Why the 2026 Midterm Could Break a Rare Presidential Streak

2 hrs ago

When an Alberta regulator fined a content creator roughly $40,000 for undisclosed stock promotions, the creator had already pocketed more than $100,000 from the same posts. The penalty was real. The deterrent was not.

This is not an isolated enforcement curiosity. It is the arithmetic that governs an entire category of financial promotion, one where the rational calculation, for many promoters, still favours breaking the rules. The Polymarket investigation added a more elaborate variant: dummy trading websites, compensation routed through a CMO’s personal PayPal account, and creators who added disclosure language only after journalists started calling. Rules existed in both cases. They simply did not work.

This piece maps the specific structural conditions that make covert financial promotion a rational business decision, what proposed reforms would actually change that calculus, and where the emerging threat from AI-generated promotions fits into the same pattern. Here is the framework for assessing whether finfluencer regulation proposals are addressing the root problem or its symptoms.

The Polymarket covert promotion campaign was not a case of sloppy compliance. It was architecture.

The operation began with dummy trading websites. A site named “PO Market” used a capitalised letter “I” in its URL to visually mimic the legitimate Polymarket platform address. Creators received passwords that allowed them to stage fabricated wins for the camera. The trades were not real. The profits were not real. The audience had no way to tell the difference.

The campaign’s structural components break down as follows:

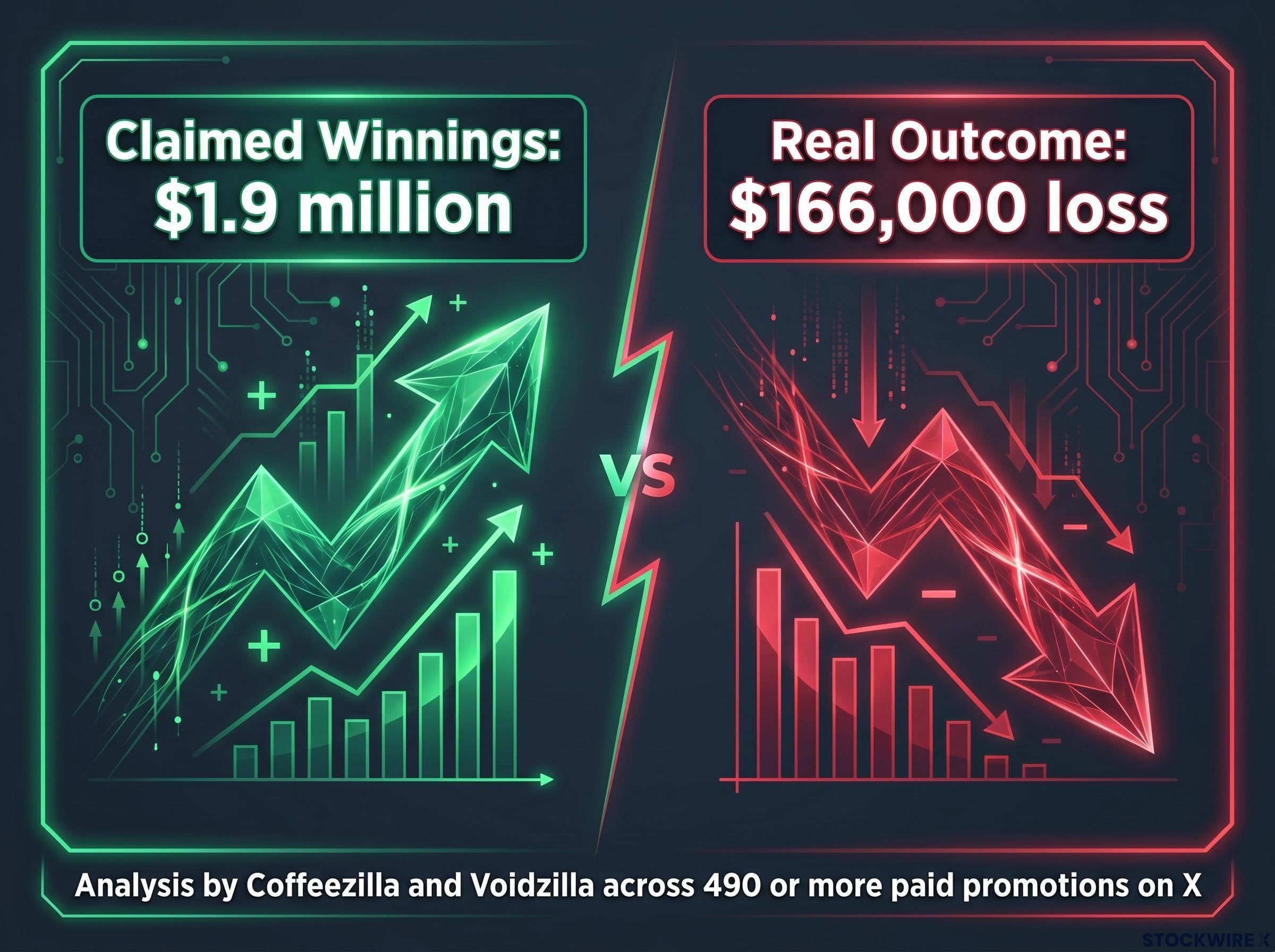

According to the Wall Street Journal, creators collectively claimed roughly $1.9 million in winnings across the videos reviewed. The trades were fabricated.

A separate investigation by Coffeezilla and Voidzilla calculated that the same bets would have collectively lost approximately $166,000 in reality. In a review of promotional ads, around 25% carried the word “free,” a framing that pointed audiences toward the idea of guaranteed or risk-free returns with no basis for scepticism.

Across 490 or more paid promotions posted on X, no clear indication of the financial relationship between creator and platform was provided. Polymarket maintained that it had no knowledge of the specific methods its marketing agency was using. The routing of payments through a personal PayPal account and the platform’s professed ignorance of its agency’s conduct are not incidental details. They reveal how responsibility can be deliberately diffused to complicate the enforcement chain, leaving no single actor clearly accountable when regulators come asking.

The Jeconomics case puts the enforcement gap into numbers a reader can evaluate in seconds.

The Alberta Securities Commission issued a penalty of around $40,000 against the Canadian creator and prohibited him from engaging in comparable promotional work for two years. During the period under scrutiny, his posts had brought in more than $100,000 in compensation. After accounting for the fine, the campaign remained financially worthwhile.

| Component | Amount |

|---|---|

| Earnings from promotional posts | $100,000+ |

| Fine imposed | $40,000 (approx.) |

| Net outcome | $60,000+ profit |

Economic deterrence theory is straightforward. The expected cost of a violation equals the probability of detection multiplied by the penalty. If that product is smaller than the expected gain, the rational actor proceeds.

Detection in influencer promotion cases is rare. The penalties, when they arrive, tend to be narrow civil fines that do not disgorge the full economic value of the campaign. That leaves misconduct in positive expected-value territory. For any reader evaluating whether enforcement is a credible check on this behaviour, the Jeconomics numbers make the answer concrete: the system as currently structured makes a fine a business cost, not a deterrent.

The problem is not that disclosure rules are absent. It is that every point where they should work in practice is a point where they break down.

Core obligations exist across major jurisdictions. In the U.S., the Federal Trade Commission (FTC) endorsement rules require that material connections between advertisers and endorsers be disclosed in a way that is clear, conspicuous, and comprehensible to ordinary viewers. In Canada, guidance published toward the end of 2024 made clear that end-of-video placements, disclosures requiring the viewer to take additional steps to access, or language that a reasonable person would find unclear or ambiguous all fall short of the required standard. Regulators have also confirmed directly that ticking the YouTube “includes paid promotion” box is insufficient to satisfy Canadian requirements on its own.

Existing rules are present across both jurisdictions. Organised campaigns disregard them, and they do so through consistent, identifiable methods.

ASIC’s April 2026 enforcement action against unlicensed creators confirmed what the Jeconomics case illustrated arithmetically: finfluencer licensing obligations are routinely ignored in part because the institutional frameworks for verifying and enforcing them at the point of consumption have not kept pace with the volume of promotional content being produced.

What regulations require:

What the Polymarket and Jeconomics campaigns actually did:

Regulations require that disclosure be prominent and delivered at the point of influence. In the Polymarket campaign, disclosure appeared only after journalists began their enquiries. The legal requirement existed but failed in its communicative purpose: audiences never adjusted their scepticism because the disclosure never reached them when it mattered.

The gap between a disclosure rule existing on paper and a disclosure actually reaching an audience at the moment of influence is where current frameworks break down. That gap is where retail investors are exposed.

Jurisdictional fragmentation is not an unfortunate regulatory complication. It is a strategic resource that organised campaigns exploit by design.

A platform like Polymarket simultaneously touches three regulatory regimes, and a different agency holds partial authority in each:

No single regulator has both full visibility and optimal incentive to intervene early. The CFTC settled with Polymarket in 2022 and renewed scrutiny after the covert campaign revelations. The Department of Justice investigated the platform but dropped its probe without charges in July 2025. The FTC could theoretically pursue advertising rule violations but has not acted. Each agency sees a piece. None owns the whole picture.

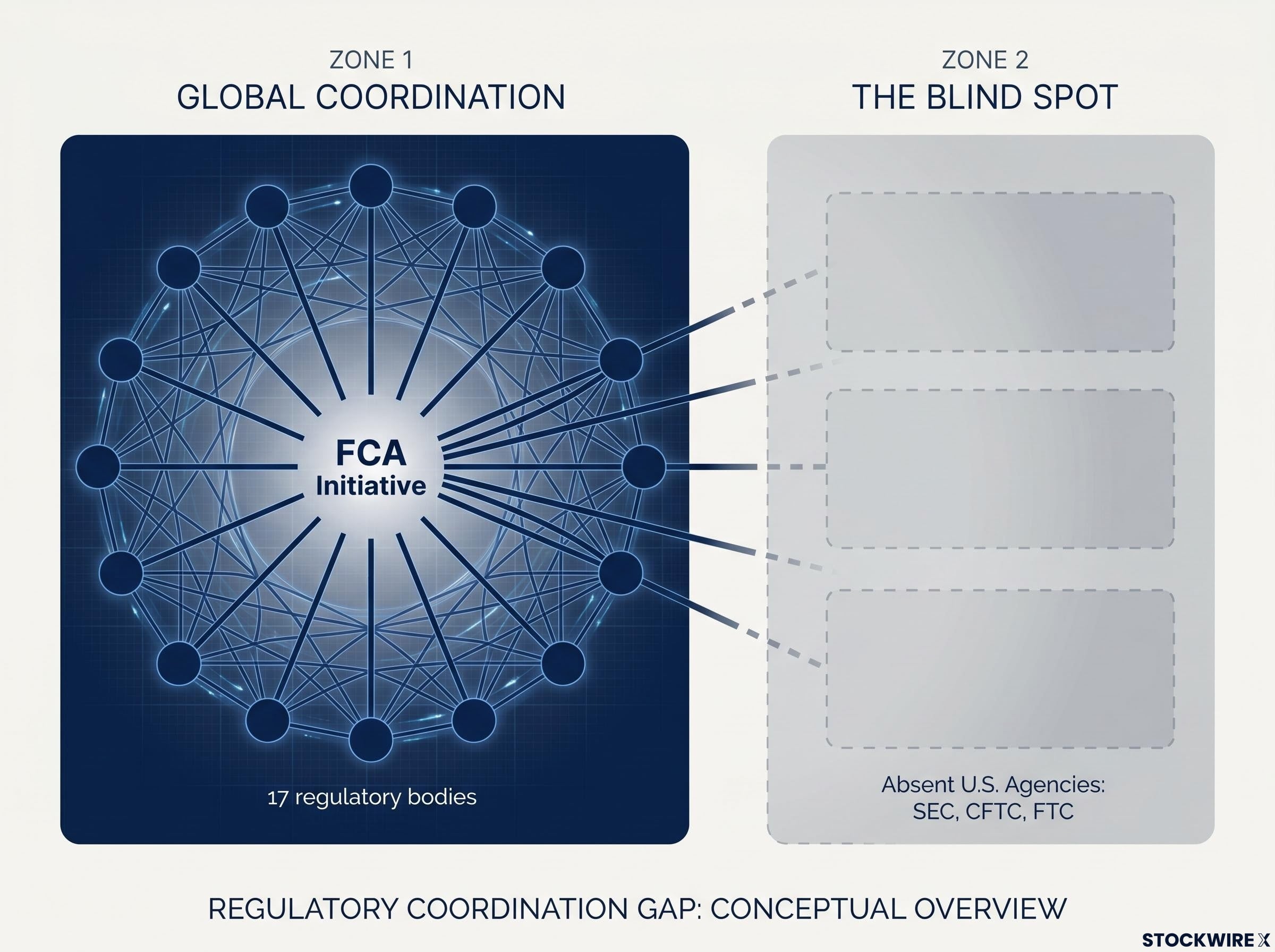

The UK Financial Conduct Authority (FCA) coordinated an annual global enforcement week directed at unlawful influencer promotion, drawing in 17 regulatory bodies from multiple countries, including Canadian authorities. It represents the most significant multinational effort to date in tackling this category of activity.

The specific gap: U.S. regulators were absent from the initiative. The SEC, CFTC, and FTC did not take part, and because U.S.-based influencers are broadly not subject to investment adviser registration obligations, companies have a structural incentive to direct their most sensitive promotional work through those individuals, where regulatory reach is weakest.

The absence of U.S. agencies from the FCA’s 17-body initiative is not a procedural footnote. It is the specific gap that allows a globally distributed campaign to route its most sensitive operations through the least accountable jurisdiction.

The AI dimension is not a separate threat. It is the same deception pattern, reproduced at lower cost and higher volume through synthetic means.

Nova Red Mining, a British Columbia-based mining company, used AI-generated video content to promote its stock rather than contracting paid human creators to do so. In a separate strand of its promotional activity, the company brought on Kirstjen Nielsen, the former U.S. Secretary of Homeland Security, as a high-profile public figure to amplify its messaging. This is not hypothetical. It is operational.

In some observed cases, AI-generated presenters mispronounced required legal disclaimers in promotional videos, a detail that captures the accountability gap in miniature: the disclaimer existed in the script, but no human was responsible for delivering it accurately.

AI-generated investment promotions share the same structural logic as the Nova Red Mining campaign: synthetic presenters, fabricated credibility signals, and content that passes platform moderation while carrying no accountability to any human promoter who can be named, licensed, or sanctioned.

The enforcement problem AI creates is structural. Disclosure and licensing frameworks assume a human promoter who can be registered, fined, or barred. Synthetic content distributes responsibility across four parties:

When content is generated by a model configured by a vendor, the company can credibly assert it did not produce the specific misleading claim. This is the same “claim ignorance” dynamic Polymarket already used. AI simply makes it cheaper to execute and harder to trace. Any regulatory framework that does not explicitly assign liability up the commissioning chain will be outpaced by AI-driven campaigns before the implementation phase is complete.

The test for any proposed reform is whether it changes the expected-value calculation for a promoter planning a campaign. Measures that do not touch the profit arithmetic or the jurisdictional blind spot leave the structural incentive intact.

Five reform categories have emerged from regulatory discussions and enforcement experience. Each addresses a different mechanism in the failure chain:

| Reform proposal | Root problem it addresses | Current status |

|---|---|---|

| Profit-based sanctions | Penalties smaller than gains | Existing laws allow disgorgement; unevenly applied in influencer cases |

| Enforceable disclosure standards | Rules exist but fail at the point of influence | Canadian guidance issued late 2024; FTC rules in place but under-enforced |

| Licensing and registration | Promotions routed through unregistered individuals | Australian model exists; Canadian informational sessions underway |

| International coordination | Jurisdictional blind spots exploited by design | FCA 17-body initiative active; U.S. agencies absent |

| AI-explicit rules | Liability diffused across commissioning chain | No jurisdiction has implemented specific framework |

In Canada, regulators have held direct outreach sessions with influencers aimed at clarifying where the boundaries of acceptable conduct lie, and further formal guidance on the rules applying to this activity is expected to follow. These are steps. Whether they change the arithmetic is the question that matters.

For readers wanting to understand how regulators are attempting to close these structural gaps in real time, our full explainer on AI regulatory accountability gaps examines ASIC’s REP 835 framework, including how frontier AI opacity breaks the accountability structures that assume a human decision-maker at the point of liability.

The Polymarket campaign, the Jeconomics fine, and the Nova Red Mining AI promotions are not three separate failures. They are three implementations of the same structural logic: covert promotion generates substantial profits, and the expected cost of getting caught remains smaller than the expected gain.

The single necessary condition for reform to work is that the penalty for getting caught must exceed the profit from running the campaign, across all jurisdictions where the campaign operates. Without that, every other reform adds procedural complexity without altering the underlying economics.

The clearest signal that reform is substantive rather than procedural will come from the next major enforcement action. If it includes full disgorgement of campaign profits plus an additional penalty, the calculus has shifted. If it produces another civil fine smaller than the earnings it targeted, the rules will keep losing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Finfluencer regulation refers to the legal frameworks requiring social media creators who promote financial products or investments to disclose paid relationships and meet advertising truthfulness standards. It matters for retail investors because undisclosed paid promotions, like the Polymarket campaign involving over 490 posts with no clear disclosure, can expose audiences to fabricated performance claims and biased recommendations without any signal to apply scepticism.

Standard civil fines frequently fall below the earnings generated by the unlawful campaign, leaving promoters in profit even after being penalised. The Jeconomics case illustrates this directly: a $40,000 fine against $100,000 in promotional earnings left a net gain of roughly $60,000, meaning the fine functioned as a business cost rather than a genuine deterrent.

Campaigns use methods including payment routing through personal accounts to obscure corporate involvement, retroactive disclosure added only after media enquiries begin, fabricated trade screenshots that make paid content look like organic user activity, and dummy websites designed to mimic legitimate platforms. The Polymarket operation combined all of these tactics across more than 490 posts.

Mandatory disgorgement of all campaign profits, combined with additional penalties on top, is the single reform with the most direct impact on the expected-value calculation that promoters make. Without profit-based sanctions, measures like improved disclosure standards or licensing requirements operate on the margins while leaving the underlying financial incentive intact.

AI-generated promotions distribute accountability across the commissioning company, the marketing agency, the model operator, and the hosting platform, allowing each party to plausibly deny responsibility for specific misleading claims. No jurisdiction has yet implemented a regulatory framework that explicitly assigns liability up the commissioning chain for AI-produced financial content, leaving enforcement frameworks structurally outpaced.