Five central bank stories across four economies converge in a single calendar week, and each one carries a data release that feeds directly into a rate decision scheduled within 30 days. The week of 18-22 May 2026 opens with China’s activity data on Monday and closes with Japan’s consumer price index on Friday, with UK inflation, FOMC minutes, and Australian employment figures landing in between. Bond markets have already started moving: UK 10-year gilt yields climbed more than 25 basis points in the prior week, and the US dollar broke out of its recent trading range. Markets are pricing rate paths that diverge sharply across the UK, US, Japan, and Australia, and the data arriving this week will either validate those bets or force a repricing. What follows maps each release to its central bank decision, explains what consensus expects, and connects the signals into a single picture of where global monetary policy stands heading into mid-2026.

Wednesday is the week’s axis: FOMC minutes and UK inflation arrive together

Two independently significant releases land on the same day, Wednesday 20 May, and they pull in opposite directions on global rate expectations. The FOMC minutes document the final meeting chaired by Jerome Powell before the leadership transition. The UK consumer price index delivers the inflation reading that will shape the Bank of England’s 18 June decision. Together, they make Wednesday the session where the week’s macro picture either sharpens or fractures.

What the FOMC minutes will and won’t tell markets about Warsh’s direction

The minutes are expected to document a significant internal shift: growing committee support for removing the easing bias from forward guidance. A split vote at that meeting, historically unusual for the Fed, will be parsed closely for what it signals to incoming Chair Kevin Warsh, confirmed by a 54-45 Senate vote on 13-15 May 2026.

Warsh’s documented hawkish orientation from his earlier tenure as Fed Governor makes the language around the easing bias removal particularly consequential. These minutes reflect a transitional moment, not a clean signal of new leadership direction, since they record the prior meeting’s deliberations rather than Warsh’s incoming posture. The two elements analysts will scrutinise most closely are the split vote itself and the specific phrasing used to frame the forward guidance debate.

The split vote the minutes will document was not a routine policy disagreement: the April 29 meeting produced a historic FOMC dissent, with hawks outnumbering the lone dovish dissenter three to one against a backdrop of PCE inflation running at 3.5% and unemployment rising to 4.3%, a dual-mandate conflict that made any clean consensus statement functionally impossible.

UK services inflation is the number inside the number

On the same morning, UK headline CPI is forecast to fall to 3.1%, with core inflation at 2.7%. The headline decline is driven primarily by government energy bill interventions announced in the 2025 budget, which makes the surface reading less informative than the detail beneath it.

The Bank of England has explicitly flagged services inflation as its primary gauge of domestic price persistence. The April services inflation forecast of 3.5%, down from a prior reading of 4.7%, is more consequential for June pricing than the headline figure. Higher petrol prices will partially offset the energy bill relief, creating a mixed picture that complicates a clean dovish read.

The Bank of England MPC minutes from March 2026 explicitly noted that a smaller-than-expected fall in services inflation contributed to a higher-than-anticipated headline CPI outcome, cementing services inflation as the committee’s primary variable in assessing domestic price persistence.

- FOMC minutes (Wednesday 20 May): document split vote and easing bias debate

- UK CPI (Wednesday 20 May): headline forecast 3.1%, core 2.7%, services 3.5%

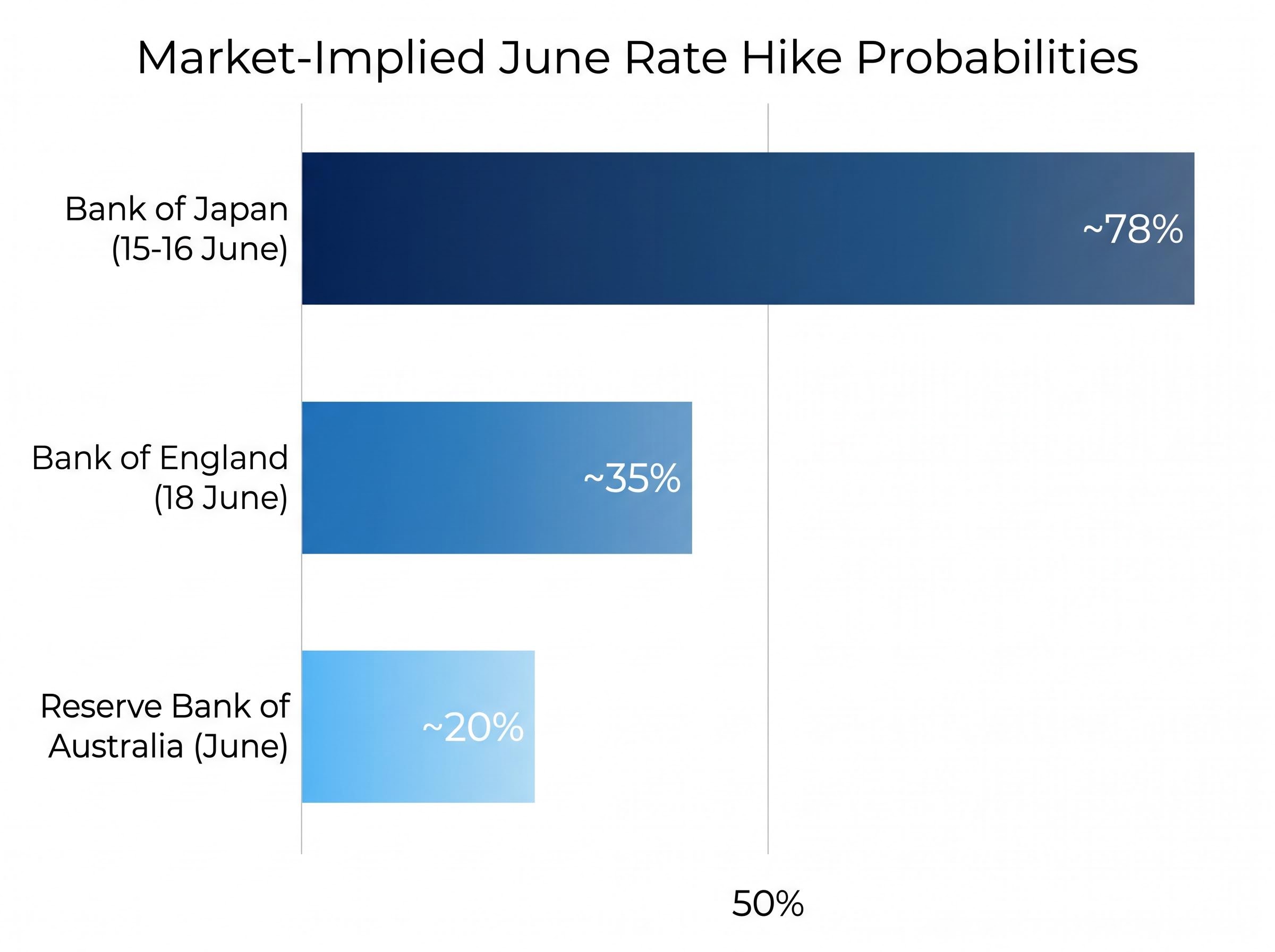

Market-implied probability of a 25 basis point BoE rate increase at the 18 June meeting stands at approximately 35%, with cumulative tightening of roughly 80 basis points priced over the next 12 months. Wednesday’s CPI print is the single most important input to whether that pricing holds.

When big ASX news breaks, our subscribers know first

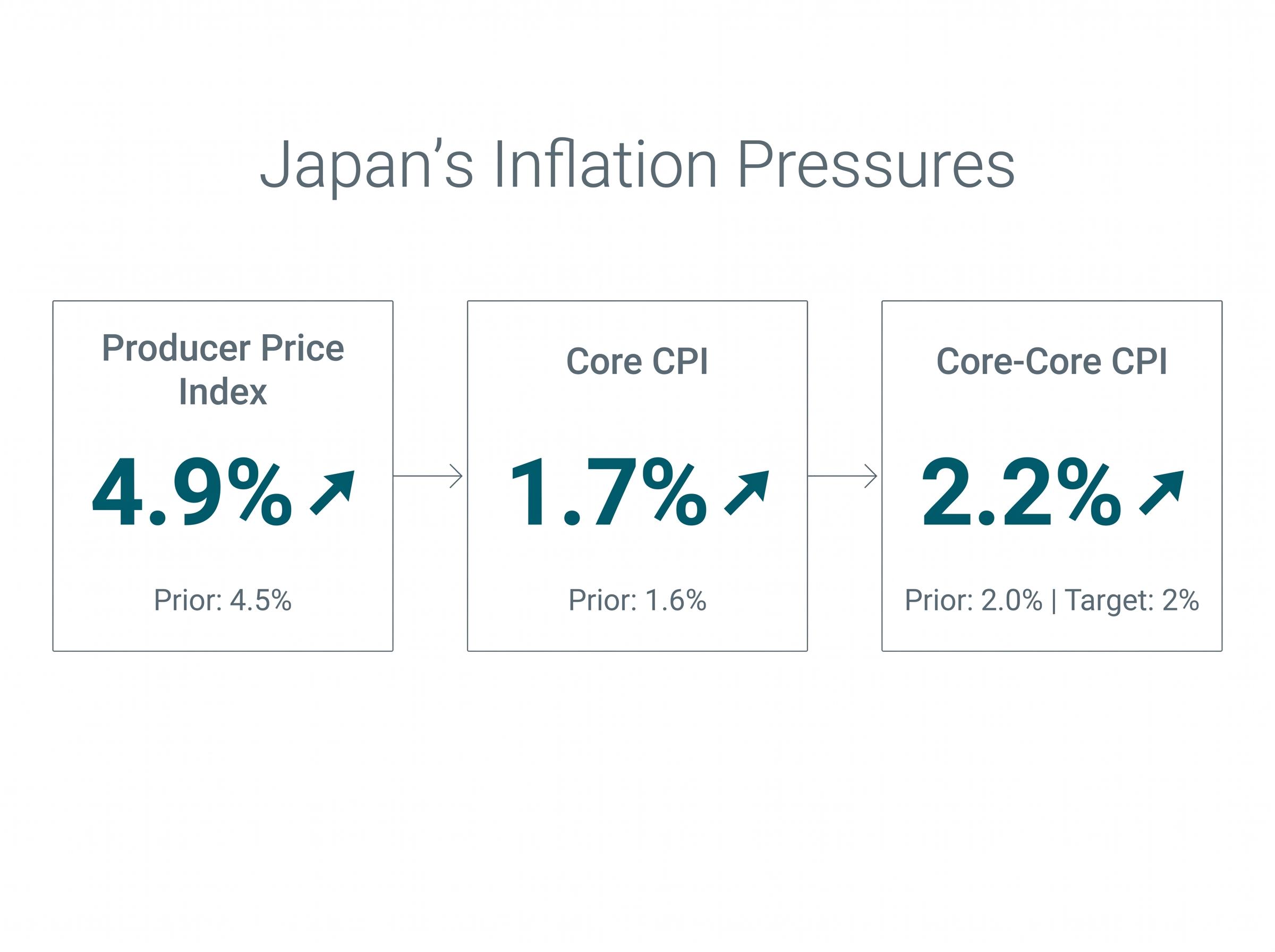

Japan’s inflation data makes a June Bank of Japan hike near-certain

The upstream signal arrived first. Japan’s producer price index printed at 4.9%, indicating that pass-through pressure on consumer prices is building from the wholesale level. In an import-dependent economy, yen weakness amplifies this dynamic: elevated import costs feed through supply chains and eventually reach the consumer basket.

Friday’s national CPI release on 22 May is expected to confirm the pressure. Consensus places the core CPI estimate at 1.7%, while the policymaker-preferred core-core measure, which strips out both fresh food and energy, is forecast at 2.2%. The BoJ has historically weighted the core-core reading more heavily in its deliberations, and a print at or above 2.2% would sit comfortably above the 2% inflation target.

The BoJ’s 2% price stability target is defined in terms of the year-on-year change in the consumer price index, and the core-core measure stripping out fresh food and energy has become the committee’s preferred gauge for assessing whether that target is being durably achieved.

| Indicator | Consensus Estimate | Prior Reading | Policy Implication |

|---|---|---|---|

| Core CPI | 1.7% | 1.6% | Supports continued normalisation |

| Core-Core CPI | 2.2% | 2.0% | Above 2% target; strongest hike signal |

| Producer Price Index | 4.9% | 4.5% | Upstream pass-through pressure building |

Market-implied probability of a 25 basis point BoJ hike at the 15-16 June meeting stands at approximately 78%. Polymarket priced the probability at 62.9% as of 11 May, suggesting the range has narrowed upward as data has accumulated.

A BoJ hike would extend the normalisation of the world’s last major ultra-loose monetary policy regime. For global markets, the significance runs beyond Japan: Japanese investors hold substantial foreign bond positions, and a tightening BoJ encourages repatriation of capital, with knock-on effects for US Treasury and European sovereign yields.

What central bank divergence actually means for currency and bond markets

The data points above describe what individual central banks might do. The interaction between those decisions is where the market-moving force lives. When four major central banks pursue different rate paths simultaneously, the divergence itself becomes a signal that reprices currencies, bonds, and cross-border capital flows.

How rate divergence drives exchange rates and capital flows

Monetary policy divergence creates directional pressure on exchange rates because capital flows toward higher-yielding currencies when rate differentials widen. The UK-US dynamic in the prior week illustrated this directly: the dollar broke out of its recent trading range while sterling experienced a sharp decline, driven in part by UK domestic political uncertainty layered on top of shifting rate expectations.

Bond yield differentials between countries operate on the same principle. When UK gilt yields rise faster than equivalent maturities in other sovereign markets, they attract foreign capital seeking the higher return, but only if investors believe the yield increase reflects durable policy tightening rather than fiscal risk. The 25 basis point spike in gilt yields in the prior week sits at the intersection of both interpretations.

Why gilt yields moving 25 basis points in a week is not a routine event

A weekly move of that magnitude in a major sovereign bond market signals significant repricing of rate expectations, not day-to-day volatility. For context, a 25 basis point move in a single week represents the equivalent of an entire standard central bank rate adjustment compressed into five trading sessions. US Treasury yields rose sharply in tandem, confirming that the repricing was not isolated to the UK.

The concept of “policy premia” helps explain the mechanics. When central bank paths are uncertain, investors demand extra yield to compensate for the risk that rates move further than expected. The cumulative 80 basis points of BoE tightening priced over 12 months reflects that premium. Whether weaker economies like the UK can absorb higher borrowing costs without meaningful growth consequences remains the open question beneath the yield move.

The 25 basis point spike in gilt yields did not arrive in isolation: it formed part of a broader global bond sell-off on 15 May 2026 that pushed US 30-year Treasury yields above 5% for the first time since 2007 and Japanese 30-year JGB yields to an all-time record, as oil shock, sticky inflation, and political risk converged into what strategists are treating as a structural repricing of long-duration sovereign debt.

- Exchange rate pressure: rate divergence drives capital toward higher-yielding currencies

- Capital flow reallocation: bond yield differentials attract or repel cross-border investment

- Policy uncertainty premia: the extra yield investors demand when central bank paths are unclear

UK labour data and Australian employment figures frame the week’s opening

Two economies at very different points in their rate cycles are both waiting on jobs data to determine whether their central banks have room to move or must hold. The releases land on Tuesday 19 May (UK) and Thursday 21 May (Australia), bookending the week’s labour market story.

UK labour data arrives with the BoE watching wage growth closely. Average earnings excluding bonuses are forecast at 3.1%, pointing to a wage-inflation dynamic that is moderating but not conclusively resolved. The unemployment rate is expected to edge down 0.1 percentage points to 4.8%. Two interpretation caveats apply: ongoing statistical reliability concerns around UK jobs data complicate how cleanly the BoE can read a single release, and the wage figure will be weighed against Wednesday’s CPI print rather than assessed in isolation.

Australian employment data carries different stakes. Consensus expects 17,500 job additions in April with the unemployment rate steady at 4.9%, but market pricing implies only a roughly 20% probability of a June RBA hike. The data needs to surprise meaningfully to shift that expectation. Easter timing effects may distort the April reading, and the full-time versus part-time breakdown will be watched more closely than the headline number.

The low probability of a June RBA move reflects how much the central bank has already delivered: the RBA tightening cycle has raised the cash rate to 4.35%, making Australia’s central bank the most aggressive in the developed world during this period and compressing household demand to the point where consumer sentiment fell sharply to 80.1 in April 2026, raising the question of whether further hikes risk overshooting into recession territory.

| Economy | Key Release | Consensus Estimate | Central Bank Meeting | Current Hike Probability |

|---|---|---|---|---|

| United Kingdom | Labour data (19 May) | Earnings ex-bonuses: 3.1%; Unemployment: 4.8% | 18 June (BoE) | ~35% |

| Australia | Employment (21 May) | Jobs: +17,500; Unemployment: 4.9% | June (RBA) | ~20% |

- UK data caveat: ongoing concerns about the statistical reliability of UK labour force survey data

- Australia data caveat: Easter timing effects may distort the April reading; full-time versus part-time split will carry more weight than the headline figure

China’s data and global PMIs set the demand backdrop every central bank is watching

Central banks do not set rates against a blank screen. Every hawkish or dovish call this week is conditional on whether global demand is holding, and Monday’s China data and Thursday’s PMI releases provide the answer.

China’s activity data presents a split picture:

- Industrial production: forecast at approximately 6%, supported by external demand

- Retail sales: expected to fall below 2%, reflecting persistent domestic consumption weakness

- Fixed asset investment: decelerating to approximately 1.6%, weighed down by ongoing property sector drag

The production strength masks a domestic demand problem. If Chinese consumption remains subdued, the global growth impulse that export-oriented economies depend on is weaker than the headline industrial number suggests.

China’s split between strong industrial production and weak retail sales is the sharpest illustration of what PMI and GDP data from across Q2 2026 confirmed as a three-speed global economy: a US soft landing, broad Asian expansion, and a contracting eurozone that is the primary source of global PMI pessimism, each tier carrying different implications for the central bank decisions this week.

Thursday’s eurozone and UK purchasing managers’ index releases connect to a separate concern. The UK composite PMI is forecast at 51.7, down from 52.6, with the prior boost from frontloaded demand ahead of Iran conflict concerns expected to unwind.

The European Central Bank faces a stagflationary dynamic: energy-price-driven inflation rising even as underlying economic conditions weaken. Thursday’s PMI data will quantify whether that tension is intensifying or stabilising, with direct implications for how credible current rate-hike pricing is across all four economies covered this week.

The week’s verdict will be written in rate probabilities that shift by Friday close

By Friday close on 22 May, markets will have absorbed data from all four economies and recalibrated the rate probabilities that currently define each central bank’s June outlook.

| Central Bank | June Meeting Date | Current Hike Probability | Key Trigger This Week |

|---|---|---|---|

| BoJ | 15-16 June | ~78% | Friday CPI (core-core at 2.2%) |

| BoE | 18 June | ~35% | Wednesday CPI, Tuesday labour data |

| RBA | June | ~20% | Thursday employment data |

| Fed | June | Transitional | Wednesday FOMC minutes |

The highest-conviction call entering the week is the BoJ hike. The most uncertain is the Fed trajectory under Warsh, given the absence of direct policy communication from the new chair. The week’s release schedule runs as follows:

- Monday 18 May: China industrial production, retail sales, fixed asset investment

- Tuesday 19 May: UK labour market data (earnings, unemployment)

- Wednesday 20 May: UK CPI, FOMC minutes

- Thursday 21 May: Australian employment, eurozone and UK PMIs

- Friday 22 May: Japan national CPI, UK retail sales

This week will not resolve every open question, but it will narrow the range of plausible outcomes for June decisions across four major economies. That makes it one of the most consequential macro weeks of the first half of 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Market-implied probabilities and consensus forecasts are subject to change based on incoming data and evolving market conditions.