CURE and CLNE: the ASX ETFs Returning 25% in 2026

8 hrs ago

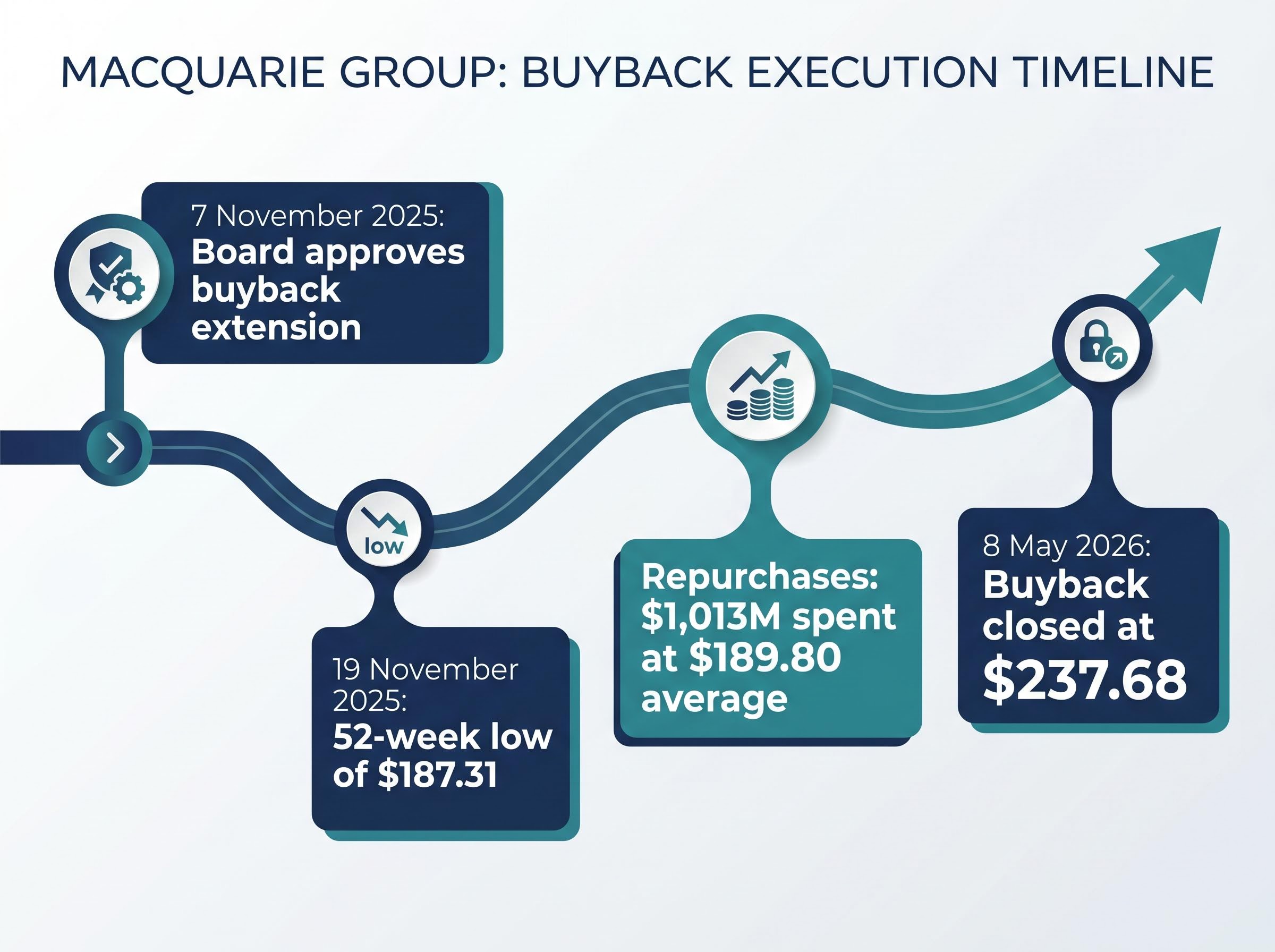

Macquarie Group spent $1,013 million buying back its own shares at an average price of $189.80 each. Then, when its board extended the programme in November 2025, the company simply stopped buying. By May 2026, with the share price sitting near $237, management closed the programme entirely and stated it had no plans to resume.

The closure was announced on 8 May 2026 alongside a record FY26 full-year result: net profit after tax (NPAT) of $4,847 million, up 30% year on year. The timing raises a straightforward but instructive question: why stop returning capital to shareholders when the company is generating more profit than ever?

What follows works through the reasoning behind Macquarie’s decision, explains the economics that make rising share prices a natural brake on buyback activity, and examines what the closure signals about how management intends to deploy capital in FY27 and beyond.

The sequence matters. Macquarie’s board approved the buyback extension on 7 November 2025. Twelve days later, on 19 November, the stock printed a 52-week low of $187.31. The programme executed its on-market repurchases in and around that trough, accumulating $1,013 million worth of shares at an average acquisition price of $189.80.

ASIC Regulatory Guide 110 on share buy-backs sets out the disclosure obligations companies must meet when conducting and closing on-market programmes under the Corporations Act 2001, including the requirement to notify shareholders of any material change to programme status.

By the time the FY26 result landed on 8 May 2026, Macquarie shares were trading at approximately $237.68, a gain of roughly 17.4% from the November low. The company confirmed it would not proceed with further repurchases under the extended programme, citing “significant business growth over recent periods, together with the prevailing market conditions.”

| Event | Date | Price / Amount |

|---|---|---|

| Board approves buyback extension | 7 November 2025 | N/A |

| 52-week low recorded | 19 November 2025 | $187.31 |

| On-market repurchases completed | November 2025 onwards | $1,013M at avg. $189.80 |

| Buyback programme formally closed | 8 May 2026 | Share price approx. $237.68 |

That gap between where the buyback was executed and where the stock trades now is the central tension of this analysis. The programme bought shares near the bottom; management stopped near the top.

The buyback closed against the strongest financial result in Macquarie’s history. FY26 NPAT reached $4,847 million, a 30% increase on FY25. The second half alone delivered $3,192 million, a record half-year profit and a 93% jump on the first half of the same year.

Q3 FY26 trading conditions already signalled the trajectory that would produce the record full-year result, with three of four divisions running substantially ahead of the prior year and the CET1 capital ratio sitting comfortably above regulatory minimums well before the May result was confirmed.

Record half-year profit: Macquarie’s 2H FY26 NPAT of $3,192 million was the strongest half-year result the company has reported, exceeding the first half by 93%.

Earnings per share rose to $12.77, up 30%. Return on equity (ROE) improved to 14%, from 11.2% in FY25. Net operating income grew 13% to $19,477 million, while operating costs increased a more modest 5% to $12,748 million, indicating widening margins. International operations contributed 68% of total income.

| Metric | FY25 | FY26 | Change |

|---|---|---|---|

| NPAT | $3,728M | $4,847M | +30% |

| EPS | $9.82 | $12.77 | +30% |

| ROE | 11.2% | 14% | +2.8 ppts |

| Net operating income | $17,237M | $19,477M | +13% |

| Operating costs | $12,141M | $12,748M | +5% |

The share price reflected this. Macquarie was up approximately 17% calendar year-to-date in 2026 against an ASX 200 that was down approximately 2.5% over the same period. The result explains why the share price recovered, and the share price recovery explains why continuing to buy shares at these levels is a structurally different proposition to the purchases made near $187.

The FY26 division-level breakdown reveals that Commodities and Global Markets surged 49% and Macquarie Capital rose 43%, a concentration of earnings growth in the higher-capital, higher-return segments that directly informs how management is weighing reinvestment options against continued buyback activity.

A share buyback is not inherently positive for shareholders. Its value depends on the price paid relative to the company’s worth. Understanding why matters for evaluating any buyback decision, not just Macquarie’s.

Buybacks are most accretive to remaining shareholders under three conditions:

When a share price rises, the inverse applies. The same capital budget retires fewer shares, the earnings-per-share accretion per dollar spent shrinks, and the opportunity cost of committing that capital to buybacks rather than reinvestment rises.

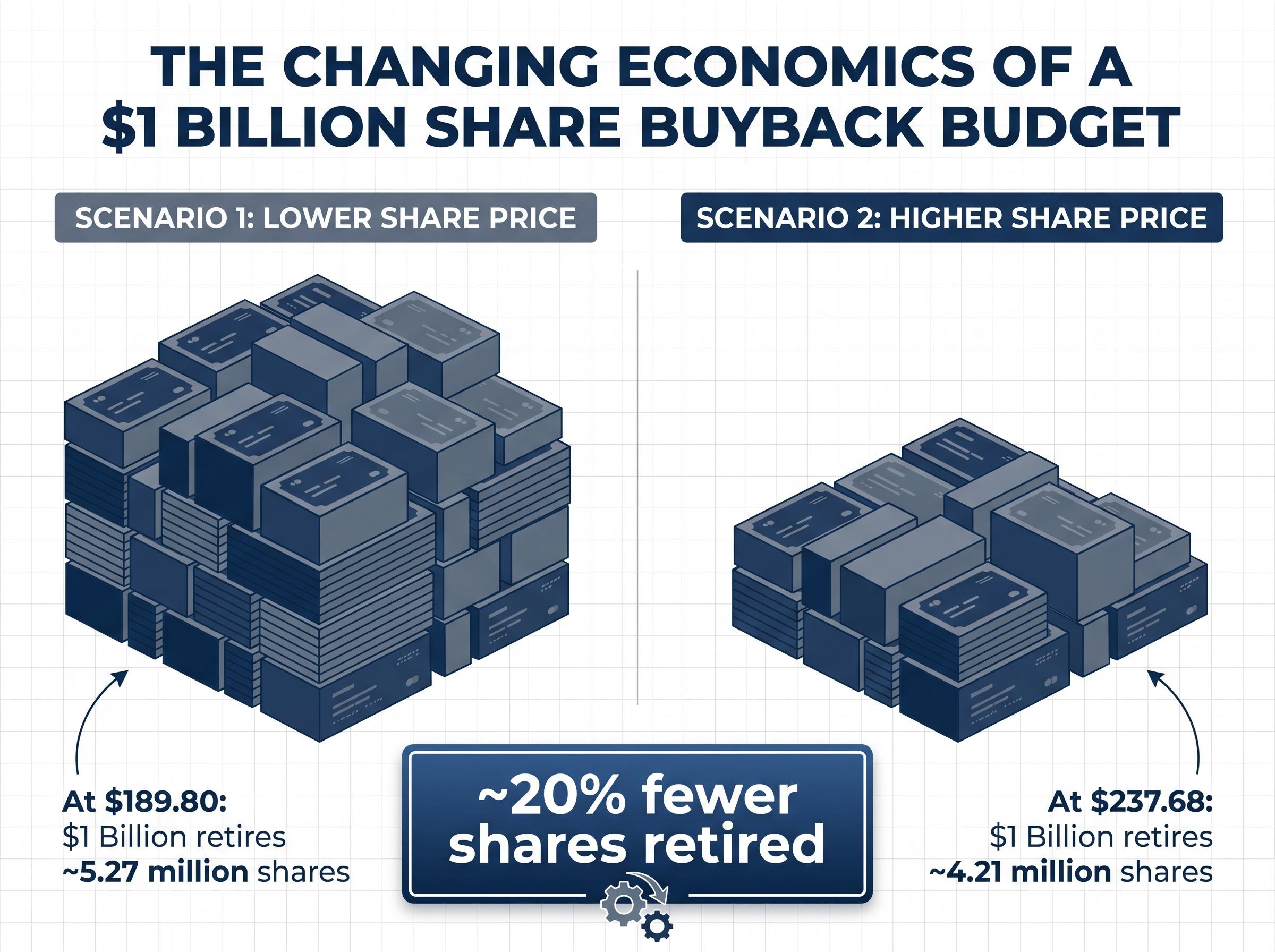

The numbers make this concrete. At $189.80 per share, $1 billion retires approximately 5.27 million shares. At $237.68, the same $1 billion retires approximately 4.21 million shares, roughly 20% fewer. The buyback’s mathematical benefit has compressed by a fifth, while the company’s organic growth options have expanded.

Macquarie’s official rationale: “Significant business growth over recent periods, together with the prevailing market conditions.”

That language is precise. It says the growth opportunities available to the business now exceed the return available from buying back shares at current prices. For retail investors, the lesson is transferable: a company stopping a buyback when its stock has re-rated is not necessarily a negative signal. It can reflect the same capital discipline that made the original programme attractive.

Macquarie’s stated rationale points toward preserving capital for organic growth and balance-sheet flexibility as it enters FY27. No specific acquisition programme has been announced. No dividend policy change has been flagged. The final dividend of $4.20 per share (35% franking, payable 2 July 2026) brings total FY26 dividends to $7.00 per share, implying a trailing yield of approximately 2.95% at $237.68.

Media and market commentary interpreted the decision through consistent lenses:

Some investors may question whether closing before fully utilising a board-approved extension signals excessive caution or a missed window for shareholder returns. If the stock continues to appreciate, the unspent buyback allocation would have been deployed at prices that still look attractive in hindsight.

The resolution sits in the evidence. No confirmed acquisition, no dividend increase, and no specific capital deployment initiative have been announced as of mid-May 2026. The decision reflects optionality rather than a specific redirect. Retaining that optionality amid strong growth conditions is consistent with Macquarie’s capital management history, where the company has repeatedly prioritised balance-sheet flexibility over formulaic capital return commitments.

The honest starting point is an evidence gap. No post-result acquisition, new infrastructure investment, or dividend policy change has been publicly announced as of mid-May 2026. The capital retained from the closed buyback programme remains unallocated to any specific identified purpose.

Macquarie’s 68% international revenue exposure provides the relevant backdrop. Organic growth in global infrastructure, asset management, and green energy transition financing represents the category of opportunity management has implicitly flagged through its official rationale.

For investors monitoring the situation, five signals are worth tracking:

For investors deciding whether the buyback closure changes their position sizing in MQG after a 17% calendar year-to-date gain, our full explainer on post-earnings decision frameworks covers the hold, trim, and wait logic in detail, including analyst-revision timing, the after-tax cost of trimming too early, and how to write conditional rules before results season rather than reacting in the moment.

The most value-accretive buybacks are executed at low prices during market dislocations. Macquarie bought near $189.80 when its stock was under pressure. The discipline to stop when the price reached approximately $237.68, a differential of roughly 25%, is the same discipline that made the original programme effective.

Classifying market signals before acting is the same discipline that makes buyback closures readable rather than alarming: management stopping repurchases near a 52-week high, after buying near a 52-week low, is a fundamentals-grounded response to changed conditions rather than a negative verdict on the stock’s long-term prospects.

There is an asymmetry worth acknowledging. Management’s closure decision incorporates a forward view on growth capital needs that is not yet public. Investors should weight that information gap when interpreting the signal, rather than treating the closure as a verdict on the stock’s value.

The practical principle: A buyback announcement is not inherently positive, and a buyback closure is not inherently negative. The price at which capital was deployed relative to the company’s value is the relevant measure.

Macquarie’s 30% profit growth provides the evidence base for management’s confidence in organic deployment over continued repurchase. Whether that confidence proves well-placed will be answered by FY27 results and the capital decisions that precede them.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding Macquarie’s capital deployment are speculative and subject to change based on market developments and company performance.

A share buyback is when a company repurchases its own shares from the open market, reducing the total shares outstanding and increasing earnings per share for remaining shareholders. The benefit is greatest when shares are purchased below their intrinsic value, as each dollar spent acquires a larger slice of future earnings.

Macquarie closed its buyback programme on 8 May 2026, citing significant business growth and prevailing market conditions, with the share price having risen roughly 25% from the average buyback price of $189.80 to approximately $237.68. Management indicated that organic growth opportunities now offered better capital deployment than continuing repurchases at elevated prices.

Macquarie spent $1,013 million buying back its own shares at an average price of $189.80 each, with purchases concentrated around the stock's 52-week low of $187.31 recorded on 19 November 2025.

Macquarie reported a record FY26 net profit after tax of $4,847 million, up 30% on FY25, with earnings per share rising to $12.77 and return on equity improving to 14% from 11.2% the prior year.

Investors should monitor ASX filings for any new buyback programme, dividend policy changes at the FY27 half-year result, ROE trajectory relative to the FY26 baseline of 14%, and any announcements relating to acquisitions or major capital commitments in global infrastructure, asset management, or green energy financing.