Citi published a note on Tuesday, 9 June 2026 warning that while broad U.S. equity positioning has improved following last week’s sharp selloff, Nasdaq bullish positioning remains dangerously stretched. The majority of long positions in tech-heavy names are still profitable, and a string of catalyst events lies ahead. The warning lands four days after the Nasdaq Composite dropped 4.18% in a single session, a move that cleared some crowded exposure from the broader market but left tech-specific positioning largely intact. Citi’s Bear Market Checklist simultaneously sits at 11.5 of 18 risk flags, its highest reading since the 2008 financial crisis. What follows is an explanation of what Citi found, why profitable long positions are a warning sign rather than a comfort, and what investors with tech-heavy portfolios need to understand about the asymmetric risk ahead.

The Nasdaq positioning problem Citi flagged this week

Citi’s 9 June note delivered a split verdict on U.S. equity markets. Broad positioning, measured across S&P 500 exposures, is genuinely “cleaner” after last week’s downturn. Some excess long exposure has been shaken out, and the overall market health picture improved.

The Nasdaq is a different story. Bullish positioning in tech-heavy names remains extended, crowded on the long side, and, per Citi, sustained by the fact that the majority of those long positions are still in profit. That profitability is not a sign of resilience. It is the source of vulnerability.

The two-part picture breaks down as follows:

- What improved: S&P 500 and broad U.S. equity positioning moderated after the selloff; some crowded long exposure was reduced, producing a healthier overall setup.

- What remains vulnerable: Nasdaq bullish positioning is still stretched; the majority of long positions remain profitable; tech-specific crowding has not resolved.

Investors who took comfort from last week’s stabilisation at the index level need to recognise that the specific risk Citi is flagging sits one layer below the headline, concentrated in the tech names that dominate many portfolios.

When big ASX news breaks, our subscribers know first

Why profitable longs are a risk factor, not a reassurance

The logic is counterintuitive but mechanically straightforward. When long positions are still in profit, holders have both the ability and the incentive to sell quickly if a negative catalyst arrives. They can lock in gains. They are not anchored by losses. The exit is clean, and it is fast.

Contrast that with underwater positions, where much of the forced selling has already occurred. Investors holding losses tend to anchor, waiting for recovery rather than crystallising a deficit. Incremental selling pressure from deeply underwater longs is lower.

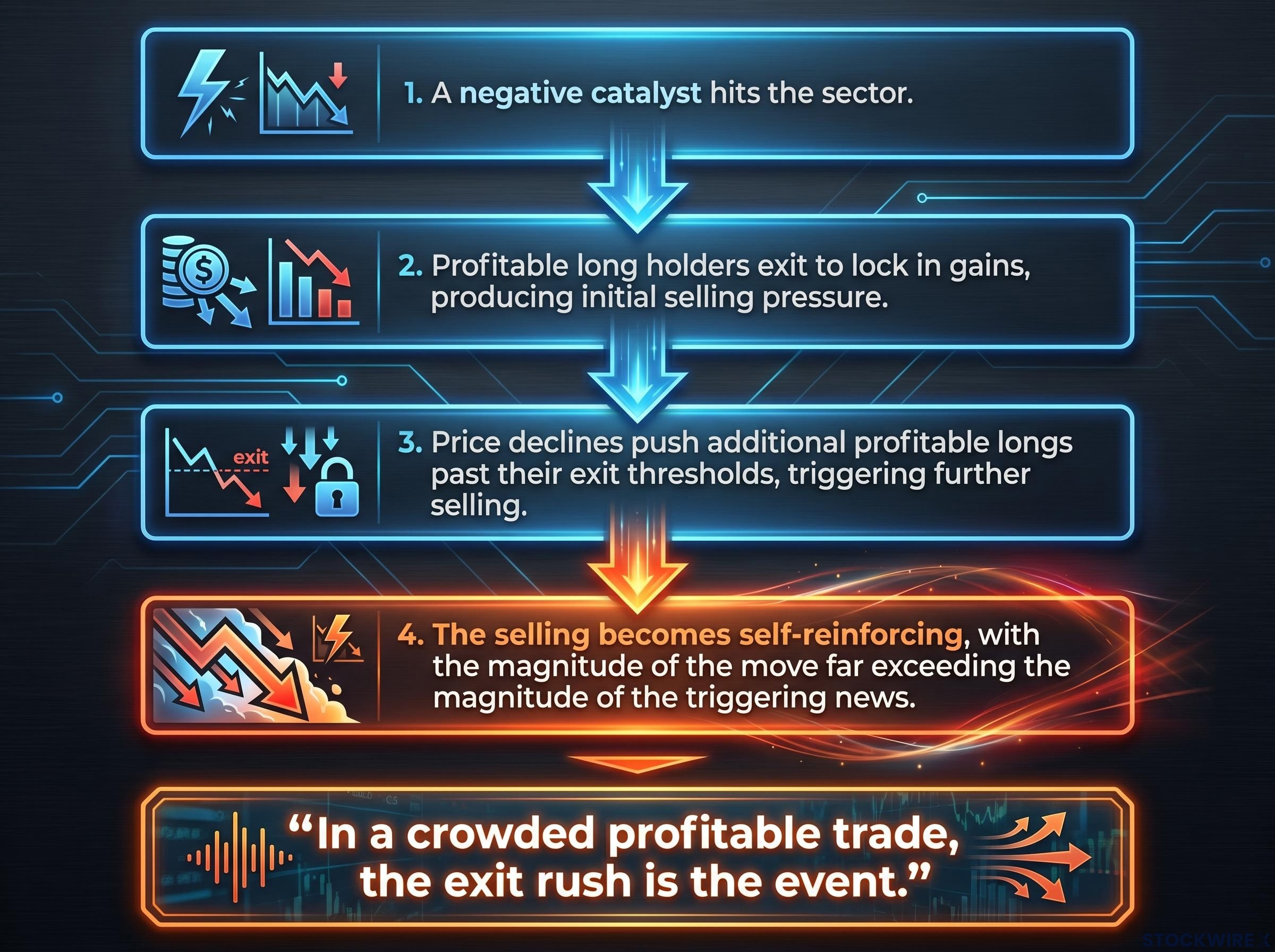

The unwinding sequence in a crowded, profitable trade follows a predictable chain:

- A negative catalyst hits the sector.

- Profitable long holders exit to lock in gains, producing initial selling pressure.

- Price declines push additional profitable longs past their exit thresholds, triggering further selling.

- The selling becomes self-reinforcing, with the magnitude of the move far exceeding the magnitude of the triggering news.

The size of a positioning-driven move can be disproportionate to the news that triggered it. In a crowded profitable trade, the exit rush is the event.

This is the mechanism Citi is warning about. The vulnerability is not fundamental deterioration in the tech sector. It is the mechanical speed at which crowded, profitable positions can unwind.

What the June 5 selloff did (and did not) fix

What the selloff cleared

The 4.18% single-session Nasdaq drop on 5 June 2026 was triggered by a stronger-than-expected jobs report. Yields rose on the data, and the “good news is bad news” dynamic hit high-valuation AI and semiconductor names hardest.

BNN Bloomberg’s June 5 market coverage confirmed the Nasdaq composite slumped 4.2% on the session, with a stronger-than-expected jobs report lifting expectations for Federal Reserve rate hikes and hitting high-valuation tech names with particular severity.

At the broad equity level, the selloff did real work. It reduced some crowded long exposure across S&P 500 positioning, producing the “cleaner” setup Citi documented four days later. For the overall market, the partial de-risking was a net positive.

What it left behind

The same selloff left Nasdaq bullish positioning still extended. Profit levels on existing longs compressed from their prior highs, but the majority of positions remained profitable. The relief was real at the index level. It was incomplete where the concentration sits.

CTA mechanical selling pressure adds a layer of non-fundamental risk that the positioning-driven unwind mechanism alone does not fully capture: Bank of America estimated that at least half of existing CTA long positions remained intact after the June 6 session, meaning a further 1-2% decline in the Nasdaq could trigger a second, cascading wave of systematic deleveraging independent of any new fundamental catalyst.

That gap is the precise reason Citi’s 9 June note carried the warning it did. The story did not end on 5 June. The broad market improved; the specific vulnerability in tech did not resolve.

AI concentration and why the whole index moves when tech does

A small cluster of AI-adjacent megacaps and semiconductor names represents an unusually large share of Nasdaq market capitalisation. In practical terms, this means any de-risking in that cluster is mechanically a de-risking of the entire index.

The distinction between “selling tech” and “selling the index” has, at current concentration levels, substantially collapsed.

Record U.S. market concentration adds a structural dimension to the positioning concern: with five names controlling roughly 30% of total U.S. equity market capitalisation, a level that now exceeds the dot-com peak, any forced exit in that cluster is not a sector event but a systemic one.

At this level of index concentration, a positioning event in a handful of names does not stay contained. It becomes an index-level event.

This concentration creates an amplification effect that works in both directions. On the way up, the same names pull the index higher. On the way down, a modest disappointment against already-elevated expectations can trigger positioning-driven volatility without any fundamental deterioration, because all holders are attempting to exit the same trade at the same time.

| Trigger type | Who exits first | Why selling accelerates | Index-level effect |

|---|---|---|---|

| Earnings miss vs elevated expectations | Profitable longs locking in gains | Price decline pushes more longs past exit thresholds | Concentrated names drag index disproportionately |

| Macro data surprise (yields rise) | Rate-sensitive growth holders | High-valuation names hit hardest; exits cluster | Tech weight transmits sector stress to headline index |

| Product or guidance disappointment | Momentum-driven allocators | Crowded positioning means exits are simultaneous | Single-name move becomes sector-wide selloff |

The bar for a “disappointing” result is lower than it appears. Expectations embedded in current positioning are already elevated, meaning even a modestly below-consensus outcome can trip the unwinding mechanism.

The Bear Market Checklist and what 11.5 out of 18 means for the outlook

Citi’s Bear Market Checklist sits at 11.5 of 18 risk flags, the highest reading since the 2008 financial crisis.

The Citi Bear Market Checklist is a multi-factor framework tracking simultaneous macro and market stress signals, and the U.S. reading of 11.5 out of 18 is notably more elevated than the global reading of 10 out of 18, a regional divergence that has not attracted the same attention as the headline figure.

11.5 of 18 risk flags triggered. The last time Citi’s Bear Market Checklist was this elevated, the global financial system was entering its worst crisis in a generation.

The checklist is a multi-factor framework that tracks macro and market stress indicators simultaneously. At 11.5, the reading signals that the Nasdaq positioning concern does not exist in isolation. It sits against a backdrop of the broadest set of simultaneously elevated risk flags in nearly two decades.

The compounding picture looks like this:

- Nasdaq bullish positioning remains extended and crowded on the long side

- AI and semiconductor concentration amplifies any sector-level move to the index level

- The majority of existing long positions remain profitable, sustaining the fast-exit dynamic

- The Bear Market Checklist sits at post-2008 highs, elevating the consequence of any unwind

- Tech catalyst events lie ahead, presenting specific triggers for the vulnerability to convert

At elevated checklist readings, Citi’s own framework acknowledges that upcoming events can amplify stress further. The macro backdrop does not cause the positioning unwind, but it raises the stakes if one begins.

What comes next and why tech catalyst events matter now

Citi’s note flagged upcoming technology sector catalyst events as presenting meaningful liquidation risk, given the still-profitable long positioning in Nasdaq-related holdings. The mechanism is specific: a disappointing result against already-elevated expectations does not need to be severe to trigger long unwinding. In a crowded profitable trade, the exit rush is self-amplifying.

The conditions under which this vulnerability converts from latent to realised are identifiable:

- A tech catalyst event arrives (earnings, guidance, product announcement, or macro data print affecting valuations)

- The result disappoints relative to the elevated expectations embedded in current positioning

- Long unwinding begins, price declines trigger further exits, and the selling becomes self-reinforcing

The layered risk picture described throughout this analysis is not a single vulnerability. It is a convergence: stretched positioning, concentrated exposure, profitable legacy longs, an elevated macro backdrop, and specific near-term catalysts capable of triggering the chain.

Investors with tech-heavy portfolios face a practical question. Citi’s analysis provides a clear basis to reassess exposure ahead of the next catalyst event, rather than treating the post-selloff stabilisation as an all-clear.

Why broad market improvement doesn’t eliminate tech risks

Broad U.S. equity positioning improved after the 5 June selloff. That improvement is real. It is also incomplete. Nasdaq-specific vulnerability has not resolved, and conflating the two is the precise error Citi’s 9 June note warns against.

The risk picture is layered: stretched Nasdaq positioning, concentrated AI and semiconductor exposure, profitable legacy longs with fast exit capability, a Bear Market Checklist at its highest since 2008, and tech catalyst events ahead. Each factor alone would warrant attention. Together, they describe an environment where the consequences of a positioning unwind are amplified at every level.

Investors with significant tech-heavy holdings have a clear basis from Citi’s analysis to reassess their exposure before the next catalyst, rather than reading “cleaner” as “safe.”

For investors reassessing their tech-heavy exposure in light of the risk picture Citi has outlined, our full explainer on market leadership rotation away from US Tech examines the valuation spread between US Technology and international developed markets, reviews historical concentration episodes including the Nifty Fifty and the TMT bubble, and presents an incremental rebalancing framework grounded in starting valuations as the most reliable long-term return predictor.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Forward-looking statements regarding market conditions and positioning risks are subject to change based on market developments.