Nvidia’s Computex Keynote Must Answer 3 Questions to Hit $250

1 hr ago

On a day when the 30-year U.S. Treasury yield is trading above 5.1% for the first time since 2007 and the S&P 500 has posted its third consecutive daily loss, one company’s quarterly revenue figure is being treated as the most important data point in markets. Nvidia’s Q1 FY2027 earnings, scheduled for release at approximately 1:20 p.m. PT today, 20 May 2026, arrive at a moment of genuine fragility for U.S. equities. The AI-driven rally that pushed the Nasdaq and S&P 500 to record highs earlier this month is now under pressure from rising yields, oil-linked inflation concerns, and geopolitical uncertainty. What follows is an examination of what investors are watching in the report, why Nvidia’s numbers carry systemic weight far beyond a single company, and what the pre-earnings market setup reveals about the stakes.

Nvidia’s data centre segment revenue has become the primary real-world validation mechanism for the AI infrastructure spending thesis. The causal chain is specific and short:

Hyperscaler AI capital expenditure commitments for 2026 have reached approximately $725 billion in combined guidance across Amazon, Microsoft, Alphabet, and Meta, with $130 billion deployed in Q1 2026 alone, figures that give Nvidia’s data centre revenue line its systemic significance: any deceleration in that order flow would represent a reversal at a scale visible across the entire technology sector.

The record highs the Nasdaq and S&P 500 reached earlier in May were built partly on the expectation that today’s print would confirm the thesis. The S&P 500 fell approximately 0.67% and the Nasdaq Composite declined roughly 0.84% on Tuesday 19 May 2026, marking the third straight daily loss heading into the release. Nvidia shares dropped approximately 0.8% during Tuesday’s regular session.

That three-day pullback is not incidental. It reflects a market recalibrating ahead of a single data point, and the asymmetry of a disappointment is now larger than it was a week ago.

Pre-earnings reporting has framed the release as “a significant test for the durability of the broader AI-driven market rally.”

Not every line item in the report carries equal weight. The three metrics traders are monitoring, ranked by market sensitivity, are:

The Q1 FY2027 report covers the quarter ended 26 April 2026. This is a fiscal year distinction worth noting: Q1 FY2026 results were reported on 28 May 2025, nearly a year ago.

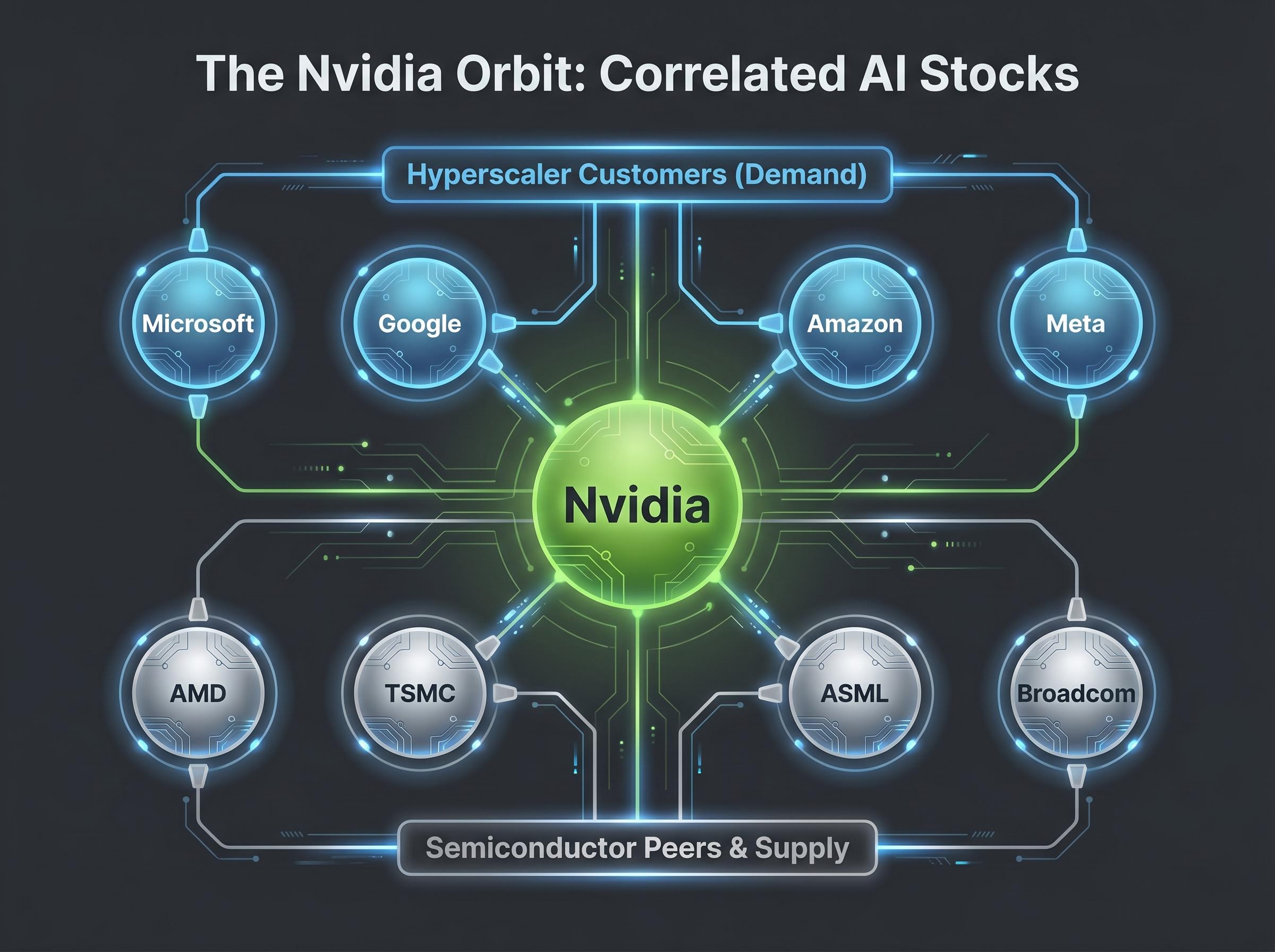

Management remarks on what Microsoft, Google, Amazon, and Meta are signalling about their AI infrastructure spending function as forward indicators that analysts treat as more valuable than any single quarter’s revenue. These hyperscalers represent Nvidia’s largest customers, and their capital expenditure commitments determine the revenue trajectory for multiple quarters ahead.

Any softening in hyperscaler language on today’s earnings call would be read as a demand headwind, even if the reported quarter itself was strong. The forward read is what reprices the stock.

Nvidia’s earnings are not landing in a vacuum. The yield environment alone changes the stakes.

Higher risk-free rates compress the present value of long-duration earnings streams, a mechanical effect that hits growth stocks like Nvidia disproportionately. When the 10-year U.S. Treasury yield reached an intraday peak of 4.69% on 19 May 2026, its highest intraday level since January 2025, it reinforced a structural headwind for technology valuations.

The 30-year Treasury yield dynamics driving today’s macro pressure are not isolated to a single session; the 5.25% threshold has been flagged by institutional strategists as the level at which allocators would be compelled to systematically reduce equity risk premia across diversified portfolios, a structural shift that would extend well beyond any single earnings event.

The 30-year U.S. Treasury yield has traded above 5.1%, a level not reached since 2007, underscoring the degree of pressure on long-duration equity valuations heading into the print.

The Federal Reserve’s April policy meeting minutes are also scheduled for release today, 20 May 2026, adding a second macro-level catalyst to an already crowded session.

| Macro pressure point | Current level (as of 19 May 2026) | Market implication |

|---|---|---|

| 10-year U.S. Treasury yield | 4.69% (intraday peak) | Highest since January 2025; compresses growth stock valuations |

| 30-year U.S. Treasury yield | Above 5.1% | First time since 2007; signals sustained long-end pressure |

| WTI crude oil futures | Around $103.80 | Elevated crude identified as inflation re-ignition risk |

| Fed April meeting minutes | Scheduled for release 20 May 2026 | Second macro catalyst on the same session; shapes rate expectations |

With Brent crude near $110.82, the inflation backdrop further constrains the Federal Reserve’s room to ease. The market’s tolerance for any guidance disappointment from Nvidia is lower than it would be in a falling-rate environment; a soft beat or cautious guidance could be punished more severely than the numbers alone would suggest.

What happens to Nvidia at 1:20 p.m. PT today will radiate through names that many investors hold without recognising the connection. AI-linked semiconductor and cloud infrastructure stocks trade as a correlated cluster around major Nvidia events, driven by shared exposure to the AI capital expenditure cycle and algorithmic trading of sector exchange-traded funds.

Tuesday’s session demonstrated this dynamic in real time. AI-linked companies, including cloud infrastructure providers and chip equipment manufacturers, declined alongside Nvidia before results were even known. Technology and semiconductor sectors were the primary drivers of the broader market retreat, with Nasdaq 100 futures declining roughly 0.2% to around 28,881.75 points as of 8:20 p.m. ET on 19 May 2026.

The capex-to-revenue lag across the semiconductor stack, estimated at 18-24 months by Morningstar analysts, is the structural risk that gives AMD, TSMC, and ASML their sensitivity to any forward-guidance revision from Nvidia; if today’s commentary signals a slower-than-expected ramp in orders, that lag means the effect would propagate through supplier earnings well into 2027.

An investor holding a semiconductor ETF, a broad technology fund, or individual positions in any of these names is materially exposed to the outcome of today’s print, whether or not they own NVDA directly.

Three positioning signals heading into the print tell a consistent story:

This setup creates an asymmetric reaction function. When positioning is cautious heading into a binary event, a strong beat can produce an outsized relief rally as sidelined capital re-enters. A miss, however, lands into a market already on edge, amplifying the selloff because protective positioning is already partially in place.

The question for the broader market is whether “the AI-driven rally that brought the Nasdaq and S&P 500 to record highs earlier in May could be sustained.”

Whether those highs hold as a base or prove to be a local peak depends substantially on whether today’s print re-anchors the AI spending thesis or introduces doubt.

Nvidia’s Q1 FY2027 report is not simply an earnings event for one company. It functions as a live referendum on the AI infrastructure spending cycle that has been the primary driver of U.S. equity market outperformance in 2026. The three signals that will define how markets interpret the print are the data centre revenue growth rate, the forward guidance tone, and any hyperscaler capex language from the earnings call.

Regardless of the initial price reaction, the commentary on demand trajectory and forward capital spending will matter more for the durability of the AI rally than any single quarter’s revenue figure. For retail investors parsing the headlines this evening, that distinction is the one worth holding onto.

The AI bull market runway and risk horizon were assessed by Paul Tudor Jones on 6 May 2026 as approximately one to two years, a framing that sits between the bull case of a durable infrastructure supercycle and the bear case of an imminent correction; the single most important metric in that assessment, a sustained drop in hyperscaler capex growth below 25% year on year, is exactly the figure today’s Nvidia guidance commentary will either confirm or challenge.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding market reactions and earnings outcomes are speculative and subject to change based on market developments and company performance.

Nvidia's Q1 FY2027 earnings report covers the quarter ended 26 April 2026 and is closely watched because the company's data centre revenue functions as a real-world readout on whether AI infrastructure spending by major cloud providers is accelerating or slowing down.

The data centre segment revenue growth rate is the most market-sensitive figure, followed by forward guidance and management commentary on hyperscaler capital expenditure commitments, which analysts treat as more valuable than any single quarter's reported revenue.

Higher risk-free rates compress the present value of long-duration earnings streams, which disproportionately hurts growth stocks like Nvidia; the 30-year Treasury yield trading above 5.1% for the first time since 2007 has added structural pressure to technology valuations heading into the print.

AMD, TSMC, ASML, and Broadcom are the four names most directly exposed: AMD competes in AI accelerator chips, TSMC manufactures Nvidia's advanced GPUs, ASML supplies the lithography equipment foundries need, and Broadcom competes in custom AI silicon for hyperscalers.

Amazon, Microsoft, Alphabet, and Meta have provided approximately $725 billion in combined AI infrastructure capex guidance for 2026, with $130 billion deployed in Q1 2026 alone, making Nvidia's data centre revenue the primary indicator of whether that spending is being sustained.