Goldman Sees Contrarian Buy Signal in KOSPI Foreign Selloff

2 mins ago

South Korea’s KOSPI is now priced as if the Global Financial Crisis is happening again. The index’s forward price-to-earnings ratio (forward P/E), the price investors pay today per unit of expected earnings over the next 12 months, has fallen to its lowest level since 2008-2009. The discount to global equities has widened to 55%, a figure that has not appeared since credit markets froze and global earnings collapsed. The crisis conditions that originally justified those multiples have not arrived.

Goldman Sachs published a stress-test note on 4 July 2026, the day after the KOSPI fell 3.8% in a single week and MSCI Korea dropped 5.5%. Rather than confirming the bearish narrative, the bank’s analysis reached a conclusion that cuts against the market’s own pricing: even if Korean corporate earnings fall by a third, history-anchored arithmetic still implies an index level above where the KOSPI trades today.

Here is how that stress test was constructed, what the valuation gap actually means, why the earnings picture complicates the bearish case, and where the genuine risks sit for anyone trying to make sense of the KOSPI forecast right now.

The week ending 3 July 2026 delivered a sharp, concentrated selloff across Korean equities:

Those are significant weekly moves. But the price decline was the mechanism, not the story.

MSCI Korea’s June rejection from the Developed Market watchlist removed a key foreign capital catalyst that had supported inflows through the earlier stages of the year’s rally, adding a structural overhang to the index’s valuation at the precise moment selling pressure intensified.

The story is what the decline unlocked. The KOSPI’s forward P/E has now fallen to its lowest reading since the 2008-2009 Global Financial Crisis. Global investors are currently paying roughly twice as much per dollar of expected earnings for the average MSCI AC World company as they are for the average Korean company, and that gap has not been this wide since the world economy was in freefall.

The difference between then and now: the comparable macro shock that accompanied the original GFC multiples has not materialised. The valuation arrived first. The question is whether the crisis follows, or whether the market has overshot.

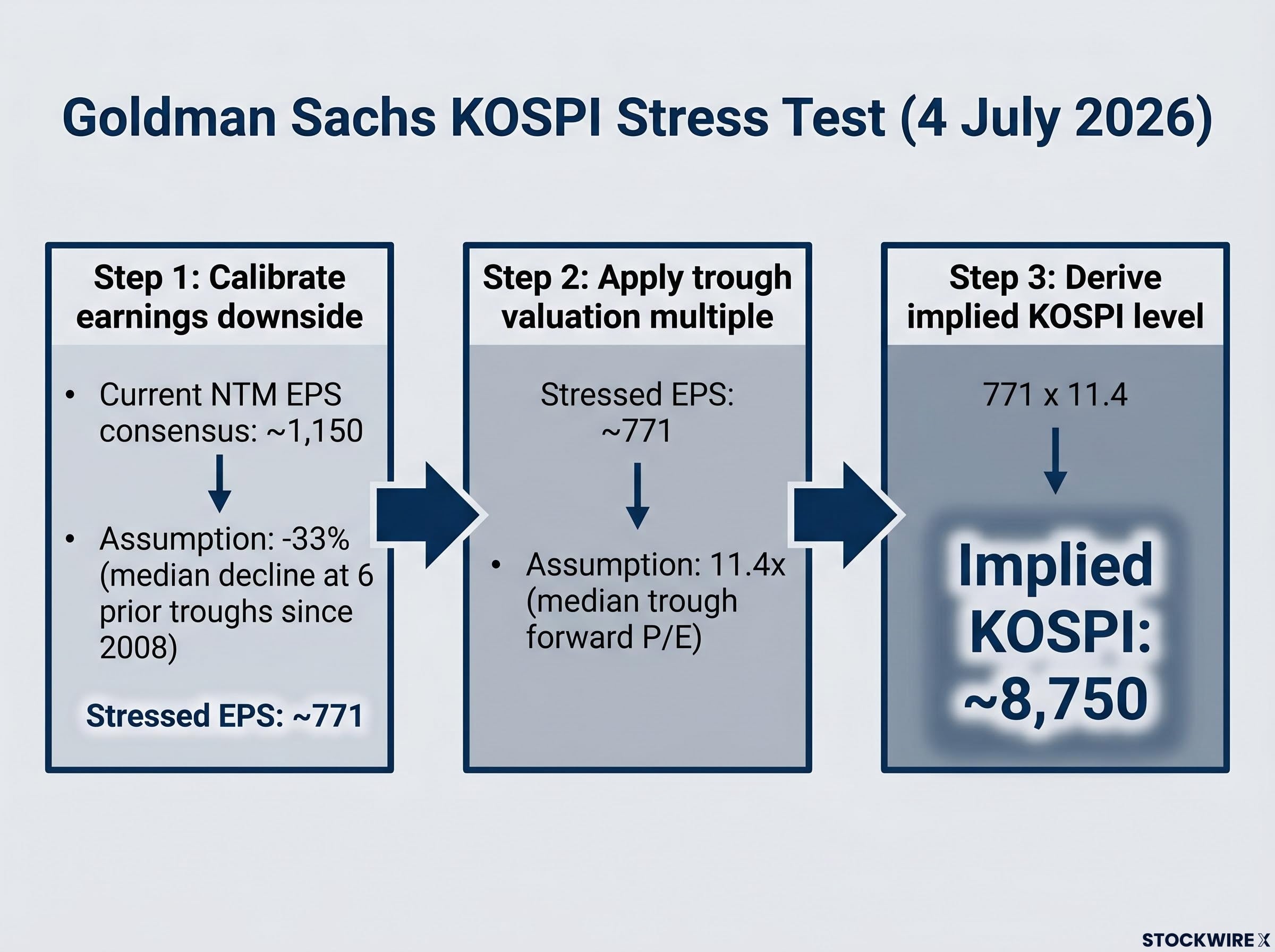

Goldman’s 4 July note laid out a three-step framework, built on six prior market troughs in Korean equities since 2008, designed to answer a specific question: how bad would things need to get before the KOSPI’s current price is justified?

| Step | Input | Assumption | Output |

|---|---|---|---|

| 1. Calibrate earnings downside | Current NTM EPS consensus: ~1,150 | Median earnings decline at six prior troughs: -33% | Stressed EPS: ~771 |

| 2. Apply trough valuation multiple | Stressed EPS: ~771 | Median trough forward P/E across same six episodes: 11.4× | Implied index level |

| 3. Derive implied KOSPI level | 771 × 11.4 | No re-rating or normalisation assumed | ~8,750 |

The framework is deliberately conservative. Goldman used the median outcome of six historical worst cases, not a best-case or consensus assumption. The 11.4× multiple reflects what investors were willing to pay at the bottom of prior cycles, not during recoveries.

The implied stress-case KOSPI level is approximately 8,750. The current KOSPI trades below that figure, meaning the market is already pricing in an outcome worse than the median of six post-2008 troughs across both earnings and valuations simultaneously.

The KOSPI would have to sustain a historically severe simultaneous collapse in both earnings and valuation multiples before reaching levels the market has already priced in. That is a structurally unusual setup.

Forward P/E is straightforward in principle: it measures what investors pay today for each unit of earnings a company is expected to generate over the next 12 months. A lower P/E means investors are paying less per unit of expected profit. A 55% discount to the global benchmark means Korean equities would need to deliver roughly double the earnings yield of the average global company to attract equivalent capital.

That discount is large. But what makes it structurally remarkable is the historical company it keeps.

The last time forward P/Es reached comparable levels, two conditions held simultaneously:

Neither condition fully applies today. Yet the KOSPI’s valuation multiple has returned to those levels.

From its March 2009 low to its 2011 peak, the KOSPI more than doubled. GFC-level multiples have, in the past, preceded exceptional medium-term returns rather than signalling permanent impairment. That precedent is informative, but it is not deterministic: the conditions enabling that recovery may not fully replicate in the current environment.

For investors wanting to understand the chaebol governance structures, payout culture, and reform catalysts that underpin this persistent undervaluation, our dedicated guide to the Korea Discount covers the Corporate Value-Up programme and the practical mechanics of accessing the Korean market across ETFs, direct KRX trading, and domestic brokerage accounts.

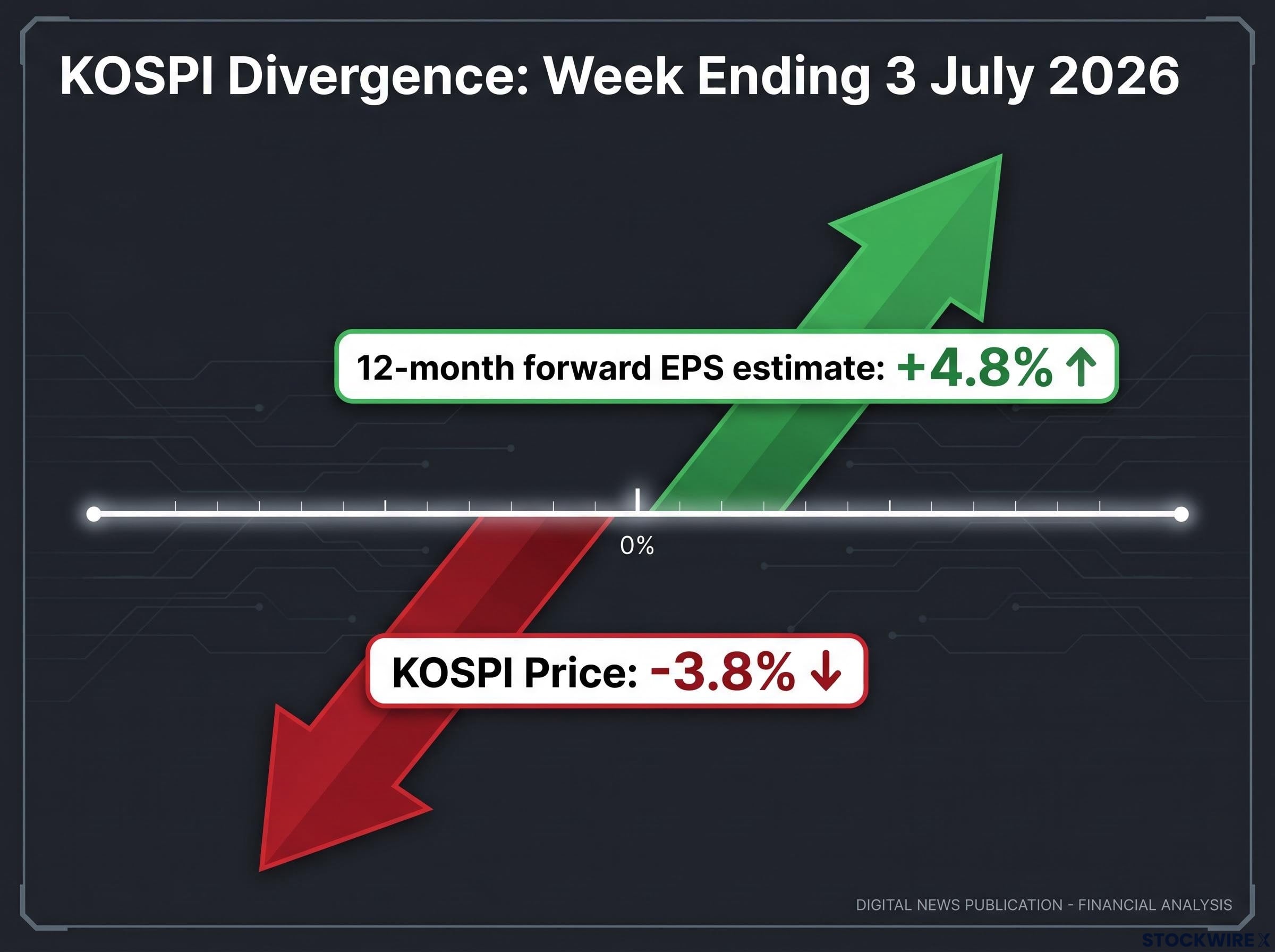

Here is the data point that should stop any reflexive bearish reading in its tracks.

In the very week that the KOSPI shed 3.8%, analysts revised the index’s 12-month forward earnings-per-share estimate 4.8% higher.

Prices down. Earnings up. The entire valuation compression came from multiple contraction, not from deteriorating fundamental expectations. Analysts closest to company-level fundamentals were, if anything, more optimistic about near-term profitability even as the index fell.

The sector-level data sharpens the picture:

| Sector | Performance vs. KOSPI | Earnings revision direction |

|---|---|---|

| Technology | -7.6% | Mixed |

| Insurance | -5.7% | Mixed |

| Retail | -5.7% | Mixed |

| Chemicals | Underperformed | Sharpest downward revision |

| Banking | Outperformed | Positive |

| Securities | Outperformed | Positive |

| Leisure | Outperformed | Largest upward revision |

When prices fall and earnings estimates rise simultaneously, the gap is being driven by sentiment and flows rather than corporate fundamentals. That changes the question from “is the business deteriorating?” to “is the risk premium justified?”

Goldman’s framework is useful. It is not infallible. Four categories of caveat deserve weight:

Semiconductor concentration risk sits at the centre of the KOSPI’s vulnerability profile: Samsung Electronics and SK Hynix together account for roughly half the index by capitalisation, a structure that allowed a single unverified media report on HBM4 production schedules to erase nearly 10% of index value in one session just days before this week’s selloff.

Korea has long traded at a structural discount to global peers for reasons that sit outside any single business cycle: corporate governance concerns, chaebol-dominated index composition, geopolitical risk from the Korean peninsula, and historically low shareholder payout ratios.

These factors do not vanish when valuation multiples recover cyclically. They set a ceiling on how far any re-rating can run, which means a portion of the 55% discount is likely permanent and any recovery trades against that structural headwind.

The stress test sets a history-anchored floor, but persistent structural discounts and ongoing technical selling mean the floor can feel very far away in the short term. Time horizon matters enormously in how much weight to give Goldman’s conclusion.

Goldman’s analysis establishes one thing with quantitative rigour: the current KOSPI level is already pricing in an outcome worse than the median of six historical worst cases across earnings and valuations simultaneously. The implied stress-case level of approximately 8,750 sits above where the index trades.

That leaves two historical resolution paths:

Emerging market valuations have fallen to the 10th percentile of their 35-year recorded history relative to US equities, a starting point that Morningstar’s research links to EM outperformance exceeding 50% over subsequent five-year periods; the KOSPI’s own compression sits within that broader dynamic, though Korea’s structural discount means it has lagged even the EM recovery.

Goldman’s stress test, by construction, explored the first path and still found valuation-based upside. The bank’s implicit position favours the second.

For anyone with a view on Korean equities, the framework reframes the question from “is this cheap?” (it demonstrably is) to “what would have to be true for it to stay this cheap?” That is a more tractable and honest starting point for any investment decision.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

The KOSPI's forward price-to-earnings ratio has fallen to its lowest level since the 2008-2009 Global Financial Crisis, placing MSCI Korea at a 55% discount to the MSCI AC World index, a gap not seen since global credit markets froze.

Goldman Sachs published a stress-test note on 4 July 2026 showing that even if Korean corporate earnings fell by 33% and valuation multiples compressed to historical trough levels, the implied KOSPI level of approximately 8,750 still sits above where the index currently trades.

The KOSPI dropped 3.8% and MSCI Korea fell 5.5% over the week, with the decline driven by multiple contraction rather than deteriorating earnings; analysts actually revised 12-month forward EPS estimates 4.8% higher during the same period, pointing to sentiment and flow-driven selling rather than a fundamental breakdown.

The Korea Discount refers to the persistent structural gap between Korean equity valuations and global peers, driven by corporate governance concerns, chaebol-dominated index composition, geopolitical risk from the Korean peninsula, and historically low shareholder payout ratios; these factors set a ceiling on any cyclical re-rating.

For the KOSPI's current price to be fundamentally justified, Korean corporate earnings would need to fall more severely than the median of six post-2008 historical worst cases while valuation multiples simultaneously compressed to trough levels, a combination the market has already priced in but which has not materialised in the underlying business data.