CURE and CLNE: the ASX ETFs Returning 25% in 2026

8 hrs ago

The US Federal Reserve cut rates three times in late 2024, delivering 100 basis points of easing. Global REIT investors expected a tailwind. Instead, the FTSE Nareit All Equity REIT Index fell 8.15% in Q4 2024 alone, closing the full year up just 4.92%.

A multi-central-bank easing cycle is now well underway. The Fed has cut to 3.50-3.75% as of May 2026. The European Central Bank (ECB) has pushed its main refinancing rate to 2.15%. Yet REIT performance has remained muted, with the index posting just 2.3% for full-year 2025. The gap between the expected rate-cut narrative and the actual return record demands explanation.

What follows unpacks the four mechanisms through which interest rates transmit into REIT valuations, maps the historical outperformance pattern, explains why the current cycle has delivered less than expected, and identifies where the structural setup may still favour REITs as the cycle matures. The goal is a clear framework for evaluating global REIT exposure in a lower-rate world, not a bullish summary.

The historical case for REIT outperformance during rate-cutting cycles is well documented, but it rests on a more specific mechanism than most investors assume. According to Franklin Equity Group portfolio managers Daniel Scher and Blair Schmicker, REITs have historically delivered their strongest relative returns when long-term interest rates decline, not simply when central banks cut policy rates.

Franklin Equity Group has noted that REIT outperformance during easing cycles has been most consistent when long-term rate declines coincide with slowing economic growth, a combination that widens the income advantage real estate offers over fixed-income alternatives.

The distinction matters because the 10-year US Treasury yield functions as the primary benchmark for valuing future REIT cash flows. When that yield falls, the present value of REIT income streams rises. When it does not, Fed cuts at the short end may do little for REIT valuations.

Historically, the conditions under which REIT outperformance has been most consistent include:

The pattern is real. But it is conditional on what happens at the long end of the yield curve, a nuance the current cycle has tested directly.

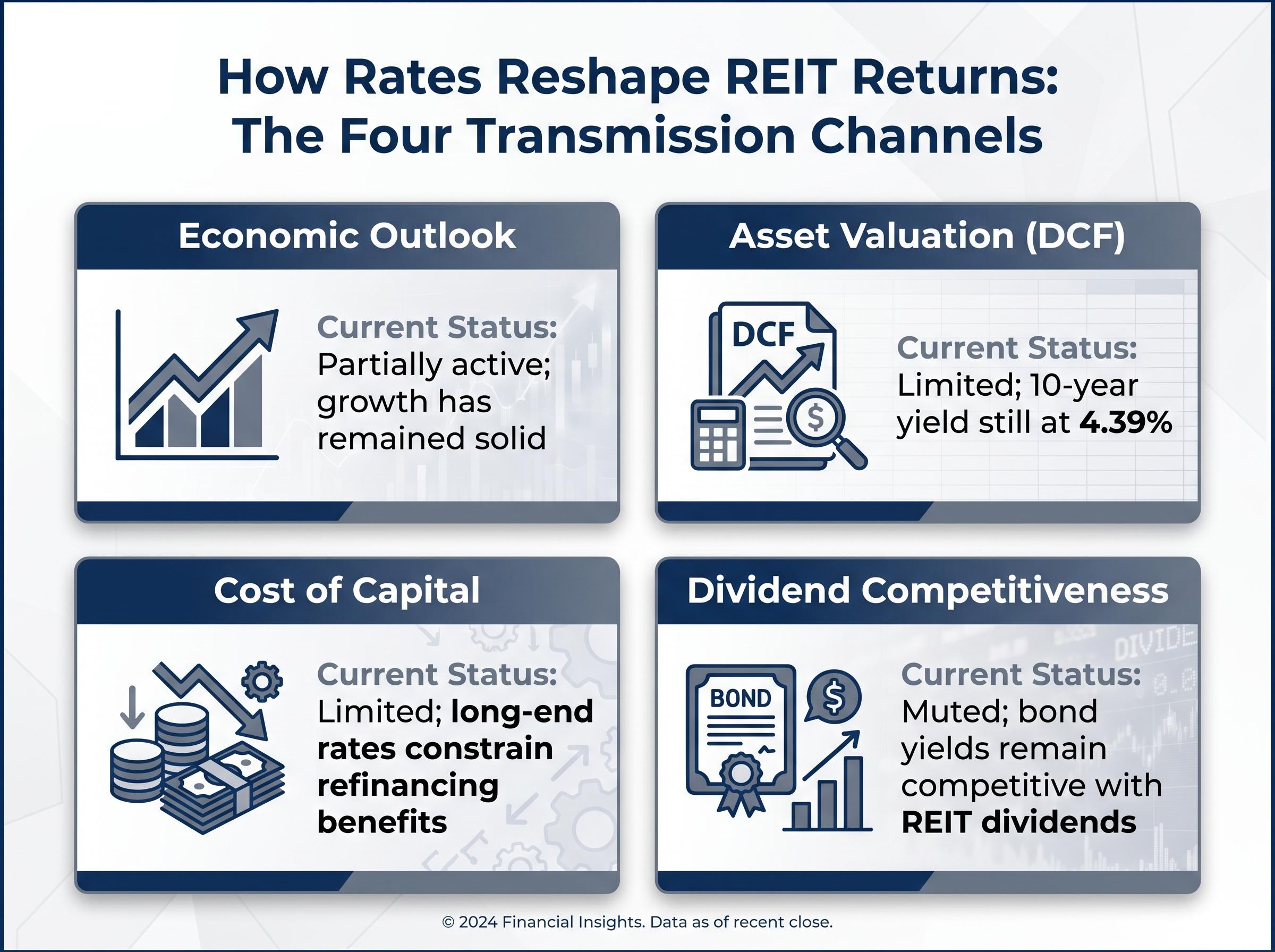

Rate movements reach REIT valuations through four distinct transmission channels. Understanding each one separately, rather than treating “rates” as a single input, is what separates a diagnostic framework from a directional bet.

The first channel is the long-end yield signal. Central bank easing typically coincides with weaker growth expectations, which compress long-term bond yields as markets price in a slower future. For REITs, this compression is the primary event: it is the 10-year Treasury moving lower, not the policy rate alone, that drives capital into stable income-producing assets and lifts demand for real estate equities.

The second channel is debt refinancing and balance sheet relief. REITs are capital-intensive businesses that carry substantial long-duration borrowing. When long-term rates fall, the cost of rolling over or issuing new debt declines, improving cash flow margins across the portfolio. This channel is structural rather than speculative: it operates through actual financing transactions, not just market pricing.

The valuation sensitivity at the core of the current REIT underperformance story is ultimately a discount rate mechanics problem: the formula P = D1 / (r – g) means that even modest upward pressure on the required return (r) produces outsized downward pressure on present value, which is precisely why a 10-year Treasury yield anchored at 4.39% can neutralise significant policy easing at the short end.

The third channel is relative income attractiveness. As government bond yields fall, the income advantage offered by REIT dividend distributions widens. Investors who need yield and previously held bonds find REIT distributions increasingly competitive, supporting capital inflows and price appreciation. With the 10-year US Treasury at 4.39% as of 5 May 2026, this channel has delivered limited relief despite cumulative Fed cuts.

The fourth channel is growth capital access. Lower long-term rates ease the conditions under which REITs can fund acquisitions, development pipelines, and portfolio expansion. Cheaper equity and debt issuance enables accretive growth that compounds NAV over time, a benefit that accrues more slowly than valuation repricing but is durable once underway. When long-end rates remain elevated, as they have through much of this cycle, this channel stays constrained alongside the others.

These four channels can work in different directions simultaneously, which is precisely why rate cuts do not guarantee REIT gains.

| Channel | Mechanism | Direction Under Rate Cuts | Current Status (May 2026) |

|---|---|---|---|

| Economic Outlook | Slowing growth drives long-term yields lower | Supportive | Partially active; growth has remained solid |

| Asset Valuation (DCF) | Lower discount rates raise present value of rental income | Supportive | Limited; 10-year yield still at 4.39% |

| Cost of Capital | Lower long-term borrowing costs improve REIT margins | Supportive | Limited; long-end rates constrain refinancing benefits |

| Dividend Competitiveness | Falling bond yields make REIT income more attractive | Supportive | Muted; bond yields remain competitive with REIT dividends |

The REIT market’s reaction to the Fed’s easing cycle has followed a pattern that institutional investors recognise but retail allocators often miss: buy the rumour, sell the news. REIT prices rose through mid-2024 in anticipation of rate cuts. When the Fed began delivering them in September 2024, Treasury yields at the long end remained stubbornly elevated, and the anticipated valuation uplift failed to materialise.

The numbers tell the story. The FTSE Nareit All Equity REIT Index returned 4.92% for full-year 2024, with most of that gain accumulated before the first cut. The Q4 sell-off of -8.15% reversed months of pre-cut optimism. Full-year 2025 delivered just 2.3%, well below the 8-10% range that early projections had assumed.

Nareit 2025 index return data confirmed the FTSE Nareit All Equity REITs Index finished the year with a total return of 2.3%, a result that validated concerns raised throughout the year about the incomplete transmission of Fed easing into REIT valuations.

The US 10-year Treasury yield stood at 4.39% as of 5 May 2026, according to Federal Reserve Economic Data (FRED), well above the 3.5-4.0% range that early 2025 consensus had priced as a base case.

The gap between the federal funds rate (3.50-3.75% as of April 2026) and the 10-year yield reveals the central analytical tension: Fed cuts have not pulled long-end yields down with them. Sticky inflation and solid economic growth have constrained the pace of easing below initial market expectations, keeping the discount rate for REIT cash flows elevated.

The concern extends beyond REIT valuations: Bank of America’s Michael Hartnett has identified a long-end yield tripwire at 5% on the 30-year Treasury, a level that sat at 4.98% as of 30 April 2026, where a breach would simultaneously push 30-year mortgage rates above 8%, raise corporate borrowing costs, and compound the federal government’s debt service burden.

The Federal Reserve FOMC decision from April 2026 confirmed the target range for the federal funds rate held at 3.50-3.75%, reflecting a committee that has delivered cumulative easing while keeping its options open as long-end yields remain resistant to compression.

Three structural factors have limited the current cycle’s REIT tailwind:

The RBA’s reversal illustrates why a globally synchronised easing narrative carries real allocation risk. Investors who positioned for a uniform global rate-cut tailwind found that Australian REIT valuations moved in the opposite direction.

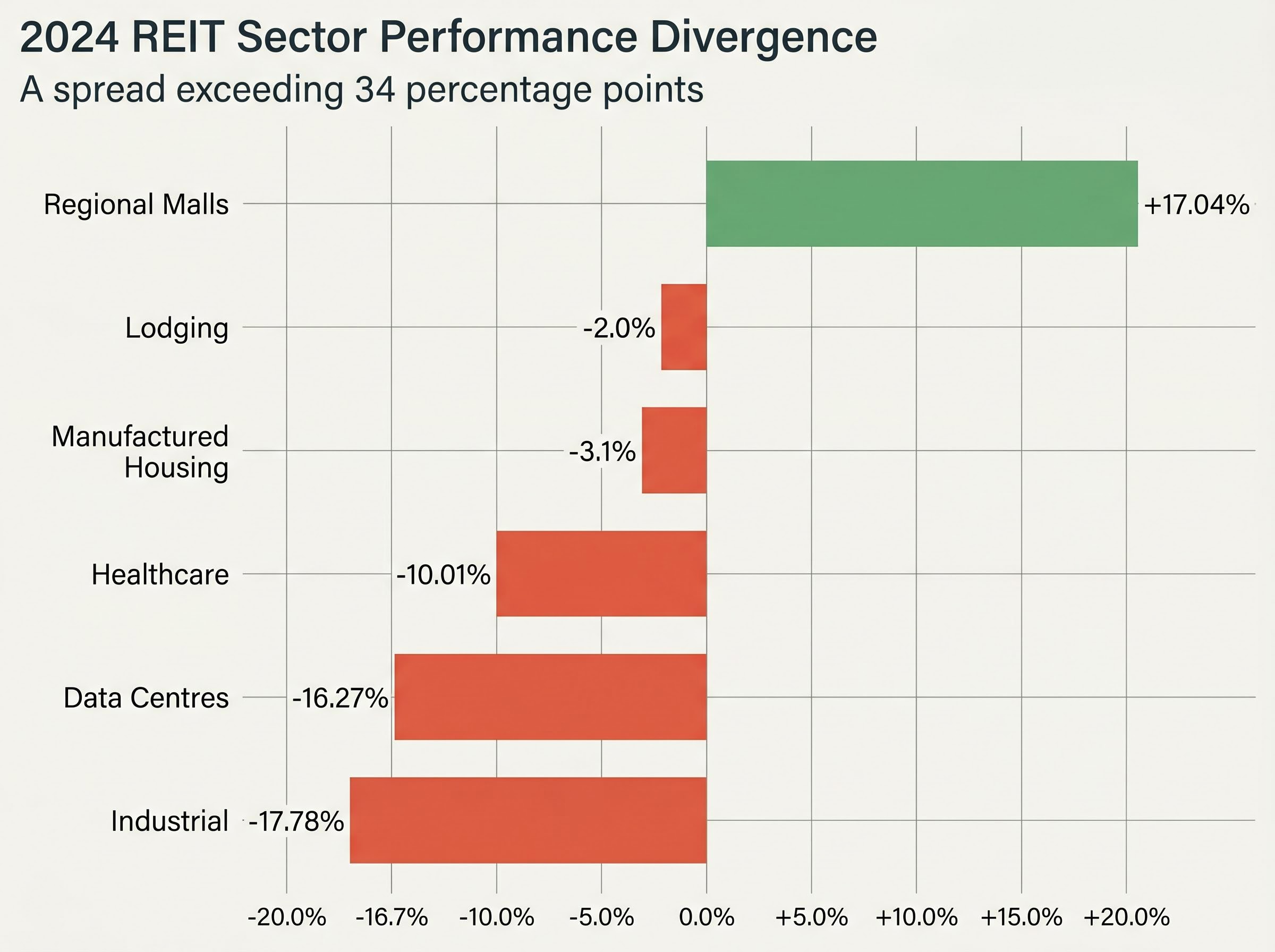

The 2024 sector-level data makes one thing clear: “REITs” is not a monolithic call. The dispersion between the best and worst performing sectors exceeded 34 percentage points, a spread that no single rate narrative can explain.

| Sector | 2024 Total Return | Primary Driver | Rate Sensitivity Profile |

|---|---|---|---|

| Regional Malls | +17.04% | Resilient consumer demand, limited new supply | Moderate; benefited from income stability |

| Lodging | -2.0% | Travel demand normalisation | Moderate; short lease durations limit rate drag |

| Manufactured Housing | -3.1% | Modest demand softening | Low; defensive income profile |

| Healthcare | -10.01% | Operational cost pressures, rate headwinds | High; long-duration leases sensitive to discount rates |

| Data Centres | -16.27% | Valuation compression despite structural demand | High; growth-oriented, sensitive to DCF channel |

| Industrial | -17.78% | Supply overhang, e-commerce deceleration | High; long leases, capital-intensive |

Regional Malls outperformed because their returns were driven by fundamentals, resilient foot traffic and constrained new supply, rather than rate sensitivity. Industrial REITs, by contrast, faced a supply overhang that coincided with the most rate-sensitive part of the market: long-duration leases and capital-intensive development pipelines. Data Centres suffered valuation compression despite structural demand from AI and cloud infrastructure, a case where the DCF channel (elevated discount rates) overwhelmed the sector’s growth narrative.

Australian retail REITs illustrate the fundamentals-versus-rate-sensitivity split in concrete terms: Scentre Group and Vicinity Centres are operating at 99.8% and 99.6% occupancy respectively, posting positive leasing spreads of +3.3% and +4.6%, while office-focused peers such as Dexus flagged delayed recovery in the same reporting period, confirming that sub-sector selection within a single jurisdiction can produce returns as divergent as the cross-sector data shows globally.

Institutional outlooks for 2025 from Franklin Templeton, CenterSquare, and JP Morgan identified Data Centres, Residential/Multifamily (supported by supply constraints), and Healthcare (defensive positioning) as sectors with structural demand tailwinds in a lower-rate environment. CenterSquare’s 2025 Global REIT Outlook also highlighted differentiated European REIT opportunities, given the ECB’s more aggressive easing relative to the Bank of England.

The sector dispersion confirms that the allocation question is not simply whether to own REITs, but which types and in which jurisdictions.

The opportunity framing that dominates most REIT commentary during easing cycles tends to understate the risk side. Four categories deserve explicit attention, ranked by current materiality:

The International Monetary Fund’s April 2025 report noted elevated asset valuations broadly, implying vulnerability to repricing across real estate markets if credit conditions tighten further.

Beneath the macro layer sit operational risks that rate narratives tend to obscure. REIT dividends are variable and dependent on rental income, which itself depends on lease occupancy and tenant credit quality. Commercial real estate credit conditions have tightened as elevated long-end yields constrain debt issuance. Regulatory risks, including rent controls, zoning restrictions, and taxation changes, vary by jurisdiction but can materially affect income growth.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The four-channel framework, combined with the sector dispersion data and the current yield environment, points to a coherent forward-looking view: the structural conditions for REIT outperformance are forming, but the catalyst has not fully materialised.

If the ECB’s aggressive cutting cycle (main rate at 2.15% as of June 2025) continues and the Fed follows with further reductions through 2026, the long-end yield compression required for the valuation channel to open may still arrive. Franklin Templeton has noted that further rate declines would create potential for “strong returns” based on historical patterns.

The energy shock running beneath the current cycle has materially complicated the forward rate path: Brent crude above $110 per barrel has already forced a repricing of global rate expectations across the Fed, ECB, and Bank of England simultaneously, with the Fed losing roughly 50 basis points of priced cuts and the ECB now facing scenarios involving renewed hikes rather than continued easing.

Franklin Templeton has stated that continued rate declines could generate “strong returns” for REITs, supported by historical patterns of outperformance during sustained easing cycles.

REIT dividend yields in the 3.5-4.0% range maintain a structural income advantage relative to equities in lower-rate jurisdictions. The 2025 index return of 2.3% represents the baseline from which any acceleration would need to build.

Three conditions would signal the valuation channel is opening:

The portfolio allocation question, then, is not whether to time a rate-cut trade precisely. It is whether to position structurally around income yield, inflation linkage through rents, and diversification away from duration-sensitive fixed income.

The historical relationship between REITs and interest rates is real, but it operates through long-end yields and the cost of capital channel, not through short-end policy rate cuts alone. That distinction explains why 100 basis points of Fed easing and cumulative global cuts have so far delivered modest REIT returns rather than the outperformance the headline narrative promised.

Global REIT exposure requires distinction between jurisdictions with advancing easing cycles and those where policy has stalled or reversed. It also requires distinction between sectors with structural demand tailwinds and those carrying supply or credit headwinds.

The conditions for the historical outperformance pattern to reassert are building across most major markets. The 10-year yield path through the remainder of 2026 will be the variable that determines whether those conditions convert into returns. That single data point, not the federal funds rate, is the one worth monitoring.

These forward-looking observations are speculative and subject to change based on market developments, central bank decisions, and macroeconomic conditions.

REITs are most sensitive to long-term interest rates, particularly the 10-year Treasury yield, rather than short-term policy rate cuts alone. When long-end yields fall, the present value of REIT income streams rises, improving valuations through lower discount rates and cheaper borrowing costs.

The FTSE Nareit All Equity REIT Index fell 8.15% in Q4 2024 despite Fed cuts because the 10-year Treasury yield remained elevated, preventing the valuation and cost-of-capital channels from opening. REIT prices had already risen in anticipation of cuts, so when the long end failed to follow the short end lower, the expected uplift did not materialise.

Data centres, industrial, and healthcare REITs carry the highest rate sensitivity because they rely on long-duration leases and capital-intensive development pipelines that are most exposed to discount rate movements. Regional malls outperformed in 2024 largely because their returns were driven by fundamentals like occupancy and supply constraints rather than rate sensitivity.

Three indicators to monitor are the 10-year US Treasury yield falling sustainably below 4.0%, continued Fed easing through the remainder of 2026, and stable or improving REIT earnings growth across rate-sensitive sectors. Until the long-end yield moves lower, the primary valuation channel remains partially closed.

Not all central banks are easing simultaneously, which creates divergent REIT performance across jurisdictions. The Reserve Bank of Australia raised its cash rate to 4.35% by May 2026, moving in the opposite direction to the Fed and ECB, producing valuation headwinds for Australian REITs that a synchronised global easing narrative would not have anticipated.