In June 2025, Brookfield Asset Management sold a 23.2% stake in Dalrymple Bay Infrastructure at a 7.9% discount to the prior close. The share price fell 6.1% on the day. Six trading sessions later, it had fully recovered.

For retail investors watching the DBI price drop on their screens, the instinct was understandable: something must be wrong. Nothing had changed about the business. What changed was the price, and with it, briefly, the implied dividend yield. That temporary dislocation, and what it reveals about how dividend yield functions as a valuation signal for contracted infrastructure assets, is the lesson this article unpacks.

What follows uses DBI’s two Brookfield sell-downs as a concrete case study in how to interpret large block trades on ASX dividend stocks without mistaking mechanical price pressure for fundamental deterioration. The framework applies to DBI specifically, but the principles transfer to any contracted infrastructure name where yield is the primary valuation input.

Why DBI’s cash flow model makes yield a credible valuation signal

Dalrymple Bay Infrastructure operates a coal export terminal in Queensland under a revenue model structurally unlike most ASX-listed equities. Three features make it unusual:

- Terminal Infrastructure Charge (TIC) on contracted capacity: Revenue is collected on 84.2 million tonnes of fully take-or-pay contracted capacity, not on actual coal shipped. Customers pay regardless of throughput volumes.

- Full cost pass-through: All operating and maintenance costs pass directly through to customers. In the 2025 full-year result, handling revenue and handling costs each totalled $351.7 million, appearing as matching line items that cancel out and do not affect distributable earnings.

- NECAP recovery mechanism: Non-Expansion Capital Expenditure (NECAP), the spending required to maintain the terminal’s existing capacity, is recoverable through a per-tonne charge added to the TIC. This means maintenance capital does not erode distributions.

The result is a cash flow profile with near-certain forward visibility. Fitch Ratings has assigned DBI a BBB- issuer credit rating with Stable Outlook, reflecting this long-term contracted revenue framework.

DBI’s regulatory framework, administered by the Queensland Competition Authority under a QCA-approved Access Undertaking, embeds the take-or-pay contract structures and cost pass-through mechanisms at the foundation of the terminal’s contracted cash flow model, giving the revenue profile a degree of regulatory backing that most ASX dividend stocks cannot claim.

From business model to valuation framework

When distributions can be forecast with confidence, the relationship between yield and price becomes genuinely informative. If the yield expands, it is almost certainly because the price has fallen, not because earnings have deteriorated unpredictably. If the yield compresses, the price has risen.

This distinguishes DBI from most ASX dividend stocks, where distribution cuts or earnings volatility introduce noise into yield signals. For DBI, yield functions as a primary valuation input rather than a supplementary one.

The widespread misconception that a high yield is inherently attractive obscures what yield actually measures: the relationship between a fixed income stream and a changing price. Treating yield as a valuation signal rather than an income magnitude requires understanding that yield expansion can reflect a falling price rather than an improving payout, a distinction that separates disciplined analysis from yield-chasing.

When big ASX news breaks, our subscribers know first

What the market considers fair value for contracted infrastructure yields

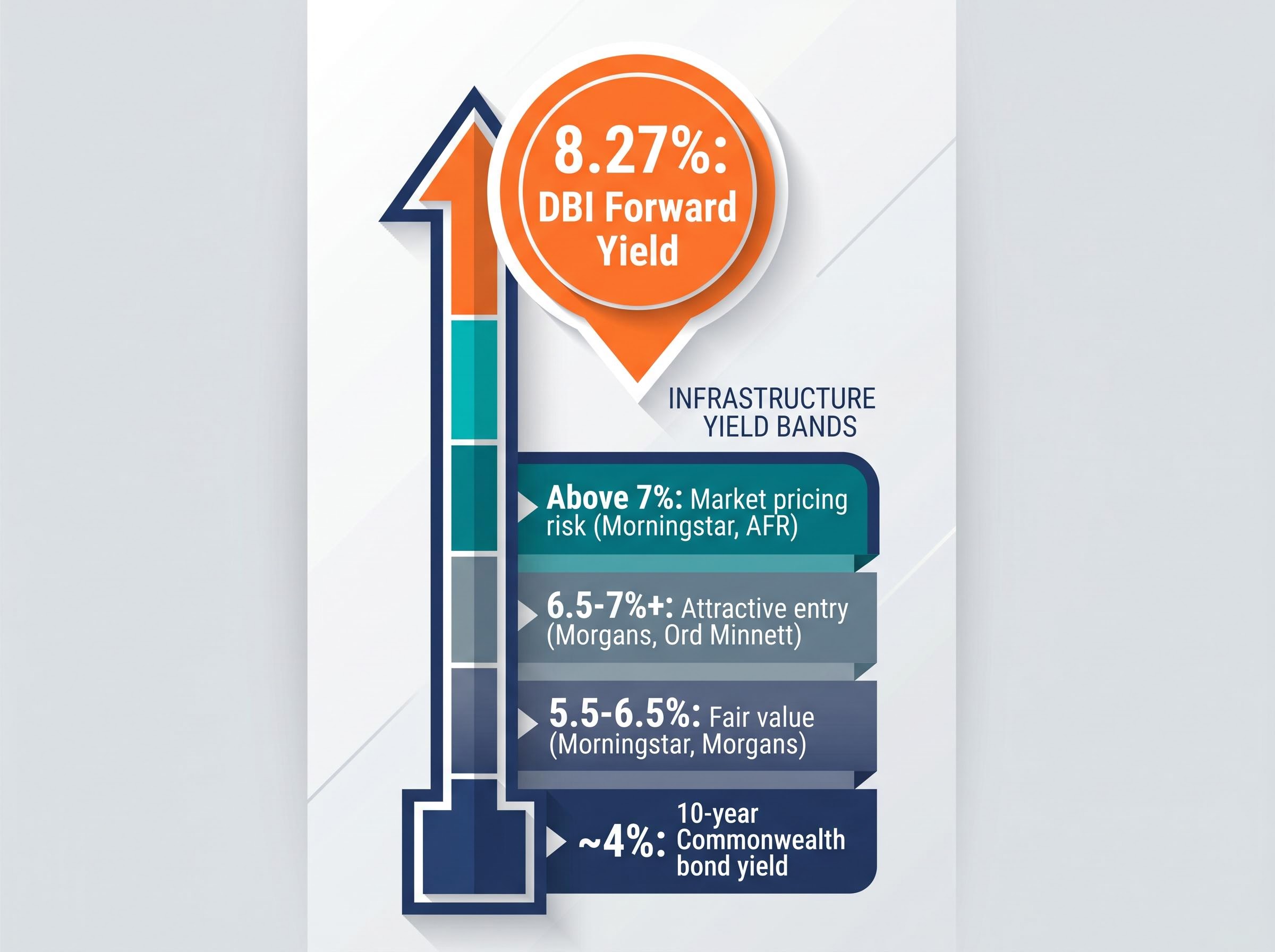

Before placing DBI’s yield on any scale, the scale itself needs calibrating. Several Australian brokers and commentators have defined yield bands for contracted infrastructure assets in the current rate environment.

The benchmark methodology centres on a spread-to-bond approach. Infrastructure equity yields are typically measured against the 10-year Commonwealth bond yield rather than against earnings multiples, because the cash flow profiles of contracted assets more closely resemble fixed-income instruments than growth equities.

Morgans Financial characterised forward yields of 5.5-6.0% for core contracted infrastructure as “broadly fair value” in a February 2025 sector update, with entry yields closer to 6.5-7% described as “attractive for long-term income investors.” Morningstar Australia suggested a 1.5-2.5 percentage point spread over 10-year Commonwealth bonds as a reasonable valuation yardstick in a March 2025 infrastructure note; with bonds trading at approximately 4%, this implied roughly 5.5-6.5% as the fair forward yield range.

Ord Minnett, in a May 2025 client note, highlighted forward yields exceeding 6.5% as compelling when distributions are at least 80% covered by contracted cash flows on a 3-5 year view. And an AFR Chanticleer column in July 2025 referenced broker commentary that yields above 7% on regulated or contracted assets are “difficult to reconcile with current funding costs unless the market is pricing in a regulatory or refinancing shock.”

| Yield Category | Forward Yield Range | Source / Basis |

|---|---|---|

| Fair value | 5.5-6.5% | ~1.5-2.5 pp over 10-year bond (Morningstar, Morgans) |

| Attractive entry | 6.5-7%+ | Morgans, Ord Minnett |

| Market pricing risk | Above 7% | Morningstar, AFR / broker commentary |

Without a benchmark, a high yield is just a number. This framework gives retail investors a calibrated reference point for assessing whether a given infrastructure yield represents opportunity, fair value, or a warning.

Where DBI’s current yield sits, and what it implies

At a last price of $3.46 as at 23 May 2026, DBI’s forward distribution of 28.62 cents per security (an 8.5% increase on the prior period) implies a forward yield of 8.27%.

DBI’s 8.27% forward yield sits materially above the 5.5-6.5% band that broker consensus identifies as fair value for contracted infrastructure, and above the 7% threshold at which markets typically begin pricing regulatory or refinancing concern.

That gap produces two competing readings. Either the market is over-discounting manageable risks, creating a yield opportunity for patient income investors. Or the risks genuinely justify the wider spread.

The case for a premium is specific. DBI’s revenue is linked to coal export infrastructure, exposing it to long-term volume and regulatory risk that Transurban and APA Group, lower-yielding “bond-proxy” peers, do not carry. The TIC is rising 8.1% to $4.02 per tonne for FY2026/27 (comprising a 4.09% CPI-linked base fee increase and a NECAP charge of $0.35 per tonne), demonstrating the inflation-linkage mechanism. But the coal exposure means the market demands more yield to hold this name than it does for a toll road.

| DBI Share Price | Implied Forward Yield |

|---|---|

| $3.30 | 8.67% |

| $3.46 | 8.27% |

| $3.70 | 7.73% |

The yield sensitivity table illustrates how quickly the implied yield shifts at modest price changes. DBI’s share price has risen approximately 32% over the prior twelve months and approximately doubled over the prior three years, compressing the yield from considerably higher levels. At 8.27%, the question is whether the remaining premium compensates adequately for the identifiable risks.

How block trades create temporary yield spikes: the Brookfield case study

Investment banks’ crossing desks price block trades at a discount to the last close for a straightforward reason: the discount compensates institutional buyers for absorbing a large parcel overnight and bearing the short-term overhang risk. The discount is a liquidity premium, not a piece of fundamental information.

Typical ASX block trade discounts range from 2-8%, according to AFR markets coverage from February 2025. In tightly held stocks, AFR’s September 2025 coverage noted spreads of 5-10% are not unusual.

Brookfield’s two DBI sell-downs followed this pattern precisely:

| Trade Date | Stake Sold | Price | Discount to Prior Close | Recovery Period |

|---|---|---|---|---|

| 12-13 June 2025 | 23.2% (~$428M) | $3.72 | 7.9% | Six trading sessions |

| 9 September 2025 | ~26% (~$527M) | $4.05 | 6.9% | Nine trading sessions |

In both cases, the day-one price decline (approximately 6.1% and 6.4% respectively) briefly expanded DBI’s implied yield before normalising as the price recovered. No guidance was revised. No distribution was cut. No operational announcement accompanied either trade.

According to Bell Potter’s equities strategy note from April 2025, retail investors often over-interpret block discounts as fundamental information. Macquarie’s trading desk described block trades as “flow events” that mean-revert when the seller is a financial sponsor with no accompanying operational announcement.

Retail investors encountering a sudden price drop must distinguish between block trade versus manipulation as the cause: block trades involve identifiable institutional sellers disclosed to the market via substantial holder notices, produce price declines proportional to the discount required to place the stock, and recover as the overhang disperses, while manipulation typically involves anonymous activity, irregular volume patterns, and no accompanying regulatory disclosure.

For any future block trade scenario, the interpretive test has three steps:

- Identify the seller type. Sponsor or asset-manager exits are frequently portfolio or fund-life decisions, not commentary on fundamentals.

- Check whether guidance or distributions changed. If neither moved, the block discount is more likely a temporary technical factor.

- Observe the typical recovery window. Many ASX block trades recover most of the discount within one to three weeks.

The next major ASX story will hit our subscribers first

Applying yield signals to entry and exit decisions for infrastructure assets

Yield compression, where the price rises and the yield falls, can function as a trim or exit signal when it pushes the yield below the “fair value” band for a given asset’s risk profile. Yield expansion, where the price falls and the yield rises, can function as an entry signal when the expansion is caused by technical factors rather than fundamental deterioration.

For DBI specifically, source theme analysis suggests a yield below approximately 5% may signal a stretched price, while the 5.5-6.0% range represents a solid entry point against the broker fair-value framework. The current yield of 8.27% sits above both thresholds.

For Australian tax-resident investors, the franking credit consideration may materially shift the calculus. The ASX Australian Investor Study 2023 found that dividends and regular income remain among the top reasons Australians invest in shares, with SMSFs and older investors prioritising high-dividend holdings. AFR reported in October 2025 that 6-7% fully or partially franked yields represent “the current sweet spot for retirees and SMSFs.” The grossed-up yield on a franked distribution can be materially higher than the headline figure, particularly for SMSFs in pension phase.

The grossed-up yield calculation matters most for franking credits for SMSF investors in pension phase, where credits are fully refundable rather than merely offsetting a tax liability, converting a headline yield into a materially higher effective return that can shift the attractiveness of an infrastructure position relative to term deposits or other income vehicles.

Yield-based valuation works best when four conditions are present:

- The asset generates contracted or regulated revenue with high forward visibility

- There is no recent history of distribution cuts

- The issuer holds an investment-grade credit rating

- Any recent price decline is attributable to an observable block trade or technical event rather than an operational catalyst

When yield signals lose their reliability

The framework breaks down when distributions are cut, when regulatory resets reduce contracted revenue, or when refinancing risk threatens the capital structure. For DBI, the Fitch BBB- Stable rating and staggered debt maturities into the early 2030s reduce, but do not eliminate, these risks. Ongoing monitoring of regulatory determinations and debt refinancing terms remains warranted.

DBI’s yield premium reflects real risk, and that is precisely the point

DBI’s 8.27% forward yield is not an unambiguous buy signal. It is an honest price for identifiable, assessable risk. The gap between that yield and the 5.5-6.5% fair-value band for core infrastructure reflects the coal-linked volume and regulatory risks that separate DBI from Transurban-style assets. The market has persistently demanded this premium, and it may be correct to do so.

Brookfield’s full exit removes one specific source of technical selling pressure. It does not eliminate the fundamental yield premium. Distribution growth of 8.5% for FY2026/27 demonstrates continued cash flow delivery against the contracted framework, but the yield remains above the Morningstar threshold at which markets typically price regulatory or refinancing concern.

The most useful question when an infrastructure stock’s yield expands sharply is not “should I buy?” but “is this expansion caused by price mechanics or by a change in the fundamental cash flow case?”

For income-focused investors wanting to model how an 8.27% forward yield fits within a broader portfolio income strategy, our dedicated guide to living off ASX dividends works through the capital requirements at different grossed-up yield assumptions, the role of franking credits in reducing the capital needed to reach a target income, and the concentration risks that arise from overweighting any single high-yield name.

Retail investors who can answer that question with evidence rather than instinct are better positioned to make disciplined decisions in the next block trade, the next yield spike, and the next moment when price and value briefly diverge.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Yield projections are subject to market conditions and various risk factors.