BOQ Share Price Discount: What NIM, ROE and CET1 Actually Show

19 mins ago

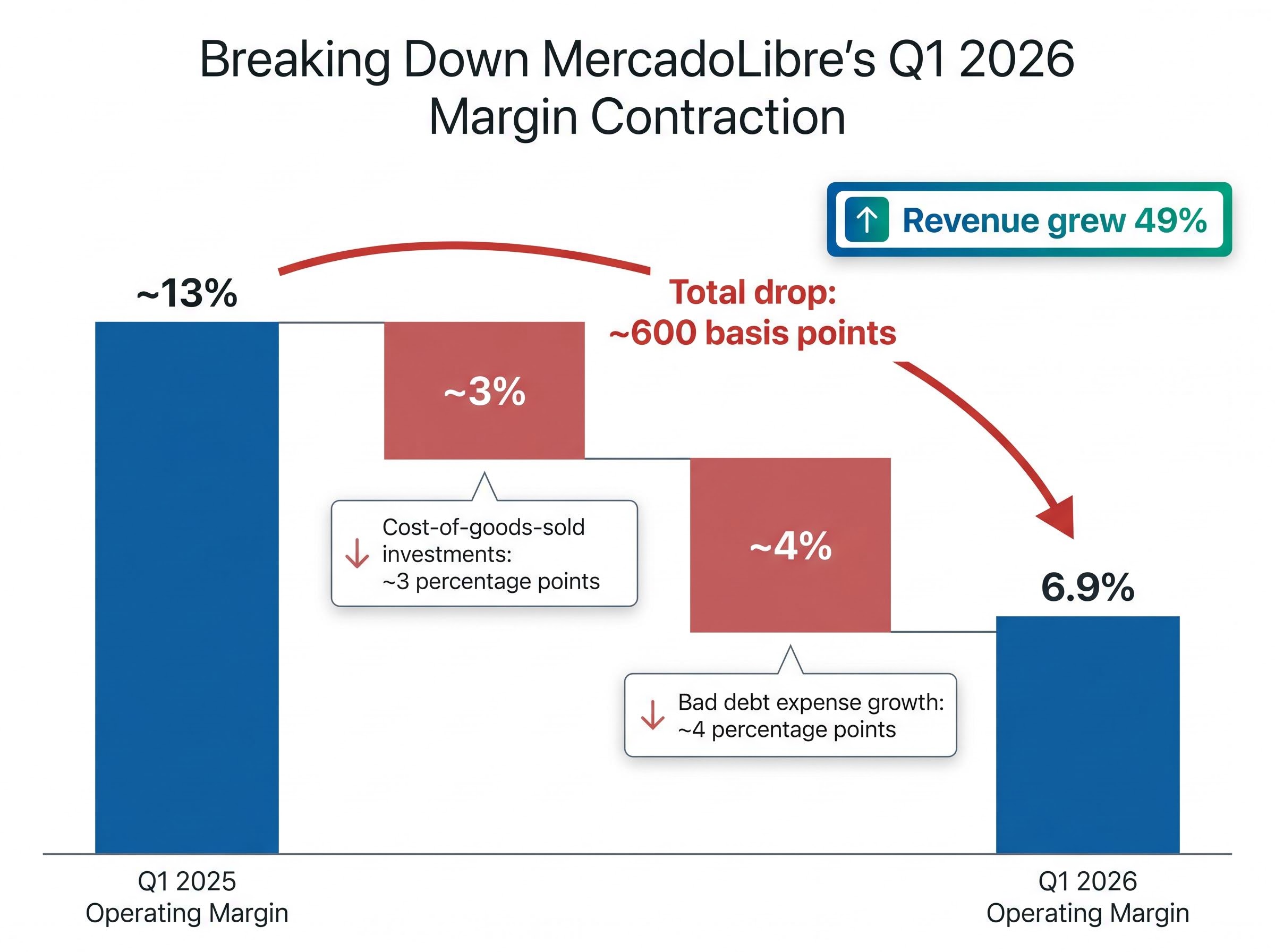

MercadoLibre’s stock is down 20% year-to-date, and its operating margin just contracted by 600 basis points. On paper, that looks like a company in trouble. The more interesting question is whether the paper tells the right story. Q1 2026 earnings, reported on 7 May 2026, delivered 49% revenue growth alongside a margin collapse from roughly 13% to approximately 7%. The combination triggered a 12% single-day stock drop and spooked investors who read the margin line as evidence of fundamental deterioration. But CFO Martin de los Santos said something notable on the earnings call: he described the compression as “natural and recurring,” and said management could restore margins tomorrow simply by slowing investment. They are choosing not to. This analysis breaks down the two specific decisions driving the margin decline, explains why GAAP provisioning mechanics on a fast-growing credit book can make a healthy business look impaired, and frames what the numbers actually signal for investors evaluating the stock near $1,632.

The surface reading is straightforward. MercadoLibre’s operating margin moved from approximately 13% in Q1 2025 to 6.9% in Q1 2026, a contraction of roughly 600 basis points year-over-year. Revenue grew 49% over the same period, which means the company did not have a demand problem. It had an expense problem, or at least one that looked like an expense problem.

The entire 600-basis-point decline traces to two line items, both of which management chose to incur:

Post-earnings analyst commentary confirmed the EPS miss was driven primarily by provisions for doubtful accounts rather than a broad-based cost problem. The distinction matters. A company whose margins are compressing across every line item is deteriorating. A company whose margins are compressing because of two identifiable, discretionary decisions is making a bet.

Reading earnings reports critically requires separating the metrics management chooses to highlight from the ones buried in footnotes or quietly dropped from quarter-to-quarter disclosures; the placement of information inside a press release is itself an analytical signal, not a neutral layout choice.

CFO Martin de los Santos, May 7 2026 earnings call: “Margins are a consequence of our investment posture… We will not try to optimize short-term margins. We are looking at a big opportunity… if we wanted to improve margins short-term, it would be easy to slow investments but not the right way.”

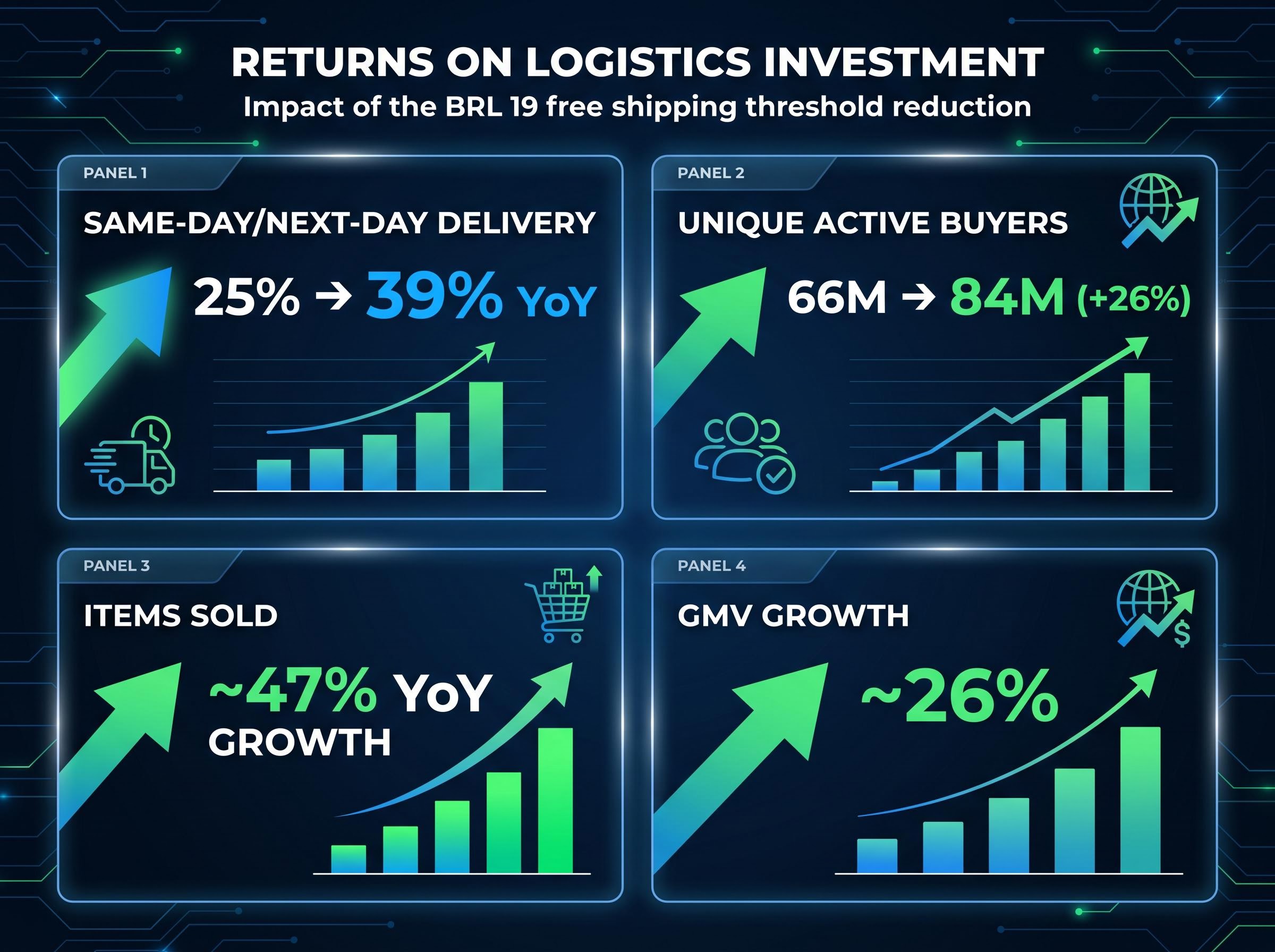

The first decision is visible in the logistics line. MercadoLibre reduced its free shipping threshold in Brazil to BRL 19, making free shipping available on a substantially wider range of orders and raising fulfilment costs per transaction. First-party inventory investments compounded the impact, ensuring product availability and price competitiveness across more categories.

The cost is real. But so is the output it purchased.

The operational metrics that followed the threshold reduction tell a clear story:

This decision contributed roughly 3 percentage points of the 6-point margin decline. A lower shipping threshold increases purchase frequency and basket size, compounding the buyer base expansion over time. The margin cost is front-loaded; the repeat-purchase benefit accrues over subsequent quarters as those 84 million active buyers transact again. Understanding that temporal structure is the difference between reading the cost as a problem and reading it as a trade.

The second decision carried the larger margin impact, and it is the one most likely to be misread. MercadoLibre’s total loan portfolio grew from approximately $8 billion to approximately $15 billion, an 87% year-over-year expansion.

| Loan Type | Approximate Portfolio Share | Context |

|---|---|---|

| Credit cards | ~46% | Largest and fastest-growing segment; lower near-term margins that improve as cohorts mature |

| Consumer loans | ~37% | Includes shift toward slightly longer-duration personal loans |

| Merchant loans | ~16% | Backed by transaction data from Mercado Pago processing volume |

The counterintuitive finding sits in the delinquency data. Despite the portfolio nearly doubling:

Improving delinquency ratios while nearly doubling loan volume is rare. It materially changes the interpretation of the provisioning charge. The cost is not a warning signal about loan quality. It is the accounting consequence of volume.

Loan book growth alongside improving credit quality has been demonstrated in other scaling fintech lenders as well; MoneyMe reported a 29% year-on-year loan book increase in Q3 FY26 while net credit losses fell from 3.7% to 2.6% and risk-adjusted net interest margin expanded materially, illustrating that rapid origination volume does not automatically translate into credit deterioration when underwriting discipline holds.

This is the mechanic that separates informed investors from those who exit prematurely. Under GAAP (Generally Accepted Accounting Principles, the standard accounting framework used for financial reporting in the United States), MercadoLibre provisions for the full expected lifetime loss on each new loan at the moment it is originated. That means the entire estimated cost of potential defaults hits the income statement before a single dollar of interest income or fees from that loan has been earned.

The CECL lifetime loss provisioning standard, established under FASB ASC Topic 326, requires lenders to recognise the full expected credit loss on a loan at origination rather than spreading that charge across the loan’s life, which is why a rapidly scaling credit book generates provisioning expenses that outpace current-period revenue even when underlying loan quality is stable or improving.

| What happens at loan origination | What happens over the loan’s life |

|---|---|

| Full expected lifetime loss is provisioned immediately | Interest income and fees accrue over months or years |

| Cost hits the income statement in the current quarter | Revenue from the loan matures gradually across future quarters |

| Reported margins compress in the origination period | Margins recover as cohort revenue catches up to the upfront provision |

A credit book growing at 87% year-over-year will mechanically generate provisioning charges that grow faster than revenue in any given quarter, compressing reported margins even if loan quality is improving. That is precisely what is happening here.

CFO Martin de los Santos: “Credit book grew 87% YoY vs. 49% revenue growth… we provision for full expected loss on new loans upfront, explaining approximately 2/3 of margin compression. This is natural and recurring.”

Bad debt expense growth contributed approximately 4 percentage points of the 6-point margin decline. Two-thirds of that increase was attributed to volume growth. The remaining one-third reflects a shift toward slightly longer-duration personal loans, which carry higher per-loan provisions but also higher lifetime returns.

The mechanic is not specific to MercadoLibre. It applies to any rapidly scaling lender reporting under GAAP. Misreading provisioning as credit quality deterioration has caused investors to exit positions in financially sound companies at precisely the wrong time.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The market’s forward-looking verdict offers a useful calibration point. Approximately 17-19 analysts cover MercadoLibre, with approximately 15-16 carrying a Buy or Strong Buy rating. No downgrades were issued following the Q1 2026 results, despite the 600-basis-point margin miss and 12% single-day stock drop.

The average analyst price target of approximately $2,420-$2,587 implies roughly 53% upside from the $1,632.52 close on 8 May 2026. The high target reaches $3,000.

Morgan Stanley maintained its Overweight rating with a price target of $2,600 as of 9 March 2026.

| Company | Market Cap | Forward P/E | Op. Margin (Recent Q) | Revenue Growth |

|---|---|---|---|---|

| MercadoLibre | ~$83-85B | ~35.7x | 6.9% | 49% |

| Nu Holdings | ~$67B | ~16x | 25%+ | ~20-30% |

| StoneCo | ~$2.6-4B | ~5.3x | ~15% | ~20-30% |

| dLocal | ~$3.9-4B | ~15.3-16.5x | ~18% | ~20-30% |

MercadoLibre commands a significant forward P/E premium over Latin American peers. Analysts broadly consider this justified given the 49% revenue growth rate versus the 20-30% range among comparable companies. The absence of any downgrade following a 600-basis-point margin miss is itself informative; it signals that institutional analysts with full access to management are treating this as an investment-phase story, not a deterioration story.

Investment-phase spending misreads are not unique to Latin American markets; Meta’s stock fell roughly 9% on Q1 2026 results despite 33% revenue growth and 41% operating margins, as the market reacted to a near-doubling of capital expenditure guidance rather than engaging with the underlying return thesis.

The analysis to this point has been deliberately sympathetic to management’s framing. The risks deserve the same analytical seriousness. Three conditions could convert the investment-phase thesis into a genuine deterioration story:

Credit cycle deterioration in broader consumer and leveraged lending markets provides the macro backdrop against which MercadoLibre’s Latin American credit expansion should be stress-tested; by late Q1 2026, US private credit default rates had reached 2.73% with Fitch projecting 4.5-5.0% for leveraged loans across the full year, a reminder that rising delinquency environments can convert provisioning timing differences into permanent losses.

Management has explicitly stated it will not optimise short-term margins, meaning sustained investment pressure is the base case, not a temporary condition. Investors should weigh that signal accordingly.

These statements are speculative and subject to change based on market developments and company performance.

The margin compression is traceable to two specific decisions, supported by improving operational and credit quality metrics, and interpreted by virtually the entire analyst community as investment-led rather than deterioration-led. A combined low-case valuation of both the commerce and fintech segments has been estimated at approximately $120 billion versus the current market capitalisation of approximately $83 billion, implying roughly 30-40% upside even under conservative assumptions, though this framework is illustrative rather than definitive.

For investors with a shorter time horizon, management’s explicit commitment to continued investment spending means near-term margin pressure is not a risk to be hedged against; it is the stated plan. The forward indicators that would confirm or challenge the thesis over the next two to three quarters are, in order of importance:

Management’s position, May 7 2026 earnings call: “We will not try to optimize short-term margins. We are looking at a big opportunity.”

A reader who finishes here should have a clear framework: the current numbers reflect choices, not decay. Whether those choices pay off depends on the three signals above. Watching them quarter by quarter converts a static moment-in-time reading into an ongoing assessment of whether the investment phase is delivering.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

MercadoLibre's operating margin declined from approximately 13% to 6.9% year-over-year due to two specific decisions: logistics investments including a lower free shipping threshold in Brazil, which contributed roughly 3 percentage points of compression, and rapid credit book expansion that triggered higher GAAP provisioning charges, contributing approximately 4 percentage points.

CECL (Current Expected Credit Loss) provisioning requires lenders to recognise the full expected lifetime loss on a loan at the moment it is originated, meaning the entire cost of potential defaults hits the income statement before any interest income or fees from that loan have been earned, which mechanically compresses reported margins for any rapidly scaling credit book even when loan quality is stable or improving.

Despite the total loan portfolio growing approximately 87% year-over-year from around $8 billion to $15 billion, both the 15-to-90-day and 90-day-plus past-due ratios as a percentage of total loans improved year-over-year, with CFO Martin de los Santos characterising asset quality as stable.

Approximately 15 to 16 of the 17 to 19 analysts covering MercadoLibre carry a Buy or Strong Buy rating, no downgrades were issued following the Q1 2026 results, and the average analyst price target of approximately $2,420 to $2,587 implies roughly 53% upside from the $1,632 close on 8 May 2026.

The three most important forward indicators are: Net Interest Margin After Losses (NIMAL) recovery as credit card cohorts mature, the direction of the 15-to-90-day past-due ratio to confirm sustained credit quality improvement, and continued unique active buyer and GMV growth to validate that logistics investment is compounding commercial output.