ResMed’s ASX-listed Chess Depositary Interests (CDIs) have fallen 19.8% since the start of 2025, dragging the RMD share price to A$29.01. Yet the stock’s price-to-sales multiple has compressed to 4.30x, barely half its five-year historical average of 8.70x. For Australian investors watching from the sidelines, that gap between a shrinking valuation and a still-growing business raises a question worth examining closely.

The company sits at the intersection of two forces pulling in opposite directions: a structural tailwind from rising global demand for sleep apnea treatment, and a structural uncertainty from GLP-1 weight-loss drugs that could, in theory, shrink the addressable patient pool. The share price has repriced sharply. The business has not stopped growing. What follows is an analysis of whether the current valuation discount represents a genuine opportunity or a rational re-rating, covering ResMed’s business divisions, how to read a price-to-sales ratio in context, and what the real GLP-1 risk looks like on the numbers.

A 19.8% decline and a valuation multiple at half its historical norm

The decline has been sharp and sustained. From the start of 2025 through 26 May 2026, ResMed’s ASX-listed CDIs have shed 19.8%, settling at A$29.01 as of 22 May 2026. Market capitalisation sits at approximately A$42.60 billion.

What makes the move analytically interesting is not the price drop alone. It is the valuation compression happening alongside revenue growth.

ResMed’s current price-to-sales ratio stands at 4.30x, compared to a five-year historical average of 8.70x.

The multiple has not collapsed because revenue deteriorated. Q3 FY2026 revenue came in at US$1.43 billion, up 11% year-over-year. Both the numerator (price) and the denominator (sales) moved, but price moved faster and in the wrong direction. That dual movement compressed the P/S ratio beyond what revenue growth alone can explain, pointing to a genuine shift in how the market is pricing the stock’s future.

Analyst consensus has not followed the share price down. The ASX consensus target sits at AU$43.57, while the NYSE consensus target is US$270.60 with an Outperform rating from 19 analysts, against a recent NYSE close of approximately US$208.05.

| Metric | Current | Five-Year Average |

|---|---|---|

| P/S Ratio | 4.30x | 8.70x |

| ASX Share Price | A$29.01 | — |

| Analyst Consensus Target (ASX) | AU$43.57 | — |

A consensus target alone is not an investment thesis. But a 50% compression in a valuation multiple while the underlying revenue base expands demands an explanation. The rest of this analysis works through the possible ones.

ASX healthcare valuation compression has not been limited to ResMed: Cochlear’s price-to-sales ratio contracted from approximately 9.18x to 2.82x over the same period, a pattern suggesting that interest-rate-driven multiple contraction across the sector created conditions in which individual stock sentiment, such as GLP-1 fears, amplified an already-underway de-rating.

When big ASX news breaks, our subscribers know first

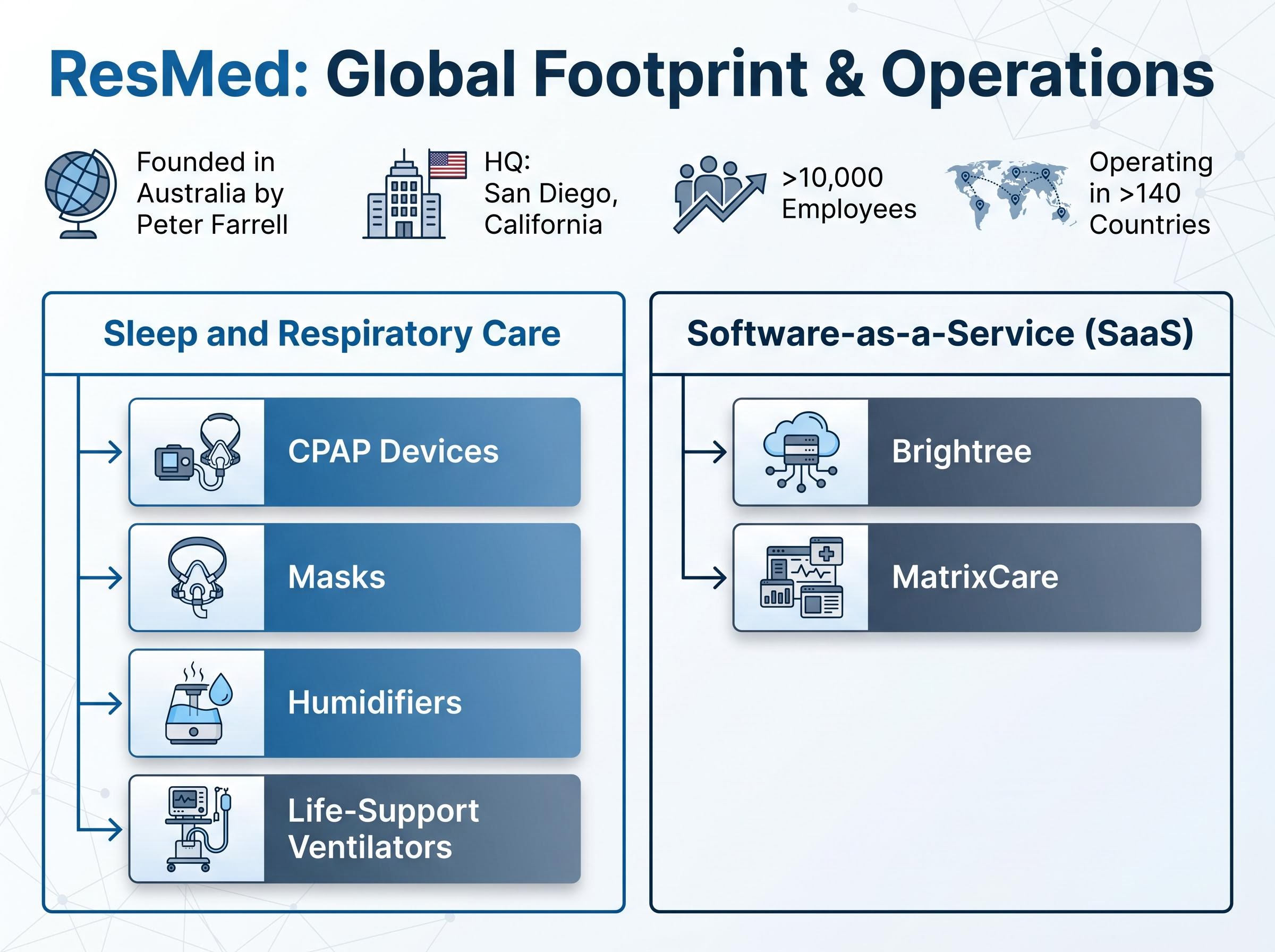

What ResMed actually does, and why its Australian roots still matter

Before the valuation debate makes sense, the business itself needs to be visible. ResMed operates across two distinct divisions, each with a different revenue profile and competitive logic.

- Sleep and Respiratory Care: CPAP devices, masks, humidifiers, and life-support ventilators

- Software-as-a-Service (SaaS): Brightree and MatrixCare platforms serving home medical equipment providers and aged-care operators

Founded in Australia by Peter Farrell, the company is now headquartered in San Diego, California, and employs more than 10,000 people across more than 140 countries. Australian investors access the stock via CDIs on the ASX, while the primary listing sits on the NYSE.

The hardware engine

The Sleep and Respiratory Care division covers the full spectrum of breathing support, from overnight CPAP users managing obstructive sleep apnea to patients dependent on continuous ventilation. Device sales generate significant revenue, but the product cycle also creates a recurring consumables stream through mask replacements and accessories.

The software layer

Brightree serves home medical equipment providers with workflow and billing software. MatrixCare targets aged-care and post-acute care operators. Both platforms embed ResMed into the daily operations of healthcare providers, creating switching costs that a hardware company alone would not generate.

The strategic logic of combining hardware with SaaS-derived data is straightforward: patient outcomes improve when device usage data feeds back into provider workflows, and that improvement reduces broader healthcare system costs. Q3 FY2026 revenue of US$1.43 billion, up 11% year-over-year (8% in constant currency), reflects both engines contributing.

How to read a price-to-sales ratio without being misled by it

A price-to-sales ratio measures how much the market is willing to pay for each dollar of a company’s revenue. The formula is simple: market capitalisation divided by annual revenue. A higher P/S suggests investors are pricing in stronger future growth or margins; a lower one suggests scepticism about one or both.

P/S is most useful as a valuation starting point for companies growing revenue rapidly, companies with variable margins, or businesses at early profitability stages where earnings-based metrics can be unreliable. ResMed fits the first category: revenue is expanding, making the P/S compression from 8.70x to 4.30x analytically meaningful rather than mechanical.

The price-to-sales ratio is most useful as a valuation starting point for growth-oriented businesses where earnings can be volatile or temporarily suppressed by reinvestment spending; comparing a company’s current multiple against its own historical average is typically more informative than comparing it against the broader market.

The compression can happen two ways simultaneously. If the share price falls while revenue rises, the ratio compresses from both ends. That is precisely what has occurred with ResMed over the past 17 months.

A P/S ratio captures market sentiment about future revenue. It does not capture the quality, durability, or margin profile of that revenue.

That limitation matters. A company trading at a low P/S multiple could be a bargain, or it could be correctly priced for deteriorating growth. The metric alone cannot distinguish between the two. Serious valuation work typically layers multiple approaches, including discounted cash flow (DCF) modelling, which projects a company’s future cash generation capacity and discounts it back to present value.

- Calculate the current P/S multiple and note the direction of the trend

- Compare it to the company’s own historical average and sector peers to establish whether the compression is company-specific or sector-wide

- Layer with at least one cash-flow-based metric (such as DCF or free cash flow yield) before drawing investment conclusions

The GLP-1 question: how real is the threat to ResMed’s core market?

The concern is direct. Drugs such as Ozempic and Wegovy reduce obesity. Obesity is a primary driver of obstructive sleep apnea. If GLP-1 drugs succeed at scale, the treatable patient pool for CPAP devices could shrink, undermining ResMed’s long-term revenue base.

The bear case rests on a logical chain:

- GLP-1 adoption is accelerating globally, with millions of patients now on weight-loss therapies

- Obesity reduction could lower the incidence of new sleep apnea diagnoses over time

- A smaller addressable market would compress both revenue growth expectations and the valuation multiple

The counter-arguments, however, narrow the threat considerably:

- Sleep apnea has causes beyond obesity, including anatomical factors, ageing, and genetic predisposition, meaning GLP-1 drugs address only one pathway to the condition

- Global diagnosis rates for sleep apnea remain low relative to estimated prevalence, leaving significant untapped demand even if new obesity-related cases decline

- Existing CPAP users do not disappear from the installed base; the consumables and replacement cycle continues regardless of GLP-1 uptake

Commentary on the Australian investing programme The Call (Ausbiz) framed GLP-1 fears as “potentially overdone,” with panellist Luke describing ResMed’s mid-teens valuation as “quite attractive” and calling the stock a buy for investors who take the view that GLP-1 impact on sleep apnea device demand will be limited.

The observable data supports the counter-arguments so far. Q3 FY2026 revenue of US$1.43 billion grew 11% year-over-year, with non-GAAP diluted earnings per share reaching US$2.86. GLP-1 disruption has not yet materialised in ResMed’s reported numbers. Whether that changes over the medium term remains the open question the market is pricing in.

Reading the numbers that matter before making a decision

The quantitative picture available to Australian investors is specific enough to structure a due diligence process, even if certain data gaps remain.

| Metric | Value | What It Suggests |

|---|---|---|

| Current P/S | 4.30x | Market pricing well below historical norms |

| Five-Year Average P/S | 8.70x | The benchmark for what the market has historically paid |

| Q3 FY2026 Revenue Growth | 11% YoY | Revenue acceleration despite sentiment headwinds |

| GAAP EPS (Q3 FY2026) | US$2.74 | Earnings generation remains intact |

| Analyst Consensus Target (ASX) | AU$43.57 | Material gap between consensus and current price |

What is not yet knowable from current data includes the full-year FY2026 revenue and margin trajectory, segment-level SaaS metrics for Brightree and MatrixCare, and the medium-term impact of GLP-1 adoption on new patient additions.

ResMed’s balance sheet adds another dimension to the valuation picture that the P/S ratio alone cannot capture: a net cash position of US$624 million, a debt-to-equity ratio of just 18.0%, and an accelerated buyback programme during the period of share price weakness, all of which signal management’s internal read on intrinsic value.

One variable specific to Australian investors deserves attention: ResMed earns in US dollars, but ASX CDI holders carry AUD/USD currency exposure. A strengthening Australian dollar would reduce the translated value of US-dollar earnings, adding a layer of risk that NYSE investors do not face.

- Assess the P/S compression in context of both the company’s own history and the specific sentiment driver (GLP-1 fears) behind it

- Monitor quarterly revenue and EPS trajectory to confirm whether growth is sustaining, accelerating, or decelerating

- Layer DCF or free cash flow analysis alongside P/S to build a more complete valuation picture

- Factor in AUD/USD currency exposure when translating US-dollar earnings into Australian portfolio returns

Whether the discount reflects fear or fundamentals is the real question

A business with global scale, 11% revenue growth, a dual-division moat combining hardware with recurring SaaS revenue, and more than 10,000 employees across 140 countries is trading at half its historical valuation multiple. That demands an explanation. The evidence available through Q3 FY2026 points to sentiment-driven repricing, specifically GLP-1 fears, rather than fundamental deterioration in ResMed’s operating performance.

The question Australian investors face is whether the 19.8% decline and the P/S compression from 8.70x to 4.30x reflect an overdone fear or a genuine structural shift in ResMed’s addressable market.

The P/S methodology used throughout this analysis is one starting point, not a verdict. Supplementary analysis, including DCF modelling, peer comparison, and segment-level SaaS metrics as they become available, would strengthen any investment conclusion. The next catalyst to watch is full-year FY2026 results and any updated commentary on GLP-1 real-world patient data from ResMed’s own reporting.

For investors wanting to stress-test whether ResMed’s recovery thesis depends on a sector-wide re-rating or on company-specific execution, our full explainer on the structural case for ASX healthcare examines the 16-percentage-point annual underperformance gap, US healthcare expenditure projections through 2033, and the specific conditions under which the sector’s structural tailwinds would historically have outweighed its valuation risks.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.