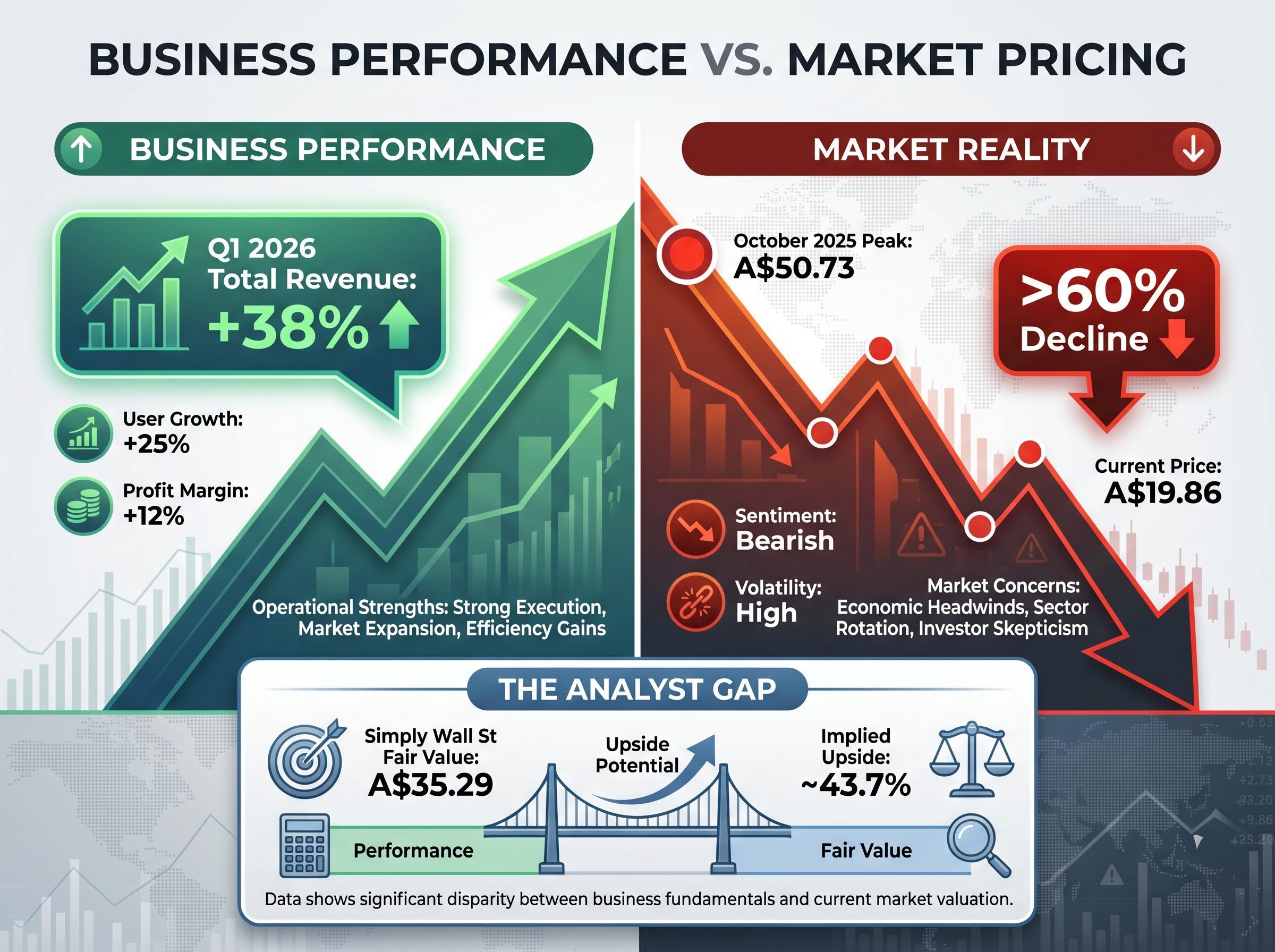

Life360 delivered a revenue beat on 11 May 2026, reporting Q1 revenue of $143.1 million against a consensus estimate of $137.3 million. The stock, however, is trading at A$19.86, more than 60% below its October 2025 peak of A$50.73. The Q1 update, released overnight, shows a business with 97.8 million monthly active users (MAU), 12 consecutive quarters of positive operating cash flow, and advertising revenue surging 329% year-on-year. The market’s response has been muted, leaving a sizeable gap between what analysts estimate the company is worth (consensus fair value of A$35.29 to A$35.66) and what investors are currently willing to pay. What follows unpacks what the Q1 numbers actually show, why the Life360 share price remains so far below analyst targets, what management is flagging about the second half of 2026, and what conditions would need to hold for a re-rating to materialise.

Revenue surging, share price lagging: the gap the market has not yet closed

Life360 reported Q1 2026 total revenue of $143.1 million, up 38% year-on-year. Subscription revenue reached $108.2 million (up 32%), while advertising revenue hit $19.7 million, a 329% year-on-year surge. Annualised monthly revenue climbed 32% to $517.9 million.

The contrast in one line: Revenue grew 38% year-on-year in Q1 2026. The share price has fallen more than 60% from its October 2025 peak.

This quarter marked the first time Life360 disclosed advertising revenue as a separate line item, signalling that the company’s second monetisation engine has reached sufficient scale to warrant standalone reporting. Management described paying circle additions in Q1 as record-breaking.

The three revenue lines in summary:

- Total revenue: $143.1 million, up 38% year-on-year

- Subscription revenue: $108.2 million, up 32% year-on-year

- Advertising revenue: $19.7 million, up 329% year-on-year

For ASX investors, the revenue beat resets the baseline for what Life360’s business is actually generating, making the price-to-performance gap the defining question at current levels.

When big ASX news breaks, our subscribers know first

What the user and subscriber numbers reveal about growth durability

Life360’s subscription model runs on three levers: monthly active users at the top of the funnel, paying circles (households that convert to a paid plan) in the middle, and average revenue per paying circle (ARPU) at the monetisation layer. All three grew in Q1.

| Metric | Q1 2026 Figure | Year-on-Year Growth |

|---|---|---|

| Monthly Active Users | 97.8 million | 17% |

| Paying Circles | 3 million | 27% |

| Average Revenue per Paying Circle | Not separately disclosed | 7% |

Global MAU reached 97.8 million, with net additions of 1.9 million in the quarter. Paying circles grew to 3 million, also adding 1.9 million net in Q1. Android registration funnel issues had suppressed MAU growth during the de-rating period, though management has indicated these are being resolved.

From free users to paying subscribers: the conversion engine

Paying circles currently represent approximately 27% of total circles, a penetration rate that reflects both meaningful traction and considerable runway for further conversion. The fact that net MAU additions and net paying circle additions matched in Q1 suggests the conversion funnel is functioning efficiently.

The 7% ARPU increase indicates that premium tier migration is working. A mix shift toward higher-priced tiers across select international markets is supporting the revenue per user trajectory, compounding on top of the volume growth above.

Why a 60% share price decline is not the same as a 60% deterioration in the business

Life360 peaked at approximately A$50.73 on 28 October 2025. At A$19.86, the stock has fallen roughly 60%. Yet every major operational metric, revenue, users, subscribers, and cash flow, improved in Q1 2026.

This disconnect is common among high-growth stocks and relates to how valuation multiples work. A company’s share price reflects not just current earnings but the multiple investors assign to expected future earnings. When interest rate expectations shift, when investor risk appetite narrows, or when operational hiccups emerge, that multiple can compress sharply, even if the underlying business continues to grow.

The ASX growth stock sell-off that compressed forward P/E multiples by 26%-64% across the sector between October 2025 and April 2026 was driven primarily by sentiment rather than earnings deterioration, with six of ten cohort stocks maintaining stable or improving earnings trajectories throughout the decline.

Six identifiable factors contributed to Life360’s de-rating:

Operational issues:

- Android registration funnel problems that suppressed MAU growth

- The Tile hardware retail exit, which created near-term revenue headwinds

- Operating expense escalation (46% year-on-year in Q1) and gross margin compression (from 81% to 77%)

Macro and valuation factors:

- Broader growth stock multiple resets across the technology sector

- Momentum cooling, with a year-to-date return of approximately -38.82% as of early May 2026

- Privacy and regulatory scrutiny on location data adding a persistent overhang

Simply Wall St estimates fair value at A$35.29 (updated May 2026), implying approximately 43.7% upside from the current price of A$19.86.

The three-year total shareholder return of approximately 3.4x provides context: Life360 has delivered material long-term value, but the recent decline reflects a repricing of expectations, not a collapse in the business itself. For ASX investors newer to evaluating technology companies, this distinction between price movement and business health is where much of the analytical value lies.

The cost story: where the profitability gap is coming from and what management says about it

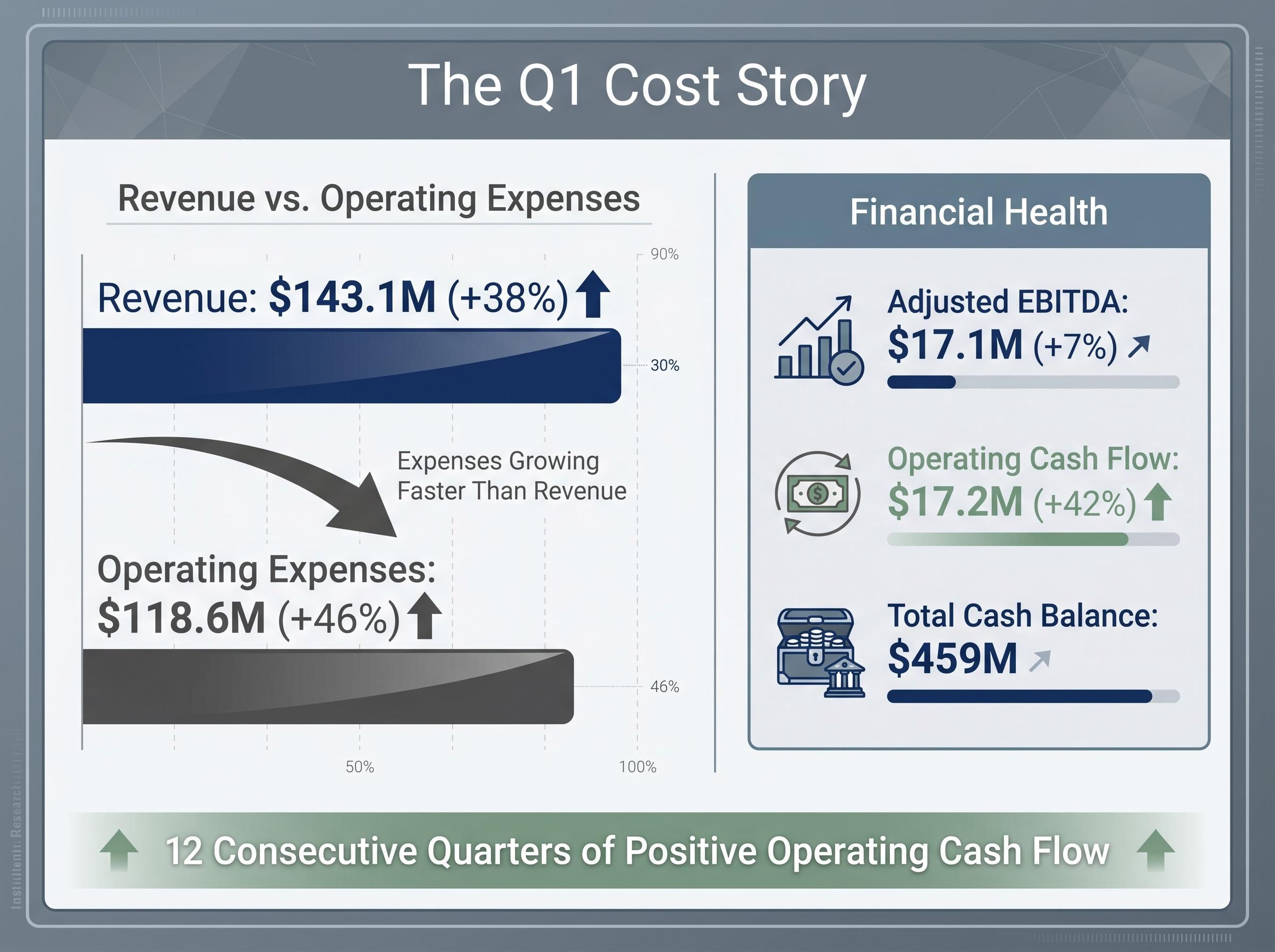

Revenue grew 38% in Q1. Adjusted EBITDA grew 7%. That gap is the contested part of the Life360 thesis.

Life360’s Q4 2025 results marked the company’s first full-year net profit in its history, with adjusted EBITDA surging 105% and operating cash flow up 172% year-on-year, establishing the profitability baseline against which Q1 2026’s cost escalation is now being measured.

| Metric | Q1 2026 | Year-on-Year Change |

|---|---|---|

| Revenue | $143.1M | +38% |

| Operating Expenses | $118.6M | +46% |

| Adjusted EBITDA | $17.1M (12% margin) | +7% |

| Operating Cash Flow | $17.2M | +42% |

| Gross Margin | 77% | Down from ~81% |

Operating expenses of $118.6 million (up 46%) reflect headcount growth from business expansion, costs associated with the Nativo integration, and increased growth-oriented media spending. The distinction between adjusted EBITDA growth (7%) and operating cash flow growth (42%) is worth noting: cash generation is healthier than the headline EBITDA figure suggests. Life360 ended Q1 with $459 million in cash, up from $288.6 million a year earlier. This was the 12th consecutive quarter of positive operating cash flow.

What management needs to deliver in H2 2026

CEO Lauren Antonoff has guided that revenue growth will accelerate in H2 2026 as advertising enters its peak seasonal period and the front-loaded investment cycle normalises. Two specific operational catalysts have been flagged: the Android registration funnel fix and the fading of the Tile hardware exit headwind.

Whether the 46% opex growth is a one-period anomaly or a structural shift in the cost base will largely determine whether the H2 margin expansion story holds. Q3 2026 is the quarter where that thesis faces its first real test.

The strategic bets that the share price may not be fully reflecting

The 329% advertising revenue surge is more than a growth metric. It represents evidence that Life360 has built a second monetisation engine on top of its subscription base, with the Nativo integration serving as a key enabler. At $19.7 million in Q1, advertising is still a fraction of total revenue, but the trajectory from a small base is the kind of compounding that consensus models may not yet fully capture.

Advertising revenue: $19.7 million in Q1 2026, up 329% year-on-year, the first quarter this line item was reported separately.

Three strategic bets underpin the longer-term outlook:

- Advertising platform scale: A 97.8 million MAU base gives Life360 the audience density to support a viable advertising platform, described by management as reaching the scale threshold for commercial viability

- Partnership-driven platform utility: The Uber partnership (announced 17 February 2026) deepens household utility beyond location tracking, extending the platform into adjacent use cases

- AI-enabled super app evolution: CEO Lauren Antonoff has cited AI as enabling faster product development toward a family super app, leveraging a user base that competitors cannot quickly replicate

If advertising revenue continues compounding while the subscription business maintains its growth trajectory, the stock could re-rate on the emerging revenue line alone, even before the core subscription business is fully valued.

What a re-rating would actually require from here

The gap between A$19.86 and analyst consensus of A$35.29 (per Simply Wall St, updated May 2026) implies approximately 43.7% upside. Motley Fool Australia rated Life360 a “strong buy” as of 7 May 2026. Rask Media commentary published on 12 May 2026 characterised the company as holding a stronger competitive moat than current market sentiment implies, while also noting that sustained profit growth is what investors will require to support a meaningful re-rating.

The bull case conditions:

- Opex normalisation in H2 2026, with margin expansion visible by Q3

- Continued subscriber growth and paying circle penetration above 27%

- Gross margin recovery toward the 80% range

- Advertising revenue maintaining its triple-digit growth trajectory

The risks that could keep the discount in place

- Privacy and regulatory scrutiny of location data remains a persistent multiple overhang

- Competition from Apple Find My and the Google ecosystem provides zero-cost alternatives to Life360’s core functionality

- Execution risk if the H2 2026 front-loaded investment cycle does not normalise as management has guided

- The H2 acceleration thesis remains unproven until Q3 2026 results provide confirmation

The OAIC corporate plan for 2025-26 explicitly identifies new surveillance technologies, including location data tracking in apps, as a priority regulatory focus area, providing a formal basis for the scrutiny that continues to weigh on location-data businesses listed on the ASX.

For ASX investors weighing whether the 60% decline represents a buying opportunity or a value trap, these conditions and risks form the specific evidential tests that the next two quarters will answer.

Strong numbers, but the proof will come in H2

Q1 2026 shows a business with genuine operational momentum: 38% revenue growth, 97.8 million users, and a 329% surge in advertising revenue. The 12th consecutive quarter of positive operating cash flow and a $459 million cash balance provide meaningful balance sheet insulation while the investment cycle matures.

The share price, however, will require sustained profit growth, not just revenue growth, to close the gap to analyst fair value. Q3 2026 will be the first real test of management’s H2 acceleration thesis, making it the next major inflection point for the stock.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Forward-looking statements regarding H2 2026 performance are based on management guidance and are subject to change based on market developments and company performance.