Palantir just delivered its fastest revenue growth since its 2020 IPO, 85% year-over-year, and the stock fell 7% on the news. That single session erased roughly $26 billion in market capitalisation. The reaction was not a puzzle. It was a message. After peaking near 100 times forward revenue in late 2025, Palantir trades at approximately 40 times forward revenue and 116.78 times forward earnings as of May 2026, even after a roughly 33% pullback from its all-time high. The business may be exceptional. The question is whether the price is. What follows is an examination of what the valuation numbers mean in context, what history says about buying stocks above 30 times revenue, what bull and bear scenarios look like over a five-year horizon, and why Michael Burry is short despite a near-perfect earnings print.

The paradox at the heart of Palantir’s stock price

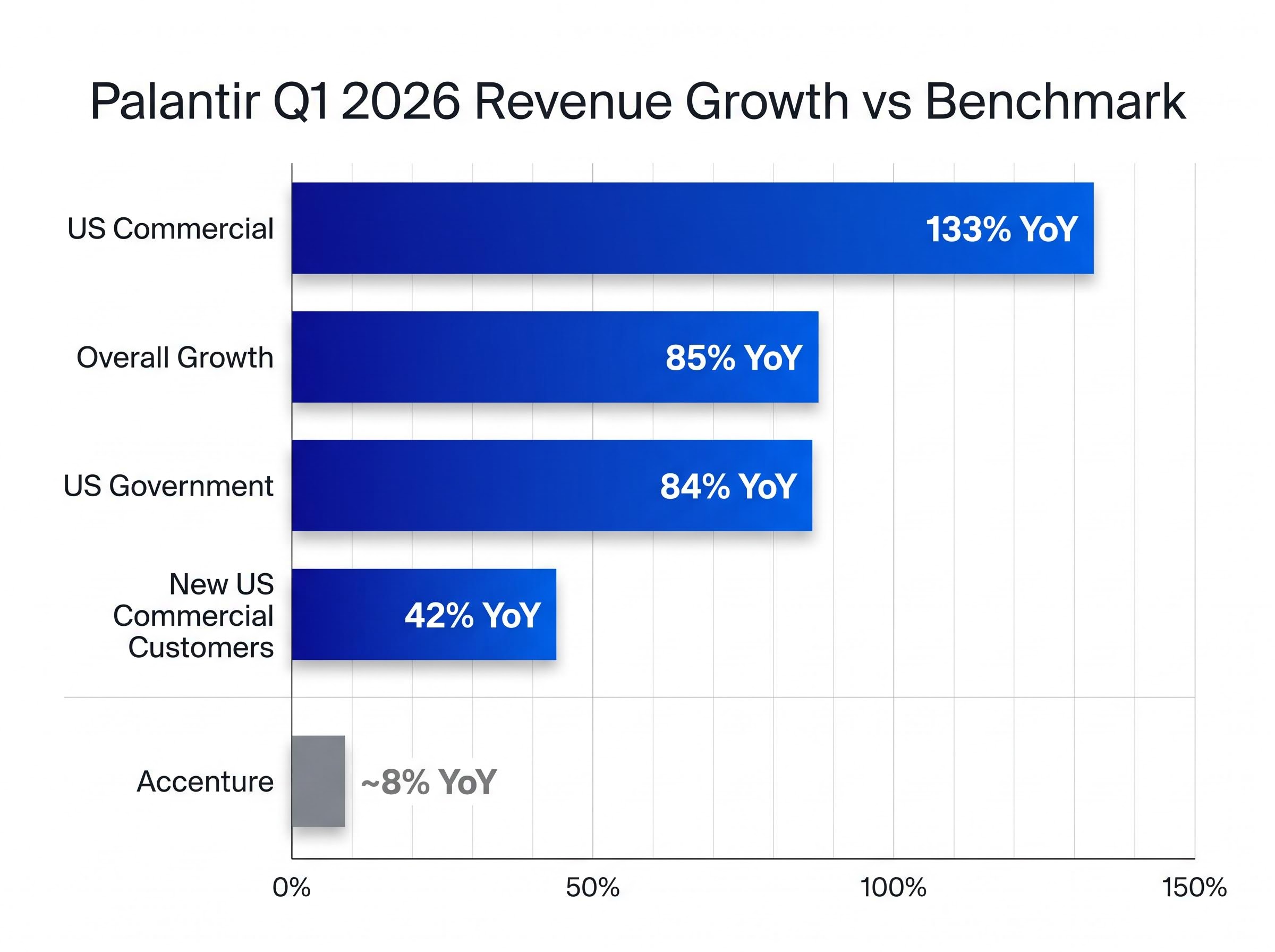

Q1 2026 revenue came in at approximately $1.6 billion, up from roughly $800-$900 million a year earlier. Growth of 85% year-over-year marked the fastest pace since the IPO. Management raised full-year 2026 guidance to $7.65 billion.

The Palantir Q1 2026 investor relations release confirmed revenue of $1.633 billion, up 85% year-over-year, alongside a raised full-year 2026 revenue guidance implying 71% growth, making it the primary source for the financial figures that underpinned the market’s reaction.

The market’s response was to sell the stock down approximately 7% in a single session, wiping out roughly $26 billion in market capitalisation. The earnings were not the problem. The price was.

The Q1 2026 earnings results reported adjusted EPS of $0.33, beating consensus by 17.86%, alongside a Rule of 40 score of 145, a level management compared only to NVIDIA, Micron, and SK hynix among public technology companies.

A stock can belong to a genuinely strong company and still present poor risk-adjusted returns if the entry price already embeds years of future execution. That tension sits at the centre of every valuation debate around Palantir today.

What the analyst range reveals

The spread of analyst price targets captures this disagreement in a single data point.

The lowest 12-month price target sits at $45, implying more than 65% downside from current levels. The consensus target is approximately $191-$194. Both figures are produced by professional analysts using internally consistent frameworks.

A range of $45 to $230 is not standard analytical disagreement. It reflects two completely different models for valuing a high-growth AI platform business. Approximately 2 sell ratings sit alongside 17 buy ratings, with 10 holds in between. The consensus label of “moderate buy” conceals a distribution of views that could hardly be wider.

When big ASX news breaks, our subscribers know first

What Palantir actually does, and why the platform argument matters

Before stress-testing the valuation, the business itself deserves a full hearing. Palantir’s platform takes a fundamentally different approach to AI deployment than most enterprise software. Rather than layering a chatbot interface over existing systems, the company maps a client’s entire data architecture, workflows, and permissions to deploy AI agents that operate within the specific constraints of that organisation.

This “ontology” approach has found traction among institutions where AI deployment failures carry high costs: military logistics, energy infrastructure, healthcare systems, and financial risk management.

The distinction between surface-level enterprise AI adoption and infrastructure-level deployment is where Palantir’s platform argument rests; research projecting a 3x ROI gap between the two approaches by 2027 helps explain why clients embedding AI at the ontology layer are unlikely to replace the integration with a cheaper wrapper vendor after the initial optimisation uplift.

Concrete client outcomes illustrate the difference:

- GE Aerospace reported a 26% increase in engine manufacturing output through AI-driven supply chain analysis deployed on the platform

- AIG uses the platform for risk evaluation, policy pricing, and fraud detection across its insurance operations

- A telecom client processing 10 million annual service interactions shifted from using the platform for call centre replacement to proactive churn prevention, converting a cost-reduction play into a revenue retention tool

The revenue data confirms the platform is scaling across segments.

| Segment | YoY Growth Rate | Key Driver |

|---|---|---|

| US Commercial | 133% | AI platform adoption across enterprise clients |

| US Government | 84% | Expanded defence and intelligence contracts |

| New US Commercial Customers | 42% | Broadening client base beyond initial government-adjacent verticals |

For context, Accenture, one of the largest technology consulting firms globally, is growing at approximately 8%. Palantir’s US commercial segment is growing at roughly 133%. The gap is not incremental. Whether that gap justifies a 73.64 times trailing price-to-sales ratio is the question this analysis turns to next.

What history says about stocks trading above 30 times revenue

The historical base rate for stocks trading at extreme revenue multiples is not encouraging.

Research into companies that traded at or above 30 times revenue has found that they historically produce below-average investor returns over the subsequent five-year period. The mechanism is multiple compression: the valuation ratio declines faster than revenue expands, eroding the stock price even as the business grows.

This is not a valuation opinion. It is a statistical pattern. It does not mean every company at 30 times revenue delivers poor returns. It means the base rate is unfavourable, and an investor buying at that level needs the company to be an exception.

Palantir’s own valuation history illustrates how quickly multiples can move. The stock traded at approximately 7 times revenue during its 2023 trough. It climbed to approximately 100 times forward revenue by late 2025. It now sits at approximately 40 times forward revenue, with a trailing price-to-sales ratio of 73.64 times and a forward price-to-earnings ratio of 116.78 times.

Growth stock valuation compression has been unusually severe in 2026, with Morningstar data showing the category trading at a 21% discount to fair value, a level recorded less than 5% of the time since 2011, which provides the macro backdrop against which Palantir’s own multiple decline from 100x to 40x forward revenue should be read.

Among AI and software peers, that multiple stands out.

| Company | Forward P/E | Price/Sales (Trailing) | Comparability Note |

|---|---|---|---|

| Palantir | 116.78x | 73.64x | AI platform; government and commercial |

| Datadog | N/A | ~11x (NTM EV/Revenue) | Cloud monitoring; high-growth SaaS |

| Snowflake | ~180x | N/A | Data cloud; comparable growth profile |

| CrowdStrike | ~mid-70s | N/A | Cybersecurity; recurring revenue model |

Only Snowflake trades at a higher forward earnings multiple. On a price-to-sales basis, Palantir’s 73.64 times trailing ratio dwarfs the peer group. The question multiple compression poses is straightforward: can Palantir grow revenue fast enough for long enough to justify the current price before the multiple normalises toward software sector averages?

The short seller thesis: commoditisation, one-time optimisation, and Burry’s bet

The bearish case against Palantir is not a valuation-only argument. It identifies specific structural vulnerabilities in the business model. Three distinct threads run through the bear thesis:

- Commoditisation risk: The argument that Palantir may ultimately function as a wrapper around third-party large language models from OpenAI, Anthropic, or Google. If the underlying AI capability is commoditised, consulting firms could replicate the integration layer at lower cost, compressing Palantir’s pricing power.

- One-time optimisation concern: AI-driven transformations such as GE Aerospace’s supply chain improvement may represent a single step-change in efficiency rather than recurring value. After the initial uplift, cheaper vendors could handle ongoing maintenance, reducing Palantir’s long-term revenue per client.

- Valuation-anchored short thesis: Michael Burry has stated that Palantir is worth “well under $50” as of May 2026. The analyst low target of $45 provides independent corroboration of this extreme bearish anchor.

Palantir management has countered that the ontology layer and deep data architecture integration make replication significantly harder than a model-wrapper thesis implies. Whether that defence holds against rapid commoditisation of the underlying AI models remains an open question.

Why Burry stayed short after the earnings beat

Burry opened an outright short position ahead of Q1 2026 earnings and maintained it after Palantir reported 85% revenue growth and raised guidance. That decision carries information.

A short seller who holds conviction after strong earnings is not betting on business deterioration. The bet is on multiple compression: that the stock’s valuation will contract faster than the business can grow into it. The signal is that Burry views the price, not the product, as the vulnerability.

Mapping five-year return potential across outcome scenarios

The most useful way to evaluate Palantir at current levels is to model what different outcomes imply for investor returns from a $137.80 entry price.

The methodology for valuing high-multiple stocks, including how to triangulate DCF analysis, TAM modelling, and comparable transaction frameworks when a company’s market capitalisation reflects a future business rather than current earnings, applies directly to the scenario arithmetic this analysis uses for Palantir.

| Scenario | 5-Year Profit Assumption | Terminal Multiple Applied | Implied Return from Current Price |

|---|---|---|---|

| Bull case | Profits grow from ~$3.5B to ~$11B | 50x earnings | ~60% total (~10% annualised) |

| Base case | Profits grow in line with guided trajectory | Multiple normalises toward software peers | Minimal appreciation |

| Bear case | Growth decelerates; margins stabilise | Multiple compresses toward 30-40x earnings | Substantial valuation correction |

In the bull case, assuming near-perfect execution with profits tripling to approximately $11 billion over five years and a terminal multiple of 50 times earnings, the implied total return from current levels is approximately 60%, or roughly 10% annualised.

That arithmetic is the core of the valuation challenge. The bull case does not require anything to go wrong. It assumes sustained 60-plus percent revenue growth (management has guided 61% for 2026), continued margin expansion, and a terminal multiple that remains well above the broader software sector average. Even then, the return is moderate relative to the risk of multiple compression.

The base and bear cases do not require business failure. They require only that the valuation multiple normalises toward the range where most mature software companies trade. Full-year 2026 revenue guidance of $7.65 billion implies approximately 71% year-over-year growth, a figure the bull camp cites as proof the premium is warranted. The question is whether that growth rate can compound for five consecutive years at a pace that outpaces the multiple’s likely decline.

Great company, dangerous price: the decision investors actually face

The all-time high closing price of $207.18 was reached on 3 November 2025. The current price of approximately $137.80 represents a decline of roughly 33% from that peak and approximately 20-25% year-to-date. The stock’s recovery from roughly 7 times revenue in 2023 to 40 times forward revenue today reflects the compounding of narrative premium around AI adoption.

For the bull case to deliver acceptable returns from current levels, three conditions would need to hold simultaneously:

- Revenue growth sustained above 60% annually for multiple years, well beyond the typical deceleration curve for high-growth software

- Margin expansion continuing as the revenue base scales, converting top-line growth into earnings power

- The valuation multiple holding above software sector averages rather than compressing toward peer norms

A forward price-to-earnings ratio of 116.78 times is the practical hurdle any new buyer must clear through earnings growth alone.

The cost basis question

An investor who bought Palantir at $20-$30 during the 2023 trough faces a completely different risk and reward profile than one entering at $137 today. The existing holder has a substantial margin of safety built into the position. The new buyer has none.

Portfolio management decisions for existing holders, whether to trim, hold, or add, involve different considerations than the initial entry decision. The analysis above applies most directly to investors evaluating a new position at current prices.

The question this analysis has built toward is not whether Palantir is a strong company. The earnings data, the client outcomes, and the revenue trajectory all point to genuine platform differentiation. The question is whether that quality is already fully reflected in a stock trading at 116.78 times forward earnings, and what happens to investor returns if the market decides the answer is yes.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. Forward-looking statements regarding revenue growth, profit trajectories, and valuation scenarios are speculative and subject to change based on market developments and company performance.

—