How AI Expands Software Markets While Killing SaaS Business Models

Key Takeaways

- Global AI-related investment reached $2.53 trillion in 2026, yet 72% of CIOs report barely breaking even, highlighting a significant gap between capital commitment and realised returns.

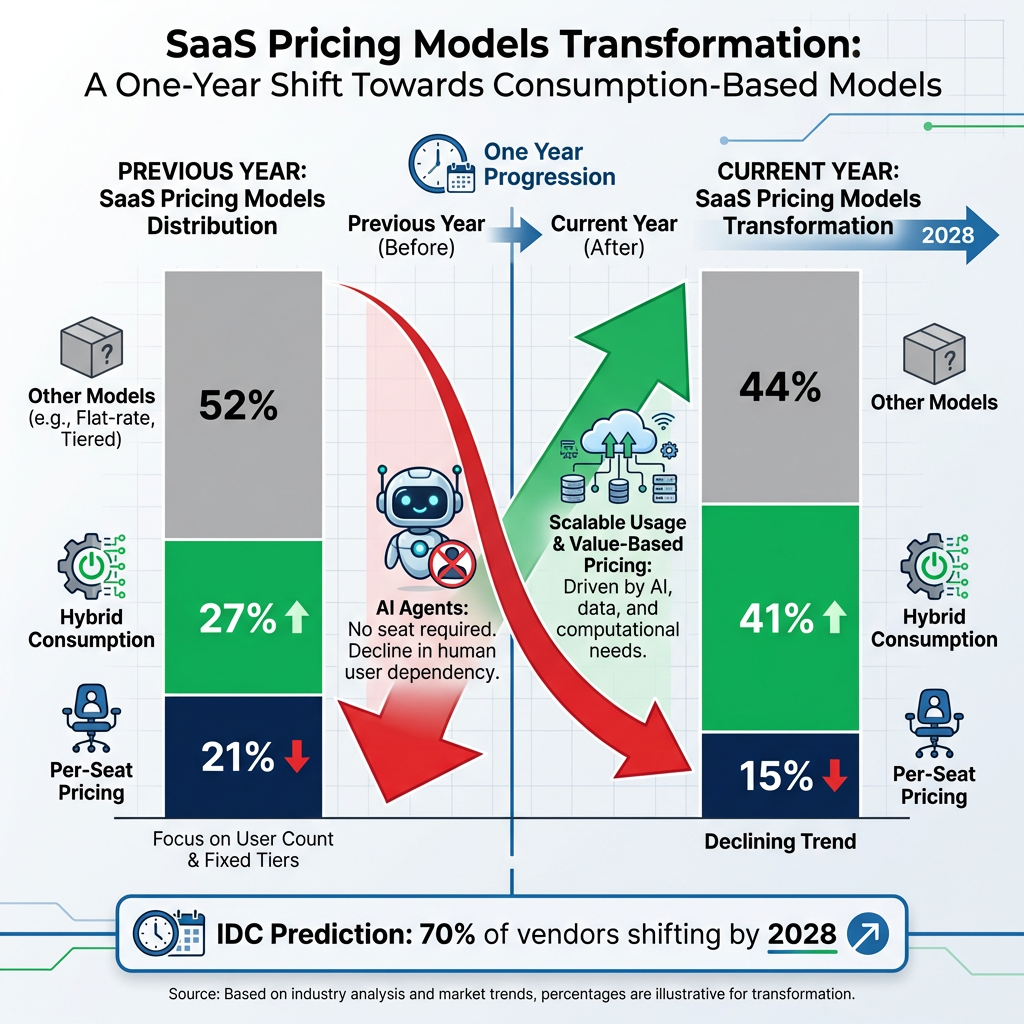

- Per-seat SaaS pricing is collapsing, dropping from 21% to 15% usage in one year, with IDC predicting the model will be obsolete by 2028 as 70% of vendors shift to consumption or outcome-based structures.

- Cloud infrastructure providers (IaaS and PaaS) are the clearest AI beneficiaries, supported by $562 billion in Big Tech capital expenditure and a projected 119% CAGR in agentic AI adoption driving sustained compute demand.

- Agentic AI is set to be embedded in 40% of enterprise applications by 2026, compressing junior developer demand by 40% and accelerating workforce composition shifts across technology organisations.

- The 2026-2028 window represents the critical transformation period, with winners defined by infrastructure positioning and pricing model agility, while vendors clinging to per-seat models and point solutions face the greatest displacement risk.

The software industry faces a paradox in 2026. $2.53 trillion flows into artificial intelligence investments whilst 72% of chief information officers report barely breaking even on those deployments. This tension defines a pivotal moment where assumptions about AI’s impact meet market reality.

Bernstein’s April 2026 research thesis argues AI expands rather than threatens the software market. Wall Street voices contrasting concerns about business model viability and revenue cannibalization. The evidence supports both perspectives, depending on which software segment receives examination.

This analysis examines investment flows, business model disruption, infrastructure dynamics, workforce transformation, and strategic implications. Readers gain clarity on a debate often reduced to oversimplified narratives of either universal benefit or existential threat.

The Investment Surge: Where $2.53 Trillion Is Actually Going

Global IT spending is projected to exceed $6.15 trillion in 2026, representing 10.8% year-over-year growth. Within this total, $2.53 trillion relates specifically to AI initiatives. These figures represent capital commitment, not yet demonstrated returns on investment.

The disconnect between capital commitment and realized value reflects broader institutional investor skepticism about AI investment returns, particularly as foundation model costs compound whilst enterprise adoption timelines extend beyond initial projections.

The five largest technology companies plan $562 billion in AI capital expenditure for 2026. Venture funding reached a record $300 billion globally in Q1 2026, with 80% ($242 billion) directed to AI companies. Merger and acquisition activity totalled $1.22 trillion in Q1 2026, the busiest first quarter since 2021, including 60 deals exceeding $10 billion each.

| Investment Category | 2026 Figure | Key Implication |

|---|---|---|

| Big Tech AI Capex | $562B | Infrastructure buildout prioritised over applications |

| Q1 VC Funding (AI-focused) | $242B (80% of total) | Capital concentrated in foundation models and tools |

| Q1 M&A Activity | $1.22T (60 deals >$10B) | Consolidation wave as major players acquire capabilities |

| Foundation Model Valuations | OpenAI $500B, Anthropic $380B | Market pricing in dominant platform potential |

The $562 billion Big Tech capital expenditure signals where investment priorities lie. Infrastructure components such as GPUs, data centres, and compute clusters receive funding ahead of application-layer development. This allocation pattern supports Bernstein’s thesis that Infrastructure as a Service (IaaS) and Platform as a Service (PaaS) benefit most directly from AI growth.

The merger and acquisition consolidation wave totalling $1.22 trillion in Q1 with 60 mega-deals suggests larger players are absorbing AI capabilities rather than building them organically. This concentration dynamic reshapes competitive landscapes across software segments.

When big ASX news breaks, our subscribers know first

How AI Reshapes Software Economics: A Framework for Analysis

Traditional software operates across a value chain: infrastructure (IaaS) provides computing resources, platform services (PaaS) offer development tools, applications (SaaS) deliver end-user functionality. AI disrupts each layer through different mechanisms.

Per-seat SaaS pricing faces structural challenges because the model historically charged per user on the assumption that humans represented the productivity bottleneck. AI agents can perform tasks without requiring user seats, undermining this pricing logic. Usage of per-seat models dropped from 21% to 15% in one year whilst hybrid consumption models rose from 27% to 41% over the same period.

Agentic AI refers to autonomous software agents that pursue goals without continuous human oversight. This category is projected to grow at 119% CAGR. Gartner forecasts 40% of enterprise applications will incorporate AI agents in 2026. These agents require compute resources, storage, and platform services, creating infrastructure demand even as they automate application-layer tasks.

AI creates both expansion effects (new categories of value, increased total addressable market) and cannibalization effects (automation of tasks previously requiring human-operated software). The remainder of this analysis examines evidence for both dynamics across different software segments.

The SaaS Pricing Collapse: Why Per-Seat Models Are Dying

Per-seat pricing usage declined from 21% to 15% in one year. Hybrid consumption models increased from 27% to 41% over the same period. This represents rapid structural shift rather than gradual evolution.

IDC predicts per-seat pricing will be obsolete by 2028, with 70% of vendors shifting to consumption or outcome-based models.

AI agents perform work without requiring user seats. Automation reduces human headcount. Enterprises increasingly resist paying per-seat for software operated partially or fully by AI. These factors drive the collapse. The 40% drop in junior developer demand in AI-heavy deployment environments illustrates workforce compression that undermines seat-based revenue models.

Market signals indicate SaaS stress:

- SaaS companies trade at a discount to the S&P 500 in 2026

- 35% of point SaaS solutions face potential replacement by 2030

- Hybrid consumption models now represent the dominant pricing approach at 41%

- Cursor, an AI-native coding tool, reached $500 million ARR and $9.9 billion valuation, demonstrating market traction for alternatives

Software vendors dependent on seat-based revenue face existential repricing challenges. Those offering consumption or outcome-based models may capture value as the transition accelerates. This dynamic explains why SaaS trades at a discount despite broader technology sector strength.

The market’s response to AI-driven business model uncertainty has produced software sector valuation compression despite limited disruption evidence in Q1 2026 revenue reports, creating a disconnect between stock performance and operational fundamentals that persists across multiple earnings cycles.

Cloud Infrastructure’s Divergent Fortune: Why IaaS and PaaS Thrive

Bernstein’s April 2026 thesis positions IaaS and PaaS as primary AI beneficiaries. AI training and inference require massive compute resources. This infrastructure demand persists regardless of application-layer disruption.

The $562 billion Big Tech AI capital expenditure flows largely to infrastructure buildout. Hyperscale cloud providers (AWS, Azure, Google Cloud) capture enterprise spending as organisations require GPU and ASIC clusters for AI workloads. Bernstein projects strong infrastructure growth through 2030 based on this structural demand pattern.

As 40% of enterprise applications incorporate AI agents, each agent requires compute, storage, and platform services. The 119% CAGR in agentic AI translates directly to cloud consumption growth. Foundation model training alone demands unprecedented infrastructure scale, creating sustained revenue opportunities for cloud providers.

| Segment | AI-Era Trajectory |

|---|---|

| Traditional SaaS | Pricing model collapse, automation of core functionality, market share loss to AI-native tools, trades at discount to broader market |

| Cloud Infrastructure (IaaS/PaaS) | Compute demand surge, consumption-based pricing alignment, AI workload growth, sustained capital expenditure signals |

Specific revenue growth figures for Azure AI, AWS Bedrock, and Google Cloud Vertex AI from Q1-Q2 2026 earnings calls are unavailable. However, the capital expenditure signals and structural dynamics support Bernstein’s infrastructure-positive thesis. Bernstein specifically identifies database consumption increases and on-premise-to-cloud migration as opportunity areas within the infrastructure segment.

The next major ASX story will hit our subscribers first

The Productivity Paradox: 50% Faster Development, Questionable Quality

92% of US developers have adopted AI coding tools by early 2026. 84% either use or plan to use these assistants. GitHub Copilot reports 20 million users globally, deployed across 90% of Fortune 100 companies. AI-assisted coding represents standard practice rather than experimental adoption.

| Metric | Finding | Source |

|---|---|---|

| Task Completion Speed | 55% faster | GitHub + Accenture (4,800 developers) |

| Delivery Cycles | 40-50% faster | Industry reports |

| Time-to-Market | 30% reduction | McKinsey |

| Development Costs | Up to 80% lower for early builds | Industry analysis |

| Code Generation | 46% of active files via Copilot | GitHub data |

AI-generated code introduces quality challenges described as “slop” requiring debugging. Developer productivity research distinguishes between “Shippers” (task-focused engineers who gain most from AI but add technical debt) and “Builders” (architecture experts burdened with cleaning up AI-generated code). 70% of routine coding is expected to automate, shifting workforce composition.

Workforce implications include:

- Junior developer demand dropped 40% in AI-heavy deployment environments

- Shift toward senior engineers managing AI tools and performing code cleanup

- 30% of engineers hitting usage limits on AI tools, creating cost friction

- McKinsey estimates 57% of US work hours are now automatable with current capabilities

Productivity gains are measurable but create offsetting costs. Technical debt accumulates. Senior engineer time diverts to debugging AI output. Usage fees rise as adoption scales. The 72% of CIOs barely breaking even on AI investments reflects this dynamic. AI accelerates individual tasks whilst introducing hidden costs that erode organizational return on investment.

Strategic Implications: Navigating the AI-Software Transition

Bernstein’s investment guidance focuses on firms bridging conventional software with AI-compute demands. The competitive environment shifts but underlying infrastructure demand remains strong through 2030. Companies referenced in Bernstein’s analysis context include Microsoft, Oracle, Alphabet, Amazon, and Salesforce.

Understanding the broader technology sector momentum drivers helps contextualize why infrastructure plays outperform even as application-layer software faces pricing model uncertainty, particularly as macroeconomic conditions and sector rotation dynamics influence which technology sub-segments capture capital flows.

For software vendors:

- Accelerate pricing model transitions to consumption or outcome-based structures before the 2028 deadline when 70% of vendors will have shifted

- Identify AI-enhanced value propositions beyond simple automation of existing functionality

- Evaluate acquisition targets or partnership opportunities given the merger and acquisition wave totalling $1.22 trillion in Q1

- Position as infrastructure-adjacent rather than pure application plays where architecturally feasible

For enterprise buyers:

- Reassess AI return on investment beyond productivity metrics to include technical debt and senior engineer cleanup time

- Plan workforce composition shifts accounting for 40% junior role compression

- Evaluate cloud consumption patterns as agentic AI scales across 40% of enterprise applications

- Audit SaaS portfolios for point solutions vulnerable to AI replacement (35% at risk by 2030)

For investors:

- Distinguish infrastructure plays from application plays as they face different structural dynamics

- Monitor SaaS pricing transition progress as a competitive signal of vendor adaptability

- Track agentic AI adoption (119% CAGR) as a leading indicator for cloud consumption growth

- Note Gartner’s prediction that 100% of IT work involves AI by 2030 (75% augmented, 25% autonomous)

The $2.53 trillion investment alongside 72% of CIOs barely breaking even reflects the bifurcation thesis. Infrastructure captures value whilst traditional SaaS models undergo forced restructuring. Neither pure optimism nor pessimism accurately characterizes this market.

Bernstein’s expansion thesis holds with qualification. AI expands the total addressable market but redistributes value within it. Winners emerge through infrastructure positioning, pricing model agility, and AI-native architectures. Losers cling to per-seat models and offer point solutions vulnerable to automation.

The 2026-2028 period represents the transformation window. By 2028, pricing models will have shifted as 70% of vendors move to consumption-based structures. Agentic AI will reach mainstream enterprise adoption. The software industry’s structure will look fundamentally different. The question is not whether AI helps or hurts software but which software segments and which business models adapt successfully.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What is the AI impact on software business models in 2026?

AI is forcing a structural shift away from per-seat SaaS pricing, which dropped from 21% to 15% usage in one year, toward consumption and outcome-based models, while cloud infrastructure providers benefit from surging compute demand tied to AI workloads.

Why are SaaS companies trading at a discount despite the AI boom?

SaaS companies face a pricing model collapse as AI agents perform work without requiring user seats, with 35% of point SaaS solutions at risk of replacement by 2030, creating valuation pressure even as broader technology stocks remain strong.

Which software segments benefit most from AI investment growth?

Cloud infrastructure providers (IaaS and PaaS) are the primary beneficiaries, capturing the $562 billion in Big Tech AI capital expenditure directed at GPUs, data centres, and compute clusters required for AI training and inference workloads.

How should investors distinguish between AI winners and losers in the software sector?

Investors should separate infrastructure plays from application-layer software, monitor SaaS vendors transitioning to consumption-based pricing before the 2028 deadline, and track agentic AI adoption (projected at 119% CAGR) as a leading indicator for cloud consumption growth.

What productivity gains does AI actually deliver for software developers?

AI coding tools deliver measurable gains including 55% faster task completion and up to 80% lower development costs for early builds, but 72% of CIOs report barely breaking even on AI investments due to technical debt accumulation and senior engineer time spent debugging AI-generated code.