Lululemon’s corporate board filed a preliminary statement on Tuesday, officially urging shareholders to reject founder Chip Wilson’s nominees and escalating a highly contested Lululemon proxy campaign. The April 28, 2026 filing formalises a deep conflict between current leadership and the founder over the company’s financial trajectory and premium athletic identity.

Trading at $140.01 as of April 29, 2026, the apparel maker now faces a severe test of corporate governance that will define its strategic direction. The upcoming ballot represents a fundamental choice between maintaining the current oversight structure and fundamentally restructuring the brand’s approach to the market.

By examining the newly filed PREC 14A materials and the competing leadership visions, investors can understand exactly what is at stake in the upcoming shareholder vote. The dispute highlights specific disagreements over capital allocation, partnership strategies, and executive succession planning at one of the most prominent retail brands in the United States.

Board leadership aggressively defends current slate against activist push

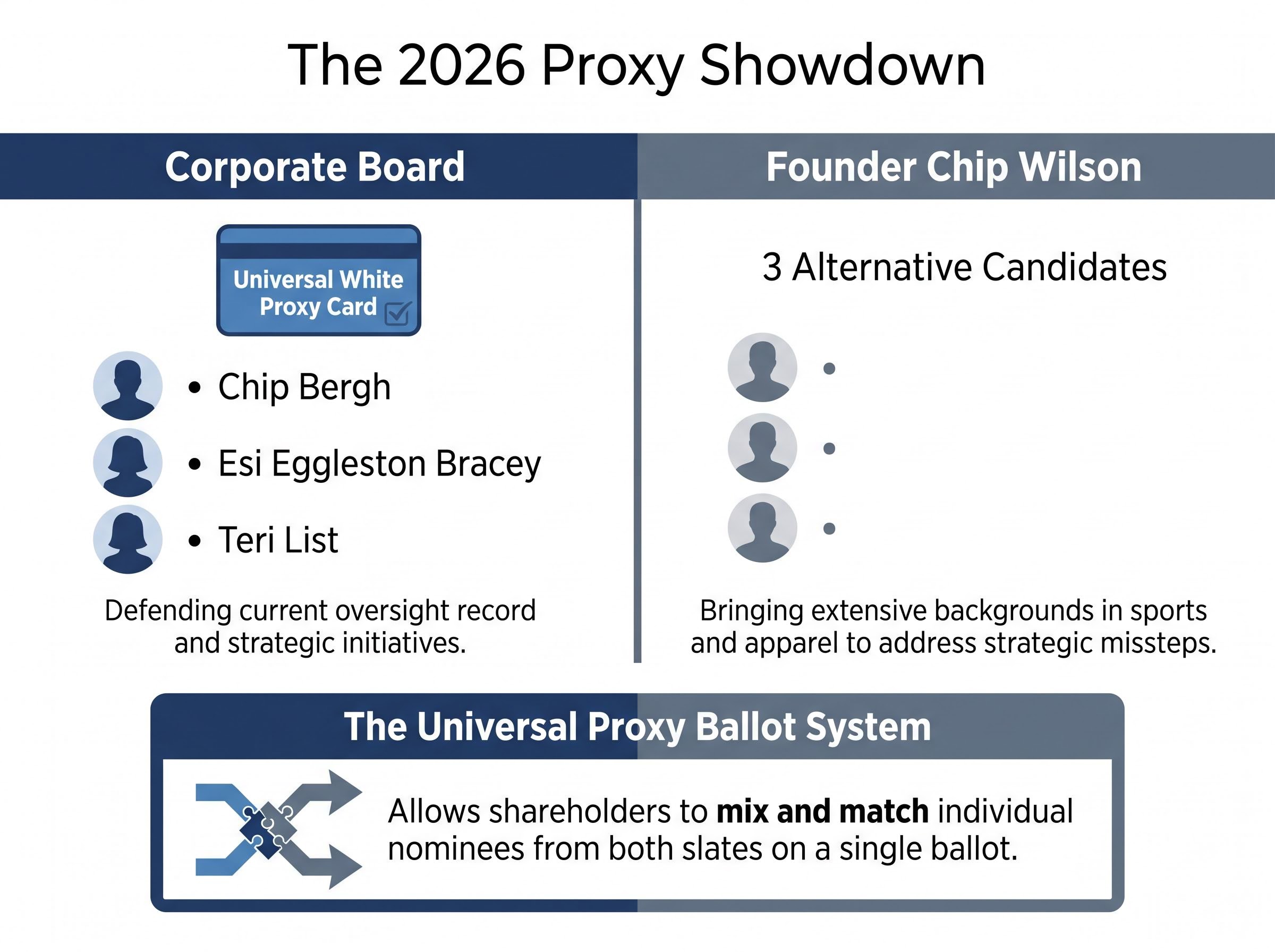

The corporate board is explicitly directing shareholders to support only their internal candidates, aggressively defending their oversight record. In their latest regulatory filing, leadership recommended voting exclusively for incumbent nominees Chip Bergh, Esi Eggleston Bracey, and Teri List using the universal white proxy card.

Board Sentiment on Nominees

“The board has concluded that adding the founder’s proposed candidates would disrupt ongoing strategic initiatives, and we strongly urge shareholders to reject efforts that could destabilise current leadership.”

The filing reveals the complete breakdown of settlement negotiations that began in December 2025. Despite the board eventually agreeing to support board declassification and refreshment efforts, the specific rejection of Wilson’s candidates halted any compromise.

The official SEC preliminary proxy statement formally details the specific timeline of these failed engagements, illustrating how fundamentally the two sides diverged on acceptable governance frameworks.

Settlement negotiations collapse over interview demands

The dispute ultimately fractured over procedural disagreements during the engagement process. According to the preliminary proxy statement, Wilson refused to allow the board to interview his nominees unless specific settlement conditions were met in advance.

The founder further complicated negotiations by alleging the board demanded an escrow deposit. Wilson claims this financial requirement was tied to a strict anti-criticism stipulation, a demand the board’s filing disputes as a mischaracterisation of standard standstill agreements.

When big ASX news breaks, our subscribers know first

Wilson targets staggered terms and private equity influence

Wilson has structured his offensive strategy around systemic governance complaints and a hand-picked slate of external industry veterans. His campaign argues that the current oversight structure insulates directors from shareholder accountability.

The founder is specifically targeting the company’s staggered director terms. According to campaign materials, his filings note that only 10% of S&P 500 organisations continue utilising a classified board structure, which prevents shareholders from voting out the entire board in a single year.

Academic research on classified board evolution confirms this sharp historical decline, noting that staggered structures have become increasingly rare among large publicly traded companies as institutional investors push for annual director accountability.

Further complicating the governance picture are alleged conflicts of interest. According to his campaign, Wilson has highlighted that four current oversight members maintain deep professional connections with Advent International, raising questions about private equity influence over the brand’s strategic direction.

To counter the incumbent leadership, Wilson has proposed three alternative candidates with extensive backgrounds in sports and apparel.

This external slate represents Wilson’s attempt to inject fresh product expertise into a boardroom he claims has lost touch with its core consumer base.

Understanding the universal proxy ballot system

For retail and institutional investors, the 2026 annual meeting will utilise a voting mechanism that fundamentally changes how contested elections operate. The universal proxy rule framework is a regulatory requirement implemented for publicly traded companies that places all competing candidates on a single ballot.

Historically, shareholders had to choose between the company’s complete proxy card or the activist’s complete card. The universal system functions differently by allowing investors to mix and match individual nominees from both the current board and the challenger’s slate.

Because of these regulations, the board is legally required to include the founder’s nominees on their ballot materials, even though they actively oppose them. This mechanism gives shareholders highly granular control over final board composition.

As of late April 2026, major proxy advisory firms like Institutional Shareholder Services and Glass Lewis lack current guidance on the Lululemon vote. Their forthcoming recommendations will heavily influence how institutional investors navigate this flexible voting system.

Controversial partnerships trigger multi-billion dollar equity plunge

The activist campaign rests heavily on the argument that strategic missteps have directly destroyed shareholder value. Wilson claims that corporate alliances with broad consumer entities have severely diluted the brand’s premium athletic image.

This ongoing brand dilution crisis has driven a sharp contraction in gross margins, reflecting a noticeable loss of pricing power amidst an increasingly competitive athletic apparel landscape.

Wall Street analysts have pointed specifically to the backlash surrounding the recent Disney collaboration. The founder described the partnership as completely misaligned with the company’s core identity, and analysts view this strategic move as an indicator of a board disconnected from its traditional customer base.

This perceived brand dilution correlates with severe financial underperformance across North and South American retail locations. The company has reported stagnation in comparable retail locations, prompting deep concern from institutional holders.

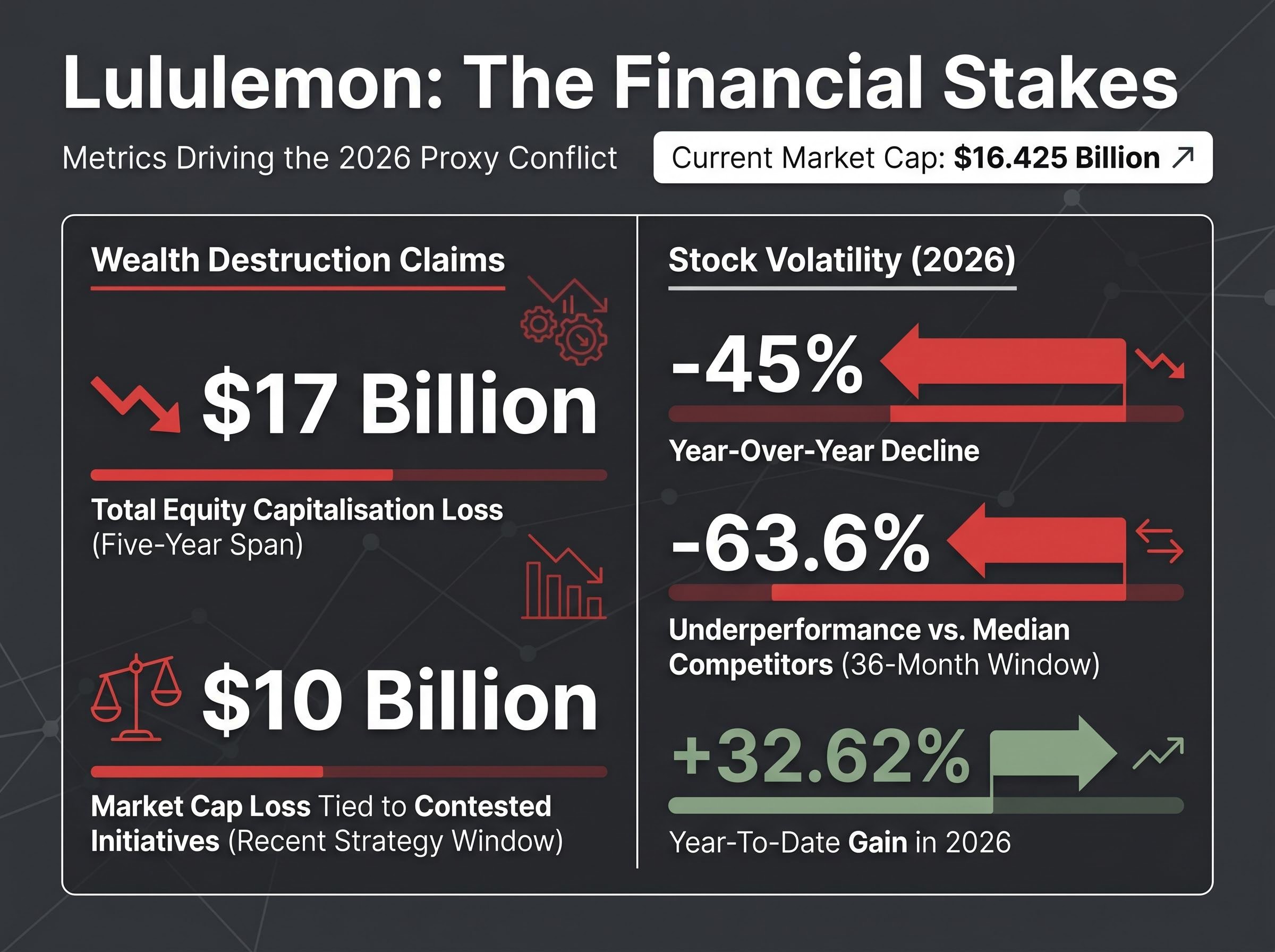

The financial damage linked to these decisions is extensive. Wilson’s campaign documents highlight specific capitalisation losses that outline the cost of the board’s current strategy.

| Timeframe | Metric | Reported Value |

|---|---|---|

| Five-Year Span | Total Equity Capitalisation Loss | $17 Billion |

| Recent Strategy Window | Market Cap Loss Tied to Contested Initiatives | $10 Billion |

| Eight Sequential Quarters | Comparable Retail Location Growth | Stagnant |

These metrics form the numerical foundation of the challenger’s argument that an immediate boardroom overhaul is required to halt further wealth destruction.

Market volatility surrounds incoming executive transition

Market sentiment remains highly reactive to the ongoing instability in the boardroom. The financial fallout from the proxy battle has created complex trading dynamics, with short-term optimism clashing against long-term deterioration.

Wilson has consistently argued that the current board lacks the product expertise necessary to guide the new executive team. This critique centres heavily on the ongoing CEO search.

The company is currently seeking a candidate to fill the top position. The founder asserts that placing a new executive under an underperforming oversight committee will only compound existing strategic errors.

Recent stock metrics illustrate the market’s conflicting reactions to the leadership transition and the activist campaign:

The stock has suffered a 45% year-over-year decline, reflecting deep operational concerns. According to campaign materials, the company recorded a 63.6% underperformance compared to median competitors over a thirty-six-month window. * In contrast, shares have posted a 32.62% year-to-date gain in 2026 as investors price in the possibility of a successful turnaround.

Institutional holders assessing these recovery prospects frequently draw comparisons to other retail turnaround initiatives, where targeted store innovations and operational efficiency programs have proven critical for restoring market confidence.

This volatility underscores how sensitive traders are to any developments in the ongoing proxy fight.

The impending corporate showdown will define Lululemon’s strategic future

The competing slates will finally face a shareholder vote at the 2026 annual meeting, setting the stage for a potentially radical alteration of the company’s leadership. With a total current market capitalisation of $16.425 billion, the financial stakes of this governance dispute are immense.

The final outcome remains highly uncertain. The major proxy advisory firms have yet to weigh in, leaving institutional voting intentions entirely unclear.

Whatever the result, the incoming executive transition in September will occur under intense public scrutiny. The new leadership team will inherit either an entrenched board focused on current strategies or a newly reconfigured oversight committee demanding immediate operational changes.

For readers wanting to review the complete timeline of negotiations and leadership demands, our full explainer on the Lululemon proxy fight details the proposed board declassification mechanisms and the specific retail expertise the alternative nominees offer.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.