Betashares ERTH ETF: Macro Tailwind Meets Real Volatility Risk

7 hrs ago

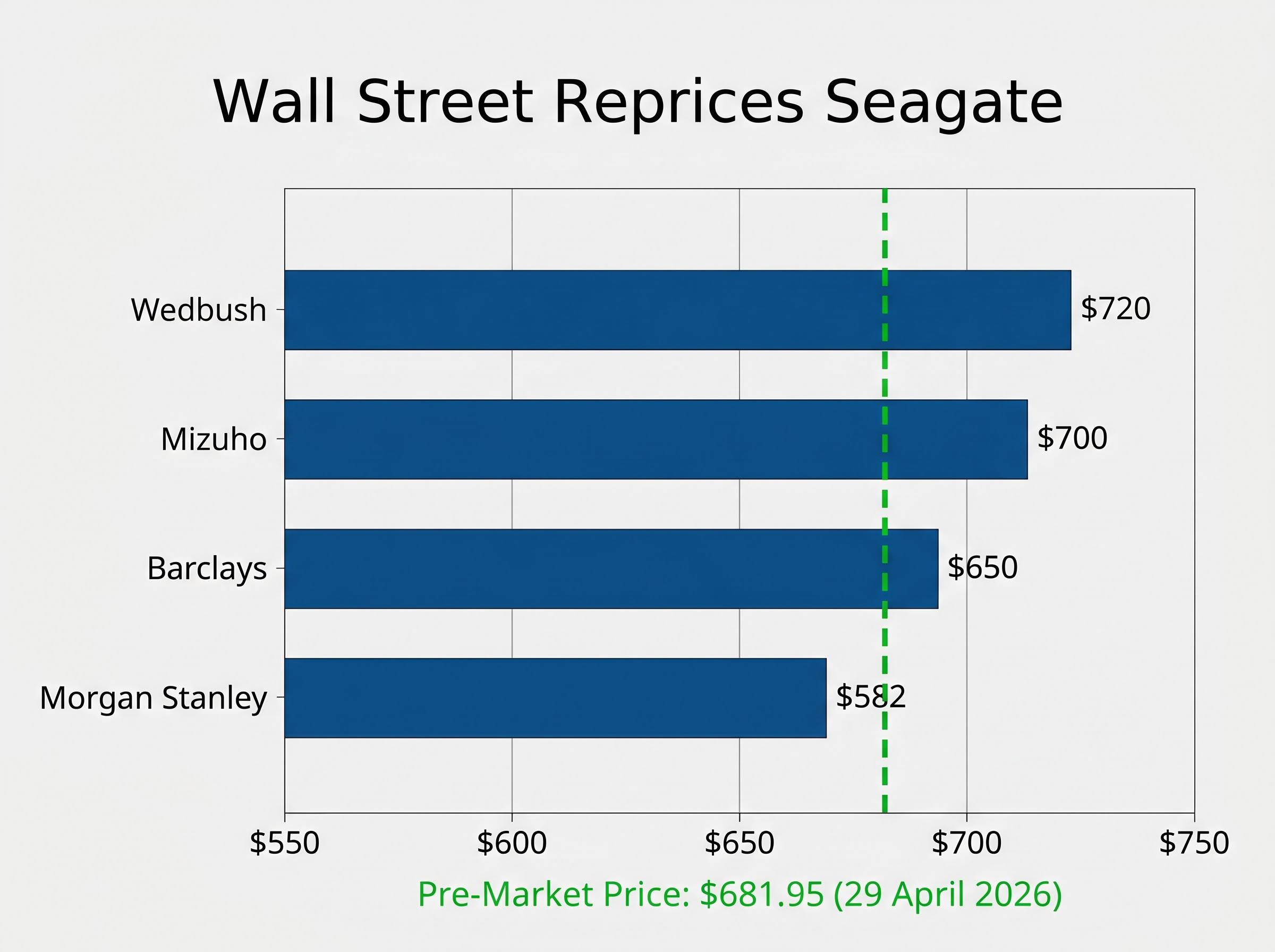

Seagate Technology shares surged 17.77% to reach $681.95 in pre-market trading on 29 April 2026, reacting immediately to a massive third-quarter earnings beat. This upward momentum reflects more than a standard cyclical hardware earnings bump for the legacy manufacturer.

Instead, the market is pricing in a structural shift driven by severe supply constraints across the enterprise storage sector. The dynamics surrounding Seagate stock have fundamentally changed as artificial intelligence data centres aggressively secure hardware capacity.

A detailed breakdown of the March quarter numbers reveals how operational efficiency is translating raw demand into shareholder value. Rapidly escalating Wall Street price targets demonstrate how institutions are adjusting their models to account for this new reality.

Financial institutions responded to the earnings release with aggressive upward revisions, validating the massive pre-market stock movement as a sudden awakening to a new market reality.

Analysts are rapidly adjusting their models to account for the sustained storage demand. Morgan Stanley demonstrated particular bullishness, noting the company as a preferred investment choice within the broader IT hardware sector.

Morgan Stanley’s rapid price target evolution ended at a $582 projection, based on a 2027 profit estimate. Other major firms followed a similar trajectory, with Mizuho upgrading its target to $700 and Wedbush reiterating an Outperform rating with a $720 target. Barclays maintained an Overweight rating and set a $650 price target, citing heavy data centre demand as a primary catalyst.

The firm later expanded this valuation model by elevating its prior bull case to a new base case, a shift largely driven by the competitive advantages of the manufacturer’s proprietary HAMR technology.

| Firm | Previous Target | New Target | Current Rating |

|---|---|---|---|

| Morgan Stanley | $468 | $582 | Top Pick |

| Wedbush | Not Specified | $720 | Outperform |

| Mizuho | Not Specified | $700 | Not Specified |

| Barclays | Not Specified | $650 | Overweight |

These revised targets provide context for the premium valuation assigned to the stock. The company currently trades at a 64.3x trailing twelve-month price-to-earnings ratio.

Investors need to see exactly how high institutions are willing to push their models to determine whether the current stock price still has runway. This multiple reflects elevated growth prospects rather than traditional hardware valuations.

The expanding reliance on large language models requires massive data retention capabilities for training datasets. As artificial intelligence token usage scales exponentially, technology companies are aggressively hoarding traditional storage capacity to secure their infrastructure.

This creates a physical reality where massive data centres require vast physical space and millions of individual drives to function.

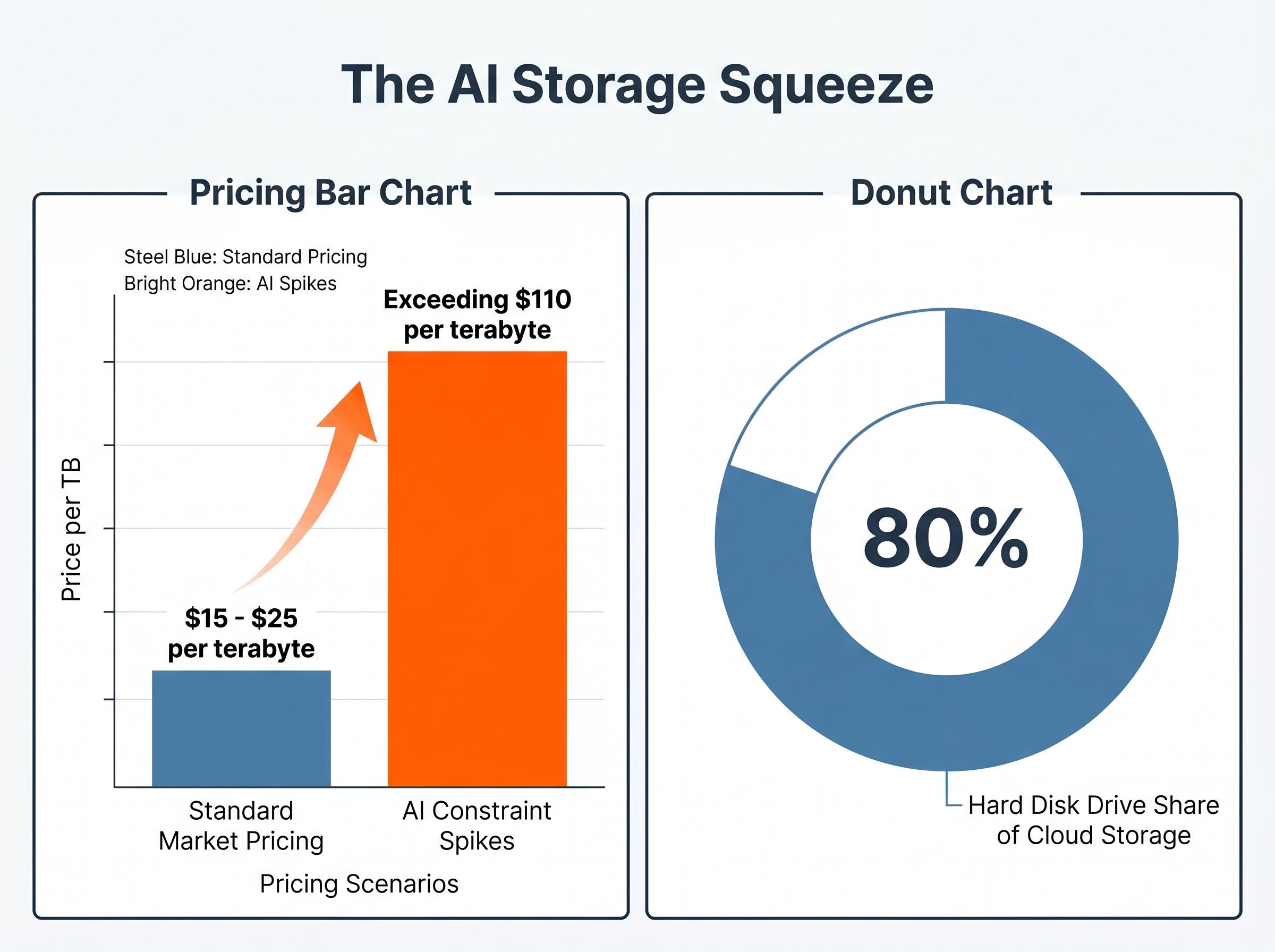

According to industry estimates, despite the development of newer flash memory technologies, traditional hard disk drives continue to secure approximately 80% of overall cloud storage requirements. Hard disk drives offer superior cost efficiency at hyperscale volumes, making them the dominant choice for long-term data retention.

Independent IDC estimates for cloud storage actually place this figure even higher, indicating that nearly 89% of data held by major service providers still resides on legacy drives.

Artificial intelligence data centres are currently absorbing every available unit to guarantee their future training pipelines. Understanding this foundational knowledge allows investors to view the manufacturer as a core artificial intelligence infrastructure play rather than an outdated consumer hardware company.

The transition from consumer computing storage to enterprise hyperscale solutions has altered the industry structure entirely. A few major suppliers now dictate market availability, allowing manufacturers to strictly control production and inventory.

This supplier concentration creates a bottleneck that benefits the primary manufacturers. The physical constraints of data centre scaling translate directly into sustained hardware demand.

The market enthusiasm is grounded in the concrete financial performance of the March quarter, where gross margin expansion serves as clear proof of the structural shift. Extreme operational efficiency allowed the company to capitalise on the sudden surge in hardware demand.

The core financial beats highlight this performance:

Revenue: $3.11 billion, representing a 44% year-over-year increase. Earnings: Non-GAAP diluted EPS of $4.10, beating the $3.50 consensus estimate for a 17.1% positive surprise. * Cash Flow: $953 million in free cash flow, supported by a GAAP gross margin of 46.5%.

The official Q3 2026 earnings release underscores how these robust cash generation metrics provide the company with ample flexibility to fund future capacity scaling without relying on expensive debt markets.

By unpacking these cash flow metrics and profit margins, readers can see the company is effectively translating raw demand into actual shareholder value. This is not simply top-line revenue inflation, but a fundamental improvement in unit economics.

Chief Executive Officer Dave Mosley confirmed that the company is leaning heavily into an areal density-driven strategy to maximise this efficiency.

“Seagate delivered outstanding March quarter results, exceeding the high end of our revenue and EPS guidance, achieving record margin performance, and generating close to $1 billion in free cash flow. We are entering a new era of structural growth as AI applications amplify data creation and support sustained storage demand.”

Forward guidance remains the primary catalyst for stock movement, and the aggressive June quarter projections significantly outpaced Wall Street modelling. The company expects Q4 2026 adjusted EPS between $4.80 and $5.20, with revenue projected between $3.35 billion and $3.55 billion.

These figures easily surpassed prior Wall Street estimates of $3.89 EPS and $3.1 billion in revenue.

This optimistic guidance stems from a dramatic pricing power shift happening at the unit level. The severe supply and demand imbalance provides the company with unprecedented pricing leverage heading into the summer months.

This structural supply discipline has fundamentally shifted pricing leverage to hardware producers, allowing them to dictate terms during periods of intense demand.

An increase in capacity cost during the first quarter pointed to a longer-term trend that is now materialising fully. Understanding these per-terabyte pricing dynamics helps investors evaluate whether the optimistic Q4 targets are sustainable.

The contrast between historical averages and current market rates highlights the severity of the supply constraint:

Standard Market Pricing: Historically averages $15 to $25 per terabyte for enterprise capacity. AI Constraint Spikes: Current market pricing for highly sought-after high-capacity drives is exceeding $110 per terabyte.

Artificial intelligence infrastructure demands have permanently altered the company’s market position. The pricing leverage and margin expansion demonstrated in the Q3 report represent structural changes, rather than temporary cyclical anomalies.

As long as technology giants continue their aggressive hoarding of physical storage capacity, primary hardware manufacturers will maintain their pricing power.

Investors must monitor enterprise hyperscale storage investments as the ultimate leading indicator for future earnings beats. The physical reality of data centre construction guarantees that software advancements will continually require extensive hardware support.

Investors exploring the broader macroeconomic vulnerabilities surrounding these capital-intensive builds will find our detailed coverage of underpriced stock market risk useful for assessing how geopolitical shocks might impact elevated technology valuations.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

Seagate stock surged by 17.77% in pre-market trading on April 29, 2026, primarily due to a massive third-quarter earnings beat and market recognition of a structural shift in enterprise storage demand driven by AI data centers.

The expanding reliance on large language models requires massive data retention for training, leading AI data centers to aggressively acquire traditional hard disk drive capacity to secure their infrastructure needs.

Seagate reported revenue of $3.11 billion, a 44% year-over-year increase, non-GAAP diluted EPS of $4.10, and $953 million in free cash flow, supported by a GAAP gross margin of 46.5%.

Following the earnings release, firms like Mizuho upgraded its target to $700, Wedbush reiterated an Outperform with a $720 target, and Morgan Stanley set a $582 projection, reflecting sustained storage demand.

Seagate projects Q4 2026 adjusted EPS between $4.80 and $5.20, with revenue between $3.35 billion and $3.55 billion, significantly surpassing prior Wall Street estimates due to strong pricing power.