BofA Lifts Stoxx 600 to 630, but Proof Waits Until 2027

8 mins ago

Barclays economists Ruben Segura-Cayuela and Evelyn Herrmann are making a call that cuts against the ECB’s own reading of the current energy shock: the Iran-linked oil disruption is structurally less dangerous than Frankfurt believes, and that divergence suggests the deposit rate will settle at or beneath 2% before 2027 draws to a close. The forecast has two parts, and the part most investors will focus on is the less important one.

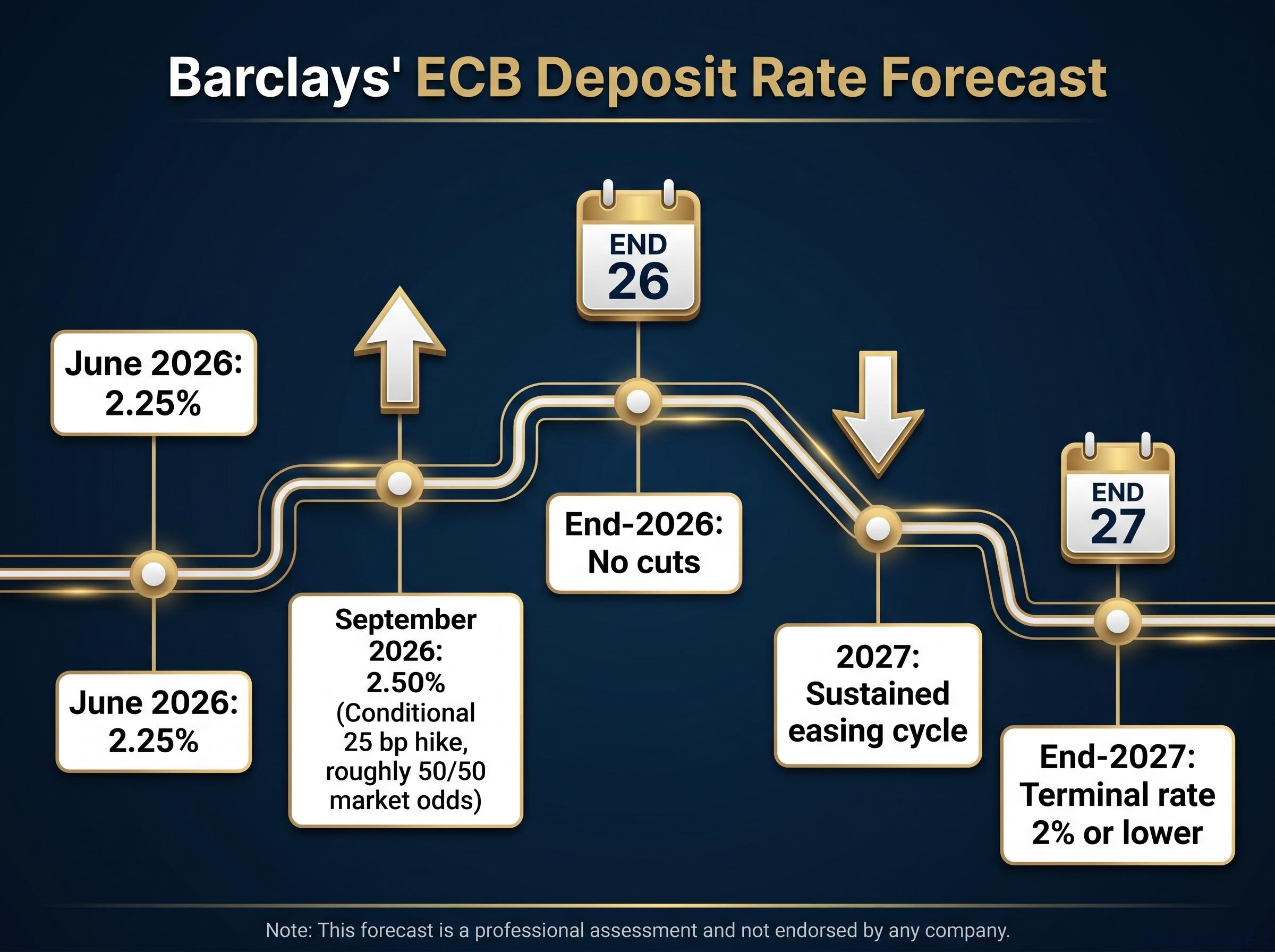

The ECB deposit facility rate sits at 2.25% following the June 2026 hike. Market-implied odds for a further 25 basis point move in September 2026 are roughly 50/50, and Barclays treats that hike as conditional rather than certain. The more consequential element of their view is what comes after: no cuts before end-2026, then a sustained easing cycle through 2027 that takes the rate back to or below 2%.

Here is a framework for reading ECB policy across the next 18 months, built on a specific structural argument about energy shocks, that gives you a concrete basis for decisions on duration, rate-sensitive equities, and euro exposure rather than waiting for meeting-by-meeting guidance to accumulate.

The Barclays forecast breaks into two components with very different confidence levels. The September 2026 hike is flagged as tactical and data-dependent. The 2027 easing cycle is where the conviction sits. That asymmetry is the starting point for using the call practically.

The full rate path looks like this:

Market pricing context: As of early July 2026, implied odds for the September hike sit at approximately 50/50, meaning the market itself has not resolved the near-term question.

What this tells you is that Barclays is not predicting a one-way tightening story. September is a near-term inflection point with genuinely uncertain odds. The direction of travel over the following 18 months, where the analysts hold far higher conviction, matters more for positioning than any single meeting outcome. Investors who fixate on September risk building a view around the lowest-confidence element of the forecast while ignoring the part that actually shapes the rate cycle.

For investors wanting to stress-test the Barclays view against the most prominent contrarian position, our full explainer on the UBS tightening scenario sets out the case for 75 basis points of total ECB tightening through December 2026, including the specific data conditions that would push the Governing Council toward a third hike.

The Barclays argument only works if the 2022 Ukraine energy shock was structurally different from what is happening now. Before accepting that claim, it is worth understanding exactly what made 2022 so severe, because the comparison is doing most of the analytical heavy lifting in the entire thesis.

The 2022 shock hit on three dimensions simultaneously. Europe was physically dependent on Russian pipeline gas, with limited alternative supply infrastructure to absorb a sudden cut. The post-COVID reopening had demand running hot, which amplified the pass-through from energy prices into core inflation across goods and services. And governments responded with large-scale fiscal packages (energy subsidies, price caps, and direct transfers) that injected demand into economies already overheating. Each dimension on its own would have been manageable. Together, they created the most persistent inflation impulse Europe had experienced in decades.

The IEA’s characterisation of the conflict as a source of structural oil inflation risk rather than a transient spike is central to understanding why the ECB moved at all in June 2026; a shock that embeds a persistent geopolitical risk premium behaves differently in central bank models than one expected to unwind within a quarter.

Understanding that anatomy is what lets you evaluate the Barclays argument critically rather than accepting the “this time is different” claim at face value. Their thesis is only as strong as the accuracy of this comparison.

| Shock dimension | 2022 Ukraine episode | 2026 Iran episode (Barclays assessment) |

|---|---|---|

| Energy supply | Heavy reliance on Russian pipeline gas; limited LNG import capacity; storage depleted | Expanded LNG terminals, diversified suppliers, rebuilt gas storage; same geopolitical stress now produces smaller, shorter price spikes |

| Demand conditions | Post-COVID reopening surge amplifying energy price pass-through into broader inflation | Soft Eurozone demand backdrop; weaker transmission from energy to core prices |

| Fiscal amplification | Large-scale government subsidy and transfer packages injecting demand into already-inflationary economies | Fiscal support for the shock capped at roughly 0.2-0.3% of Eurozone GDP, on the assumption oil prices stay well below recent peaks |

The fiscal estimate carries a condition worth noting: it holds only if oil prices remain substantially lower and no further supply disruptions emerge. If either assumption breaks, the fiscal response could scale up and start resembling the 2022 pattern.

The ECB’s June 2026 Eurosystem staff projections represent the formal baseline against which Barclays is dissenting. The gap between the two is not about different facts. It is about how persistent the energy impulse will prove to be.

| Measure | 2026 | 2027 | 2028 |

|---|---|---|---|

| Headline HICP | 3.0% | 2.3% | 2.0% |

| HICPX (excluding energy and food) | 2.5% | 2.5% | 2.2% |

HICPX, the measure of inflation excluding energy and food, is the figure that matters most here. It strips out volatile components and shows what is happening to underlying price pressures. The ECB projects it staying at 2.5% through both 2026 and 2027, peaking at approximately 2.7% in early 2027.

The number Barclays is implicitly challenging: an HICPX peak of approximately 2.7% in early 2027. If their energy shock assessment is correct, this peak never materialises at that level.

Barclays believes the three structural differences they identify mean energy pass-through will fade faster than ECB models assume, leaving core inflation likely to undershoot these staff projections. Under that scenario, the ECB would be forced to reverse part of its 2026 tightening through cuts in 2027, a sequence Frankfurt does not currently anticipate.

The ECB’s caution is institutionally rational. Its mandate is price stability, and erring on the side of tightness protects credibility. But if Barclays is right, the September 2026 hike would in retrospect look like a policy error corrected by 2027 cuts, and investors who positioned for that outcome early would be holding duration exposure at the right moment. The trip-wire to watch: if HICPX prints materially below 2.5% in late 2026, the easing case strengthens in real time.

The rate path from a deposit rate of 2.50% (post-September) down to 2% or below by end-2027 is not abstract. It maps directly onto four asset classes with specific mechanisms:

European equity positioning among institutional investors remains structurally underweight even as Barclays formally upgraded the asset class on 3 July 2026, a combination that creates a specific dynamic for rate-sensitive sectors: the repricing catalyst from ECB cuts may arrive while the largest potential buyers are still rebuilding exposure from historically low allocations.

Central bank policy divergence between the ECB and the Federal Reserve is the key transmission mechanism for the euro FX implication: if the Fed holds rates in the 3.50-3.75% range while the ECB cuts toward 2% through 2027, the differential creates directional pressure on the euro that is more durable than short-term positioning moves.

Each of these implications activates only if the easing cycle materialises on the timeline Barclays projects. Understanding the mechanism behind each one lets you monitor whether conditions are aligning before committing to rate-sensitive positions.

The Barclays analysts flag four specific conditions that would invalidate their reading. Each one targets a different structural claim in the thesis, and each is falsifiable, meaning you can watch for it in the data.

Fiscal threshold to watch: the Barclays baseline assumes government energy support stays within a band of roughly 0.2-0.3% of Eurozone GDP, a ceiling that holds only while oil prices remain well below recent highs and no additional supply shocks materialise.

The credibility risk is distinct from the other three. You cannot price it from energy or macro data alone, because it depends on how the Governing Council weighs its institutional reputation against incoming disinflation. That makes it the hardest risk to hedge and the most important to monitor through ECB communication and forward guidance signals.

The Barclays argument rests on two load-bearing claims: the Iran energy shock is structurally weaker than the 2022 Ukraine episode on three measurable dimensions, and the ECB’s current inflation projections likely overstate persistence, making meaningful 2027 cuts the more probable outcome.

September 2026 is a near-term data checkpoint, not a pivot in itself. Under the Barclays scenario, a conditional 25 bp hike represents the policy peak. What matters is what comes after.

The signals to track across the next 18 months:

If you find the structural argument convincing, the implication is to build rate-sensitive exposure ahead of the easing cycle rather than waiting for confirmation that may arrive after the repricing has already begun. If you find the risk conditions credible, the implication is to wait for the data checkpoints before acting. Either way, treating each ECB meeting as an independent event is the positioning mistake this framework is designed to prevent.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking rate projections are subject to change based on evolving economic conditions, geopolitical developments, and central bank policy decisions.

Barclays forecasts the ECB deposit facility rate falling to 2% or lower by the close of 2027, driven by a sustained easing cycle following a conditional 25 basis point hike to 2.50% in September 2026.

Barclays identifies three structural differences: Europe has expanded LNG capacity and rebuilt gas storage, Eurozone demand is soft rather than post-COVID hot, and fiscal support for the 2026 shock is capped at roughly 0.2-0.3% of GDP compared to the large-scale subsidy packages deployed in 2022.

The ECB's June 2026 Eurosystem staff projections show HICPX, the measure excluding energy and food, staying at 2.5% through both 2026 and 2027, with a peak of approximately 2.7% in early 2027, a level Barclays believes will not materialise if energy pass-through fades faster than Frankfurt assumes.

The most important signal is HICPX prints in late 2026: if core inflation comes in materially below the ECB's 2.5% staff forecast, the case for 2027 cuts strengthens in real time. Investors should also monitor the Iran conflict trajectory, the scale of fiscal energy support packages, and ECB forward guidance tone.

A deposit rate falling from 2.50% to 2% or below by end-2027 would reprice forward rate expectations lower across the sovereign curve, benefiting duration holders in government bonds and supporting sectors with high leverage or discount-rate sensitivity such as utilities, real estate, and infrastructure.