Vanguard VIHY Declares First Distribution at 49.49 Cents per Unit

2 hrs ago

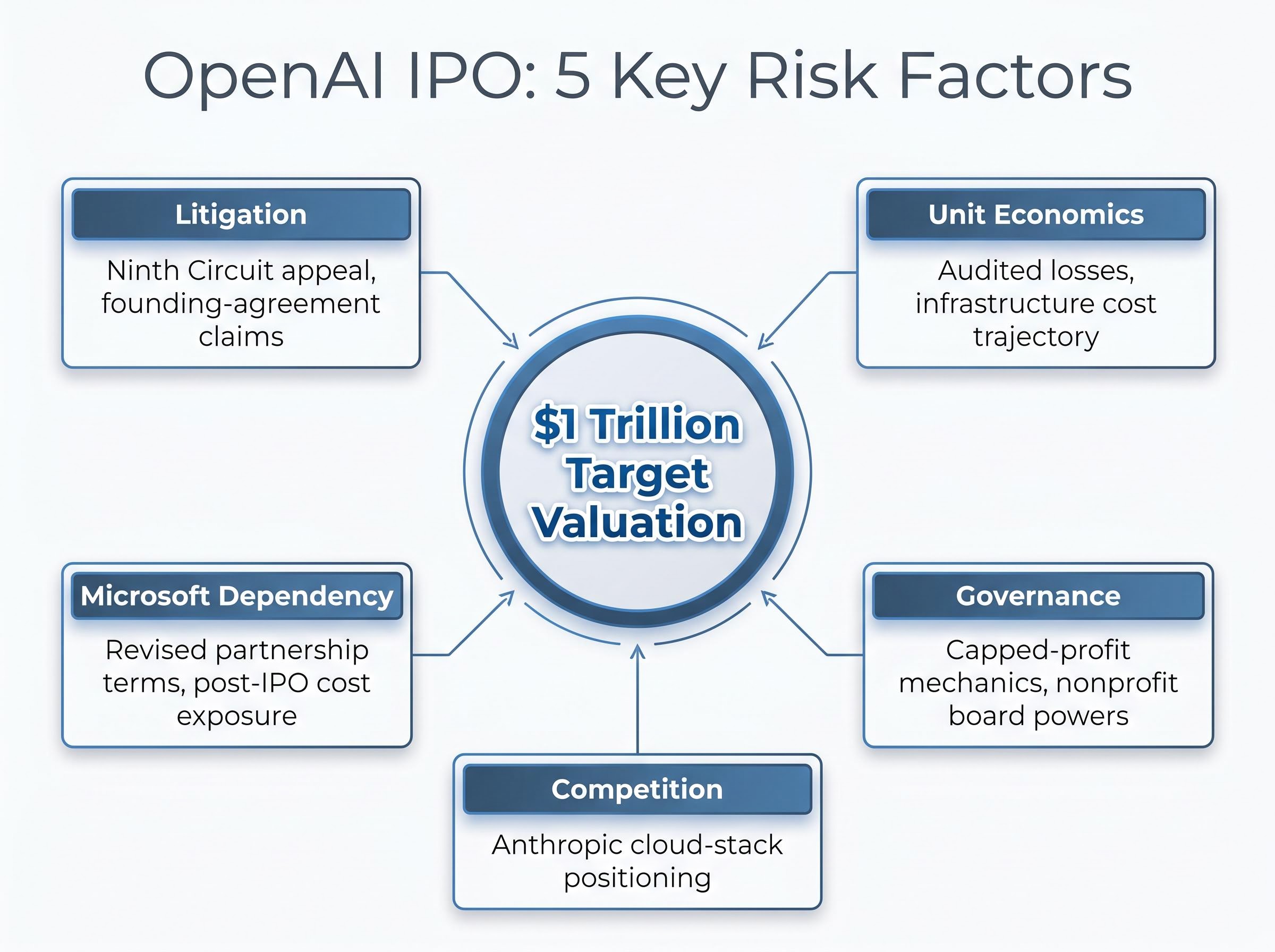

OpenAI is weeks away from filing a confidential IPO registration with regulators, yet the company cannot tell prospective shareholders what it costs to stay at the frontier, how long its losses will continue, or what legal claims may follow it onto the exchange. With Goldman Sachs and Morgan Stanley drafting the prospectus and a September 2026 market debut in range, the offering is moving fast. Speed, however, does not dissolve the risk factors accumulating around it: an active litigation threat, a unit-economics story that even bullish analysts describe as strained, a governance structure with no clean public-market precedent, and a competitor in Anthropic that is closing the enterprise gap faster than most observers expected. What follows is a breakdown of the five risk categories investors need to interrogate before the prospectus lands, drawing on the latest available data on OpenAI’s financials, the Musk litigation outcome, and the competitive dynamics reshaping enterprise AI in 2026.

The verdict arrived on 18 May 2026, and for OpenAI, the headline was clean: a unanimous jury ruling against Elon Musk in U.S. District Court in Oakland, before Judge Yvonne Gonzalez Rogers. The finding should have been the line investors wanted to read.

It was not a merits-based dismissal. The jury ruled on statute-of-limitations grounds, finding that Musk had waited too long to bring his claims. The substantive questions at the centre of the dispute, founding agreements, mission integrity, IP practices, were never adjudicated. In procedural terms, that distinction matters: a limitations ruling leaves the underlying legal arguments untouched.

Musk and his counsel announced their intent to appeal to the Ninth Circuit on 18-19 May 2026. No appeal has been filed or heard as of 20 May 2026, but the window now overlaps directly with the IPO timeline.

The litigation history underscores how far the case has travelled:

A statute-of-limitations ruling leaves the substantive founding-agreement claims unadjudicated. For institutional due-diligence teams, this case remains unresolved regardless of the trial outcome.

Any negative development at the Ninth Circuit could re-inject governance and IP uncertainty into a company seeking a valuation approaching $1 trillion.

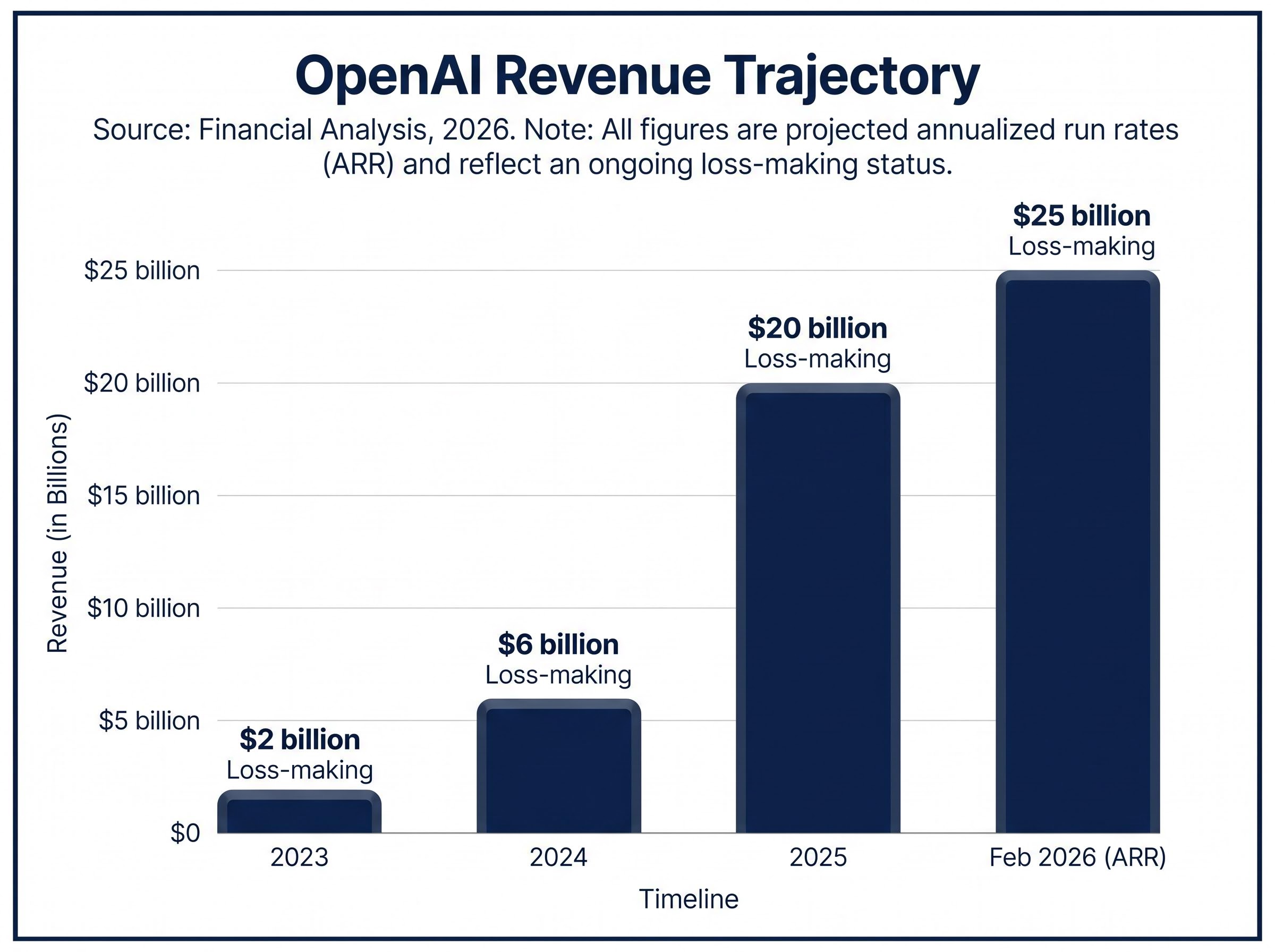

The revenue trajectory is real and it is striking. OpenAI generated approximately $2 billion in 2023, roughly $6 billion in 2024, and approximately $20 billion for the full year 2025. By February 2026, the annualised revenue run rate had reached approximately $25 billion, according to reporting from The Information and Sacra estimates via Reuters. That growth rate, roughly 6-7x over three years, has few parallels in enterprise software history.

Then the cost side arrives. Training frontier models requires multi-billion-dollar compute clusters and continuous reinvestment. Inference at scale, serving hundreds of millions of ChatGPT users and enterprise API customers, remains expensive. Each model generation demands another capital commitment with no natural plateau. Revenue growth at this pace is necessary, but it is not sufficient.

AI infrastructure capital commitments across the four major hyperscalers reached $130 billion in Q1 2026 alone, with full-year combined projections at $725 billion, a spending environment that contextualises why OpenAI’s training and inference costs show no sign of plateauing and why the company’s multi-billion-dollar compute clusters represent ongoing rather than one-time capital exposure.

| Year | Approximate Revenue | Status |

|---|---|---|

| 2023 | $2 billion | Loss-making |

| 2024 | $6 billion | Loss-making |

| 2025 | $20 billion | Loss-making |

| Feb 2026 (ARR) | $25 billion | Run-rate estimate; loss-making |

Two data gaps sit at the centre of the financial picture. No audited operating loss figure has been made publicly available for 2025 or 2026. The revised Microsoft-OpenAI financial terms, including cloud exclusivity length and equity adjustments, have not been disclosed. Microsoft Azure provides the underlying infrastructure, with OpenAI incurring usage-based costs rather than standalone capital expenditure, but the precise post-IPO cost exposure under those terms remains opaque.

No audited operating loss figure and no disclosed Microsoft partnership terms create a known blind spot in the IPO prospectus. At a valuation approaching $1 trillion, that opacity is not an administrative detail.

Analysts continue to characterise OpenAI’s economics as strained relative to its infrastructure burden. A valuation of this magnitude demands extraordinary forward multiples, and without a disclosed path to operating profit, investors are being asked to price a business whose cost structure is partially hidden behind a partnership agreement that has not been made public.

OpenAI does not operate like a standard technology company. It was founded as a nonprofit, and its commercial entity operates under a nonprofit governance overlay. Investor returns are subject to a cap rather than the unconstrained equity upside that public-market shareholders typically expect from technology IPOs. The nonprofit board retains authority over mission-aligned decisions, creating a structural layer between shareholder interests and commercial strategy that has no clean precedent in public markets.

For retail investors unfamiliar with the model: in a conventional IPO, common shareholders own equity that rises or falls with the company’s performance, with no predetermined ceiling on returns. OpenAI’s capped-profit structure places a limit on how much investors can earn. The nonprofit board can, in principle, override commercial decisions if they conflict with the organisation’s stated mission. That dual authority has been a consistent concern in analyst commentary throughout 2025 and 2026.

The nonprofit board authority question is not the only governance overhang investors must assess before the prospectus lands; the Altman conflict-of-interest probe, launched by the House Oversight Committee in May 2026, adds a second layer of congressional scrutiny to a governance structure that has no clean public-market precedent.

Reporting from The Information indicates OpenAI is actively making governance and reporting changes to support the IPO. Analysts question whether incremental adjustments will satisfy institutional investors without full structural transparency. Three disclosure questions are expected to face intense pressure during the roadshow:

Investors who have participated in standard technology IPOs should recognise that these questions have no analogues in prior offerings. The prospectus will need to explain how shareholder interests are protected within a governance model that was never designed for public markets.

Model benchmarks still favour OpenAI in several categories. That is not where the competitive threat is sharpest. Enterprise CIOs selecting AI infrastructure increasingly make decisions at the cloud-stack level, not the model level, and Anthropic has positioned itself on both sides of the non-Microsoft cloud ecosystem.

Amazon Web Services invested up to $4 billion in Anthropic and designated it the preferred foundation model for Amazon Bedrock. Google Cloud also resells Anthropic’s Claude models. That twin-cloud distribution means enterprise buyers already committed to AWS or Google infrastructure can adopt Anthropic without switching platforms. Named adopters in industry coverage include JPMorgan Chase, SAP, and multiple enterprise software providers integrating Claude via cloud platforms.

Anthropic’s revenue trajectory reflects the structural advantage. Bloomberg reporting placed the company’s annualised revenue run rate at approximately $850 million by late 2024, up from approximately $100 million earlier that year. Analyst assessments consistently describe Anthropic as gaining ground in regulated and safety-sensitive enterprise segments, where constitutional AI positioning and native cloud data governance controls are differentiators.

Anthropic enterprise revenue growth accelerated sharply through early 2026, with run-rate revenue surpassing $30 billion by April 2026 and the number of enterprise customers spending over $1 million annually doubling to 1,000, figures that materially narrow the revenue gap cited in earlier competitive assessments.

OpenAI is categorised as part of the Microsoft stack. Anthropic occupies the AWS and Google stack. The competitive outcome in enterprise may be determined less by which company ships the best model and more by which cloud sales motion reaches the CIO first.

| Dimension | OpenAI | Anthropic | Implication |

|---|---|---|---|

| Primary cloud partner | Microsoft Azure | AWS / Google Cloud | Anthropic reaches two of the three hyperscalers |

| Revenue scale (latest) | ~$25B ARR | ~$850M ARR (late 2024) | Gap narrowing rapidly in enterprise |

| Enterprise positioning | Broad consumer + enterprise | Safety-sensitive, regulated segments | Anthropic owns a defensible niche |

| Key risk | Microsoft dependency | Scaling beyond niche | Cloud lock-in shapes both trajectories |

For investors assessing OpenAI’s long-term pricing power, this dynamic is the most structurally important competitive risk. Enterprise share could be allocated by platform bundling and cloud lock-in rather than model performance.

Investors wanting to map the cloud-stack competitive dynamics in detail will find our full explainer on Q1 2026 hyperscaler earnings, which covers Google Cloud’s 63% year-over-year growth, AWS’s $364 billion backlog surge, and a Goldman Sachs warning about profit distortion from equity gains, providing the quantitative foundation for assessing how Anthropic’s dual-cloud positioning is translating into commercial outcomes.

OpenAI’s strategic response has moved along three tracks, each addressing a distinct competitive pressure:

The Microsoft relationship provides global distribution reach through Azure AI, Office 365 Copilot, GitHub Copilot, and Azure AI Studio. It also provides capex support that OpenAI could not replicate independently. The cost is strategic dependence: if partnership terms shift unfavourably post-IPO, OpenAI faces sharply higher infrastructure costs or reduced distribution reach, and the full revised terms remain undisclosed.

Notably, no major sector-specific enterprise deals analogous to the AWS-Anthropic arrangement have been confirmed for OpenAI in healthcare, finance, or manufacturing as of May 2026. Tech industry media report speculation about vertical-industry partnerships, but nothing of comparable scale has been publicly announced.

Analysts characterise the governance changes underway as potentially insufficient without full transparency on the capped-profit economics and Microsoft relationship terms.

The gap between tactical responses and the structural transparency institutional investors require is where the prospectus will face its hardest scrutiny.

The arithmetic is straightforward. OpenAI’s most recent funding round closed at a post-money valuation of approximately $852 billion, with $122 billion in committed capital, according to Reuters and Bloomberg reporting. The IPO target is up to $1 trillion. Against an annualised revenue run rate of approximately $25 billion and confirmed ongoing losses, that implies a revenue multiple of approximately 40x.

OpenAI’s $852 billion private valuation has also drawn institutional attention through the Microsoft equity stake it implies: Bill Ackman’s Pershing Square disclosed a high-conviction Microsoft position in February 2026 specifically on the basis that Microsoft’s roughly 27% economic interest in OpenAI is unrecognised in the current stock price, a bull-case argument that sits in direct tension with the governance and cost-structure risks the prospectus must address.

For that multiple to hold in public markets, investors need a credible path to profit margins that frontier AI economics have not yet demonstrated. Training costs show no sign of plateauing. Inference costs remain high at scale. Pricing power faces compression from Anthropic, Google’s Gemini, and Meta’s open-source LLaMA ecosystem. A 40x revenue multiple on a loss-making business requires conviction that the margin story will arrive; the prospectus is where that conviction must be built or abandoned.

AI startup revenue multiple methodology at the frontier tier has consistently placed leading generative AI companies in the 35x to 50x range, well above traditional SaaS peers, a pricing convention that reflects anticipated margin expansion rather than demonstrated unit economics.

| Risk Factor | What the Prospectus Must Address |

|---|---|

| Litigation | Ninth Circuit appeal status, potential financial exposure, founding-agreement claims |

| Unit economics | Audited losses, infrastructure cost trajectory, timeline to profitability |

| Governance | Capped-profit mechanics, nonprofit board powers, shareholder return constraints |

| Competition | Enterprise retention metrics, switching costs, cloud-stack positioning vs. Anthropic |

| Microsoft dependency | Full revised partnership terms, post-IPO cost exposure, exclusivity duration |

Investors who do not receive clear answers to each item in the prospectus should treat that opacity as a pricing input, not an administrative detail.

The five risk clusters are distinct, but they converge on the same valuation:

This is not a question of whether OpenAI is a significant company. It is a question of whether the prospectus delivers the transparency required to price these risks at a $1 trillion valuation. Goldman Sachs and Morgan Stanley are expected to file the registration imminently, with the earliest market debut targeted for September 2026. That document will either resolve these risk questions or confirm they will follow the company onto the exchange.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in this analysis are subject to market conditions and various risk factors.

OpenAI operates under a nonprofit governance overlay that places a ceiling on investor returns, meaning public shareholders cannot earn unconstrained equity upside as they would in a conventional technology IPO. The nonprofit board also retains authority over mission-aligned decisions, creating a structural layer between shareholder interests and commercial strategy that has no clean precedent in public markets.

A unanimous jury ruled against Musk on statute-of-limitations grounds on 18 May 2026, but the underlying substantive claims regarding founding agreements and IP practices were never adjudicated. Musk announced his intent to appeal to the Ninth Circuit, meaning the litigation remains unresolved and overlaps directly with the IPO timeline.

Against an annualised revenue run rate of approximately $25 billion and confirmed ongoing losses, a $1 trillion valuation implies a revenue multiple of approximately 40x. Analysts note this requires conviction that frontier AI economics will eventually produce profit margins that have not yet been demonstrated.

Anthropic has secured investment and preferred model status with both Amazon Web Services and Google Cloud, meaning enterprise buyers already on AWS or Google infrastructure can adopt Anthropic's Claude without switching platforms. Named enterprise adopters include JPMorgan Chase and SAP, and Anthropic's annualised revenue run rate surpassed $30 billion by April 2026, materially narrowing the gap with OpenAI.

No audited operating loss figure has been made publicly available for 2025 or 2026, and the revised financial terms of the Microsoft partnership, including cloud exclusivity length and equity arrangements, have not been disclosed. At a valuation approaching $1 trillion, analysts describe this opacity as a material pricing concern rather than an administrative detail.