heavily. If the Strait of Hormuz situation deteriorates during the week, it could rapidly override whatever constructive narrative earnings and GDP might otherwise establish.\n\nThe XLE (State Street Energy Select Sector SPDR ETF) has reverted to close correlation with oil prices, suggesting energy equities are now tracking the commodity rather than broader equity sentiment. That correlation is itself a signal: energy is pricing geopolitical risk, not earnings optimism.\n\n## What this means for investors: key levels, scenarios, and what to watch\n\nThe S&P 500 close of approximately 7,194 on April 25 and futures near 7,203 establish the line in the sand. A sustained push into record territory would confirm the constructive positioning reflected in futures. A failure to break above and hold would be a warning that event risk is proving heavier than pre-week sentiment anticipated.\n\nThe priority watching order for the week:\n\n1. Monday: Geopolitical news flow, particularly any updates on U.S.-Iran negotiations and Strait of Hormuz transit status\n2. Wednesday pre-market: Positioning ahead of the earnings and Fed double event\n3. Wednesday afternoon/evening: Mega-cap earnings releases followed by the FOMC statement and Powell’s press conference\n4. Thursday morning: Q1 GDP advance estimate from the BEA, interpreted in the context of whatever Wednesday established\n\nRecommended data sources for tracking developments in real time:\n\n- CME FedWatch: Live Fed rate probability shifts\n- FactSet, Refinitiv, or Bloomberg Terminal: Updated earnings consensus estimates as companies release results\n- BEA.gov: Official GDP advance estimate release on April 30\n- CNBC, Bloomberg, Reuters: Intraday market coverage and geopolitical updates\n\nThis is not a week to navigate passively. Understanding the specific levels, the sequence of catalysts, and the interaction effects between them allows for more deliberate positioning decisions rather than reactive ones.\n\n> This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.\n\n> Past performance does not guarantee future results. Financial projections and forward-looking statements referenced in this article are subject to market conditions and various risk factors.\n\n## Where the week lands\n\nThe week of April 28, 2026 is not one event but four, each carrying its own interpretive range, arriving in a sequence that creates compounding rather than independent risk. The baseline heading in is constructive: futures near record highs, a moderate VIX, and general earnings optimism. The downside tail, however, is specific and measurable, priced into Brent above $101 and an OVX that remains historically elevated.\n\nWednesday is the fulcrum. Mega-cap earnings plus the Fed decision in the same afternoon will establish the narrative that Thursday’s GDP either confirms or complicates. Powell’s final meeting adds interpretive weight that extends beyond the rate decision itself. And the Strait of Hormuz remains the independent variable capable of overriding all of it.\n\nMarkets heading into this week are conducting a stress test across three dimensions simultaneously: corporate earnings health, monetary policy direction, and macroeconomic momentum. How all three resolve, and whether they resolve consistently, will define U.S. equities’ posture heading into May and the summer months beyond.\n\n—” } “`

The volatility positioning frameworks that preserved capital during the Strait of Hormuz-driven drawdowns earlier in 2026 offer a structured starting point: sector rotation into energy and safe-haven exposure, rebalancing thresholds calibrated to event-risk weeks, and the specific asset allocation moves that reduced drawdown when oil-driven inflation suppressed rate-cut probability.

For investors wanting to understand what Powell’s departure means beyond the rate decision itself, our full explainer on the incoming Fed leadership and balance sheet trajectory covers Kevin Warsh’s known preference for aggressive balance sheet reduction, the $2.1 trillion in additional cuts outlined in a recent Fed research paper, and the implications for reserve markets and rate-sensitive assets through 2026-2027.

The relationship between oil prices above $100 and Fed rate cut expectations has been the defining macro tension of the first half of 2026, with markets moving from pricing two cuts at the start of the year to a 73% probability of no cuts at all as energy-driven inflation blocks the easing path.

The BEA’s expenditures approach to measuring GDP advance estimates relies exclusively on demand-side components available within roughly 30 days of quarter-end, which means the Q1 2026 print will be constructed from preliminary consumption, investment, government spending, and net export data before more complete income-side figures are available for revision.

The week of April 28, 2026 delivers four simultaneous mega-cap earnings reports from Alphabet, Amazon, Meta, and Microsoft on Wednesday, the Federal Reserve's FOMC rate decision, and the Q1 2026 GDP advance estimate on Thursday, making it one of the most event-dense weeks of the year.

The FOMC is the Federal Reserve's policy-setting body, and its April 28-29 meeting is expected to hold rates at 3.50%-3.75%; this meeting carries extra significance because it is Jerome Powell's final session as Fed Chair, meaning his departing language may signal what the incoming leadership inherits.

U.S.-Iran tensions over the Strait of Hormuz have pushed Brent crude above $101 per barrel, and any further escalation could override positive signals from earnings or GDP by driving inflation expectations higher and reducing the probability of near-term Fed rate cuts.

The consensus forecast for the Q1 2026 GDP advance estimate is 2.5% annualised growth, a sharp rebound from 0.5%-0.7% in Q4 2025; a miss below 2.0% could introduce recession concerns and trigger a dovish repricing of Fed expectations.

Investors should monitor geopolitical updates on the Strait of Hormuz on Monday, track Wednesday's mega-cap earnings and FOMC statement closely, and interpret Thursday's GDP print in the context of how Wednesday's events resolved, using the S&P 500 level of approximately 7,194 as a key reference point.