Why Orion Stock Fell 4.3% Despite 47% Profit Growth in Q1

51 mins ago

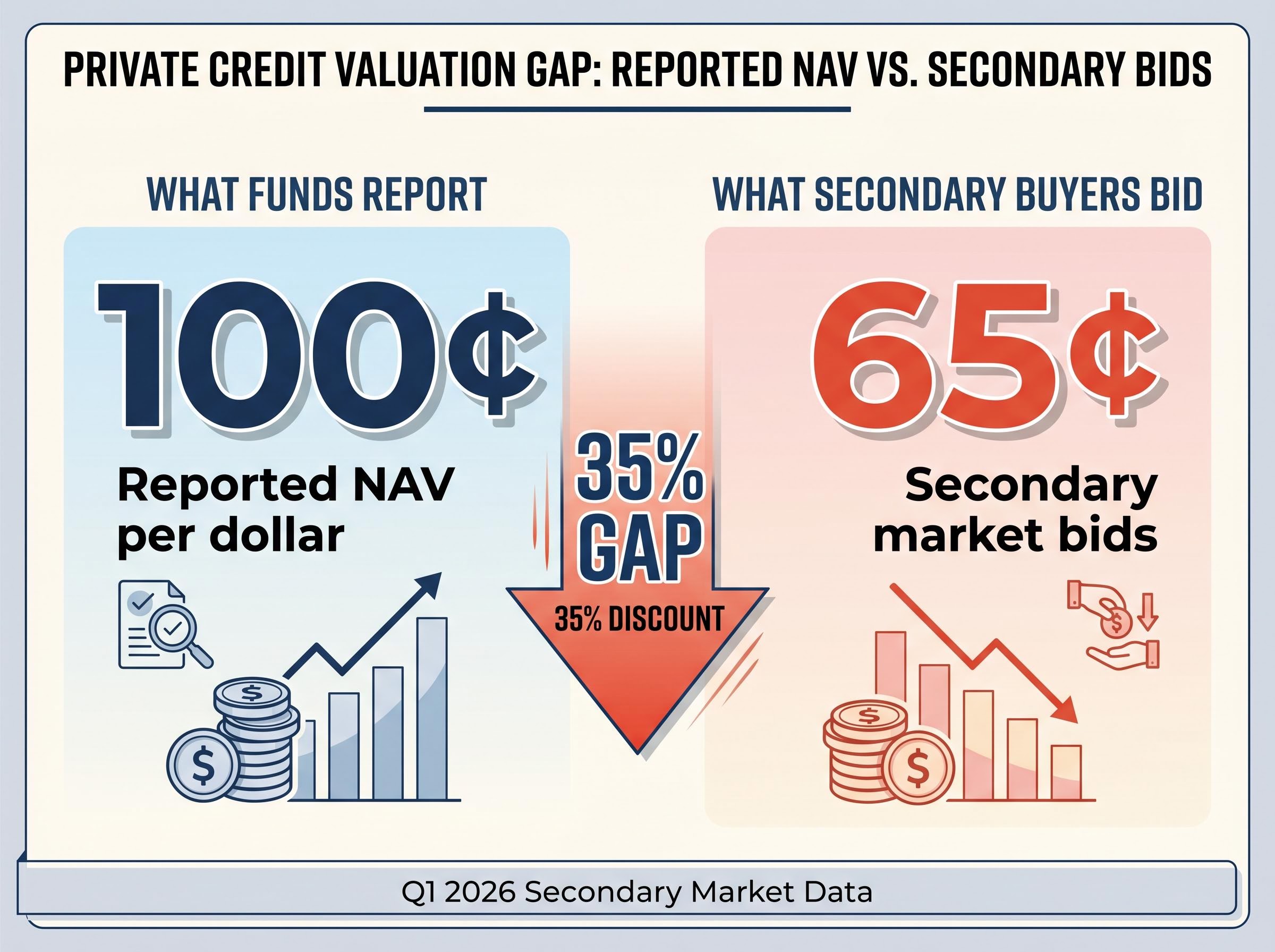

Secondary market buyers are bidding 65 cents on the dollar for private credit fund stakes whilst managers continue reporting those same assets at full net asset value. This 35% gap between what investors will pay and what funds claim their holdings are worth has become the central question of 2026 for a sector managing $644 billion in assets.

The year has become a stress-test for private credit valuations. Q1 redemption requests hit $19.5 billion, with only 53% honoured. Publicly traded business development companies (BDCs) are trading at 19-28% discounts to reported net asset value (NAV). The failed Blue Owl merger in November 2025 exposed the tension between reported values and market-clearing prices in a transaction that should have been straightforward if stated values were accurate.

This analysis examines what the evidence reveals about whether private credit valuations are systematically overstated, which signals investors should monitor, and what the coming quarters may reveal as $875 billion in commercial mortgage debt and $620 billion in high-yield bonds mature through 2026.

Publicly traded BDCs ended Q1 2026 at an average discount of approximately 25% to stated net asset value. This represents an extreme historical outlier. Only 5% of months in the past 25 years showed wider discounts than currently observed, compared to the long-term historical average of approximately 3.1%.

The discounts are not isolated to distressed names. SLR Investment Corp (NASDAQ: SLRC) trades at a 19% discount despite meeting street expectations in late February earnings. Goldman Sachs BDC (GSBD) trades at a 28% discount. Gladstone Investment Corporation (GAIN) trades at 91 cents on the dollar despite net asset value rising from $12.99 per share in mid-2025 to $14.95 by year-end 2025.

| Fund Name | Ticker | Current Price-to-NAV | Discount Percentage |

|---|---|---|---|

| SLR Investment Corp | SLRC | 0.81 | 19% |

| Goldman Sachs BDC | GSBD | 0.72 | 28% |

| Gladstone Investment | GAIN | 0.91 | 9% |

Secondary market transaction data provides additional evidence of systematic repricing. Saba Capital Management, led by Boaz Weinstein, disclosed in February 2026 that it had made offers to purchase stakes in multiple private credit funds at prices ranging from 20-35% discounts to stated net asset values. These are not theoretical model-based estimates. They represent actual capital willing to transact at those levels.

Analysis of secondary market bids reveals offer prices of approximately 65 cents on the dollar, implying discounts of roughly 35% to stated NAVs. Industry research acknowledges that private market assets often require discounts of 11-20% simply to transact under normal market conditions. The 35% secondary market discounts suggest markets are pricing in either fundamental deterioration in underlying asset quality or systematic overvaluation in how funds are marking positions.

When multiple independent pricing signals converge on similar discount levels, it suggests systematic rather than idiosyncratic mispricing. Public market pricing provides observable, real-time data that challenges the assumptions embedded in quarterly NAV calculations.

The NBER working paper on private credit capitalization and performance presents comprehensive fund-level and asset-level data showing that valuation practices vary significantly across the sector, with some managers applying more conservative assumptions than others. This research validates the market’s concern that systematic overvaluation may exist in portions of the $2 trillion private credit market.

Blue Owl Capital Corporation (NYSE: OBDC), the publicly traded entity, planned to acquire Blue Owl Capital Corporation II (BOCC II), a private business development company sponsored by the same management team. The merger mechanics appeared straightforward: exchange ratios would be based on each company’s reported net asset value.

The problem emerged in the pricing. OBDC was trading at approximately a 20% discount to its reported net asset value when the merger was proposed. BOCC II shareholders seeking liquidity would be forced to accept that 20% haircut to NAV in order to receive publicly traded shares that could be more easily sold. By the time the merger was terminated in November 2025, OBDC’s discount to NAV had widened to approximately 25%.

If both entities held similar assets and BOCC II’s NAV was accurate, shareholders should have been indifferent to receiving shares at a 20% discount. The merger failure suggests either BOCC II shareholders believed their fund’s NAV was overstated or they were unwilling to trade marked-down public shares as an alternative to waiting for better liquidity terms.

Three months after the merger failed, Saba Capital and Cox Capital Partners announced tender offers to purchase shares of BOCC II at prices expected to be 20-35% below the most recent estimated net asset values. The tender offers extended to Blue Owl Technology Income Corp (OTIC) and Blue Owl Credit Income Corp (OCIC), indicating a broad-based view that Blue Owl’s multiple BDCs were overvalued by similar margins.

This case demonstrates that when market-based pricing confronts management valuations in a high-stakes transaction, the gap becomes impossible to paper over. The merger failure is a proof point that the valuation disconnect has real consequences for investors seeking exits and for sponsors attempting to provide liquidity pathways.

Private credit assets are valued using Level 3 inputs under ASC 820, the accounting standard covering fair value measurements. Level 3 inputs are unobservable inputs requiring management assumptions about risks that market participants would consider when valuing an asset. Valuations assume orderly transactions rather than forced liquidation prices.

The ASC 820 fair value measurement standard establishes the framework for Level 3 inputs, which require management to make unobservable assumptions about risks that market participants would consider when pricing illiquid assets. This methodology creates structural differences from public markets where prices update continuously based on actual trades.

This methodology creates structural differences from public markets where prices update continuously based on actual trades. Private credit NAV calculations incorporate recent transactions of a similar nature and duration, common industry practices, and historical trends. However, when market sentiment shifts dramatically, the methodology is not designed to capture real-time price discovery.

The contrast between rapid repricing of geopolitical risk in liquid markets and the quarterly valuation cycles of private credit funds highlights why secondary market discounts can widen dramatically even when fundamental credit quality has not materially deteriorated.

Three key factors make private credit valuation inherently subjective:

Understanding valuation methodology matters because it reveals why NAVs can remain stable whilst market sentiment shifts dramatically. The methodology is not designed to capture real-time price discovery, which creates structural lag during stress periods.

The structural lag between when market sentiment shifts and price discovery in illiquid assets becomes a critical factor when evaluating whether current private credit valuations reflect genuine deterioration or temporary dislocation. Equity markets repriced Iran risk in 72 hours during April 2026, whilst private credit NAVs updated on a quarterly cycle with methodologies explicitly designed to smooth through short-term volatility.

The Securities and Exchange Commission announced in March 2026 that it would hold a roundtable discussion dedicated specifically to private markets valuation issues. This represents an elevation of regulatory focus on an issue that had previously remained largely in the background despite the growth of private markets assets to substantial proportions.

On 26 February 2026, the SEC announced settled charges against a private credit adviser that had improperly applied its stated valuation policies to asset valuations. According to the SEC’s cease-and-desist order, the adviser had promised investors that loan sales would be priced at fair value or fair market value, but the company actually priced loans using a simplified methodology that merely subtracted unamortised loan fees from the sale price without properly factoring in the asset valuation changes that had occurred during the pandemic period.

Katten, a major international law firm, has advised that private credit funds and BDCs should “review and pressure-test valuation procedures” given the infrequency with which private credit assets trade. The firm emphasises that funds must revisit their valuation processes and procedures, ensure that applicable methodologies are being applied and documented properly, and consider involving additional adviser oversight to support net asset value determinations.

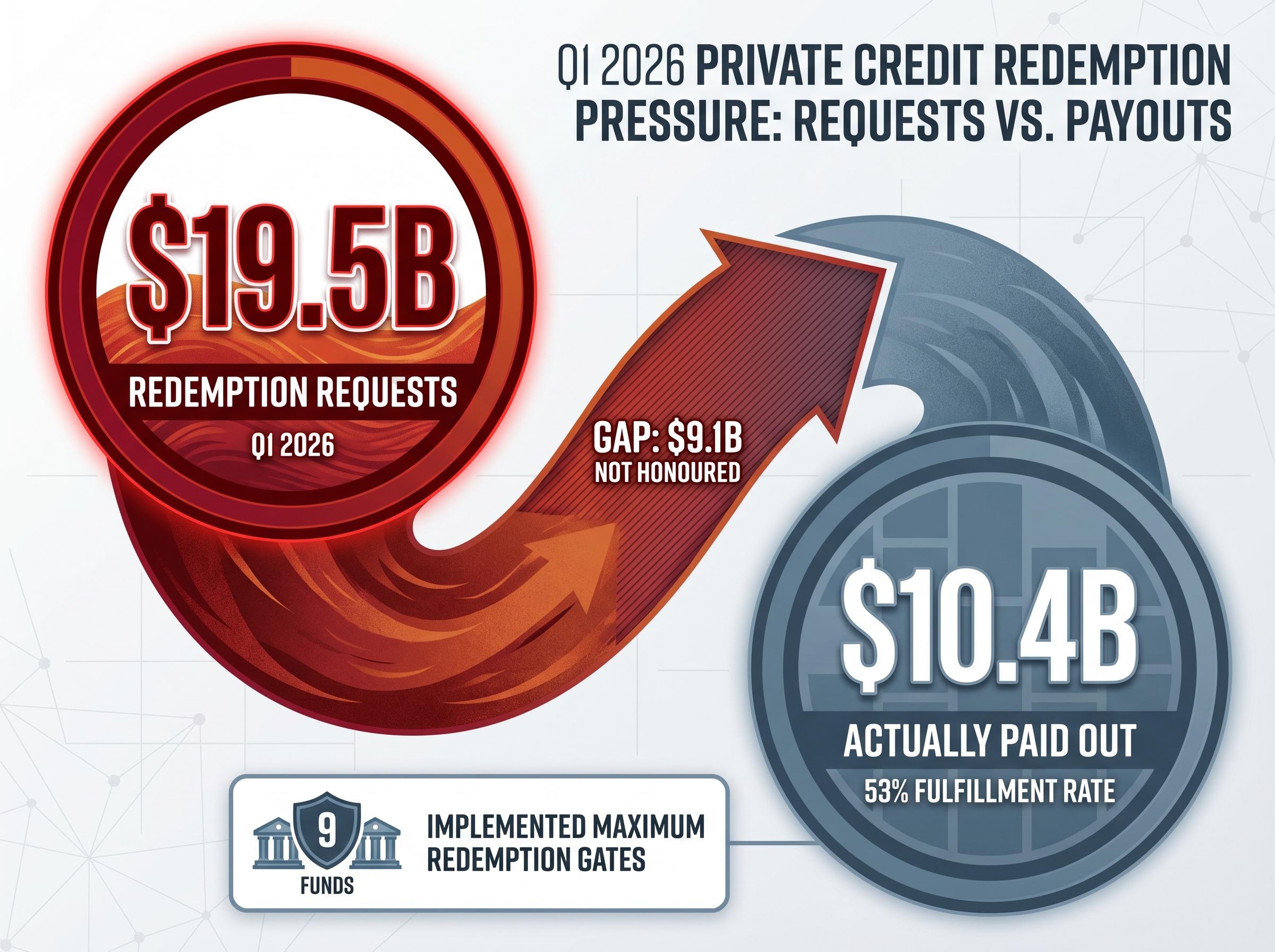

The first quarter of 2026 delivered the largest redemption wave the sector has experienced. Analysis of SEC filings by 17 major investment vehicles managing private credit direct lending strategies revealed that investors submitted redemption requests totalling $19.5 billion in net asset value during the quarter.

Despite $19.5 billion in redemption requests, only 53% were actually honoured, translating to $10.4 billion in actual payouts to investors. Nine funds implemented maximum redemption gates during the first quarter, capping investor withdrawals at the contractually permitted threshold of 5-7% of fund net asset value rather than attempting to honour larger proportions of redemption requests.

| Fund | Redemption Requests (Q1 2026) | Amount Honoured | Fulfillment Rate |

|---|---|---|---|

| Blue Owl Credit Income Corp | $4.3B | $988M | 23% |

| Cliffwater Corporate Lending Fund | $4.5B | $2.2B | 49% |

| Apollo Debt Solutions BDC | $1.6B | $730M | 46% |

| Ares Strategic Income Fund | $1.2B | $524.5M | 44% |

| Blackstone Private Credit Fund | $3.7B | $3.7B | 100% |

Blue Owl Technology Income Corp redeemed 15.4% of shares in Q4 2025, satisfying 100% of repurchase requests through 8 January 2026. When Q1 2026 arrived and redemption requests continued to flow in, the fund joined the ranks of those implementing gating, capping withdrawals at the maximum permitted levels.

Blackstone’s Strategic Differentiation Blackstone Private Credit Fund, the largest non-traded BDC with $82.7 billion in assets, declined to implement the standard 5% quarterly redemption cap and instead honoured all redemption requests, returning $3.7 billion to investors in the quarter. The decision demonstrates both confidence in its liquidity position and potentially a strategy to enhance confidence in its valuations by demonstrating ability to meet redemption requests at stated net asset values without gating.

Redemption behaviour reveals revealed preferences. When investors rush to exit at stated NAV despite knowing they may be gated, it suggests they believe current valuations may be generous relative to what they could achieve by waiting. The asymmetry between the value of redemptions requested and the cash honoured creates incentives for future redemption cascades.

Approximately $875 billion in commercial mortgage debt and $620 billion in high-yield bonds and loans are scheduled to mature in 2026. This maturity wall creates a natural experiment that will force price discovery on a large scale.

Default rate projections vary but converge on material deterioration from current levels. Fitch projects the US private credit default rate will reach approximately 9.2% at peak, more than triple the current rate. UBS initially estimated a private credit default rate of 14-15% for 2026 but subsequently revised this down to approximately 9-10%. Morgan Stanley has warned that direct lending default rates currently running around 5.6% could reach 8%.

Three scenarios emerge for how the maturity wall resolves:

The bifurcation between borrowers that successfully refinance and those that struggle creates scope for significant dispersion in realised returns. Companies with strong EBITDA growth, improving leverage metrics, and stable customer bases should refinance despite higher rates. Borrowers facing revenue pressure, margin compression, or leverage deterioration will face more difficult refinancing environments and may require workout support, covenant waivers, or debt restructuring.

For readers wanting to understand how rising financing costs interact with operational performance in alternative credit markets, our detailed coverage of how financing costs can offset operational improvements examines a parallel case in European real estate where improving occupancy metrics could not overcome interest expense pressure, a dynamic directly relevant to evaluating whether private credit borrowers can successfully refinance maturing debt in 2026.

The maturity wall creates forcing functions that will resolve valuation uncertainty one way or another. Investors with exposure to private credit should understand that the next 2-3 quarters will provide concrete data on whether secondary market discounts reflect genuine overvaluation or temporary liquidity dislocation.

Deal economics in private credit began to move meaningfully in lenders’ favour during Q1 2026. New private credit deals are clearing at wider spreads, equity cushions are increasing on new transactions, and structures are tightening.

Morgan Stanley projects that asset yields on directly originated first lien loans will trough in the 8.0-8.5% vicinity during 2026. This represents compression from current levels and reflects the expectation that new deal origination will increasingly occur at lower yields as private credit supply exceeds demand and competition for loans intensifies.

Structure tightening reflects implicit acknowledgement that prior vintage pricing was inadequate to the actual risk profile of the loans. Both lenders and the investment community are demanding more conservative pricing and better covenant protection for new commitments.

The systematic nature of the valuation signals is difficult to dismiss. Multiple independent data points converge on similar conclusions: public discounts of 19-28%, secondary bids at 65 cents on the dollar, tender offers at 20-35% discounts, and redemption fulfillment rates of 23-49% at most funds.

The countervailing case deserves consideration. Pension funds have maintained allocations despite visible stress. Major banks including Morgan Stanley continue to forecast positive excess returns from private credit relative to public credit alternatives. Fitch notes that credit quality deterioration remains primarily sector-specific rather than broadly distributed across the $2 trillion private credit market.

Three key signals to monitor over coming quarters:

Investors seeking to understand portfolio construction strategies during market volatility will find that the principles emerging from the geopolitical dislocations of early 2026 apply directly to asset-specific valuation questions in illiquid markets.

Refinancing outcomes will provide the validation or refutation that current pricing debates cannot resolve. If default rates remain in the 3-5% range, current valuations could begin to stabilise and earn back from current discounts. If default rates exceed 8-10%, secondary market pricing will likely be validated and further repricing downward will likely occur.

This interpretive framework matters because the evidence is genuinely mixed. Investors need to understand what would confirm or disconfirm the bearish thesis rather than accepting either extreme interpretation.

The private credit valuation debate in 2026 centres on whether 25-35% market discounts represent temporary liquidity dislocation or systematic overvaluation. The maturity wall of $1.5 trillion in debt maturing through 2026 will force the answer as borrowers face refinancing challenges and realised losses either validate current valuations or expose them as overstated.

Regardless of which interpretation proves correct, the days of assumed NAV stability are ending. Transparency pressure from secondary markets, regulators, and redemption behaviour will reshape how private credit valuations are produced and scrutinised. The sector is transitioning from a rapid-growth phase where valuation questions remained largely theoretical to a maturation phase where market forces are demanding observable price discovery.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Private credit valuation is the process of estimating the fair value of illiquid loan assets using management assumptions under accounting standard ASC 820, rather than observable market prices. It has become controversial because secondary market buyers are bidding only 65 cents on the dollar for fund stakes while managers continue reporting those same assets at full net asset value, creating a 35% gap.

Publicly traded BDCs ended Q1 2026 at an average discount of approximately 25% to stated net asset value, a level only seen in 5% of months over the past 25 years. The discounts reflect investor scepticism about whether reported asset values are accurate, compounded by high redemption requests, the failed Blue Owl merger, and secondary market bids at 20-35% below stated NAV.

The maturity wall refers to approximately $875 billion in commercial mortgage debt and $620 billion in high-yield bonds scheduled to mature in 2026, forcing large-scale refinancing or default events that will test whether current private credit valuations are accurate. If default rates reach the 8-10% range projected by UBS and Morgan Stanley, secondary market discounts of 25-35% are likely to be validated.

Investors should track three key signals: whether redemption fulfillment rates improve or deteriorate further from the current 53% average, whether secondary market bid levels stabilise or widen beyond the current 35% discount, and whether default rates on maturing debt confirm or refute the stress pricing already visible in public markets.

Blue Owl Capital Corporation attempted to acquire its privately managed sibling fund Blue Owl Capital Corporation II using exchange ratios based on reported net asset values, but the merger was terminated in November 2025 because OBDC was trading at a 25% discount to NAV, meaning BOCC II shareholders would have had to accept that haircut. The failure demonstrated that when market-based pricing confronts management valuations in a real transaction, the gap between stated and market values cannot be papered over.