Why Orion Stock Fell 4.3% Despite 47% Profit Growth in Q1

12 mins ago

A 17.8% revenue surge and 47% profit expansion would typically send shares climbing, yet Orion Corporation’s stock dropped 4.3% following its Q1 2026 earnings release on 23 April 2026. The Finnish pharmaceutical company has been one of Europe’s standout performers, rallying 52.64% since the beginning of 2025 on the strength of its prostate cancer drug Nubeqa. This quarter’s results continued that operational momentum, with the company raising its full-year guidance in response to what management described as “a solid start of the year.”

This analysis examines why markets punished strong results, what the 47% cash flow decline reveals about earnings quality, and whether Orion’s current valuation leaves room for further appreciation.

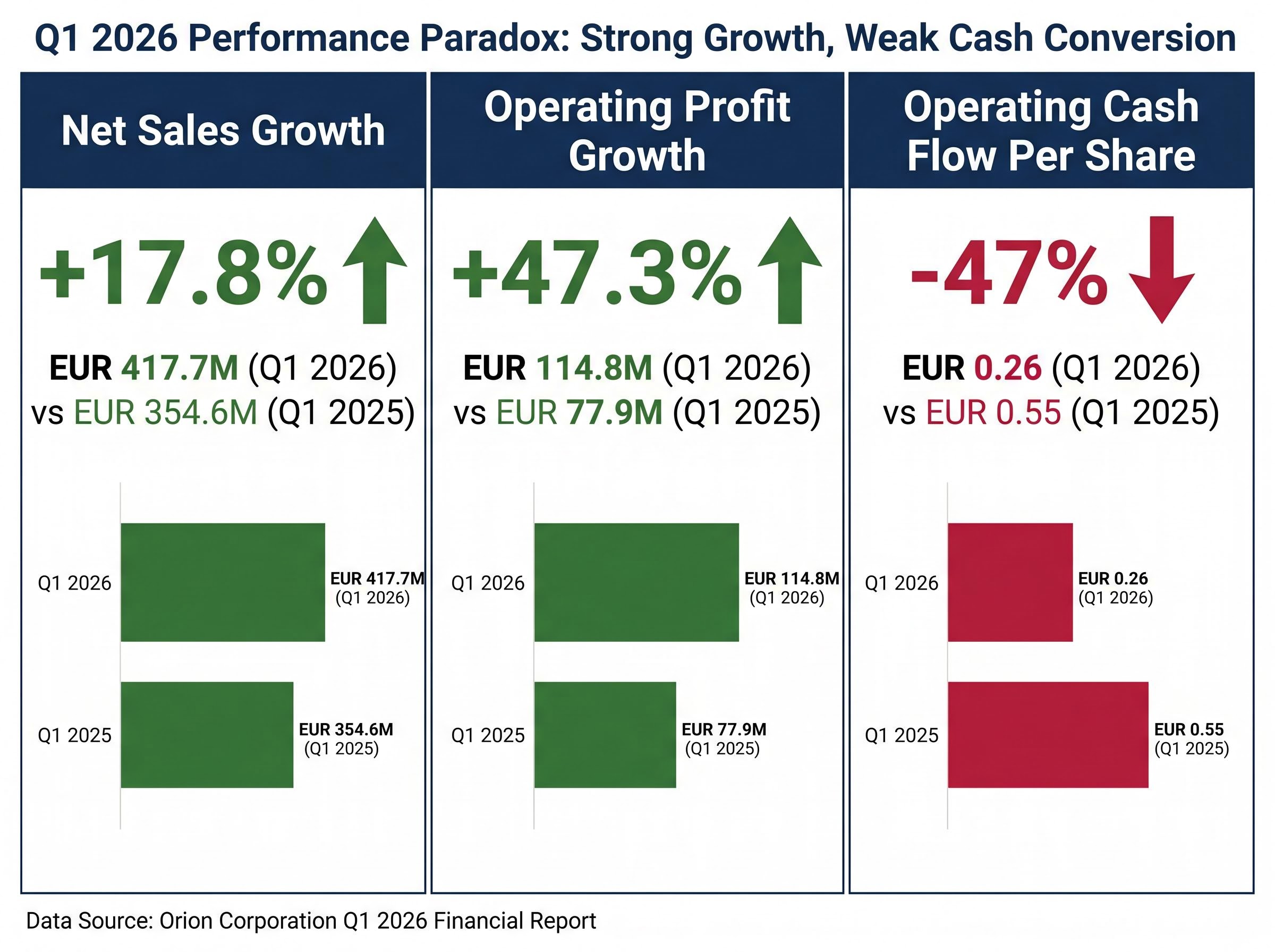

Orion Corporation reported Q1 2026 results at noon EEST on 23 April that demonstrated substantial operating leverage across the business. Net sales reached EUR 417.7 million, up 17.8% from EUR 354.6 million in the prior-year quarter. Operating profit surged to EUR 114.8 million, representing 47.3% growth from EUR 77.9 million in Q1 2025. Basic earnings per share improved to EUR 0.64 compared to EUR 0.44 a year earlier.

The revenue growth reflected underlying commercial execution rather than episodic contractual windfalls. Milestone payments contributed just EUR 0.5 million to Q1 2026 net sales, down from EUR 1.1 million in the prior-year quarter, indicating that the 17.8% top-line expansion was driven by sustained Nubeqa momentum and broader portfolio gains rather than one-time milestone receipts.

Management characterised all business segments as “performing robustly, contributing to our growth trajectory.” The raised full-year guidance (net sales EUR 1,950-2,100 million from EUR 1,900-2,100 million previously, operating profit EUR 600-750 million from EUR 550-750 million) reflected confidence that the quarter’s operational strength would persist through the remainder of 2026.

| Metric | Q1 2026 | Q1 2025 | Year-on-Year Change |

|---|---|---|---|

| Net Sales | EUR 417.7M | EUR 354.6M | +17.8% |

| Operating Profit | EUR 114.8M | EUR 77.9M | +47.3% |

| Basic EPS | EUR 0.64 | EUR 0.44 | +45.5% |

| Milestone Payments | EUR 0.5M | EUR 1.1M | -54.5% |

These results confirm that Nubeqa’s commercial trajectory and broader portfolio gains are translating into meaningful profit expansion, validating the investment thesis that drove the 52.64% rally.

The quarter’s headline strength carried a discordant note that explains the market’s scepticism. Operating cash flow per share contracted 47% to EUR 0.26 from EUR 0.55 in Q1 2025, even as operating profit surged 47.3%. Strong earnings growth that failed to convert into cash raises questions about the sustainability of reported profitability and the timing uncertainty around royalty receipts.

The divergence between Orion’s 47% profit growth and 47% cash flow contraction highlights the importance of KPI-based earnings quality assessment, where investors screen beyond headline EPS to identify the single operational metric (in this case, operating cash flow per share) most likely to reveal sustainability concerns before they manifest in share price corrections.

The company acknowledged that collaboration agreements with pharmaceutical partners often include variable payments that “can significantly fluctuate year-on-year” with timing and magnitude “only known post-study completion.” This introduces material uncertainty around when reported royalty income actually converts into collected cash.

“Collaboration agreements can significantly fluctuate year-on-year. The timing and magnitude of these payments is only known post-study completion.”

When earnings surge but cash flow contracts, investors must question whether reported profitability reflects sustainable business performance or timing-related accounting that may reverse in future quarters. The 47% cash flow decline suggests that some portion of Q1’s strong earnings growth was deferred in terms of actual cash collection, creating a gap between accounting profit and economic reality.

Understanding royalty-based pharmaceutical revenue models helps investors distinguish between genuine cash flow concerns and predictable quarterly volatility inherent to pharmaceutical partnership structures, where reported earnings and cash flow often diverge due to contractual payment timing lags.

Pharmaceutical royalty structures create predictable divergence between reported earnings and cash flow that investors must understand to assess earnings quality properly. The mechanics work through a three-step process:

Milestone payments introduce additional volatility. These contractual payments are triggered by specific clinical, regulatory, or commercial achievements (trial completion, regulatory approval, sales thresholds). Orion received EUR 183 million in total milestone payments during 2025, creating lumpy cash flow patterns that do not repeat predictably.

Critically, the company’s 2026 guidance explicitly excludes material milestone payments, establishing a baseline where profitability growth must come from sustained Nubeqa commercial momentum rather than episodic contractual windfalls. Management stated that “the single biggest factor influencing the level of net sales and operating profit is Nubeqa, the net sales of which are expected to continue to grow strongly in 2026.”

Understanding these mechanics helps investors distinguish between genuine cash flow concerns and predictable quarterly volatility inherent to pharmaceutical partnership structures. The Q1 divergence may reflect normal royalty timing lags rather than fundamental business deterioration.

Orion’s stock declined 4.3% on the day of the earnings release despite strong operational results, reflecting rational profit-taking after extended appreciation rather than rejection of fundamentals. The shares had rallied 52.64% since the beginning of 2025 and climbed 61.5% from the 2025 low to the 2026 high, trading in a range of EUR 73.45-75.30 through mid-April 2026.

Analyst consensus sits at a “Moderate Buy” rating with an average twelve-month price target of EUR 74.17, representing only approximately 15% upside from current trading levels in the EUR 73-75 range. When a stock has already appreciated 52.64%, even genuinely strong earnings may fail to push shares higher because expectations have reset to a higher baseline.

Analyst Consensus Rating: Moderate Buy Average Price Target: EUR 74.17 Implied Upside: Approximately 15%

The negative market reaction reflected four interconnected factors:

This pattern has precedent. Orion’s stock fell 7.99% in Q3 2025 despite strong quarterly results, suggesting a recurring dynamic where positive operational performance meets sceptical market reception at elevated valuations.

Nubeqa represents the foundational driver of Orion’s financial performance and future prospects, creating both substantial opportunity and material vulnerability. The company estimates that annual Nubeqa net sales (comprising tablet sales to commercial partner Bayer plus royalty income from Bayer’s global commercialisation) have the potential to exceed EUR 1 billion annually, though achievement depends on “various changing conditions such as the regulatory environment, market environment and indication of the product.”

The European Commission approved darolutamide in combination with androgen deprivation therapy for advanced prostate cancer on 21 July 2025, specifically for metastatic hormone-sensitive prostate cancer (mHSPC). This approval was based on the Phase III ARANOTE trial, which demonstrated a 46% reduction in the risk of radiological progression or death versus placebo plus androgen deprivation therapy. Nubeqa is now approved in more than 85 markets worldwide, reflecting broad geographic presence and ongoing market expansion.

The ARANOTE Phase III trial published in the Journal of Clinical Oncology reported a hazard ratio of 0.54 (95% CI, 0.41 to 0.71; P < .0001) for darolutamide plus androgen deprivation therapy versus placebo, establishing the evidentiary basis for the European Commission's mHSPC approval decision in July 2025.

The drug is showing strong uptake in triplet therapy combinations that incorporate darolutamide with androgen deprivation therapy and chemotherapy as an established new standard of care in mHSPC. This paradigm shift toward combination approaches expands the addressable market for advanced therapeutics in this setting.

The competitive landscape in advanced prostate cancer therapeutic development has intensified as Nubeqa expands into mHSPC indications while competitors like Clarity Pharmaceuticals advance radiopharmaceutical approaches such as 67Cu-SAR-bisPSMA, creating a multi-modal treatment paradigm that extends beyond androgen receptor inhibitors.

| Product | 2023 Global Sales | Patent Expiration | Key Developments |

|---|---|---|---|

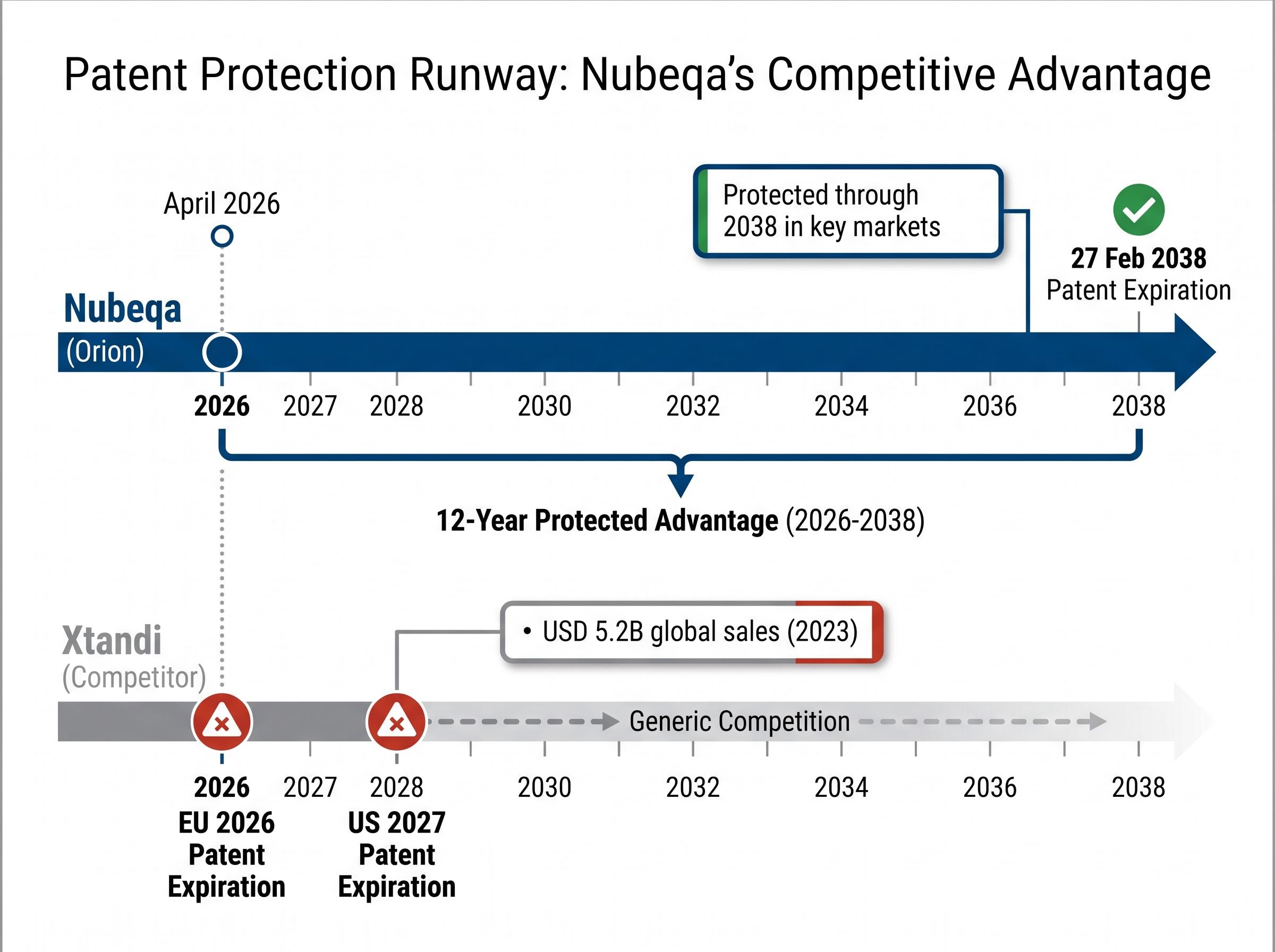

| Nubeqa (Orion) | Growing (royalty-based) | 2032-2038 | EU approval for mHSPC (July 2025) |

| Xtandi (Competitor) | USD 5.2B | EU 2026 / US 2027 | Facing imminent patent cliff |

Nubeqa’s competitive positioning benefits from extended patent protection and regulatory momentum while the dominant competitor Xtandi faces imminent generic competition with European patent expiration in 2026 and U.S. patent expiration projected for 2027. Xtandi generated USD 5.2 billion in global sales in 2023, indicating the substantial market Nubeqa is positioned to capture as physicians transition patients away from generic enzalutamide to differentiated branded alternatives.

Patents for darolutamide are expected to expire between 2032 and 2038, with a specific expiration date of 27 February 2038 in key jurisdictions including the United States. This represents approximately twelve years of future patent protection from April 2026, providing a prolonged runway for continued commercial growth and royalty generation before facing potential generic competition.

However, the extreme concentration of business outlook on a single product creates substantial risk. The company explicitly states that Nubeqa is “the single biggest factor” influencing financial performance. Any disruption to Nubeqa’s commercial trajectory (introduction of superior competing products, emergence of unexpected safety signals, pricing pressures, or market access challenges) would materially impact consolidated financial performance with limited offset from alternative revenue streams.

Investors must accept that this concentration amplifies both upside and downside scenarios. Nubeqa’s success drives exceptional growth, but dependence on a single product creates vulnerability that cannot be diversified away within Orion’s current portfolio structure.

For readers wanting to understand how pharmaceutical companies transition from development-stage cash burn to sustainable profitability, our comprehensive walkthrough of single-product pharmaceutical profitability models examines how Clinuvel achieved 9.5 consecutive years of profitability with a single commercial asset, including cash flow conversion rates, capital allocation discipline, and the specific financial metrics that distinguish durable business models from temporary milestone-driven earnings.

External forces beyond Orion’s operational control create headwinds that compound the challenges of sustaining the 52.64% rally. Currency dynamics represent a material pressure point. EUR/USD exchange rate forecasts project the euro at 1.14 over a three-month horizon and 1.20 over twelve months, with currency analysts noting the dollar is expected to “remain strong as long as the uncertainty in the Middle East remains high.”

A strong dollar creates translation headwinds for European pharmaceutical companies that derive significant revenue in U.S. dollar-denominated markets (particularly Nubeqa royalties from Bayer’s U.S. commercialisation) while reporting consolidated results in euros. Dollar-denominated sales translate into fewer euros when consolidated, mechanically reducing reported revenue and earnings metrics independent of underlying commercial performance.

The Nordic pharmaceutical sector faces distinct pressures. Danish pharma stocks, particularly Novo Nordisk and Genmab, experienced declines of 23-38% in recent periods, creating negative sentiment spillover across regional pharmaceutical equities. The Morningstar Finland Index significantly outperformed broader Nordic and global indices through April 2026, with dramatic Finnish market gains making Finnish equities, including pharmaceutical stocks, relatively expensive on absolute valuation grounds.

Broader macroeconomic conditions intensify the challenging backdrop:

The European Central Bank maintained its deposit facility rate at 2.0% as of April 2026, explicitly citing ongoing Middle East conflict as creating “upside risks for inflation and downside risks for economic growth.” ECB projections for 2026 indicate euro area headline inflation of 2.6% (revised upward, specifically attributed to elevated energy prices) and GDP growth of just 0.9% (revised downward), creating a stagflationary backdrop that particularly pressures equity valuations.

The ECB’s March 2026 monetary policy statement projecting 2.6% inflation and 0.9% GDP growth explicitly attributed upward inflation revisions to elevated energy prices stemming from ongoing Middle East conflict, illustrating how geopolitical tensions create stagflationary pressures that weigh on equity valuations across European pharmaceutical companies regardless of operational performance.

Even companies executing well operationally face challenges when currency dynamics reduce reported earnings and sector sentiment weighs on comparable valuations.

Orion Corporation’s Q1 2026 earnings demonstrate genuine operational strength, with Nubeqa driving the commercial momentum that has propelled the stock 52.64% higher since early 2025. Net sales grew 17.8%, operating profit expanded 47.3%, and management raised full-year guidance in response to what they characterised as “a solid start of the year.” These results validate the investment thesis around Nubeqa’s commercial trajectory and the company’s ability to convert drug development success into meaningful profit expansion.

However, the 47% cash flow decline, elevated valuations offering limited upside to analyst targets of EUR 74.17, and extreme concentration on a single product explain why markets responded with scepticism rather than enthusiasm. The 4.3% post-earnings decline reflected rational profit-taking after a 52.64% rally rather than rejection of fundamental business quality.

For long-term investors, Orion’s fundamental quality remains intact. Nubeqa is a proven commercial asset with twelve years of patent protection, expanding indications, and competitive positioning against rivals facing imminent generic threats from 2026-2027 patent expirations. The company’s raised guidance (net sales EUR 1,950-2,100 million, operating profit EUR 600-750 million) and commitment to increased research and development spending signal confidence in sustained momentum.

For tactical investors seeking near-term appreciation, current valuations at EUR 73-75 with only 15% upside to consensus targets suggest the easy gains have already been captured. The combination of cash flow quality concerns, single-product dependency, currency headwinds from euro strength versus the dollar, and Nordic pharmaceutical sector weakness of 23-38% creates a challenging backdrop for additional multiple expansion.

Investors should monitor quarterly cash flow patterns as indicators of earnings quality, pipeline progress with ODM-212 as evidence of long-term value creation beyond the Nubeqa franchise, and Nubeqa’s continued commercial execution in newly approved indications as validation of the EUR 1 billion annual sales potential management has outlined. The stock’s suitability depends on investment horizon: strategic holders benefit from a quality asset with extended runway, while tactical buyers face limited margin of safety at current valuations.

—

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Orion Corporation reported Q1 2026 net sales of EUR 417.7 million, up 17.8% year on year, with operating profit surging 47.3% to EUR 114.8 million and basic earnings per share rising to EUR 0.64 from EUR 0.44 in the prior year.

Despite strong operational results, Orion's stock fell 4.3% because the shares had already rallied 52.64% since early 2025, operating cash flow per share contracted 47%, and analyst consensus targets of EUR 74.17 implied limited additional upside from current trading levels.

Nubeqa is Orion's prostate cancer drug, commercialised globally by Bayer, and it is the single largest driver of the company's revenue and profit growth, with management estimating annual Nubeqa net sales have the potential to exceed EUR 1 billion and patent protection extending to 2032-2038.

Royalty revenue is recognised when a commercial partner reports sales, but the actual cash transfer can lag by one or more quarters under contractual payment terms, creating a predictable divergence between reported earnings and operating cash flow that investors must account for when assessing earnings quality.

Following its Q1 2026 results, Orion raised its full-year guidance to net sales of EUR 1,950-2,100 million and operating profit of EUR 600-750 million, with management citing Nubeqa's continued commercial momentum as the primary growth driver.