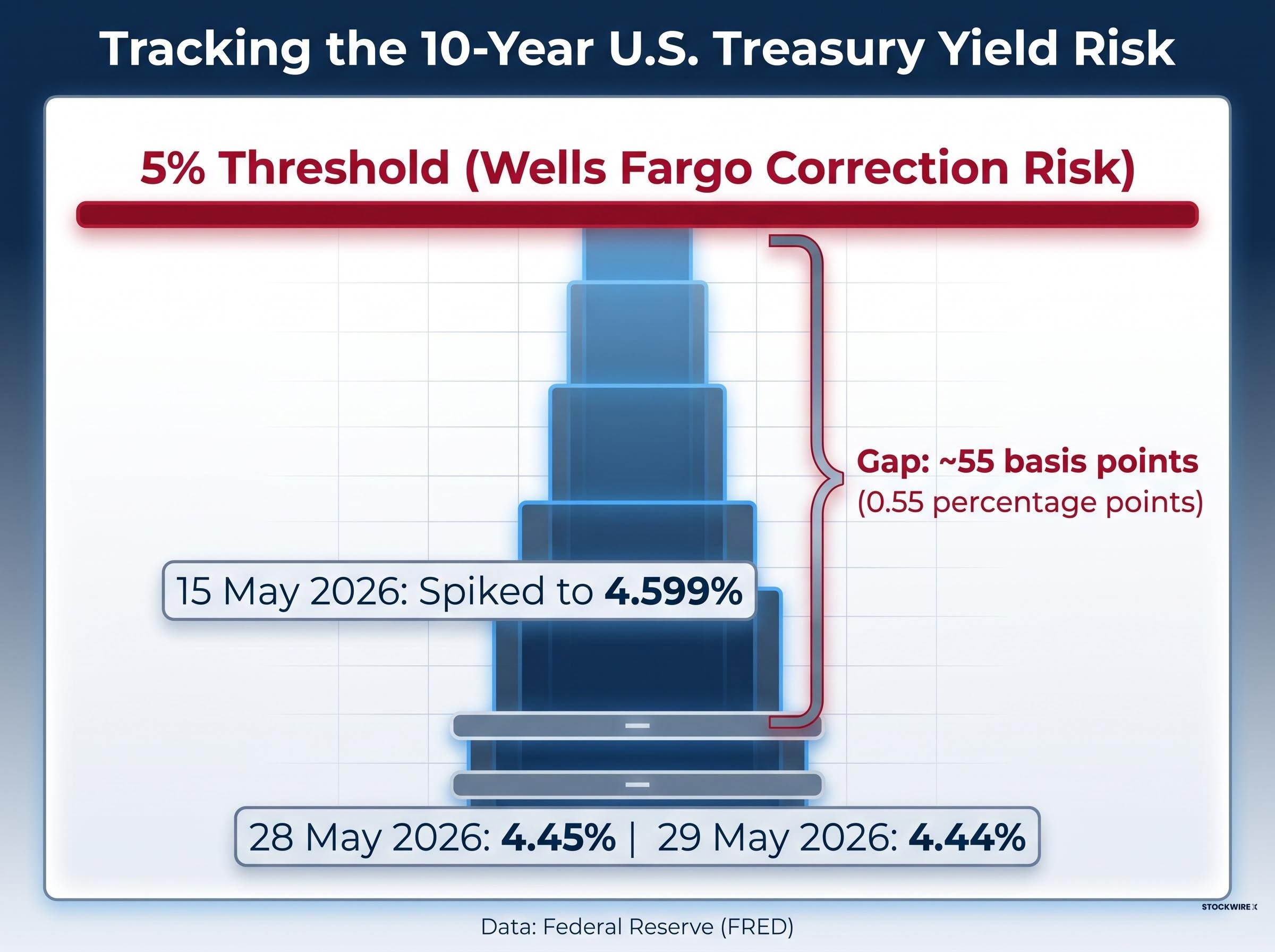

The 10-year U.S. Treasury yield closed at roughly 4.44% on 29 May 2026, sitting approximately 55 basis points below the level that Wells Fargo has identified as a potential breaking point for the current equity rally. That gap sounds comfortable until the arithmetic is laid out: the yield briefly touched 4.599% just two weeks earlier, and U.S. stocks have spent most of 2026 climbing on a foundation of AI-driven earnings growth that the same firm says could crack under its own weight. Wells Fargo’s newly published risk framework names two specific conditions capable of triggering a stock market correction, gives investors a measurable threshold to track, and pairs the warning with a positioning playbook for what to do if either trigger fires.

The two triggers Wells Fargo says could end the rally

Wells Fargo has not pointed to a single catalyst. Instead, the firm has outlined two distinct conditions, either of which it says could produce “a more meaningful pullback” in U.S. equities, language that signals a correction framework rather than a crash prediction.

The first is qualitative: a deterioration in the AI growth narrative that has underpinned large-cap technology and semiconductor valuations. The second is quantitative: a move in the 10-year Treasury yield toward 5%.

- AI narrative risk: A slowdown or reversal in AI-driven earnings expectations, particularly if capital expenditure fails to generate anticipated returns.

- Yield threshold: A climb in the 10-year U.S. Treasury yield toward 5%, compressing equity valuations and narrowing the premium investors receive for holding stocks over bonds.

The framework was outlined in a Wells Fargo note cited by Investing.com on 31 May 2026. Of the two, the yield trigger offers something the AI narrative risk does not: a specific number investors can monitor in real time.

When big ASX news breaks, our subscribers know first

Where Treasury yields stand right now and why 55 basis points matters

The 10-year yield closed at 4.45% on 28 May 2026 and 4.44% on 29 May 2026, according to Federal Reserve (FRED) data. That places it approximately 0.55-0.56 percentage points below the 5% line Wells Fargo has drawn.

The FRED DGS10 series, maintained by the Federal Reserve Bank of St. Louis, provides the daily constant-maturity 10-year Treasury yield that underpins the basis point calculations investors need to track against Wells Fargo’s 5% threshold in real time.

The gap looks manageable on a chart. It looks less so in recent memory.

On 15 May 2026, the 10-year yield spiked to an intraday high of 4.599%, driven by oil-price concerns and hotter-than-expected inflation data, before pulling back. That move closed more than half the distance to the threshold in a single session.

The 30-year Treasury yield briefly exceeded 5.19% intraday on 19 May 2026, its highest level since 2007, a move driven by the Moody’s sovereign downgrade, persistent inflation expectations, and heavy Treasury supply that pushed the broader yield curve higher across maturities and contributed to the intraday spike in the 10-year that Wells Fargo’s threshold framework is designed to track.

A 55-basis-point move is well within the range of what bond markets have delivered in compressed timeframes during 2026. The current level is not alarming on its own, but the speed at which yields can travel, as mid-May demonstrated, means the threshold is a live risk rather than a distant hypothetical. Investors tracking this framework need to watch the pace of any yield move as closely as the absolute level.

What the AI narrative risk actually means for equity valuations

The second trigger is harder to pin to a single data point, which makes it more difficult to track but potentially more destabilising. AI-driven earnings growth is not a sideshow in the current bull case; it is the load-bearing wall.

Sell-side consensus still anticipates strong double-digit earnings growth for AI beneficiaries in 2026, supported by demand for cloud-AI workloads, accelerator chips, and software monetisation. The capital expenditure commitments fuelling that growth are concentrated in three categories:

- Data centres: Hyperscaler buildouts expanding capacity across North America and Asia.

- GPUs and accelerators: Multi-year procurement cycles for next-generation chips.

- Network upgrades: Infrastructure spending to support rising AI compute traffic.

Management teams have characterised these commitments as multi-year programmes. The risk is that they become multi-year cost burdens if revenue fails to follow. A counternarrative has gained traction in early 2026 analyst commentary, centred on overbuild risk and questions about when, or whether, AI capex will generate returns that justify current spending levels.

AI capex return scrutiny has intensified through 2026 as the four largest US hyperscalers guide toward combined capital expenditure well above $600 billion annually, a scale that Goldman Sachs has flagged as surpassing dot-com era technology spending as a share of GDP and that raises the stakes considerably if enterprise revenue adoption lags the infrastructure buildout.

As of late May 2026, the prevailing consensus remains positive, but the degree of unanimity is lower than it was in 2025. That erosion matters, because the moment consensus shifts from “spend now, monetise later” to “prove monetisation now,” the premium valuations carried by AI beneficiaries face compression.

How bond markets drive equity risk, and why 5% is not an arbitrary number

The 5% threshold carries weight because of how bond yields interact with equity valuations. When the yield on a risk-free government bond rises, the return investors demand from stocks rises with it. This compresses the price-to-earnings multiples that the market is willing to pay, particularly for long-duration growth stocks whose value depends on earnings years into the future.

The mechanism runs through a concept called the equity risk premium: the extra return stocks offer above the risk-free rate. As Treasury yields climb, that premium narrows. At some point, the gap becomes too small to justify the additional risk of holding equities, and capital rotates out.

Wells Fargo has placed that inflection point near 5%. The firm is not alone in linking higher yields to equity correction risk, though the specificity of the threshold is distinctive.

The equity risk premium, the extra return stocks must offer above the risk-free rate to attract capital, stood at approximately 4.24% as of 1 May 2026 on Damodaran’s implied measure, a reading that sits in the moderate-return zone of a 65-year dataset rather than at the extreme that would signal either deep undervaluation or classic bubble territory.

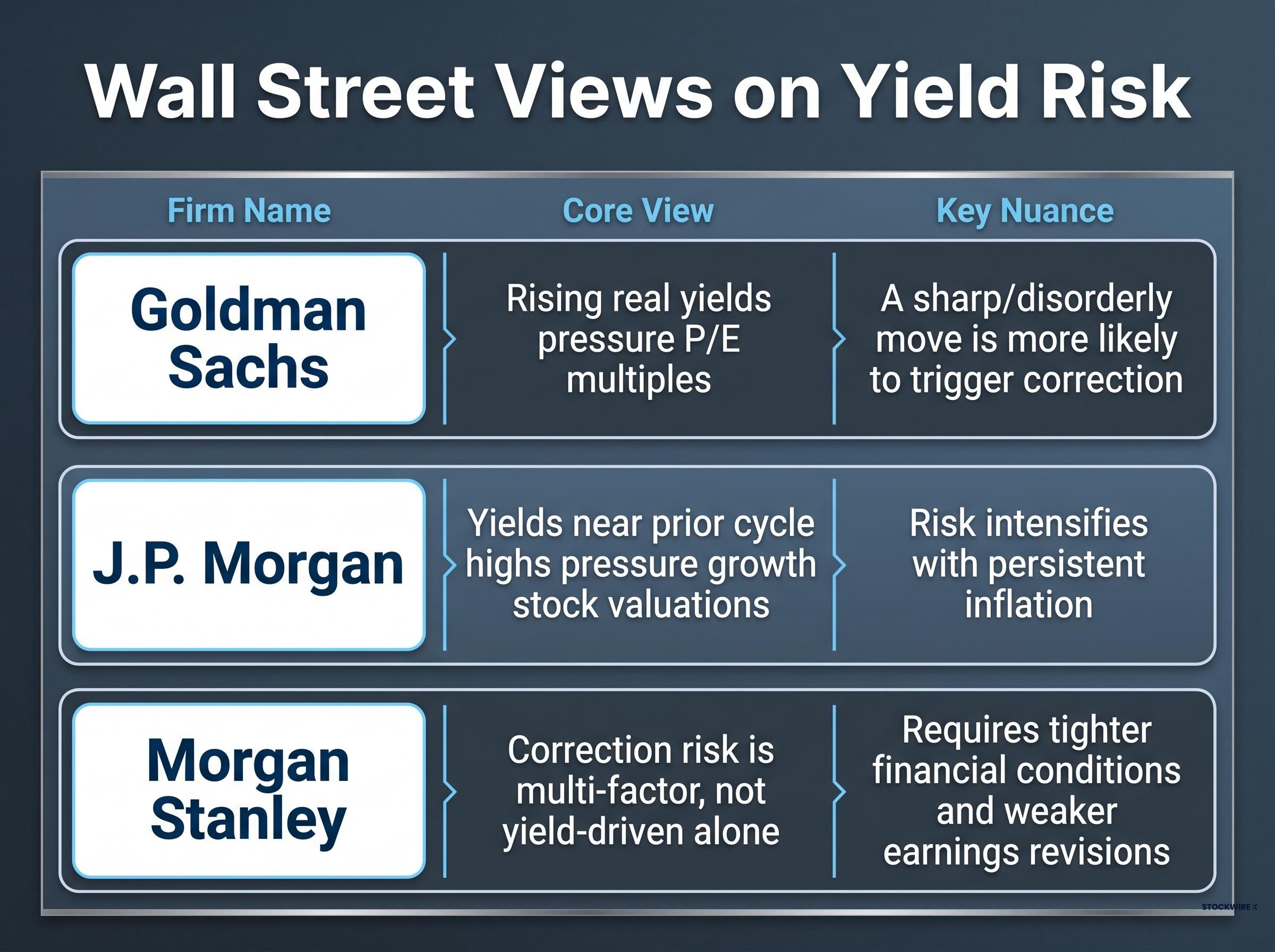

What other major Wall Street firms are saying

Several major firms broadly validate Wells Fargo’s framework while adding texture around pace versus level.

| Firm | Core View on Yield Risk | Key Nuance |

|---|---|---|

| Goldman Sachs | Rising real yields pressure P/E multiples | A sharp or disorderly move is more likely to trigger correction than a gradual drift |

| J.P. Morgan | Yields near prior cycle highs pressure growth stock valuations | Risk intensifies when accompanied by persistent inflation |

| Morgan Stanley | Correction risk is multi-factor, not yield-driven alone | Higher yields must coincide with tighter financial conditions and weaker earnings revisions |

The consensus is that the direction and pace of yield moves matter as much as the absolute number. Wells Fargo’s contribution is attaching a specific level to the risk.

The market is still rising, but the watchlist is growing

As of late May 2026, neither trigger has been activated. Treasury yields remain below 5%, and AI earnings consensus is still positive, though less unanimous than it was a year ago. U.S. large-cap equities have advanced year-to-date despite absorbing multiple volatility episodes, each of which has so far validated Wells Fargo’s view that rate-driven pullbacks are buyable.

The framework’s value is not in predicting what happens next. It is in giving investors two specific variables to monitor as conditions evolve:

- 10-year Treasury yield relative to 5%: Currently approximately 0.55 percentage points below the threshold, with recent intraday action demonstrating the gap can narrow quickly.

- AI earnings revision trends and capex return scrutiny: Consensus remains positive, but the emerging overbuild counternarrative warrants monitoring for signs of downgrade momentum.

Neither variable demands action today. Both demand attention. The rally is intact, the risks are quantified, and the distance between the two is measured in basis points and earnings revisions rather than abstractions.

Wells Fargo’s positioning playbook: large-cap equities over bonds, and buying dips

Identifying the risks is half the framework. The other half is what Wells Fargo is telling investors to do about them.

The firm’s positioning call is explicit, and it tilts toward equities despite the risks it has outlined:

- U.S. large-cap equities preferred over fixed income as the primary allocation stance.

- Investment-grade credit favoured over high-yield within fixed income, citing late-cycle dynamics and narrow high-yield spreads that offer insufficient compensation for default risk.

- Rate-driven pullbacks framed as entry points for investors with a longer time horizon.

Wells Fargo has characterised equity pullbacks driven by interest rate volatility as buying opportunities rather than signals to reduce exposure, a view consistent with how short-lived volatility episodes in 2026 have played out.

That framing carries a specific implication: the firm is not positioning for a regime change. It is positioning for a market where periodic corrections happen, where yields create temporary dislocations, and where investors who hold through those episodes are rewarded. The distinction matters, because it tells readers how Wells Fargo interprets the very triggers it has identified, as sources of opportunity within an intact bull case, not evidence of structural breakdown.

Investors wanting to stress-test Wells Fargo’s dip-buying stance against the full range of institutional views will find our deep-dive into the 2026 bull market outlook, which surveys BlackRock, J.P. Morgan, Fidelity, Morgan Stanley, and Bank of America on where they stand on equity positioning, late-cycle risk, and the case for defensively tilted portfolios as the easy gains narrow.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.