Why Orion Stock Fell 4.3% Despite 47% Profit Growth in Q1

1 hr ago

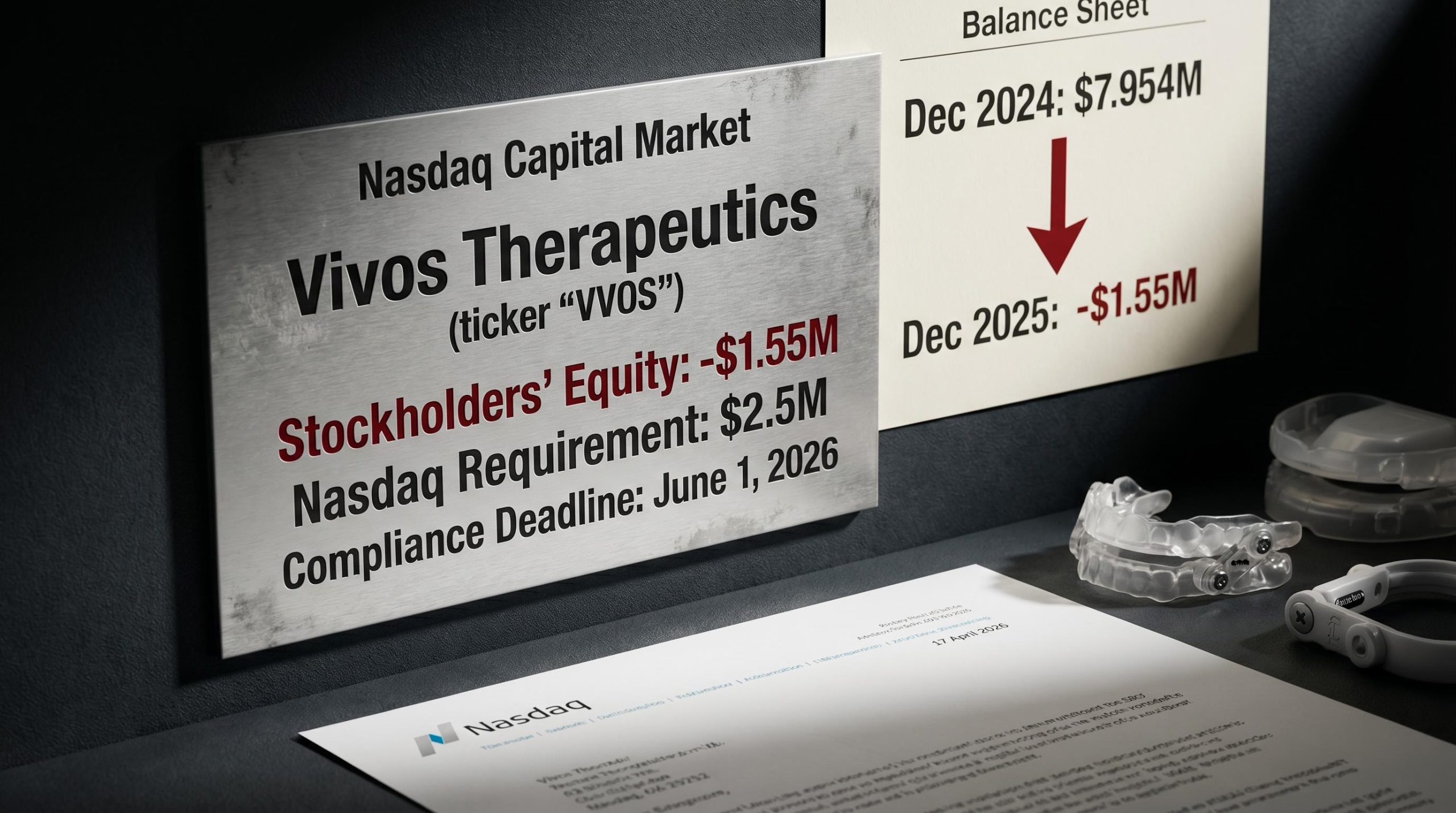

Vivos Therapeutics received a formal deficiency notice from Nasdaq on 17 April 2026, for failing to meet minimum stockholders’ equity requirements, placing its listing on the Capital Market at risk. The medical technology company, which specialises in oral appliance treatments for sleep apnoea, reported negative stockholders’ equity of approximately $1.55 million as of 31 December 2025, falling well short of Nasdaq’s $2.5 million threshold. The notice follows a year in which the company’s strategic transformation consumed capital faster than anticipated.

This article explains what the deficiency means, how Vivos reached this point, what the company must do to maintain its listing, and what investors should watch as the 1 June compliance deadline approaches.

The company’s negative stockholders’ equity of $1.55 million as of 31 December 2025 fell short of Nasdaq Listing Rule 5550(b)(1)’s requirement of at least $2.5 million. The notice, disclosed publicly on 22 April, does not immediately affect the listing status of VVOS common stock, which continues to trade on Nasdaq.

The SEC Form 8-K Item 3.01 disclosure requirements for listing deficiencies mandate that companies publicly report receipt of exchange deficiency notices within four business days, ensuring investors have timely access to material information about threats to a company’s exchange listing status.

Equity Shortfall Negative stockholders’ equity of approximately $1.55 million as of 31 December 2025, falling short of Nasdaq’s $2.5 million minimum requirement.

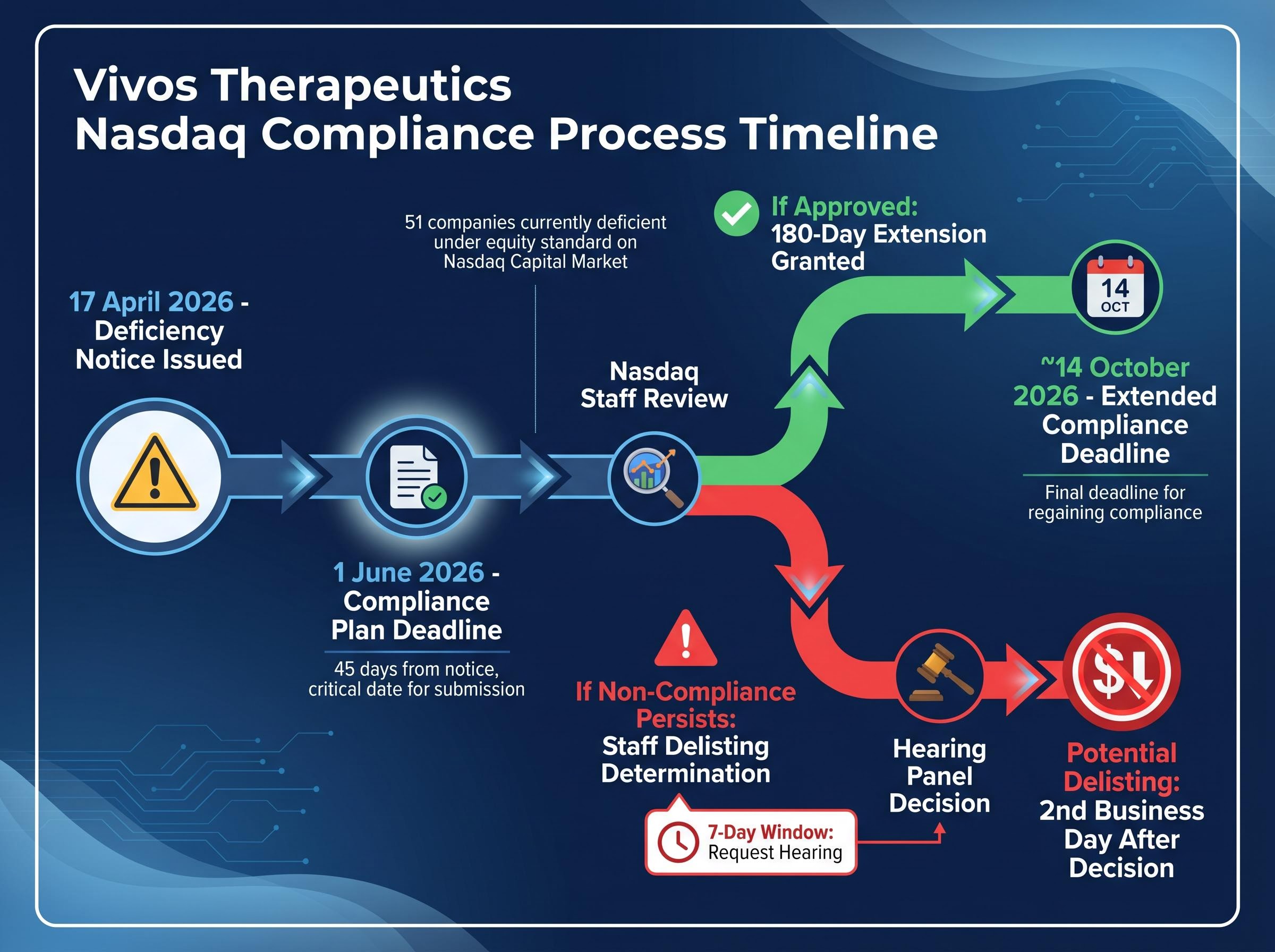

Vivos has until 1 June 2026 to submit a detailed compliance plan demonstrating a credible pathway back to positive equity and sustained compliance. If Nasdaq’s Listing Qualifications Staff accepts the plan, the company may receive an extension of up to 180 calendar days from the notice date, extending the compliance deadline through approximately 14 October 2026.

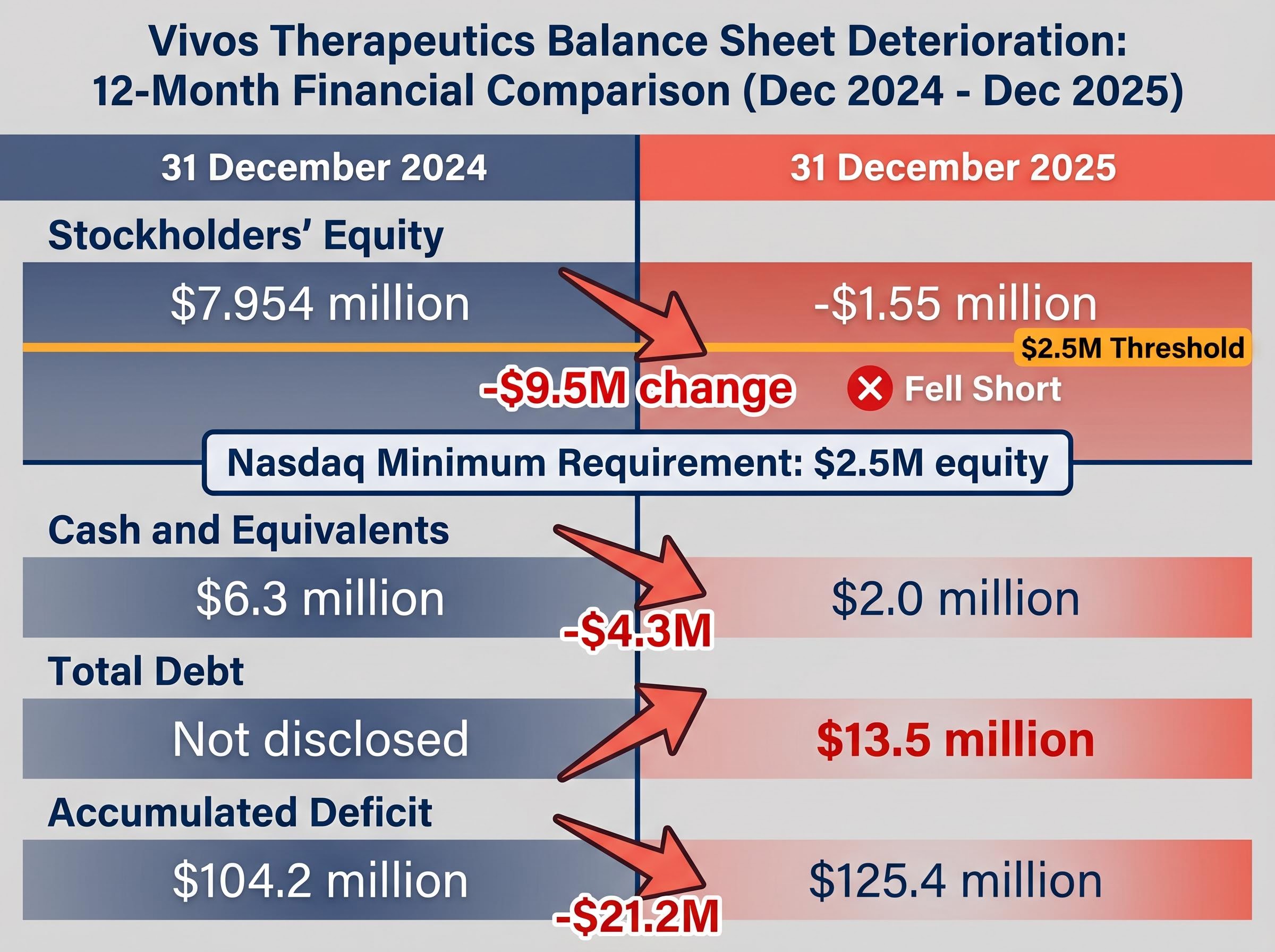

Vivos reported full-year 2025 revenue of $17.4 million, representing 16% year-on-year growth from $15.0 million in 2024. The growth came primarily from sleep testing services and obstructive sleep apnoea (OSA) treatments following the June 2025 acquisition of The Sleep Center of Nevada (SCN) assets. Gross profit reached $10.5 million, a 17% increase, maintaining approximately 60% gross margin.

The revenue growth, however, came at severe cost. Operating expenses surged 50% to $30.4 million from $20.2 million in 2024, driven substantially by integration and management costs associated with operating SCN and related treatment centres. The company posted a $21.2 million net loss and operating loss of $19.9 million, compared to $11.2 million in operating losses the prior year.

The speed of deterioration is visible in the balance sheet collapse. Stockholders’ equity swung from positive $7.954 million at 31 December 2024 to negative $1.55 million twelve months later, a $9.5 million deterioration. Cash and cash equivalents fell to $2.0 million from $6.3 million. Total debt reached $13.5 million, with $8.4 million classified as current. The accumulated deficit climbed to $125.4 million from $104.2 million.

| Metric | 31 December 2024 | 31 December 2025 |

|---|---|---|

| Stockholders’ Equity | **$7.954 million** | **-$1.55 million** |

| Cash and Equivalents | **$6.3 million** | **$2.0 million** |

| Total Debt | Data not provided | **$13.5 million** |

| Accumulated Deficit | **$104.2 million** | **$125.4 million** |

The strategic bet on healthcare service acquisitions overwhelmed the company’s capital capacity. The June 2025 SCN acquisition created $8.6 million in goodwill on the balance sheet but generated only modest incremental earnings while demanding substantial upfront integration investment. The company remained in what management characterised as a pre-revenue stabilisation phase relative to SCN integration as of year-end 2025.

For investors exploring how medical device and imaging companies monetise healthcare service relationships with pharmaceutical clients, our full explainer on pharma partnership revenue models for medical imaging companies examines contract structures, milestone-based payment terms, and the typical revenue ramp timelines that shape cashflow projections in early-stage commercial partnerships.

Nasdaq Listing Rule 5550(b)(1) requires companies on the Capital Market to maintain at least $2.5 million in stockholders’ equity. Alternative compliance criteria include net income from continuing operations or market value of listed securities meeting specified thresholds. Vivos failed to meet the equity standard and apparently failed alternative standards as well.

The Nasdaq Listing Rule 5810 deficiency notification procedures require companies failing continued listing standards to submit a compliance plan within 45 days and establish the framework under which Nasdaq may grant extensions of up to 180 days for companies demonstrating a credible path to regain compliance.

The compliance timeline follows a defined sequence:

As of available regulatory analysis, 51 companies listed on the Nasdaq Capital Market were deficient under the equity standard. Stockholders’ equity deficiencies, whilst serious, are not extraordinarily rare. However, many companies receiving notices ultimately fail to cure deficiencies and are delisted.

Vivos raised $6.8 million in gross proceeds during the first quarter of 2026, comprising $4.6 million from warrant exercise inducement and $2.25 million from a 31 March private placement with V-Co Investors 3 LLC, an affiliate of New Seneca Partners Inc.

The 31 March transaction included:

Total warrant coverage reached approximately 4 million shares, compared to roughly 9.3 million outstanding shares at 31 December 2025. The warrants include anti-dilution protections and 19.99% beneficial ownership cap. Registration rights require filing a resale registration statement within 45 days, maintained for up to three years.

New Seneca Partners’ total investments in Vivos reached $13.4 million since 2024. The 31 March transaction pricing of $1.34 per share reflected the market’s assessment of Vivos’ distressed valuation. The capital raises demonstrate the company’s ability to access funding but at terms that substantially dilute existing shareholders, with warrant overhang creating potential for further dilution if exercised.

For readers wanting to understand the mechanics and pricing dynamics of dilutive capital raises in the healthcare sector, our dedicated guide to how institutional placements get structured in distressed healthcare capital raises examines term sheet negotiation, warrant coverage ratios, anti-dilution protections, and the pricing discounts typically demanded by investors in sub-investment-grade biotech offerings.

H.C. Wainwright & Co. maintained its Buy rating on 17 April 2026 despite slashing the price target to $2.50 from $7.00, a 64% reduction. The firm’s analysis incorporated full-year 2025 earnings results showing revenue of $17.4 million exceeded Wainwright’s projection of $15.3 million, whilst the net loss of $21.2 million exceeded the estimated loss of $18.6 million.

H.C. Wainwright Assessment Price target slashed 64% from $7.00 to $2.50, with debt of $13.5 million exceeding market capitalisation of $11.5 million.

Wainwright highlighted the company is “quickly burning through cash” and noted the significant debt burden of $13.5 million against market capitalisation of just $11.5 million, a debt-to-market-cap ratio of 117%. The maintained Buy rating despite extreme price target reduction suggests Wainwright sees potential value in restructuring or strategic transaction, viewing Vivos through a distressed restructuring lens rather than conventional equity valuation.

Broader analyst consensus showed a “Hold” rating based on three analyst ratings: one sell recommendation, one hold recommendation, and one buy recommendation. Price targets ranged from $2.25 (low) to $6.50 (high), with consensus at $4.92. The wide dispersion reflects fundamental disagreement about the company’s future viability, with the low estimate implying continued deterioration and potential bankruptcy whilst the high estimate assumes successful turnaround or merger transaction.

The stock closed at $0.97 on 17 April 2026, a 10.63% decline, recovering to $1.01 on 20 April (3.69% increase, volume 181,157 shares). Proximity to the $1.00 minimum bid price threshold creates dual compliance risk. If the stock remains below $1.00 for 30 consecutive business days, a separate deficiency notice would be issued, compounding the company’s regulatory challenges.

Vivos faces several potential pathways to restore positive stockholders’ equity and regain Nasdaq compliance. Each option carries distinct execution challenges and timeline constraints.

Strategic options available:

Management stated on the 15 April 2026 earnings call that the company targets breakeven operating cash flow by the end of 2026, focusing on optimising operations in Las Vegas and Detroit, onboarding large new practice relationships, and closely managing expenses. The company acknowledged “no assurance that its plan will be accepted or that it will achieve compliance through additional capital raises or enhanced performance.”

The critical dates shaping the outcome are 1 June 2026 (compliance plan submission deadline) and 14 October 2026 (potential extended compliance deadline if plan accepted). The stock’s proximity to the $1.00 minimum bid price threshold creates parallel compliance threat. If the stock remains below $1.00 for 30 consecutive business days, a separate deficiency notice compounds regulatory challenges.

The most probable compliance strategy, based on available evidence, involves additional equity capital raising with new or existing investors (particularly New Seneca Partners), aggressive operational cost reductions and efficiency improvements, and potential asset sales or strategic transactions to supplement capital position. The compliance plan projections must show a path to operational breakeven through cost reductions, capital raises sufficient to provide equity cushion for compliance, and funding for operations through completion of business optimisation initiatives.

Vivos Therapeutics faces a critical test of survival over the coming months. The company’s strategic transformation generated revenue growth but consumed capital at an unsustainable rate, leaving it with negative stockholders’ equity and a concrete Nasdaq deadline. The $6.8 million raised in Q1 2026 provides short-term liquidity but at the cost of substantial dilution, and further capital raises appear likely if the company is to restore compliance.

The outcome will depend on whether Vivos can execute cost reductions, raise additional capital at acceptable terms, or secure a strategic transaction within the compressed timeline. Investors should monitor the 1 June compliance plan submission and Nasdaq’s response, the company’s cash position and burn rate through quarterly disclosures, and whether the stock remains above the $1.00 minimum bid price threshold. The path forward likely requires a combination of all three strategic options to satisfy both immediate compliance requirements and longer-term operational sustainability.

A Nasdaq stockholders equity deficiency notice is an official warning that a listed company has fallen below the exchange's minimum $2.5 million equity requirement. For Vivos Therapeutics, it means the company must submit a compliance plan by 1 June 2026 or risk delisting from the Nasdaq Capital Market.

Yes, VVOS common stock continues to trade normally on Nasdaq following the deficiency notice disclosed on 22 April 2026, as the notice does not immediately affect listing status while the company pursues a compliance plan.

Vivos recorded negative stockholders equity of approximately $1.55 million as of 31 December 2025 after a $9.5 million deterioration over 12 months, driven by a $21.2 million net loss and operating expenses that surged 50% to $30.4 million following the June 2025 acquisition of Sleep Center of Nevada assets.

Vivos can pursue additional equity capital raises (requiring roughly $6-8 million to provide a realistic cushion), aggressive operational cost reductions targeting a 55-60% cut in operating expenses, a strategic transaction such as a merger or asset sale, or a combination of all three approaches before the 14 October 2026 extended deadline.

If Nasdaq rejects the compliance plan or the company fails to regain compliance, Nasdaq will issue a Staff Delisting Determination letter, after which Vivos has seven calendar days to request a hearing before an independent Nasdaq Hearings Panel, with delisting effective the second business day after an adverse panel decision.