KOSPI Drops 10% as Crowded AI Trade Unwinds Across Global Markets

13 hrs ago

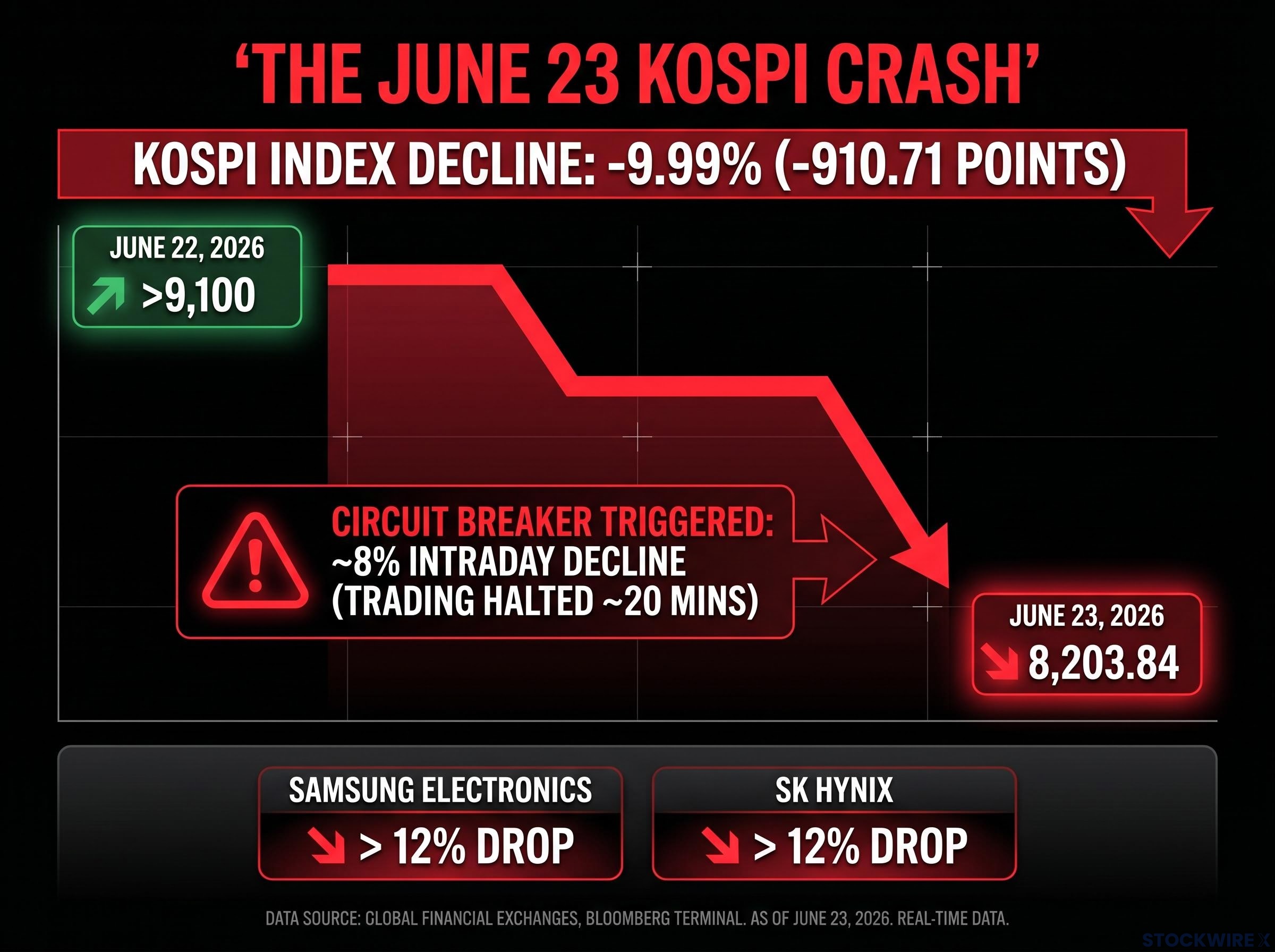

The KOSPI set an all-time high above 9,100 on Monday, 22 June. One session later, it lost nearly 10%. The reported trigger was a single newspaper article about a chip production schedule.

A 94.67% year-to-date rally had compressed every margin of safety out of valuations. When Chosun Biz reported that SK Hynix was decelerating its HBM4 expansion timetable, the market did not process the claim as a nuanced production adjustment. It processed it as confirmation that the AI hardware supercycle might not be linear, and in a market priced for perfection, that was enough.

What follows explains what the architecture of the KOSPI made inevitable, why one media report could produce a near-10% decline, and what the episode tells you about concentration risk in any AI-exposed market.

The KOSPI closed above 9,100 for the first time on 22 June 2026. The index ended the following session at 8,203.84, a loss of 9.99% and 910.71 points in a single day of trading.

The proximate cause was a Chosun Biz report alleging that SK Hynix had pulled back on HBM4 capacity build-out and was redirecting resources toward higher-margin general-purpose DRAM, a move reportedly tied to softer demand projections for Nvidia’s upcoming Rubin-generation chip. Samsung Electronics and SK Hynix shares each shed more than 12%, with the scale of those declines prompting Korea Exchange to activate its circuit-breaker mechanism and suspend trading across the market for around 20 minutes after the index had dropped beyond the 8% intraday threshold.

Losses deepened after trading resumed. The circuit breaker slowed the fall; it did not interrupt the mechanics driving it.

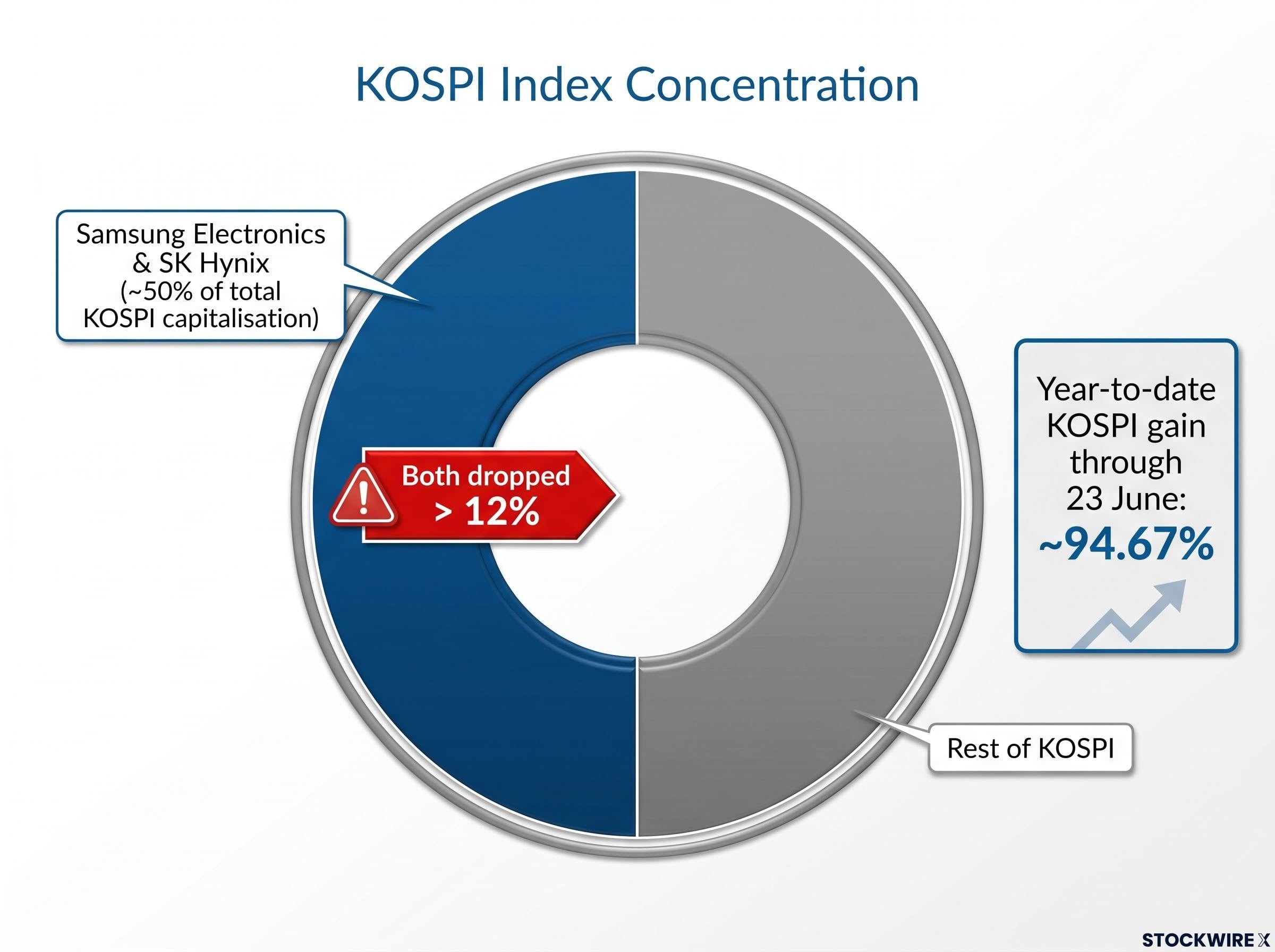

Samsung Electronics and SK Hynix together account for approximately 50% of total KOSPI capitalisation. That single figure explains almost everything about 23 June.

When two stocks representing half an index each fall more than 12%, the mathematical outcome is a near-10% index decline before any contagion, any panic, or any secondary selling enters the picture. The result was predetermined by the index architecture the moment those two stocks began falling.

Structural concentration risk: Owning a broad KOSPI index fund or ETF means holding, in effect, a leveraged bet on two semiconductor companies. Diversification within the index is partially an illusion.

Passive funds, index trackers, and ETFs tracking the KOSPI had no discretionary option. As the index fell, these vehicles were compelled to sell mechanically, regardless of any view on underlying fundamentals. The selling was not a choice. It was a feature of the product design.

HBM stands for High Bandwidth Memory, the specialised chip architecture that serves as the strategic core of AI memory infrastructure. SK Hynix and Samsung together control the vast majority of global HBM supply, which is why any perceived slowdown in this category carries outsized signal value for AI investors worldwide.

According to Chosun Biz, SK Hynix was winding back its HBM4 ramp-up and reducing planned production volumes, with the report linking this decision in part to revised demand assumptions for Nvidia’s Rubin chip. In its own public statements, SK Hynix stressed the strength of its position at the frontier of advanced HBM technology. Meanwhile, Nvidia’s own communications pointed in a different direction entirely.

| Chosun Biz claim | Nvidia / industry reporting |

|---|---|

| SK Hynix decelerating HBM4 expansion | SK Hynix publicly reaffirmed leading HBM position |

| Partly linked to revised Rubin demand forecasts | Nvidia indicated Rubin mass production proceeding aggressively |

| Pivot toward general-purpose DRAM suggested | Trial production in June 2026, initial shipments targeted Q3 2026 |

The conflict between these two framings is the point. The 23 June selloff may have been a market reacting to a worst-case interpretation of ambiguous information. That is a different, and potentially more actionable, conclusion than “AI demand is falling.”

Once the initial drop began, most of the selling was not chosen. It was compelled. Three mechanical channels turned a semiconductor sentiment shock into a market-wide cascade:

Trading was halted for roughly 20 minutes under the exchange’s circuit-breaker rules. It did not halt the underlying dynamic. When the market reopened, the same mechanical forces resumed.

Korea’s financial regulator had issued specific cautions about leveraged ETFs and the volatility amplification they create in concentrated markets, in the period immediately preceding 23 June. The timing matters: the structural vulnerability was identified, not overlooked. But identification is not the same as mitigation at sufficient speed. The warning arrived; the exposure did not reduce before the shock did.

The KOSPI did not crash in isolation. The Nasdaq 100 had surrendered all of the ground it had gained during June by the point of the Korean selloff, and the largest AI beneficiaries were already well off their peaks:

The question is whether the South Korean event was a localised fragility failure or a concentrated expression of a broader AI-valuation recalibration already underway across global markets. The evidence suggests both.

Evercore ISI analyst Julian Emanuel argued that megacap technology names would regain favour once results season validated the underlying earnings case, and flagged that investors should expect a period of choppiness and negative sentiment to run its course before conviction in the largest technology stocks is restored.

Micron had posted gains of more than 300% year-to-date according to Bloomberg data, making it the clearest short-term read on AI memory sentiment. Bloomberg Intelligence forecast that its fiscal Q3 revenue would come in around 18% above the company’s own guidance, on the back of firmer chip pricing. Those results are expected 25 June 2026. If Micron delivers, it complicates the narrative that AI memory demand is softening. If it disappoints, the Chosun Biz report starts to look less like an outlier and more like a leading indicator.

The KOSPI remains up approximately 94% year-to-date, even after 23 June. The all-time high was set one session before the crash. A reported production schedule adjustment for one chip category produced a near-10% index decline. That disproportion is the story.

| Trigger event | Market response |

|---|---|

| Reported HBM4 schedule adjustment | 9.99% index decline (910.71 points) |

| Single media report, unconfirmed | Circuit breaker activated at 8% threshold |

| No confirmed earnings miss or demand collapse | Two largest stocks fell more than 12% each |

The fragility stack that produced this outcome is not unique to Korea. It is a portable analytical framework:

Any market where these three layers coexist carries the same latent risk. At all-time highs, that risk is maximised: every holder is in profit, no latent buyers are waiting at a perceived “fair value,” and the psychological and structural conditions for rapid unwinding are at their peak.

The gap between the severity of the news and the severity of the market response is the most precise measure of how much speculative froth had been priced in. For any investor still holding Korean equity exposure, that gap is the calibration tool that matters most.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The immediate trigger was a Chosun Biz report claiming SK Hynix was slowing its HBM4 expansion and pivoting toward general-purpose DRAM, partly due to revised demand forecasts for Nvidia's Rubin chip. Because Samsung Electronics and SK Hynix together make up roughly 50% of KOSPI capitalisation, their combined 12%-plus declines mathematically produced a near-10% index collapse before broader panic or contagion even entered the picture.

HBM4 (High Bandwidth Memory 4) is the next generation of specialised memory architecture that powers AI hardware, and SK Hynix and Samsung together control most of the world's supply. Any perceived slowdown in HBM production carries outsized signal value for AI investors globally, which is why a single report about a schedule adjustment was enough to trigger a market-wide selloff in Korea.

Korea Exchange activated its circuit breaker and suspended trading for around 20 minutes after the KOSPI dropped beyond the 8% intraday threshold. The halt slowed the decline but did not stop it; when trading resumed, the same mechanical forces, including margin calls, leveraged ETF rebalancing, and passive fund selling, continued to push the index lower.

When two stocks represent approximately 50% of an index's total capitalisation, a 12%-plus decline in both produces a near-10% index fall through pure arithmetic, before any secondary selling or panic occurs. Passive funds and ETFs tracking the index then compound the damage by selling mechanically as the index falls, with no discretion over fundamentals.

The episode is a portable framework for any concentrated, leverage-heavy market: index design dominated by a few stocks, elevated margin debt converting volatility into forced selling, and daily-rebalancing ETFs adding programmatic downward pressure. At all-time highs, this fragility stack is maximised because no latent buyers are waiting at a perceived fair value and every holder is already in profit.