Aristocrat’s Profit Is Surging, but Its Share Price Has Fallen 13%

34 mins ago

Dalrymple Bay Infrastructure just announced a 28.62 cent per security distribution for FY2026/27, an 8.5% increase on the prior corresponding period. Most investors will register the headline number. Fewer will recognise that the increase was structurally locked in before the financial year even started.

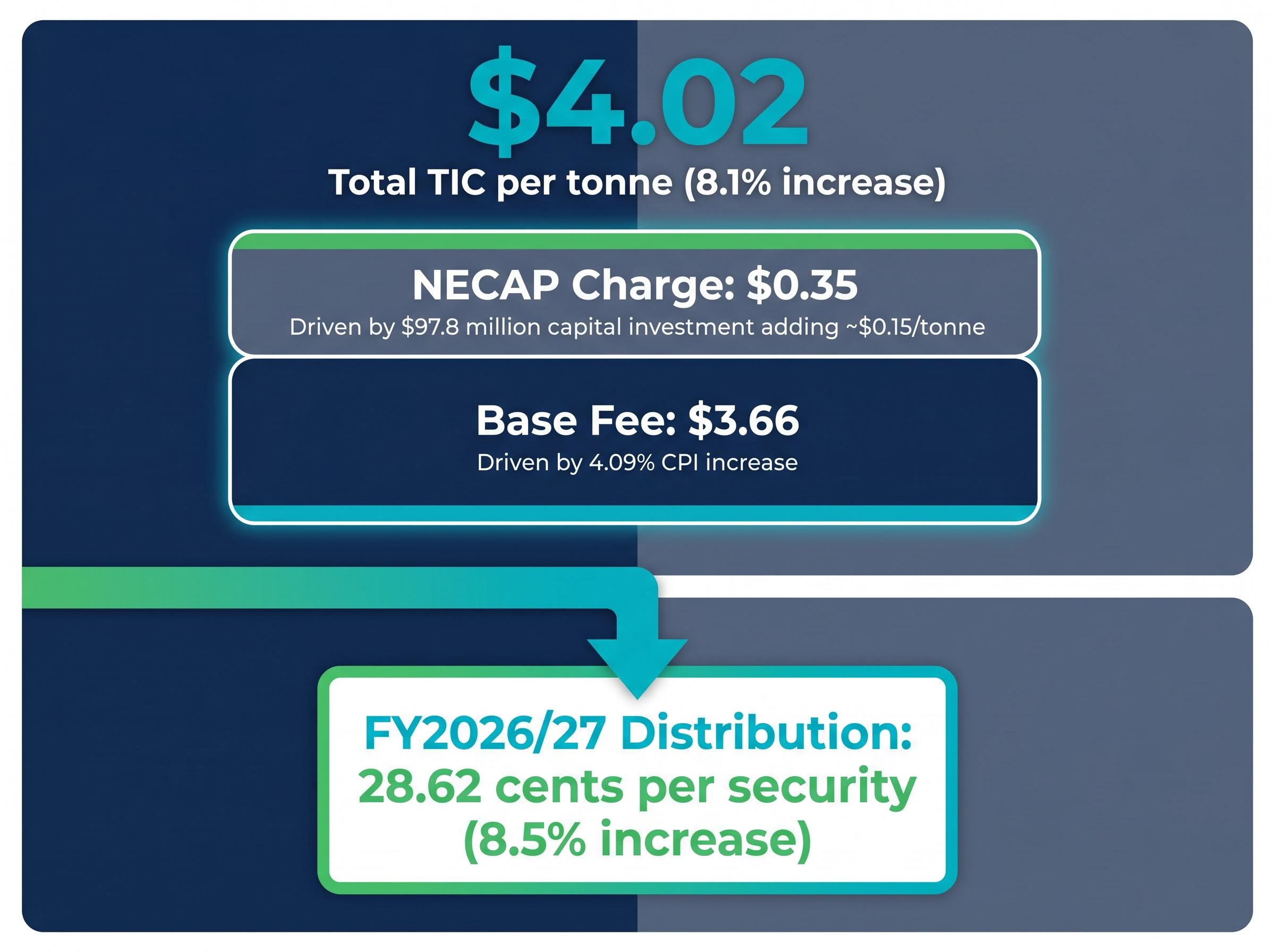

On 19 May 2026, DBI released its quarterly update disclosing an 8.1% rise in its Terminal Infrastructure Charge (TIC) to $4.02 per tonne, effective 1 July 2026. The connection between that per-tonne fee adjustment and the distribution increase is not coincidental. It is the entire business model.

What follows is an examination of the contractual architecture behind DBI’s revenue: how the TIC’s two components (the CPI-linked base fee and the NECAP capital recovery charge) work together to produce distributions that grow with inflation and capital deployment rather than coal prices or throughput volumes.

The instinct is understandable. A company operating Australia’s largest coal export terminal should, logically, be a coal bet. That instinct is wrong.

DBI collects its Terminal Infrastructure Charge on contracted annual capacity, not on actual tonnes shipped. The structure is take-or-pay: customers including Peabody Energy, Stanmore Resources, and Whitehaven Coal pay for their contracted capacity whether or not they use it. As at the 2025 annual result, DBI held 84.2 million tonnes of fully contracted take-or-pay capacity.

Take-or-pay contract structures transfer utilisation risk from the infrastructure operator to the customer and are consistently valued at a premium to usage-based revenue arrangements, a distinction that applies across asset classes from coal terminal capacity agreements to AI network connectivity contracts.

Take-or-pay principle: DBI bills contracted capacity regardless of actual shipment volumes. Revenue is a function of agreements, not operations.

The remaining revenue lines net to zero for distribution purposes:

Terminal capacity has grown from 14.5 million tonnes per annum in 1983 to 85 million tonnes currently, but it is the contracted capacity, not the physical throughput, that determines revenue. Volume risk sits with the customers, not with DBI.

The TIC is not a single number adjusted at management’s discretion. It is a formula with two moving parts, and under normal conditions both parts move upward.

| Component | FY2026/27 Rate ($ per tonne) | Change Driver |

|---|---|---|

| Base Fee | $3.66 | CPI-linked annual adjustment (4.09% increase) |

| NECAP Charge | $0.35 | Capital investment added to recoverable asset base |

| QCA Levy | Negligible | Regulatory cost recovery |

| Total TIC | $4.02 | 8.1% increase on prior year |

The base fee resets each 1 July based on the prior year’s Consumer Price Index outcome. There is no renegotiation, no regulatory approval required for the annual adjustment. Inflation flows directly and automatically into DBI’s per-tonne pricing.

CPI-indexed infrastructure models have become one of the primary drivers of the ASX industrials sector’s five-year outperformance over the broader ASX 200, because automatic annual price resets remove the negotiation risk that caps revenue growth for operators without contractual inflation pass-through.

The implication for investors is direct: elevated inflation periods produce above-average TIC growth. The 4.09% base fee increase for FY2026/27 reflects exactly that mechanism at work.

NECAP stands for Non-Expansion Capital Expenditure. Every dollar of qualifying capital expenditure DBI incurs is added to a recoverable asset base, on which DBI earns an ongoing return linked to bond yields. That return is recovered through the NECAP component of the TIC.

Over the past year, $97.8 million of additional capital investment was added to the NECAP asset base. That addition is the direct cause of the approximately $0.15 per tonne increase in the NECAP charge. As long as DBI continues investing in qualifying capital works and bond yields remain at current levels, this component compounds.

The 8.5% distribution increase is not a management decision made in isolation. It is arithmetic.

Because handling costs, capital works costs, and operating expenses all pass through at zero margin, TIC revenue after those pass-throughs is the primary source of distributable cash. The pathway is mechanical:

FY2026/27 distribution: 28.62 cents per security, representing an 8.5% increase on the prior corresponding period.

The TIC increase is not the only tailwind. Debt refinancing completed over the past year, including a $350 million Australian Medium-Term Note priced on 13 March 2026, is projected to deliver approximately $75 million in interest cost savings. That saving flows directly to distributable cash alongside the higher TIC.

FY25 provided the precedent: Funds From Operations (FFO) rose 10.6% while distributions per security grew 11.9%. The pattern is structural, not episodic.

For most equities, yield is an incomplete valuation signal because future earnings are uncertain. DBI is different. The contracted, take-or-pay revenue base means cash flow visibility is unusually high, making yield a more direct measure of value than price-to-earnings ratios or discounted cash flow models.

Contracted infrastructure assets like DBI sit in a narrow category where dividend yield as a valuation signal carries more weight than conventional earnings multiples, precisely because the cash flow underpinning each distribution is secured years in advance through take-or-pay agreements rather than exposed to operational volume risk.

Two yield thresholds emerge as practical benchmarks:

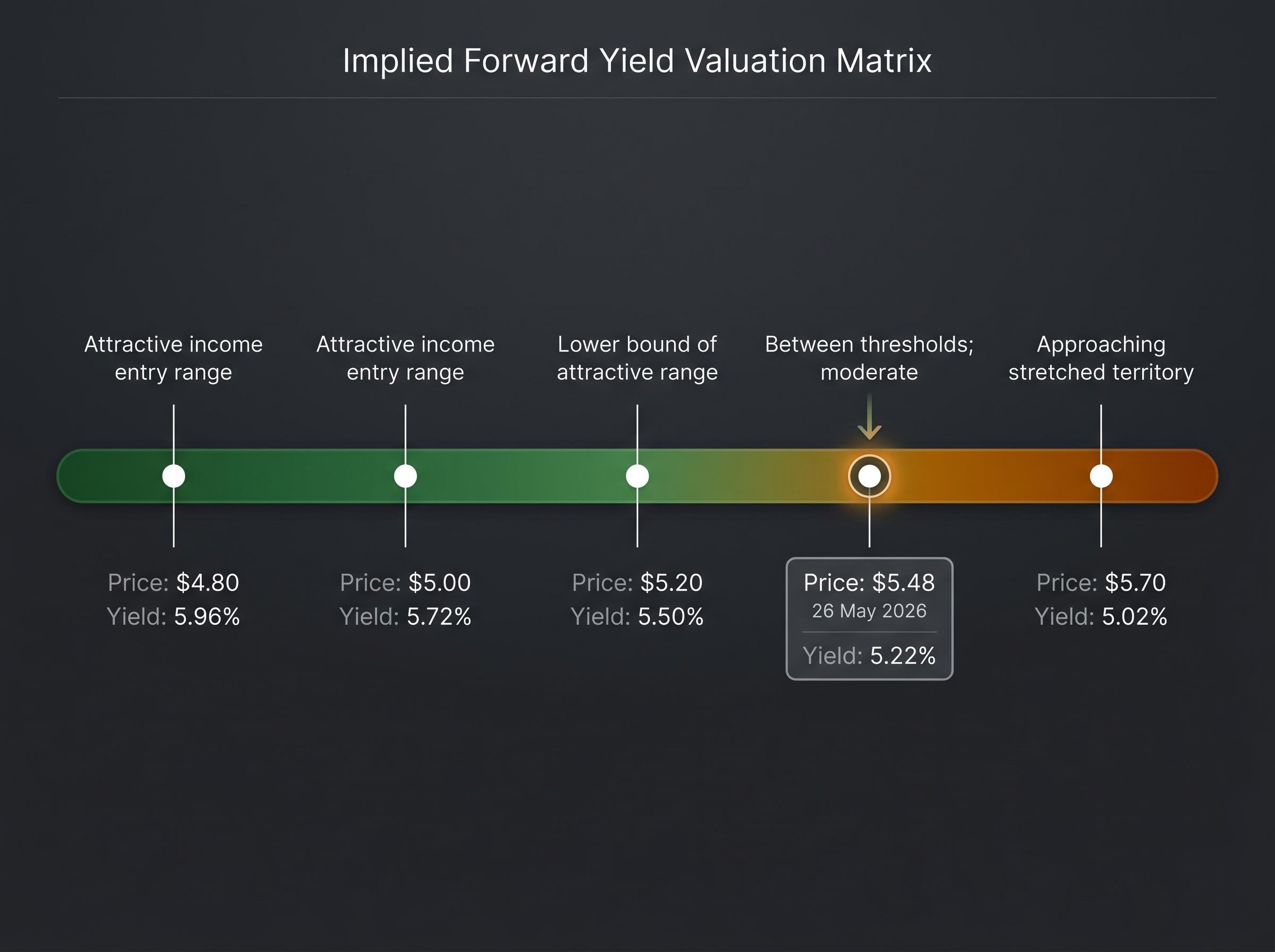

At the 26 May 2026 share price of $5.48, the implied forward yield on the 28.62 cent distribution is approximately 5.2%, sitting between the two thresholds.

| Share Price | Implied Forward Yield | Valuation Signal |

|---|---|---|

| $4.80 | 5.96% | Attractive income entry range |

| $5.00 | 5.72% | Attractive income entry range |

| $5.20 | 5.50% | Lower bound of attractive range |

| $5.48 | 5.22% | Between thresholds; moderate |

| $5.70 | 5.02% | Approaching stretched territory |

DBI’s share price has risen approximately 34% over the prior twelve months and roughly doubled over three years. Intelligent Investor published a BUY recommendation at a review price of $5.01 on 4 March 2026, noted here as historical context rather than a current assessment.

Two block trades by Brookfield in 2025 tested whether DBI’s yield-driven valuation could absorb large, technically motivated sell-downs. Both times, it did.

| Date | Stake Sold | Transaction Value | Discount to Close | Day-of Price Fall | Recovery Period |

|---|---|---|---|---|---|

| 12-13 June 2025 | 23.2% | ~$428 million | 7.9% ($3.72/share) | 6.1% | ~6 trading sessions |

| 9 September 2025 | ~26% | $527 million | 6.9% ($4.05/share) | 6.4% | ~9 trading sessions |

Neither trade reflected a change in DBI’s business or earnings outlook. Both were structural sell-downs driven by discount pricing mechanics. The recovery pattern in each case was identical: the temporary price decline pushed DBI’s implied yield higher, which attracted income-seeking buyers who corrected the price within one to two weeks.

Three implications follow for current investors:

Three structural pillars support DBI’s distribution profile:

The $75 million in projected interest cost savings from recent debt refinancing adds a near-term earnings tailwind that does not depend on TIC mechanics, reinforcing distribution visibility over the next several years.

The tension for prospective investors is straightforward: DBI’s share price has roughly doubled over three years and risen approximately 32% in twelve months. Forward distributions of 28.62 cents per security are growing, but the yield at current prices sits at approximately 5.2%, below the 5.5-6.0% range that has historically attracted income-focused capital.

Income-oriented investors evaluating DBI need to hold two ideas simultaneously. The contracted fee mechanism is structurally sound, and the distribution growth rate is well supported. Whether the current share price offers sufficient income return depends on the individual investor’s yield threshold.

For income-oriented investors wanting to stress-test whether DBI’s distribution profile warrants a place as a core portfolio holding versus a satellite allocation, our deep-dive into dividend investing strategy examines the conditions under which yield-focused positions earn their allocation, including quality screening, payout sustainability, and the portfolio sizing discipline that separates income investing from yield-chasing.

DBI’s 8.1% TIC increase and 8.5% distribution growth are not the product of a favourable coal market. They are the direct output of a contracted fee architecture where CPI linkage lifts the base and capital deployment lifts the NECAP charge.

The yield valuation framework outlined above provides income-focused investors with a practical tool for monitoring whether the share price remains within an appropriate range. At $5.48, the forward yield of approximately 5.2% sits in moderate territory, neither stretched nor at the attractive entry point that the Brookfield block trades briefly created.

As long as DBI continues investing in NECAP-qualifying capital expenditure and inflation remains positive, both components of the TIC have structural reasons to grow each year. The distribution follows.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Terminal Infrastructure Charge (TIC) is the per-tonne fee DBI collects on contracted capacity at its coal export terminal. It has two components: a CPI-linked base fee that adjusts automatically each year with inflation, and a NECAP charge that grows as DBI adds qualifying capital expenditure to its recoverable asset base. Because TIC revenue is the sole source of distributable earnings, any increase in the TIC flows directly into higher distributions for securityholders.

No. DBI operates on a take-or-pay contract structure, meaning customers pay for their contracted annual capacity regardless of whether they actually ship coal. As at the 2025 annual result, DBI held 84.2 million tonnes of fully contracted take-or-pay capacity, so revenue is determined by agreements rather than operational throughput volumes.

NECAP stands for Non-Expansion Capital Expenditure, and it refers to qualifying capital works that DBI invests in at the terminal. Every dollar of NECAP-qualifying investment is added to a recoverable asset base on which DBI earns a bond-yield-linked return, recovered through the NECAP component of the TIC. Over the past year, $97.8 million was added to this base, directly causing an approximately $0.15 per tonne increase in the NECAP charge and contributing to distribution growth.

At the 26 May 2026 share price of $5.48, DBI's forward yield on the announced 28.62 cent per security distribution is approximately 5.2%. This sits between two practical benchmarks identified in the article: below approximately 5% signals stretched valuation, while approximately 5.5% to 6.0% has historically attracted income-focused capital.

Brookfield completed two large block trades in 2025, selling stakes of approximately 23.2% and 26% at discounts of 7.9% and 6.9% respectively. In both cases the share price recovered within approximately 6 to 9 trading sessions, as the temporary yield increase attracted income-seeking buyers. With Brookfield fully exited, comparable block-trade technical pressure is no longer present on the register.