Why DBI’s 8.5% Distribution Rise Was Locked in Before the Year Started

18 mins ago

A space company that has never traded publicly is quietly shaping how Australian retail investors think about their portfolios in mid-2026. The BetaShares Space Industry ETF (ASX: RCKT) debuted on 12 May 2026 and has risen approximately 30% since listing. Global X has announced a competing space ETF under the ticker MOON, with no confirmed launch date. Both products are arriving at the same moment that SpaceX IPO speculation is intensifying, and the timing is not coincidental. What follows maps the connection between SpaceX’s anticipated public listing and the sudden availability of space-sector investment products on the ASX, examines what Australian investors can realistically expect from ETF-based exposure, and identifies the structural considerations that should shape any decision before acting.

On the surface, the narrative is straightforward: two ASX-listed ETF providers have launched or announced space-themed funds, and investors are responding. RCKT’s approximate 30% gain since its 12 May 2026 listing signals genuine appetite for the sector.

Underneath that surface sits a more specific catalyst. Both RCKT and MOON are structured as space sector funds that would be expected to add SpaceX as a constituent if, and when, the company successfully lists on a public exchange. Neither fund currently holds SpaceX. It has not listed. No formal S-1 registration statement has been filed with the U.S. Securities and Exchange Commission. No binding IPO date, listing venue, or confirmed valuation has been announced.

SpaceX has made no formal IPO filing with U.S. regulators as of the time of writing. All references to potential listing timelines remain speculative, based on market commentary rather than regulatory filings.

The ETF provider timing is widely interpreted as deliberate positioning ahead of a high-profile listing event, not routine product development. Elon Musk has publicly stated a preference to keep SpaceX private until cash flows stabilise, adding further uncertainty to any timeline. Investors buying these funds today are purchasing space sector exposure shaped by anticipation, not present-tense SpaceX ownership.

SpaceX operates across three core business areas:

The corporate portfolio extends well beyond rockets. Starlink alone has become the subject of separate listing speculation, raising the question of whether any eventual “SpaceX IPO” involves the full entity or a subsidiary carve-out.

One version of a SpaceX public listing that has circulated in media commentary involves a Starlink-only offering rather than the full SpaceX parent. For ETF investors, the distinction matters: a Starlink-only listing would likely carry a different index classification and weighting profile than a full SpaceX listing, potentially affecting how and when products like RCKT and MOON absorb the exposure. This remains unconfirmed but is worth tracking as a structural variable.

The scale of any potential listing commands attention. Media reporting from mid-2024 referenced a private-market valuation of approximately US$180-190 billion, based on secondary share transactions. Subsequent market commentary has cited projections running significantly higher, though those later figures lack confirmed sourcing from named publications. Related coverage has speculated that a successful IPO could position Musk as the world’s first trillionaire, though such projections remain forward-looking estimates subject to market conditions.

Australian retail investors face a genuine structural barrier when it comes to U.S. IPOs. Standard brokerage accounts available in Australia do not typically provide access to IPO allocations on U.S. exchanges. Even investors with international trading accounts are rarely eligible for institutional-grade IPO pricing. Direct SpaceX shares at listing price would be effectively inaccessible through conventional retail channels.

Direct SpaceX access routes for Australian investors are constrained by a structural reality: domestic brokers do not offer IPO allocations on U.S. exchanges, and investors who open international brokerage accounts to buy on secondary markets face first-day volatility, AUD to USD conversion costs, and the likelihood of purchasing well above the institutional offer price.

ASX-listed ETFs tracking space indices offer a structural answer: once SpaceX lists and meets index eligibility criteria, the ETF adds the stock as a constituent, and Australian investors gain exposure through their existing ASX brokerage account. The wrapper is familiar, the access is real, and the cost is a management fee rather than an IPO allocation lottery.

The timing nuance complicates this picture. ETF inclusion does not occur at the IPO moment. Newly listed companies are assessed against rules-based eligibility criteria, including minimum market capitalisation thresholds and free-float requirements. Only after meeting those criteria, and after an index rebalancing cycle, does the company enter the index. ETF investors may gain SpaceX exposure weeks or months after the IPO date, not on day one. RCKT charges a management fee of 0.57% per annum, representing an ongoing cost that direct shareholders would not incur.

| Attribute | Direct U.S. IPO shares | ASX space ETF |

|---|---|---|

| Access for Australian retail investors | Effectively unavailable through standard channels | Available via any ASX brokerage account |

| Timing of SpaceX exposure | At IPO pricing (if allocated) | Post-IPO, after index eligibility and rebalancing |

| Cost structure | Brokerage at purchase and sale only | Ongoing management fee (RCKT: 0.57% p.a.) |

| Concentration risk | 100% single-stock exposure | Diversified across multiple space sector holdings |

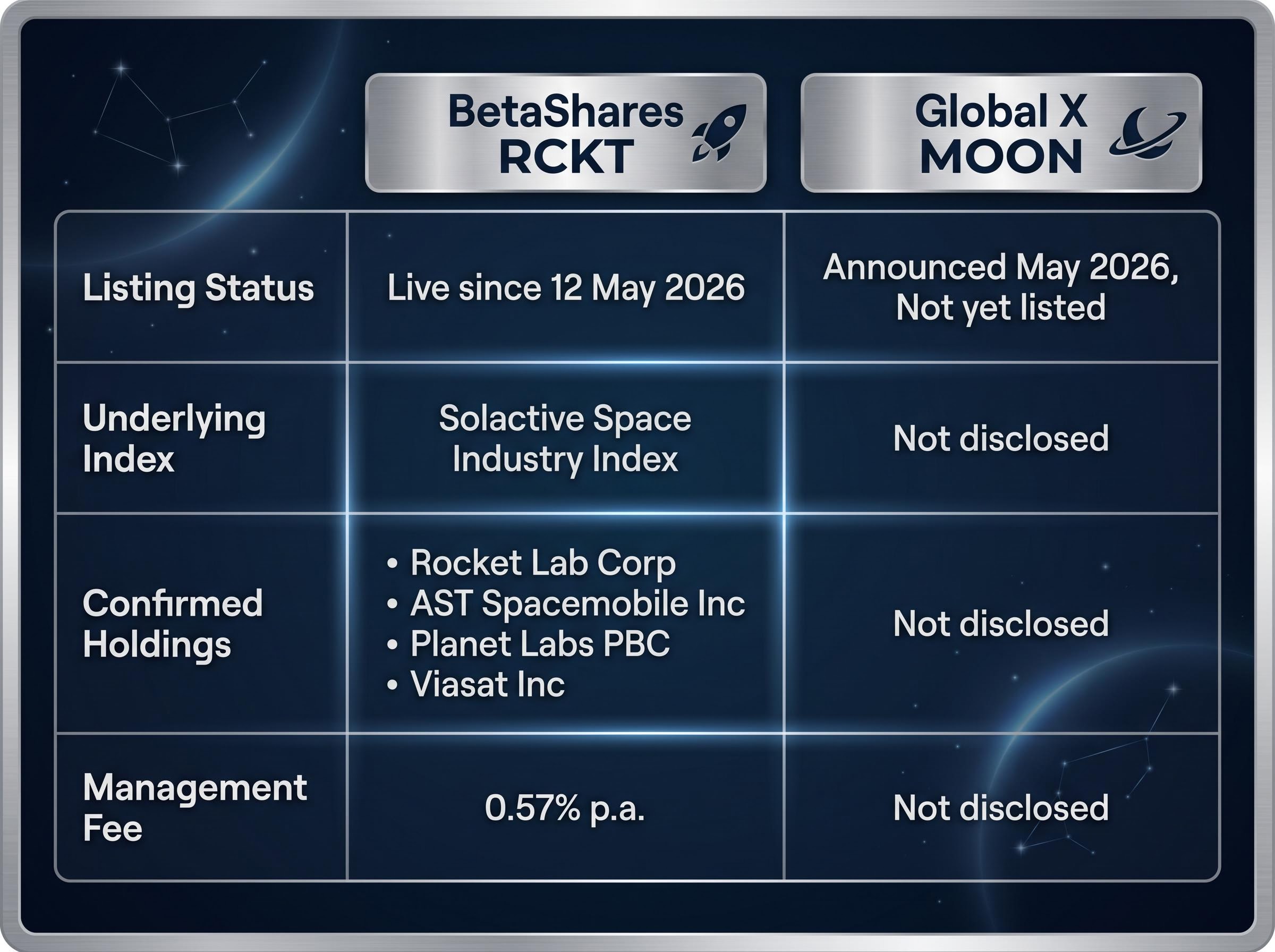

RCKT tracks the Solactive Space Industry Index, a rules-based benchmark that selects companies with revenue or operational exposure to the space economy. Its confirmed top holdings as of listing include:

These are the companies investors actually own today when they buy RCKT. None of them is SpaceX. The fund charges a management fee of 0.57% per annum and has gained approximately 30% since its 12 May 2026 debut, reflecting strong early investor sentiment toward the space theme.

Global X MOON presents a less complete picture. Announced in May 2026, MOON has not yet listed on the ASX. No underlying index, confirmed holdings, or management fee has been publicly disclosed. Comparative analysis is limited until those details are available.

ASIC’s regulatory guide for exchange-traded product issuers (RG 282) sets out portfolio disclosure requirements, product naming obligations, and general conduct standards that ETF providers listing thematic funds on the ASX must satisfy, providing a framework that underpins the disclosure expectations investors can hold RCKT and MOON to.

| Attribute | BetaShares RCKT | Global X MOON |

|---|---|---|

| ASX ticker | RCKT | MOON |

| Listing status | Live since 12 May 2026 | Not yet listed |

| Underlying index | Solactive Space Industry Index | Not disclosed |

| Confirmed holdings | Rocket Lab, AST Spacemobile, Planet Labs, Viasat | Not disclosed |

| Management fee | 0.57% p.a. | Not disclosed |

Neither fund holds SpaceX because SpaceX is not publicly listed. No ETF provider publishes planned weightings for unlisted companies. Investors evaluating RCKT should assess whether the existing portfolio composition aligns with their risk appetite independent of any future SpaceX addition.

The SpaceX narrative is compelling. The risk picture deserves equal attention. Three distinct layers of risk are worth holding in view:

The thematic ETF behaviour gap, the divergence between a fund’s reported time-weighted return and the money-weighted return actually experienced by investors, is measurably worse in high-sentiment sectors; the ARK Innovation ETF reported a 233% cumulative gain while the typical investor experienced approximately negative 35%, a pattern driven by concentrated inflows near peak valuations that mirrors the conditions currently surrounding space sector funds.

The RCKT risk profile carries specific dimensions worth quantifying: Rocket Lab and AST SpaceMobile together represent 23.3% of the fund, 74.3% of holdings are in unhedged USD-denominated equities, and Morningstar has assigned a high-risk designation with estimated annualised volatility of 28%, while UBS Australia has recommended capping the position at less than 5% of a portfolio.

The most consequential variable in this investment thesis, whether and when SpaceX lists, remains entirely outside any ETF provider’s control.

RCKT’s 30% gain since listing partly reflects SpaceX IPO anticipation. Some portion of a positive future scenario may already be priced in. ETF tracking error and ongoing management fees represent an additional drag on returns relative to hypothetical direct exposure. Against a diversified index fund, the concentration of thematic ETF risk is measurably higher.

Past performance does not guarantee future results. These statements are speculative and subject to change based on market developments and company performance.

The strategic case is genuine: ASX space ETFs represent the most accessible and cost-efficient pathway available to Australian retail investors for eventual SpaceX exposure. Direct U.S. IPO access is not practically available through standard channels, and ETF wrappers solve a real structural problem.

What investors should be monitoring before acting:

Time horizon shapes the decision. Investors with a long-term view on the space sector may find current ETF exposure coherent regardless of IPO timing; the existing holdings carry their own investment case. Short-term investors positioning specifically for an IPO-driven price event face higher timing and valuation uncertainty, given that ETF inclusion post-IPO depends on index rebalancing schedules with no guaranteed entry point aligned to the listing date.

RCKT remains the only currently live product with a confirmed structure and fee. MOON is an announced but unquantified option requiring further disclosure before meaningful comparison is possible.

Investors wanting a precise breakdown of the listing mechanics should read our full explainer on the SpaceX Nasdaq listing timeline, which covers the SPCX ticker designation, the June 11 pricing date, Starlink’s $8.2 billion in 2025 revenue and $7 billion in adjusted EBITDA, and the anticipated $50-75 billion raise that would make this the largest IPO in recorded market history.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The SpaceX IPO is a legitimate catalyst for space sector investing interest in Australia. For the first time, Australian investors have an ASX-listed vehicle to participate in the global space economy, and a second product is imminent. That is genuinely new.

The actual SpaceX exposure event, however, is structurally deferred. No filing has been made. No timeline is confirmed. No ETF currently holds the stock. The chapter in Australian investor portfolios that involves SpaceX directly will begin when, and only when, the company lists on a public exchange and meets the index eligibility criteria that determine ETF inclusion. Until then, the products available offer space sector exposure, not SpaceX exposure, and the distinction matters.

—

The BetaShares Space Industry ETF (ASX: RCKT) is an ASX-listed fund tracking the Solactive Space Industry Index, holding companies like Rocket Lab and AST SpaceMobile. It does not currently hold SpaceX, but is structured to add it as a constituent once SpaceX lists publicly and meets index eligibility criteria.

No, Australian retail investors cannot typically access U.S. IPO allocations through standard domestic brokers, and even those with international accounts face first-day volatility and the likelihood of buying well above the institutional offer price. ASX-listed space ETFs are considered the most accessible alternative once SpaceX meets index inclusion criteria.

ETF inclusion does not happen on IPO day. Newly listed companies must meet rules-based eligibility criteria including minimum market capitalisation and free-float requirements, and then pass through an index rebalancing cycle, meaning ETF investors could gain exposure weeks or months after the IPO date.

Key risks include IPO timing uncertainty (no confirmed filing or date exists), post-listing valuation risk if SpaceX enters the index at a premium above its IPO price, and the inherent volatility of thematic ETFs concentrated in high-growth or pre-profit companies, with RCKT carrying an estimated annualised volatility of 28% per Morningstar.

RCKT charges a management fee of 0.57% per annum and currently holds companies including Rocket Lab Corp, AST SpaceMobile Inc, Planet Labs PBC, and Viasat Inc. SpaceX is not a current holding as it has not yet listed on a public exchange.