Australia’s FY2026-27 Investment Outlook: the Easy Years Are Over

1 hr ago

Samsung Electronics just reported the most profitable quarter in its history, and its stock fell more than 6%. That is not a contradiction. It is a lesson in how modern equity markets actually work.

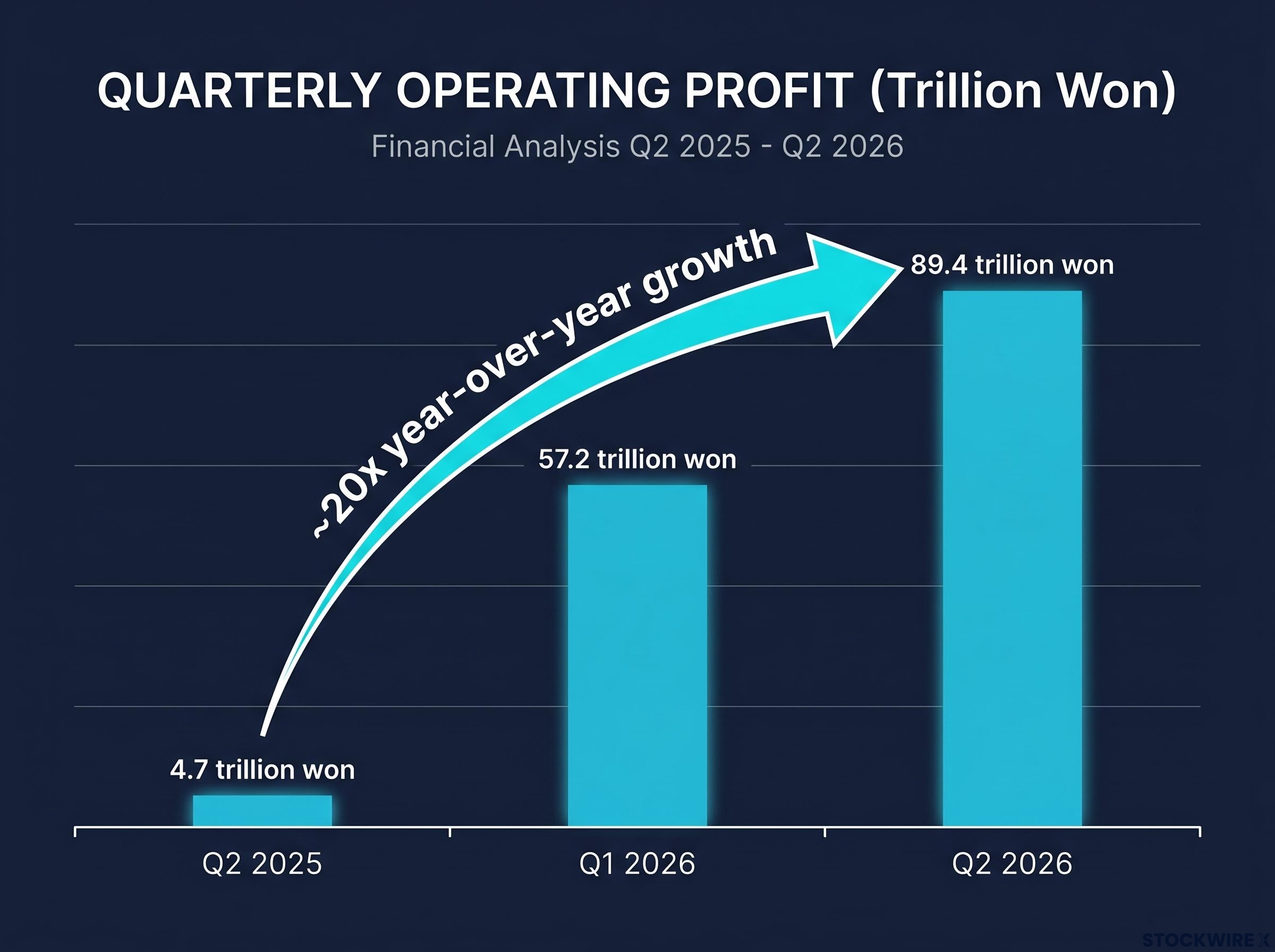

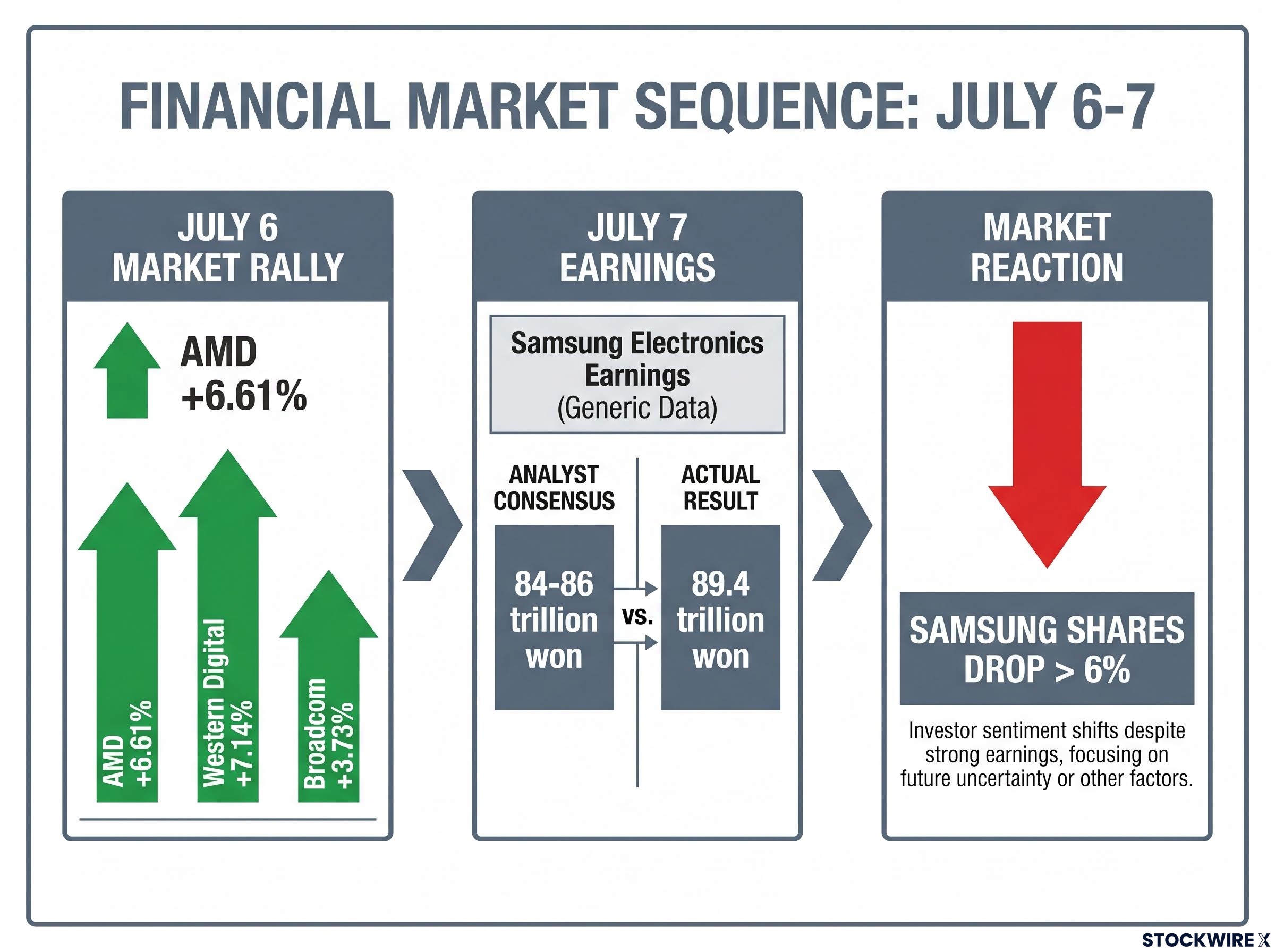

On 7 July 2026, Samsung released preliminary Q2 2026 figures showing operating profit of 89.4 trillion won (approximately $58 billion), a result roughly 20 times larger than the equivalent period a year earlier and one that topped the company’s total earnings for both 2024 and 2025 combined. The numbers arrived against a backdrop of a semiconductor sector that had already been rallying hard: AMD had jumped 6.61% and Western Digital had surged 7.14% in the previous session, with the Dow Jones pushing above 53,000 for the first time ever. The expectation bar for Samsung was already sitting at altitude.

Here is what the data actually tells you about the gap between a record-breaking business and a well-timed investment: what drove the result, why professional investors sold into it, and what the episode reveals about valuing high-growth technology stocks in an AI-driven market.

The scale of Samsung’s Q2 2026 result demands a moment before the analysis begins.

89.4 trillion won (~$58 billion) in a single quarter, nearly 20 times the year-ago result.

In Q2 2025, Samsung reported operating profit of 4.7 trillion won. Twelve months later, that figure had multiplied almost twentyfold. This is not incremental improvement. It is a structural transformation in how much money the company earns.

The trajectory makes the scale clearer:

The quarter’s profit alone outstripped everything Samsung earned across all of 2024 and 2025 put together. It was the company’s third consecutive record quarterly profit. The AI infrastructure buildout is generating hardware demand so acute that it has structurally transformed one of the world’s largest chipmakers in under 24 months.

The headline number comes from one place. Samsung’s Device Solutions (DS) division, which houses its memory chips, system LSI, and foundry operations, contributed 93% of company profit in Q1 2026, and that concentration continued into Q2.

The demand driver is hyperscaler spending on AI training and inference infrastructure. Data centres running large language models and AI workloads require high-bandwidth memory (HBM), the specialised memory chips designed for the massive parallel processing that AI demands, alongside conventional DRAM and NAND storage at scale. Supply has not kept pace with demand. Memory average selling prices (ASPs) are estimated to have risen 40-60% quarter-on-quarter (analyst estimate), and industry analysis suggests supply will remain tight through at least 2027.

Hyperscaler capex from the four largest US cloud operators reached approximately $130 billion in Q1 2026 alone, with full-year 2026 combined guidance sitting at $725 billion and trajectories pointing toward a $1 trillion annual run rate in 2027, a scale of committed spending that underpins the memory demand environment Samsung is benefiting from.

Samsung is betting heavily that this demand persists. The company has committed over 110 trillion won (~$73 billion) to capex and R&D in 2026 alone.

| Metric | Figure | Period |

|---|---|---|

| DS division share of company profit | 93% | Q1 2026, continuing into Q2 |

| Memory ASP growth (QoQ) | 40-60% (analyst estimate) | Q2 2026 |

| 2026 capex and R&D commitment | Over 110 trillion won (~$73B) | Full-year 2026 |

| Memory supply tightness outlook | Tight through at least 2027 | Industry estimate |

When one division generates 93% of a company’s profit on the back of AI infrastructure demand, that concentration is both the source of Samsung’s extraordinary results and the key risk variable investors are pricing.

The analyst consensus before the announcement was already projecting operating profit of approximately 84-86 trillion won, which itself implied an 18x year-over-year gain. The actual result of 89.4 trillion won beat expectations, but not by a margin that shocked anyone tracking the most bullish forecasts.

Markets price future expectations, not past results. When a result is already embedded in the share price, the incremental surprise needed to push shares higher shrinks to almost nothing. Samsung’s quarter was strong. It was not stronger than what professional investors had already positioned for.

The timing compounded the dynamic. On 6 July 2026, semiconductor stocks had already staged a broad rally:

The semiconductor rally context leading into Samsung’s announcement extended well beyond the single session on 6 July: Micron, Sandisk, and SK Hynix had already combined for gains exceeding 250% in the 30 days ending 12 May 2026, with HBM capacity across SK Hynix and Micron reported as sold out through 2026-2027.

The Dow Jones crossed 53,000 for the first time that same session. By the time Samsung’s numbers hit screens the following morning, the optimism had already been pulled forward. S&P 500 futures had retreated by roughly 0.2% and Nasdaq 100 futures by roughly 0.8% on the morning of 7 July, with the broader market already digesting the prior session’s gains.

The 6% decline in Samsung’s Seoul-listed shares is not a verdict on the business. It is a signal that professional investors had already positioned for a strong result and used the confirmation to take profits, a pattern that tells you more about where the stock was priced than where the company is headed.

“Sell the news” is the market phenomenon where a widely anticipated positive event causes a price decline because the expectation was already built into the share price before the event occurred. The good news is real. The stock falls anyway because the good news was already priced in.

“Once the market expects 18x year-over-year growth, that becomes the floor, not the ceiling.”

Once analysts are projecting approximately 84-86 trillion won in quarterly profit, that figure becomes the minimum that sentiment requires to hold steady. Future quarters will be judged against this elevated base, making it structurally harder for Samsung to keep positively surprising. The bar moves up with every record.

There is a forward guidance dimension as well. After a near-vertical profit ramp, investors immediately ask whether memory prices, AI capex, and demand growth can continue at the same rate. Samsung’s commitment of over 110 trillion won in 2026 capex frames the scale of the bet that must be justified by sustained demand. Can memory ASPs keep rising 40-60% quarter-on-quarter (analyst estimate)? The market is already pricing its answer.

Once you understand that share prices encode future expectations rather than past results, a post-earnings decline on good news stops looking irrational. It is a rational re-pricing of what “good” now means as the baseline.

A headline profit of 89.4 trillion won conceals several tensions worth examining:

Spending over 110 trillion won in a single year on semiconductors is a bet that AI demand will sustain its current trajectory. If the cycle extends, the payoff is enormous. If it does not, the downside exposure is equally amplified.

Memory cycles have historically reversed. The current AI-driven upcycle is structurally different from prior cycles in some respects, but capex commitments made at peak pricing have historically created oversupply risk when demand normalises. Memory and AI chips are highly cyclical; current supply shortages are not permanent.

The current memory chip supercycle is structurally unlike prior DRAM upcycles in one critical respect: AI data centre operators now account for an estimated 70% of total memory shipment volumes, a demand concentration that converts what was historically a cyclical commodity market into something closer to a structural supply agreement regime.

The concentration of profit in a single division running on a cyclical commodity means that Samsung’s extraordinary results carry embedded fragility. The same AI demand that created the record quarter is also the single point of failure if spending patterns shift.

Samsung’s chip franchise is objectively strong: record profits, a dominant position in memory, and structural AI tailwinds that show no immediate sign of reversing. That does not automatically mean today’s share price represents a good entry.

The AI demand story is well known and thoroughly embedded in analyst models. Financial industry estimates suggest Samsung’s full-year 2026 operating profit could reach approximately 300 trillion won (~$217 billion) (analyst estimate, not independently confirmed). That is the scale against which the current valuation is being set.

For investors exploring how this dynamic plays out across the broader technology sector, our full explainer on growth stock valuation discounts examines why technology equities were trading at a 21% discount to fair value as recently as March 2026, including the macro conditions that must resolve before that discount closes.

Potential edges lie in understanding the variables the market has not yet resolved:

“Sell the news” is not a verdict that AI is a fad or that Samsung is a flawed business. It is a signal that the market had already priced in the good news, and the next move depends on what comes next, not what just happened. The investors who will navigate this environment well are not the ones who buy on record headlines or sell on price drops; they are the ones who focus their analysis on what is already priced in and what remains unresolved.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced in this article are subject to market conditions and various risk factors.

'Sell the news' is when a widely anticipated positive event triggers a price decline because the expectation was already built into the share price before the announcement. Samsung's Q2 2026 profit of 89.4 trillion won beat consensus forecasts of 84-86 trillion won, but not by enough to surprise investors who had already positioned for the strong result, so they took profits on confirmation.

Samsung's Device Solutions division, which covers memory chips, system LSI, and foundry operations, contributed 93% of company profit, driven by surging demand for high-bandwidth memory and conventional DRAM from AI data centre operators running large language models and AI workloads.

Samsung has committed over 110 trillion won (approximately $73 billion) to capital expenditure and R&D in 2026 alone, a bet that AI-driven demand for memory and semiconductors will sustain its current trajectory through at least 2027.

High-bandwidth memory is a specialised chip architecture designed for the massive parallel processing that AI training and inference require; it commands significantly higher average selling prices than conventional DRAM. With HBM supply sold out through 2026-2027 according to industry reports, Samsung's ability to scale HBM production is the central driver of its profit surge.

Over 90% of Samsung's profit is concentrated in its semiconductor division, meaning any slowdown in AI memory demand would hit the whole company disproportionately; on top of that, the 110 trillion won capex commitment creates significant downside exposure if the AI demand cycle reverses, as memory markets have historically been highly cyclical.