SEC Moves to End Mandatory Quarterly Reporting After 50 Years

6 hrs ago

ServiceNow shares plunged 17% on Wednesday despite the enterprise software giant posting 22% subscription revenue growth that topped its own guidance ceiling. The disconnect between strong Q1 numbers and market punishment reflects investor anxiety about decelerating forward growth and margin pressure from the company’s $8 billion Armis acquisition. For investors tracking enterprise software and AI adoption trends, the results offer a case study in how even beat-and-raise quarters can disappoint when valuations leave no room for imperfection. This article breaks down what ServiceNow actually reported, why the stock sold off anyway, and what the results signal about the AI pricing transition reshaping enterprise software.

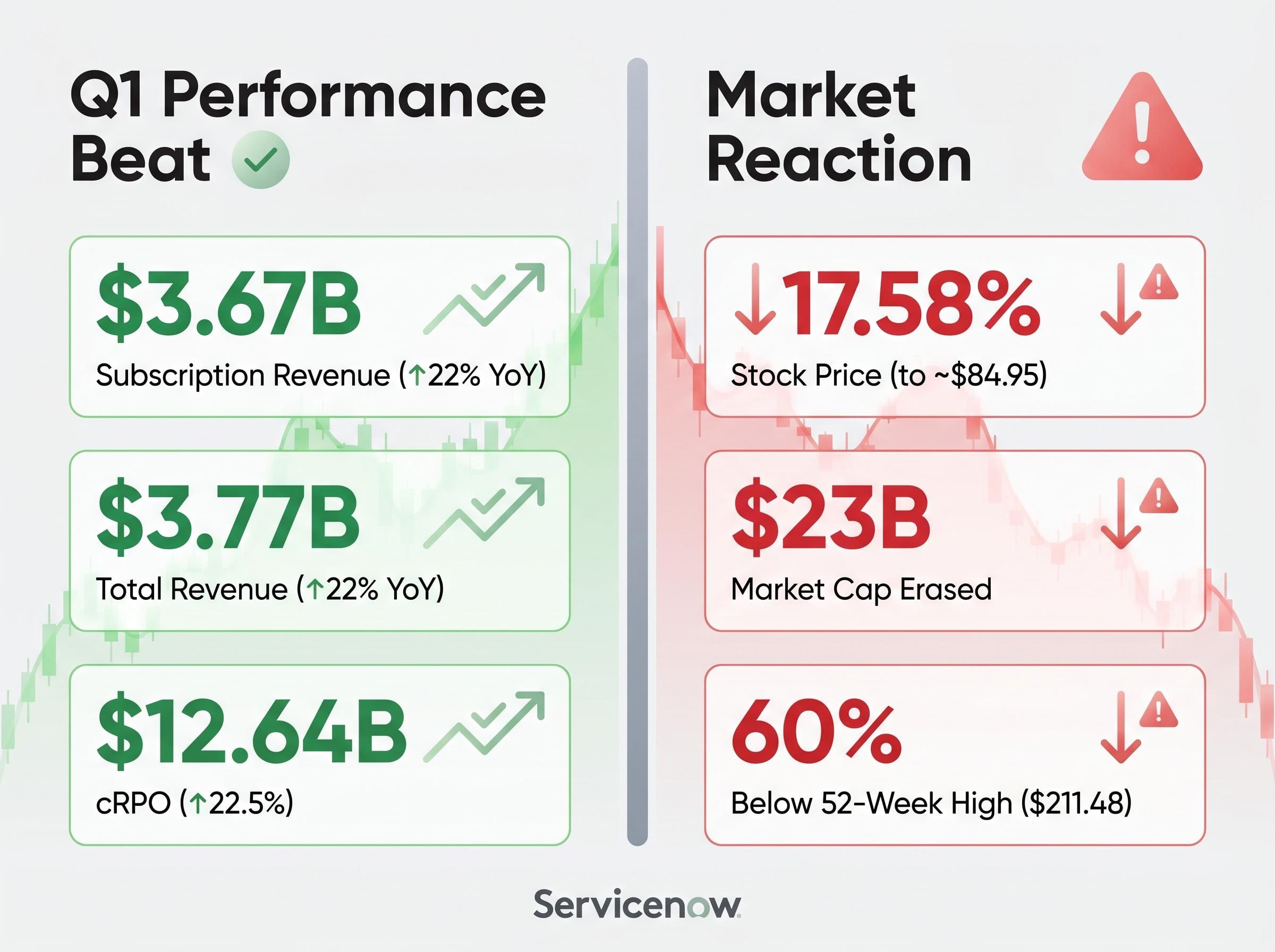

ServiceNow delivered Q1 subscription revenue of $3.67 billion, a 22% year-on-year increase that exceeded the upper end of its own guidance range. Total quarterly revenue reached $3.77 billion, also up 22%. Current remaining performance obligations (cRPO) hit $12.64 billion, growing 22.5%.

Then came the Q2 guidance. Management projected cRPO growth of 19.5% on a constant-currency basis, down from 21% in Q1. That deceleration landed hard.

Shares dropped 17.58% to approximately $84.95, erasing roughly $23 billion in market capitalisation and leaving the stock 60% below its 52-week high of $211.48. The selloff reflected a market repricing a stock that traded at roughly 50 times earnings with no tolerance for slowing momentum. When forward guidance signals deceleration at a premium valuation, operational execution alone cannot sustain the multiple.

For readers wanting to understand why operationally strong quarters can still trigger double-digit selloffs at premium valuations, our dedicated guide to the beat-and-raise paradox in high-multiple growth stocks examines Netflix’s Q1 2026 earnings where 16% revenue growth and 32% operating margins still produced a 12% share price decline when forward guidance disappointed at a 39x earnings multiple.

Q2 cRPO Growth Guidance: 19.5% constant currency, down from 21% in Q1

Key Q1 metrics:

Current remaining performance obligations represent contracted revenue ServiceNow expects to recognise within the next 12 months. For subscription businesses, cRPO functions as a leading indicator of near-term revenue trajectory, making it more forward-looking than quarterly revenue figures that reflect contracts signed months earlier.

Investors focus on cRPO growth rate changes rather than absolute dollar amounts. A deceleration from 21% to 19.5% signals that new contract signings are slowing, even if existing contracts continue to generate strong quarterly revenue. That gap explains why ServiceNow could beat Q1 guidance yet still disappoint on forward momentum.

cRPO Definition: Contracted revenue anticipated within the next 12 months, serving as a forward-looking indicator of subscription revenue trends

The Q2 guidance of 19.5% constant-currency cRPO growth marked the clearest signal yet that the pipeline was cooling. For investors unfamiliar with enterprise software metrics, understanding cRPO as a leading indicator explains why the stock moved on guidance rather than results. The metric is the market’s early warning system for subscription revenue trends.

Venura Consultants’ analysis of RPO and cRPO as SaaS valuation metrics explains why cRPO growth rates matter more than absolute dollar figures, a principle that clarifies why a deceleration from 21% to 19.5% triggered the selloff despite ServiceNow beating absolute revenue guidance.

CEO Bill McDermott disclosed on the earnings call that 50% of net new business now comes through non-seat-based pricing, a milestone that marks the AI pricing transition reaching a tipping point. The components include tokens, infrastructure, hardware, and connectors, all tied to usage rather than per-user licences.

ServiceNow signed sixteen transactions exceeding $5 million in net new annual contract value during Q1, with many structured around these consumption-based models. The shift addresses investor concerns that AI-powered automation might cannibalise traditional per-user software licensing by reducing the number of seats required. Instead, ServiceNow is positioning AI as an additive revenue stream that complements rather than replaces seat-based contracts.

The shift to non-seat-based pricing reflects a broader transformation documented across the enterprise software sector, with per-seat SaaS pricing collapsing from 21% to 15% usage in one year and IDC forecasting the model will be obsolete by 2028.

Bain & Company’s research on software pricing model transitions confirms that hybrid seat and consumption-based structures have emerged as the dominant pattern across enterprise software, positioning ServiceNow’s 50% non-seat milestone as execution of an industry-wide strategic shift rather than an isolated experiment.

AI Pricing Milestone: 50% of net new business now comes from non-seat-based pricing models

Non-seat pricing components:

The hybrid model offers a template for how incumbents might navigate the AI transition without destroying their installed base. Predictable seat revenue provides a foundation whilst usage-driven AI components layer on top, capturing demand for automation without forcing customers to rip out existing deployments. Whether this model can sustain historical growth rates as seat expansion slows remains the central question.

ServiceNow’s hybrid seat-plus-consumption pricing model mirrors strategies used across consumer and enterprise software, with the freemium model proving profitable at scale for companies like Life360, which crossed from loss-making to profitability in 2025 whilst maintaining 32% revenue growth and 26% subscriber growth simultaneously.

Two distinct headwinds compressed Q1 results and complicated the forward outlook. ServiceNow reported a 75-basis-point drag on subscription revenue growth from postponed Middle East on-premise contracts, though CFO Gina Mastantuono noted some of those deals have already closed in Q2. The timing issue was geographic and temporary.

The Armis acquisition introduced structural margin pressure. Management raised full-year subscription revenue guidance to a range of $15.735 billion to $15.775 billion, with Armis contributing approximately 125 basis points to that outlook. The margin impact, however, cuts deeper.

| Margin Category | Armis Headwind (Basis Points) |

|---|---|

| Subscription Gross Margin | 25 bps |

| Operating Margin | 75 bps |

| Free Cash Flow Margin | 200 bps |

The free cash flow margin hit matters most for investors modelling 2026 profitability. A 200-basis-point drag on a business that historically delivered expanding margins introduces a reset year where profitability improvement stalls. Management raised guidance despite these headwinds, indicating confidence in underlying demand, but the market priced the margin compression as a structural concern rather than a one-time integration cost.

Investors weighing the stock need to separate temporary timing issues (Middle East delays reversing in Q2) from longer-term margin pressure (Armis integration playing out across 2026). The distinction matters for modelling whether profitability reaccelerates in 2027 or whether the acquisition permanently compresses ServiceNow’s margin profile.

The 17% single-day drop positions ServiceNow as a data point in the broader software sector repricing around AI disruption concerns. Even after the selloff, shares traded at approximately 50 times earnings, an elevated multiple relative to decelerating cRPO growth. The valuation left no room for imperfection.

Enterprise software has faced mounting scrutiny over whether AI-powered automation will cannibalise seat-based pricing models faster than companies can transition to consumption-based revenue. ServiceNow’s results offered evidence for both sides. The 50% non-seat pricing milestone suggests the transition is progressing. The 19.5% Q2 cRPO guidance suggests growth is slowing anyway.

The disconnect between AI capital commitment and realised returns extends beyond software vendors to their enterprise customers, where a KPMG survey found 75% of large-company CEOs believe generative AI has been overhyped, yet nearly 80% still plan to allocate at least 5% of capital budgets to AI initiatives in 2026.

Bull case summary:

Bear case summary:

The ServiceNow reaction is not isolated. Markets are demanding faster proof that AI monetisation can replace or augment seat-based revenue before sustaining premium valuations. Peers reporting in coming weeks will face the same test: beat-and-raise quarters may not suffice if forward guidance signals any deceleration at rich multiples.

ServiceNow delivered operationally, topping Q1 guidance on subscription revenue and raising full-year outlook despite margin headwinds from the Armis acquisition. The market punished the stock anyway, repricing shares on decelerating Q2 cRPO growth guidance at a valuation that demanded acceleration. Three threads define the quarter: cRPO slowing from 21% to 19.5%, AI pricing reaching 50% of new business, and Armis integration compressing margins by 200 basis points on free cash flow.

The forward-looking question is whether the AI pricing shift can sustain growth rates as seat-based expansion cools. Investors tracking enterprise software should monitor Q2 results for confirmation of whether the Middle East deals closed as expected and whether the Armis integration stays on timeline. The answers will determine whether this selloff marks a valuation reset or the start of a longer derating cycle for premium software multiples.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

ServiceNow reported Q1 subscription revenue of $3.67 billion, a 22% year-on-year increase that exceeded the upper end of its own guidance range, with total revenue of $3.77 billion and current remaining performance obligations of $12.64 billion growing 22.5%.

Despite beating Q1 guidance, ServiceNow shares fell roughly 17.58% because management guided Q2 cRPO growth of only 19.5% on a constant-currency basis, down from 21% in Q1, signalling a slowdown in pipeline momentum that investors could not accept at a valuation of approximately 50 times earnings.

Current remaining performance obligations (cRPO) represent contracted revenue a company expects to recognise within the next 12 months, making it a forward-looking indicator of subscription revenue trends; a deceleration in cRPO growth signals that new contract signings are slowing even if current quarterly revenue remains strong.

The Armis acquisition is expected to drag on ServiceNow's subscription gross margin by 25 basis points, operating margin by 75 basis points, and free cash flow margin by 200 basis points, introducing a reset year where profitability improvement stalls across 2026.

ServiceNow has shifted toward non-seat-based pricing tied to consumption, including tokens, infrastructure, hardware, and connectors; CEO Bill McDermott confirmed that 50% of net new business now comes through these models, marking a significant milestone in the company's AI pricing transition.