Why Orion’s 47% Profit Surge Led to a 4.3% Share Price Drop

17 mins ago

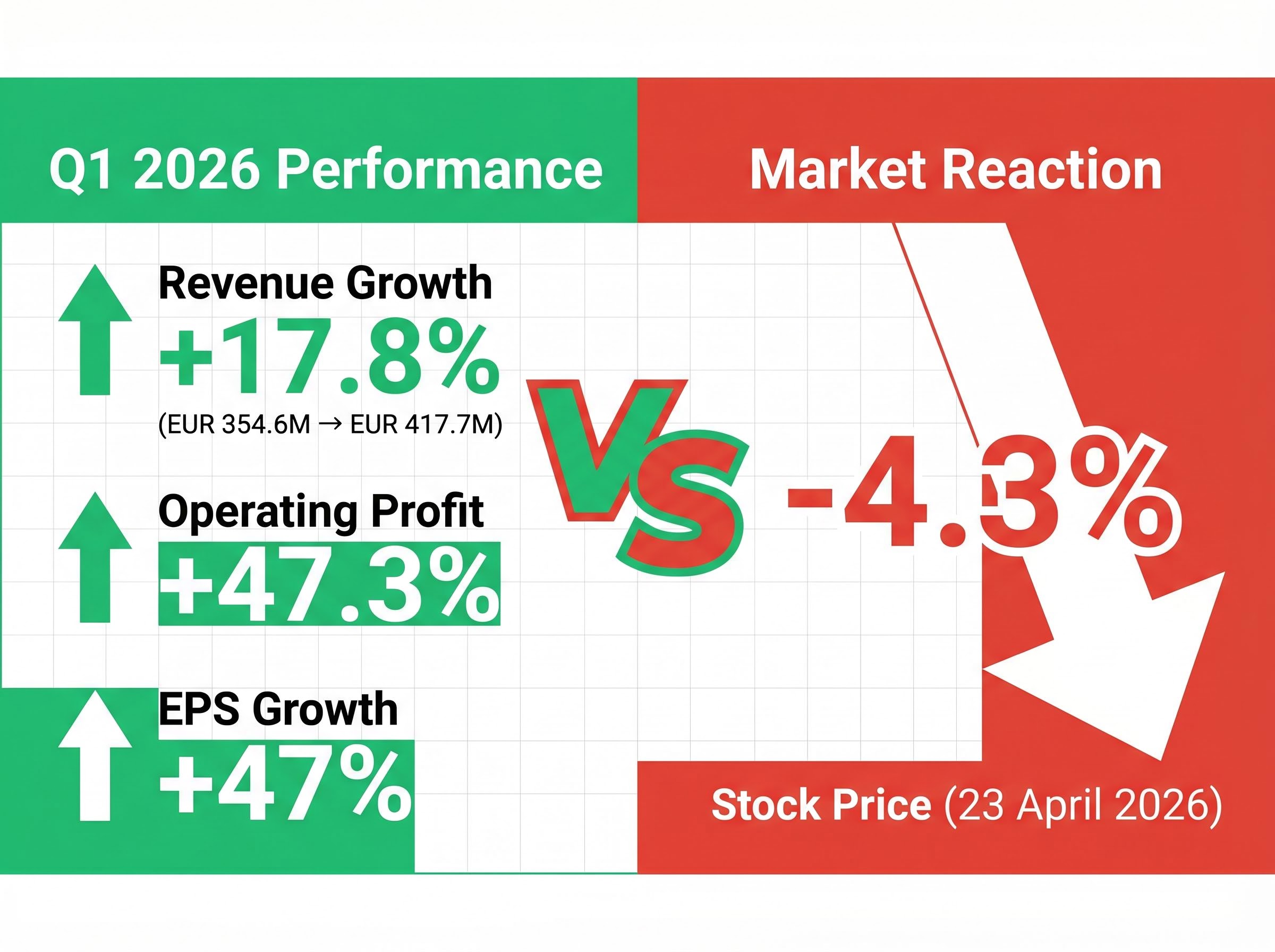

A pharmaceutical company delivers 17.8% revenue growth, 47.3% operating profit expansion, and raises full-year guidance, yet its stock drops 4.3% on announcement day. Orion Corporation’s Q1 2026 results, released on 23 April 2026, present exactly this contradiction. For investors tracking pharmaceutical equities, the Finnish company’s market reception demands explanation beyond headline metrics.

This analysis unpacks the six factors driving the counterintuitive response, from earnings quality concerns to competitive clinical evidence, revealing what sophisticated institutional investors see that strong quarterly numbers obscure.

Orion’s Q1 performance arrived with metrics that typically trigger positive price action. Revenue climbed to EUR 417.7 million from EUR 354.6 million in Q1 2025, marking 17.8% growth. Operating profit expanded 47.3% year-over-year, substantially outpacing revenue growth and indicating operational leverage within the cost structure. Basic earnings per share rose 47% versus the prior-year period.

The company raised 2026 guidance alongside the results. Net sales expectations moved to EUR 1,950-2,100 million from the January range of EUR 1,900-2,100 million. Operating profit guidance lifted to EUR 600-750 million from EUR 550-750 million. Management explicitly stated the outlook excludes material milestone payment expectations, framing growth as operationally driven rather than dependent on one-time windfalls.

Shares of ORNBV on the Helsinki Stock Exchange fell 4.3% on 23 April despite these figures.

For investors wanting to understand why strong headline numbers can produce negative market reactions, our dedicated guide to KPI-based earnings analysis walks through the operational metrics institutional investors prioritise when assessing whether reported results translate to sustainable performance, with worked examples across multiple sectors including pharmaceuticals.

| Metric | Q1 2025 | Q1 2026 | Change | Stock Reaction |

|---|---|---|---|---|

| Net Sales | EUR 354.6M | EUR 417.7M | +17.8% | -4.3% |

| Operating Profit Growth | Baseline | +47.3% YoY | +47.3% | |

| Basic EPS Growth | Baseline | +47% YoY | +47% |

Revised 2026 Guidance Net sales: EUR 1,950-2,100 million Operating profit: EUR 600-750 million (Excludes material milestone expectations)

The EUR 50 million midpoint increase on both net sales and operating profit represents a modest uplift relative to Q1’s performance. Given that the quarter substantially outperformed consensus expectations, some institutional investors interpreted the conservative magnitude as signalling limited visibility or confidence in sustaining exceptional full-year performance.

Context matters. Q4 2025 included a EUR 180 million Nubeqa-related milestone payment that temporarily boosted profitability. That windfall will not recur in 2026. The revised guidance explicitly excludes similar one-time events, meaning 2026 profitability growth depends entirely on underlying business momentum.

Management’s own statement acknowledged inherent difficulty in predicting royalty levels from a strongly growing product. Variance from projected royalty streams can have notable impact on operating profit. The measured guidance revision, paired with this acknowledgement of forecasting challenges, may have planted the first seed of doubt about whether Q1’s strength translates to full-year outperformance.

Original vs Revised 2026 Guidance:

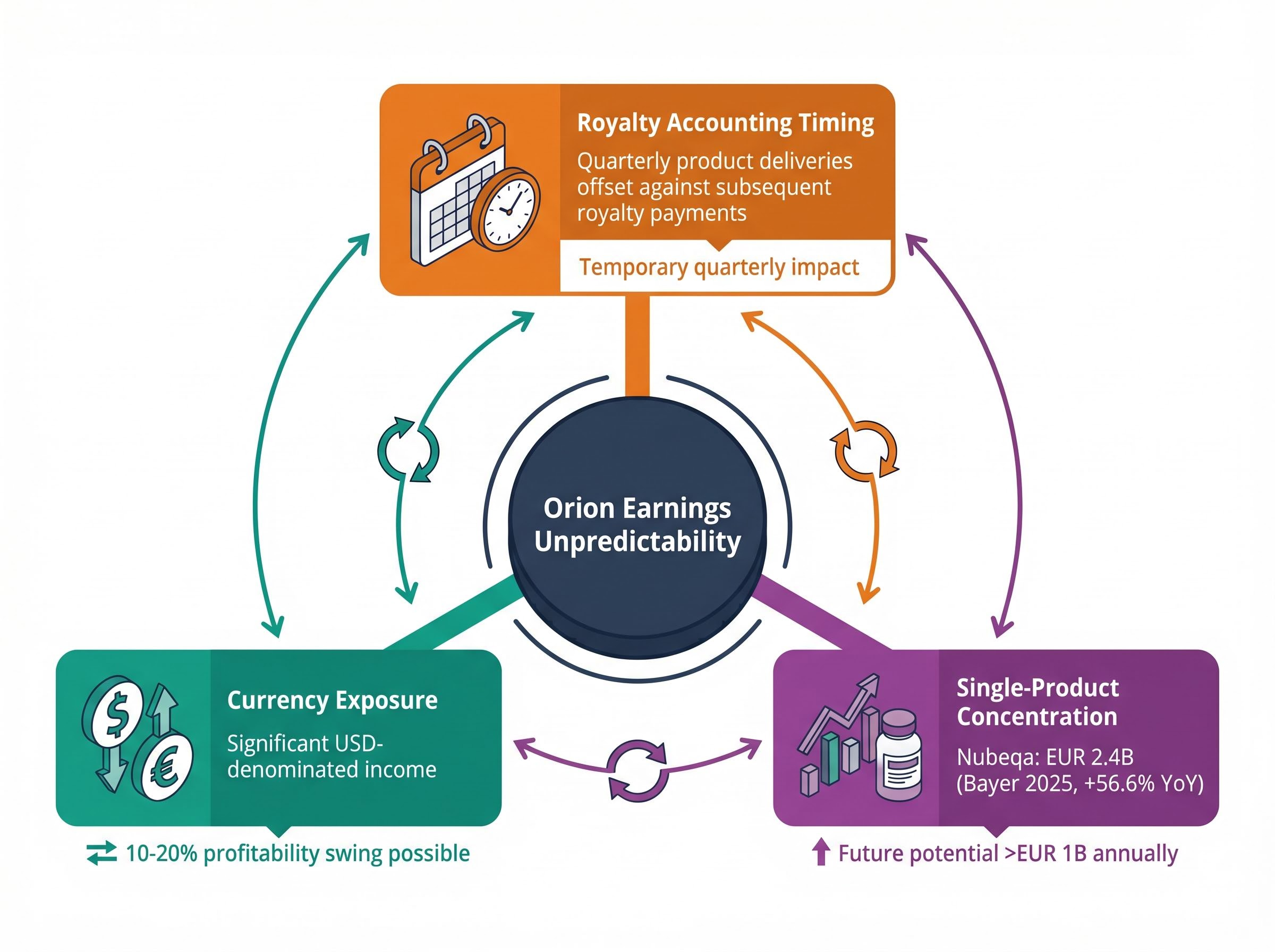

Orion receives a percentage of Bayer’s global Nubeqa sales as royalty income. The specific percentage remains undisclosed, but the mechanism creates structural volatility in reported earnings independent of underlying business performance.

The accounting works as follows: each quarter’s product deliveries to Bayer are fully deducted from the following quarter’s royalty payments. This timing mechanism, governed by the IFRS 15 revenue recognition standard for licensing and royalty arrangements, causes operating profit to fluctuate quarter-to-quarter even when Nubeqa’s market performance remains stable.

Royalty-dependent revenue models in pharmaceutical companies create structural earnings volatility independent of underlying product performance, a pattern visible across multiple ASX-listed biotech equities receiving percentage-based payments from global commercialisation partners.

The accounting works as follows: each quarter’s product deliveries to Bayer are fully deducted from the following quarter’s royalty payments. This timing mechanism causes operating profit to fluctuate quarter-to-quarter even when Nubeqa’s market performance remains stable. Management stated the impact is temporary on operating profit but may have notable annual effects depending on delivery timing.

Currency exposure compounds the unpredictability. Significant portions of Nubeqa royalty income derive from US dollar-denominated sales, primarily from the United States. Changes in the USD/EUR exchange rate cause material fluctuations in euro-reported operating profit. A 10-20% swing in profitability from currency movements alone is plausible during periods of material dollar strength or weakness.

Bayer reported EUR 2.4 billion in global Nubeqa revenue for 2025, representing 56.6% year-over-year growth. Orion estimates annual Nubeqa net sales recorded by the company have potential to exceed EUR 1 billion in the future. That concentration makes the royalty stream extraordinarily valuable but also creates dependence on a single product’s trajectory.

Management Statement on Forecasting Challenges “Royalty levels are difficult to predict from a strongly growing product. Variance from predicted levels can have notable impact on operating profit.”

Three sources of earnings unpredictability:

While Q1 delivered strong results, multiple threat vectors emerged during the quarter that sophisticated investors weighed against current performance.

In February 2026, Johnson & Johnson announced real-world head-to-head analysis results comparing Erleada (apalutamide) and Nubeqa (darolutamide) in patients with metastatic castration-sensitive prostate cancer (mCSPC) who were not receiving docetaxel chemotherapy. The findings favoured Erleada.

Clinical evidence from head-to-head trials shaping competitive positioning has become increasingly determinative of market share trajectories in oncology and specialty therapeutics, where payers and physicians weigh real-world comparative effectiveness data alongside randomised controlled trial results when making formulary and prescribing decisions.

Erleada Clinical Advantage Patients initiating Erleada without docetaxel experienced a 51% reduction in risk of death compared to darolutamide without docetaxel through 24 months (HR 0.49, 95% CI: 0.30-0.83, p=0.007). The survival advantage reached statistical significance.

The study was retrospective real-world analysis rather than a prospective randomised controlled trial, which limits the strength of conclusions. However, a statistically significant mortality reduction of this magnitude in a clinically relevant patient population presents a material competitive challenge. If physicians shift prescribing patterns based on this evidence, Nubeqa’s market share trajectory in the mCSPC indication could slow, directly impacting Orion’s royalty income growth.

Nubeqa continues achieving robust sales growth and meaningful market penetration despite competition from Erleada, Xtandi, and other therapies. The prostate cancer treatment market supports multiple successful products. The question is whether the February 2026 clinical evidence accelerates competitive pressure that constrains Nubeqa’s growth rate over the medium term.

The prostate cancer therapeutic landscape supports multiple successful products across different mechanisms of action and patient populations, with androgen receptor inhibitors, radiopharmaceuticals, and chemotherapy combinations all maintaining market share despite direct competition, suggesting the Erleada clinical data may shift prescribing patterns without eliminating Nubeqa’s commercial opportunity.

The Trump administration’s Most Favoured Nation (MFN) pricing policy transitioned from proposal to increasingly enforceable mechanism during 2025-2026. As of March 2026, 16 pharmaceutical companies had signed confidential MFN deals with the US government, including Novartis and Roche. The policy aims to force pharmaceutical companies to charge US consumers prices comparable to those in other wealthy countries.

The HHS real-time prescription drug pricing rule effective October 2025 grants doctors and patients access to comparative pricing data at the point of prescribing, a transparency mechanism that complements MFN policy pressure by creating direct price visibility for prescribers evaluating treatment options.

In February 2026, the TrumpRx.gov prescription drug website launched, creating a high-profile platform where failure to offer lowest international prices results in exclusion. Novo Nordisk signed an MFN deal and reduced Wegovy and Ozempic prices from over $1,000 per month to $350 per month via TrumpRx. The company is forecasting potential revenue declines of 5-13% for 2026 as a result.

Nubeqa generates significant revenues from US markets through Orion’s royalty streams. If Bayer is forced to reduce US Nubeqa prices for MFN compliance, Orion’s royalty income declines directly, regardless of whether prescription volumes remain healthy. The pricing pressure dynamics could create earnings volatility independent of underlying demand.

MFN policy implications for Orion:

Nordic pharmaceutical markets demonstrated exceptional divergence during 2025. Denmark’s Copenhagen market fell more than 20% in 2025, tracking toward the country’s worst year since 2008. Finland performed substantially stronger. The divergence reflects company-specific challenges, competitive dynamics, and varying exposure to pricing pressures across the region. Orion operates within this fragmented Nordic landscape where sector headwinds create macro uncertainty even for companies executing well operationally.

Orion trades at a forward P/E of 19.49 and trailing P/E of 21.10 as of April 2026. The valuation multiples are neither exceptionally cheap nor extraordinarily expensive relative to European pharmaceutical sector comparables. The stock appreciated 61.70% over the prior year, indicating the market had already recognised and rewarded the company’s Nubeqa-driven growth trajectory.

Institutional ownership stands at approximately 70.25% of outstanding shares. This high concentration means research-driven analysis and quantitative models drive the majority of trading patterns. The 4.3% decline on strong earnings reflects sophisticated recalibration rather than retail panic or market inefficiency.

The market is pricing sustainability risk. Current valuation already reflects near-term positive expectations. Further multiple expansion requires evidence that Nubeqa growth can withstand Erleada’s competitive positioning, MFN pricing compression, currency volatility, and the structural unpredictability inherent in royalty-dependent earnings.

Key factors investors should monitor going forward:

Orion’s strategic investments, including the Cambridge R&D centre opened in 2025 and the April 2026 appointment of Berkeley Vincent as Executive Vice President of Innovative Medicines, position the company to develop next-generation products. However, near-term financial performance remains heavily dependent on the single-product Nubeqa royalty stream, and the market is demanding proof of execution before rewarding further valuation expansion.

Orion Corporation’s Q1 2026 results demonstrated genuine operational strength with 17.8% revenue growth and 47.3% operating profit expansion. The company raised full-year guidance proactively. Yet the market’s 4.3% negative response reflects rational evaluation of concentration risk, competitive clinical evidence favouring Erleada, pricing headwinds from MFN policy, and earnings unpredictability from royalty accounting and currency exposure.

For investors considering Orion, the central question is not whether Q1 was strong (it objectively was) but whether Nubeqa’s growth trajectory can withstand mounting competitive pressure, pricing compression, and the structural volatility inherent in royalty-dependent earnings. The market is pricing sustainability risk rather than ignoring good news.

The paradox resolves when understood through the lens of earnings quality and forward visibility rather than headline growth metrics. Institutional investors holding 70% of shares are recalibrating expectations at a company navigating the complex intersection of commercial success, competitive threats, and pharmaceutical sector headwinds in 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Orion stock fell 4.3% on 23 April 2026 despite reporting 17.8% revenue growth and 47.3% operating profit expansion because institutional investors weighed concentration risk, competitive clinical evidence favouring rival drug Erleada, MFN pricing policy headwinds, and structural earnings unpredictability from royalty accounting and currency exposure against the headline figures.

Royalty-dependent earnings volatility refers to fluctuations in reported profit caused by the accounting timing of royalty payments rather than changes in underlying product performance. For Orion, each quarter's product deliveries to Bayer are deducted from the following quarter's Nubeqa royalty payments, causing operating profit to swing even when Nubeqa's commercial performance remains stable.

The Trump administration's Most Favoured Nation pricing policy could force Bayer to reduce US Nubeqa prices to comply with government requirements, which would directly reduce Orion's euro-reported royalty income regardless of whether prescription volumes remain healthy.

In February 2026, Johnson and Johnson published real-world analysis showing Erleada reduced the risk of death by 51% compared to Nubeqa in metastatic castration-sensitive prostate cancer patients not receiving docetaxel chemotherapy (HR 0.49, p=0.007). If this evidence shifts physician prescribing patterns, Nubeqa's market share growth could slow, directly impacting Orion's royalty income trajectory.

Investors should track quarterly Nubeqa sales data from Bayer results, Erleada market share evolution in relevant patient populations, any Bayer pricing actions linked to MFN policy compliance, and pipeline progress on ODM-212 and other candidates that could reduce Orion's dependence on a single royalty stream.