Warsh Drives Real Yields to a 12-Month High, Pressuring Risk Assets

39 mins ago

The investors most likely to get hurt by Kevin Warsh’s confirmation as Federal Reserve Chair are the ones who waited for it to happen before deciding what to do about it. That is not a provocation for its own sake. It is the core of an argument that Ken Fisher, Founder, Executive Chairman, and Co-Chief Investment Officer of Fisher Investments, laid out in his 19 June 2026 commentary, and it applies to far more than one Senate vote. Warsh was confirmed on 13 May 2026 and sworn in on 22 May 2026. Since then, coverage has been relentless. Investors are asking whether to reposition around what this means for interest rates, Fed independence, and monetary policy direction. Fisher’s answer is direct: the question itself is the mistake. By the end of this piece, you will understand why widely anticipated macro events rarely move markets the way investors expect, and you will have a four-question framework to apply to the next loudly advertised headline, whatever it turns out to be.

Markets are forward-looking instruments. They do not wait for a Senate vote to process information that has been publicly available for months. Investors collectively studied Kevin Warsh’s background, analysed his policy orientation, and repositioned accordingly well before the confirmation date arrived.

Warsh served as a Fed governor from 2006 to 2011. His disposition, his intellectual framework, and his likely policy posture were extensively documented and publicly debated throughout the nomination process. By the time the vote was televised, the market had already absorbed the outcome that mattered.

The Federal Reserve History record on Warsh confirms his tenure as a Board of Governors member from February 2006 to March 2011, a five-year span that generated a documented archive of speeches, votes, and policy positions that analysts had already modelled well ahead of his 2026 confirmation vote.

The question worth asking is not “what does Warsh’s confirmation mean?” It is “what, if anything, about Warsh’s confirmation surprised the market?” The answer is almost nothing.

Three reasons his confirmation qualifies as a pre-priced event:

Ken Fisher’s core framing (19 June 2026): Widely discussed events lose their capacity to generate surprise market movements. If everyone is talking about something, the odds are high that markets have already incorporated the consensus view.

If you feel the urge to reposition around the confirmation, you are experiencing a timing illusion: believing you are responding to fresh news when the market processed that news weeks or months before the Senate voted.

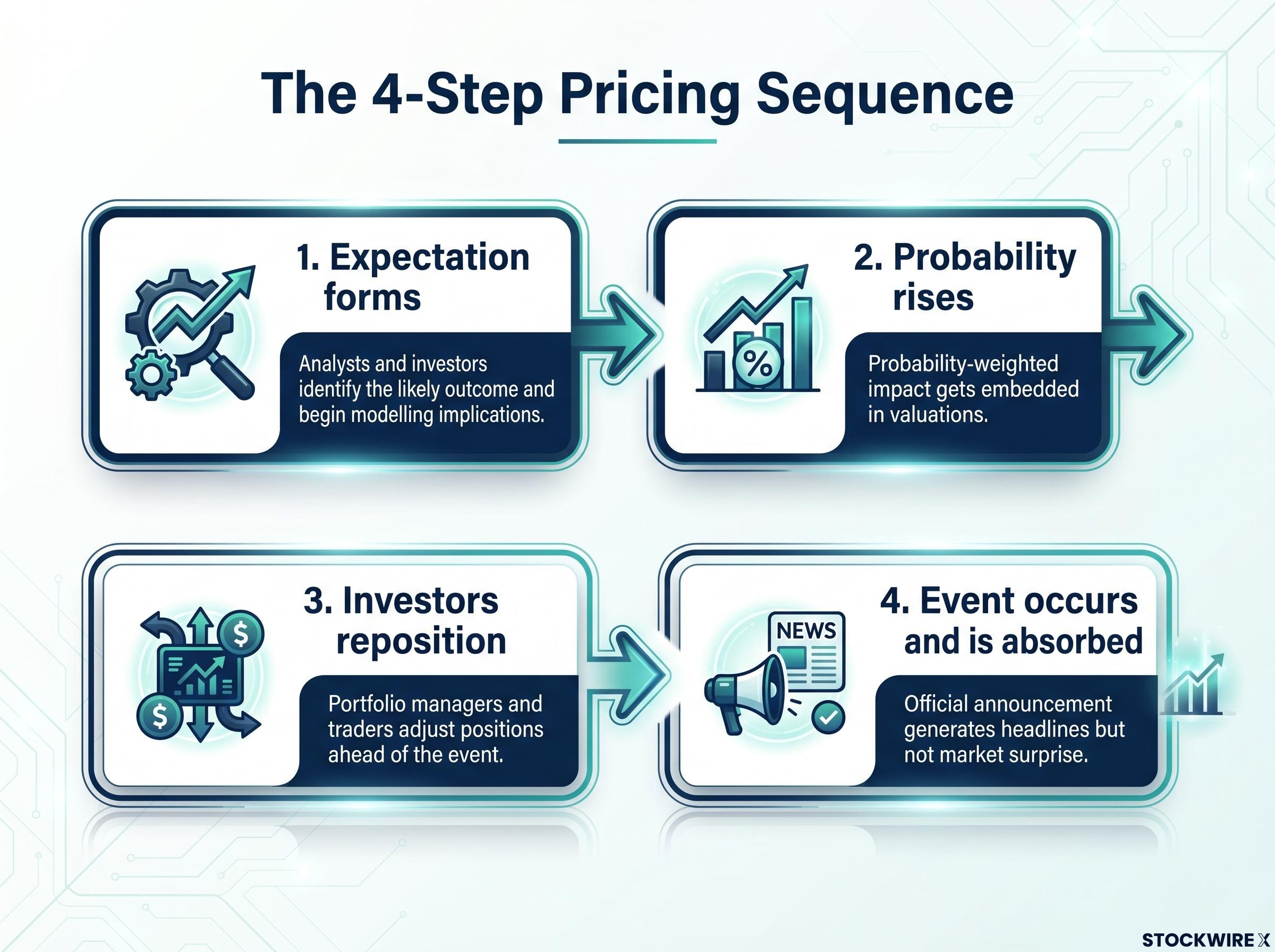

The mechanism behind pre-pricing, the process by which markets reflect expected outcomes before those outcomes officially occur, follows a logical sequence. Understanding the sequence changes how you read headlines.

Pre-pricing works because investors continuously act on expectations about the future. When an outcome is widely anticipated, the expected implications for rates, inflation, and growth are gradually built into asset prices as the probability of that outcome rises. This happens incrementally, not all at once, which is why there is no single “pricing-in” moment you can point to on a chart.

The price discovery process operates continuously and incrementally, with passive limit orders sitting in the order book contributing roughly 45% of all price discovery according to research by Brogaard, Hendershott, and Riordan, meaning asset prices are being updated in real time as new information and expectations enter the market, long before any official announcement is made.

The pricing sequence works in four steps:

Here is the counterintuitive part: the volume of media attention given to an event is inversely related to its remaining investment edge. More coverage means more repositioning has already occurred. The noise itself is evidence that the pricing has already happened. That tells you the noisier a macro event becomes in financial media, the less likely it is to produce the portfolio-level disruption that the noise implies.

This is categorically different from genuine surprises. A sudden geopolitical shock, an unexpected economic data release, or a policy reversal that contradicts consensus can and does move markets sharply. The distinction matters: the pre-pricing principle applies to anticipated events, not to genuine surprises that arrive without warning.

Warsh’s qualifications and prior Fed experience were pre-existing, public information. There was no hidden policy orientation waiting to be revealed after the confirmation vote. The administration nominated him precisely because his general disposition was already understood and politically acceptable, which eliminated the “unknown new regime” variable that sometimes accompanies leadership transitions.

Even if Warsh held strong personal policy views, the Federal Open Market Committee (FOMC), the Fed’s policy-setting body, has 12 voting members. The Chair leads and influences but must build consensus. Institutional norms and the Fed’s culture of gradualism constrain even strongly opinionated chairs. Unilateral action is structurally unavailable.

A divided FOMC committee, with dissenters pulling simultaneously toward immediate cuts and additional hike signalling, is not a condition that any single chair can resolve unilaterally; the institutional constraint the article identifies as structurally unavoidable is visible in real time across the Fed’s own voting record.

If the pre-pricing mechanism explains why Warsh’s confirmation did not move markets, history explains why the anxiety around it was so predictable.

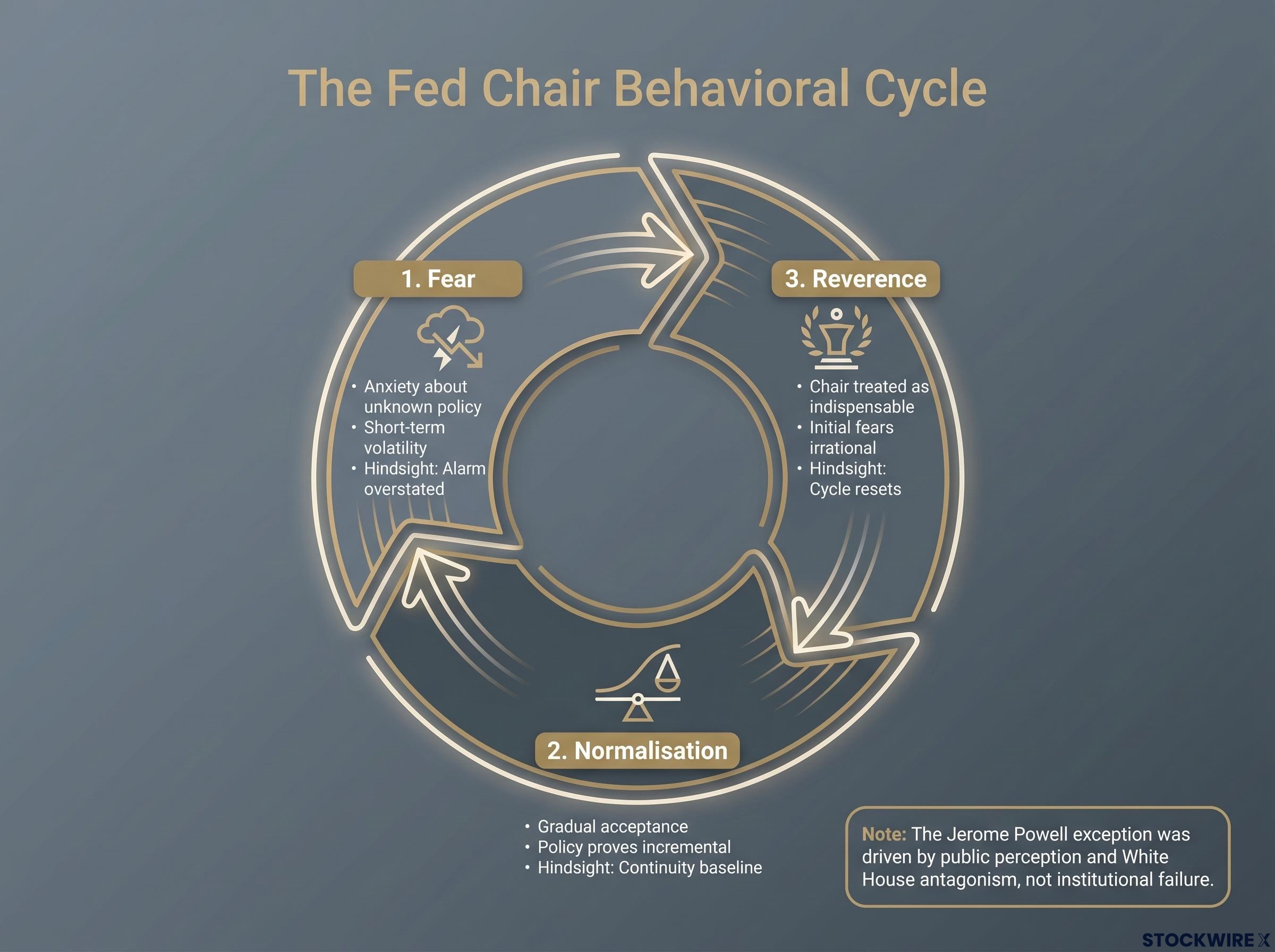

Fisher identifies a three-phase cycle that has repeated consistently across Fed Chair appointments: fear at the appointment, normalisation during the tenure, and eventual reverence in hindsight. The cycle is behavioural, not analytical. It reflects how investors process uncertainty about new leadership, not how the Fed actually functions.

| Phase | Investor Sentiment | What Actually Happened | Hindsight Assessment |

|---|---|---|---|

| Fear | Anxiety about unknown policy direction; “new regime risk” dominates commentary | Short-term sentiment volatility, driven by narrative rather than fundamental change | The alarm was overstated |

| Normalisation | Gradual acceptance as the chair communicates, acts, and is constrained by the institution | Policy changes proved incremental; the system continued functioning | Continuity was the baseline all along |

| Reverence | The same commentators who expressed alarm treat the chair as indispensable | The initial fears look irrational in retrospect | The cycle resets with the next appointment |

The pattern tells you that your unease about a new Fed Chair, however rational it feels in the moment, is a predictable emotional response that has been wrong in the same direction, consistently, across decades of appointments.

The Powell exception is worth addressing directly. Jerome Powell is flagged as unusual in public perception, not in institutional outcomes. The exception arose because prolonged, public antagonism from the White House coloured how certain groups viewed Powell’s tenure, pulling broader opinion in a similar direction. The Fed as an institution did not stop functioning. The structure held. Warsh’s situation lacks that adversarial political backdrop entirely; the administration nominated him because it views him favourably.

Knowing the pattern helps you name what you are experiencing as a behavioural cycle rather than a reasoned analytical response. That is the precondition for not acting on it.

The Warsh case illustrates a principle. The principle is what you keep. Fisher’s logic suggests four checks to apply before making portfolio moves in response to any major macro headline:

Running any major headline through these four questions before acting gives you a structured reason to stay the course when the emotionally compelling answer is to move. That is where most reactive portfolio mistakes originate.

Reactive selling decisions are where most portfolio value destruction actually concentrates: research from the University of Chicago found that randomly selected exit points outperformed professional portfolio managers by up to 150 basis points annually, identifying the impulse to act on prominent headlines as a measurably costly behaviour rather than a prudent one.

Walk through the checks. Is the Warsh confirmation widely discussed? Overwhelmingly yes. How long has it been on the market’s radar? Months before the vote, through nomination, hearings, and public analysis. What would actually surprise the market? A genuine policy shock that contradicts Warsh’s known orientation, which no consensus forecast anticipates. Are you reacting to signal or noise? The volume of post-confirmation coverage is noise; the pricing happened before the swearing-in.

All four checks return the same answer, strongly supporting the hold-course conclusion. If your honest answers differ from the consensus scenario, perhaps because you anticipate a genuine policy shock, examine whether that view is based on non-consensus information or anxiety. The distinction matters.

Policy outcomes under Warsh will depend on the FOMC consensus, economic data, and inflation dynamics. They will not depend on his personal views operating in isolation. The 12-voting-member structure and the institutional culture of gradualism constrain policy changes regardless of the chair’s individual disposition.

Genuine market-moving surprises, if they occur, will emerge from developments that are not yet heavily covered and priced:

The variables that will actually shape your portfolio outcomes over the next 12 months are far more likely to emerge from data the market has not yet fully digested than from a leadership transition that was telegraphed months in advance. Your attention is better directed toward less-discussed information than toward consuming more coverage of the already-priced-in appointment.

Warsh’s confirmation is a market non-event, not because it is unimportant in a policy sense, but because its market implications were processed long before the confirmation date. A qualified, experienced candidate with a known track record was nominated by a politically aligned administration, confirmed through a widely telegraphed process, and constrained by the same institutional machinery that has governed every Fed Chair before him.

The behavioural trap, mistaking media prominence for investment significance, is not unique to Fed appointments. It will recur with the next major macro headline. The four-question diagnostic applies identically to whatever that headline turns out to be, and that is where the real portfolio protection lies.

Negativity bias in financial media is structural rather than incidental: negative financial headlines outnumber positive ones by approximately 17 to 1, a ratio optimised for audience engagement rather than investor accuracy, which means the volume and tone of Warsh confirmation coverage reflects a media production incentive as much as any genuine analytical signal.

The principle worth keeping: Attention destroys surprise, and surprise is what actually moves markets. (Ken Fisher’s analytical framework, 19 June 2026 commentary)

For long-term investors, the rational move is almost certainly to hold course. The mental energy previously spent on confirmation coverage is better deployed searching for less-covered, less-digested developments where genuine pricing gaps may still exist.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements are speculative and subject to change based on market developments and company performance. Past performance does not guarantee future results.

—

Market pre-pricing is the process by which investors collectively absorb and reflect an anticipated event in asset prices before it officially occurs. Because Warsh's background, policy orientation, and confirmation timeline were publicly known for months, markets had already repositioned around his Fed Chair appointment well before the Senate voted.

Warsh was nominated well before his confirmation on 13 May 2026, and his prior five-year tenure as a Fed governor from 2006 to 2011 gave analysts a detailed public record to model. Markets tracked the nomination, committee hearings, and confirmation vote in real time over months, meaning the pricing process began long before the official vote.

According to Ken Fisher's 19 June 2026 commentary, the volume of media attention given to an anticipated event is inversely related to its remaining investment edge, because widespread coverage accelerates repositioning and reduces residual surprise, which is what actually moves markets.

Fisher's framework asks: how widely is the event being discussed; how long has it been on the market's radar; what outcome would actually surprise the market; and whether you are reacting to signal or noise. If the answers point to a well-known, heavily covered, expected outcome, the event is likely already priced in.

The Federal Open Market Committee has 12 voting members, meaning the Chair must build consensus rather than act unilaterally. Institutional norms and the Fed's culture of gradualism constrain even strongly opinionated chairs, so any single chair's personal policy views cannot dictate outcomes independently.