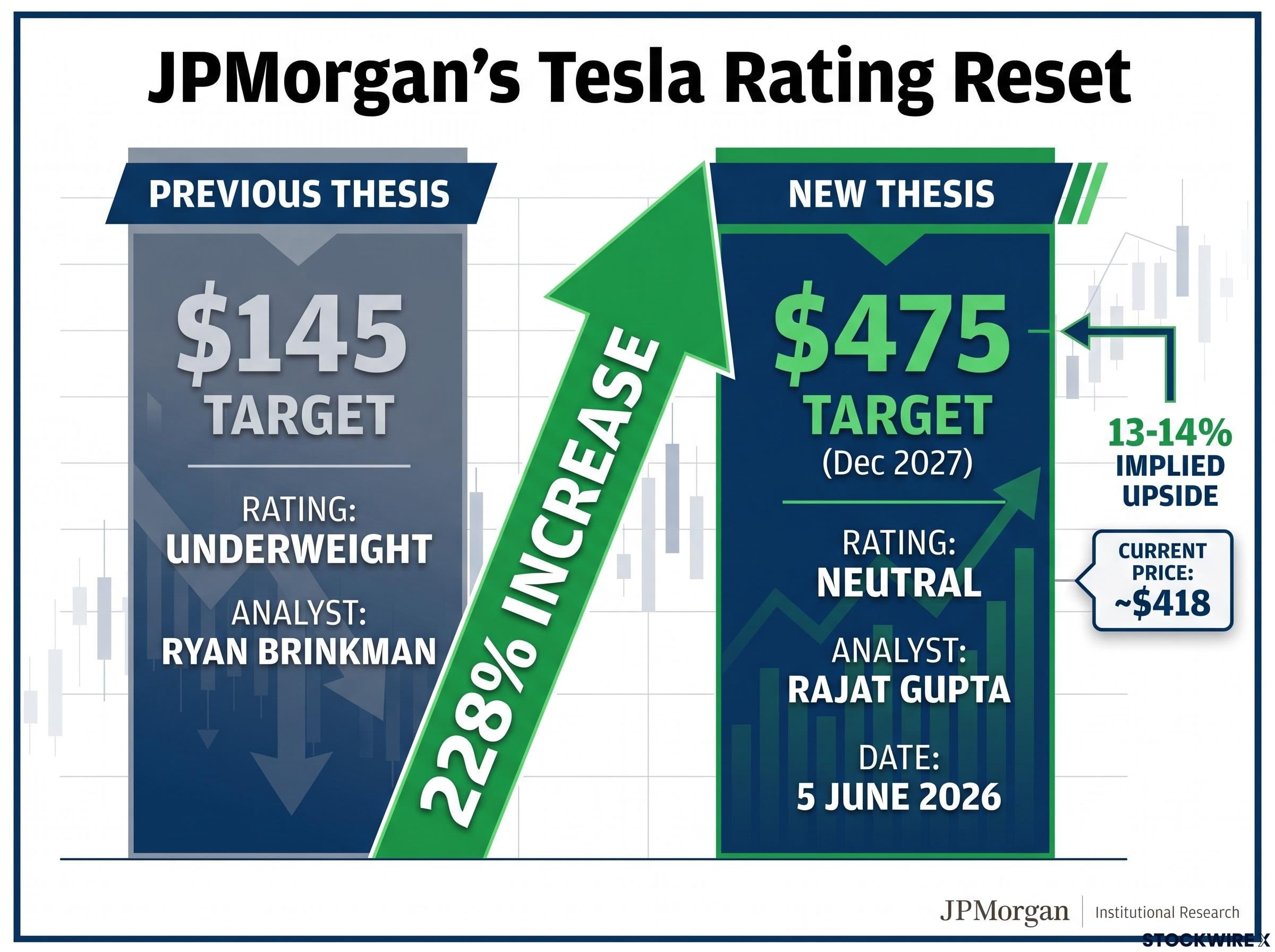

JPMorgan tripled its Tesla price target overnight. The move, from $145 to $475, published on 5 June 2026, ended one of Wall Street’s most entrenched bearish positions on the stock and reframed how the bank values the company entirely. Led by analyst Rajat Gupta, the JPMorgan Tesla upgrade shifts the institution’s lens from near-term automotive earnings to a long-duration physical AI thesis built on three businesses that do not yet operate at commercial scale. For investors holding or evaluating Tesla at around $418, the question is immediate: does the upgrade signal a buying opportunity, a validation of existing conviction, or a warning that the upside is already priced in?

This analysis unpacks what JPMorgan actually changed in its thesis, examines the three business pillars underpinning the $475 target, measures the gap between ambition and operational reality, and identifies where the bank itself sees near-term risk.

From perma-bear to neutral: what JPMorgan actually changed and why it matters now

The scale of this reversal is difficult to overstate. Under former analyst Ryan Brinkman, JPMorgan had maintained an Underweight rating on Tesla for years, with a $145 price target that implied roughly 65% downside from the stock’s trading levels.

The magnitude: JPMorgan raised its Tesla price target from $145 to $475, a 228% increase, in a single research note.

Rajat Gupta assumed coverage in early May 2026, and the upgrade followed within weeks. That sequencing matters. This was not a minor adjustment to an existing view; it was a deliberate institutional reset under new leadership.

The details of the new rating carry their own signal:

- Rating change: Underweight to Neutral

- Prior price target: $145

- New price target: $475 (December 2027)

- Covering analyst: Rajat Gupta, JPMorgan

- Effective date: 5 June 2026

With Tesla trading at approximately $418 at the time of the note, the $475 target implies roughly 13-14% upside. That is a modest margin for a stock that just received a 228% target increase. JPMorgan is validating the long-term thesis without pounding the table on near-term entry.

When big ASX news breaks, our subscribers know first

Tesla’s three long-horizon bets: the business pillars JPMorgan is now paying for

The $475 target is not built on automotive earnings growth. It is assembled from three distinct, speculative but quantifiable revenue streams that JPMorgan projects could account for approximately half of Tesla’s incremental revenue growth between 2025 and 2030.

JPMorgan estimates Tesla’s annual revenue will expand from $95 billion in 2025 to $203 billion by 2030, with earnings per share reaching approximately $7.50 by the end of that period. The three new business lines driving that growth are robotaxi services, Optimus humanoid robotics, and Full Self-Driving (FSD) licensing.

| Business pillar | Current status | Role in the $475 thesis | Projected timeline |

|---|---|---|---|

| Robotaxi | Pilot service in Austin; limited fleet, geofenced area | Nearest-term revenue contributor among the three new lines | Scaled deployment projected 2027-2029 |

| Optimus humanoid robot | Low hundreds of prototype units; internal factory use | High-margin hardware and automation revenue at scale | Meaningful commercial volumes projected 2027-2028 |

| FSD licensing | No executed third-party deal disclosed; $3.60B deferred revenue | Software licensing and recurring revenue from external OEMs | No confirmed agreement as of mid-2026 |

The connective tissue across all three pillars is vertical integration. JPMorgan characterised Tesla’s degree of hardware and software integration as unmatched at industrial scale.

Sum-of-parts analysis reveals a striking implication at current prices: Piper Sandler’s 17-segment framework values the core Tesla automotive and energy business at approximately $400 per share, meaning the Optimus division and inference-as-a-service are effectively assigned near-zero value by the market, even as Wall Street estimates for Optimus alone range from $100 to $1,000 per share.

Why JPMorgan’s Amazon comparison is more than a metaphor

JPMorgan drew an explicit parallel between Tesla’s trajectory and Amazon’s development of AWS and its Kiva robotics division. Just as Amazon built cloud infrastructure and warehouse automation on the back of its retail operations, Tesla is using its own production facilities as a live testing environment for Optimus.

This factory-first strategy is central to the bull case. Optimus would need to demonstrate measurable manufacturing utility, reducing costs and proving reliability, before external commercial sales become credible. Tesla’s $3.60 billion in FSD deferred revenue as of Q1 2025 (per Tesla’s Form 10-Q, filed 2 May 2025) already indicates a substantial installed base generating software-related obligations and future revenue potential.

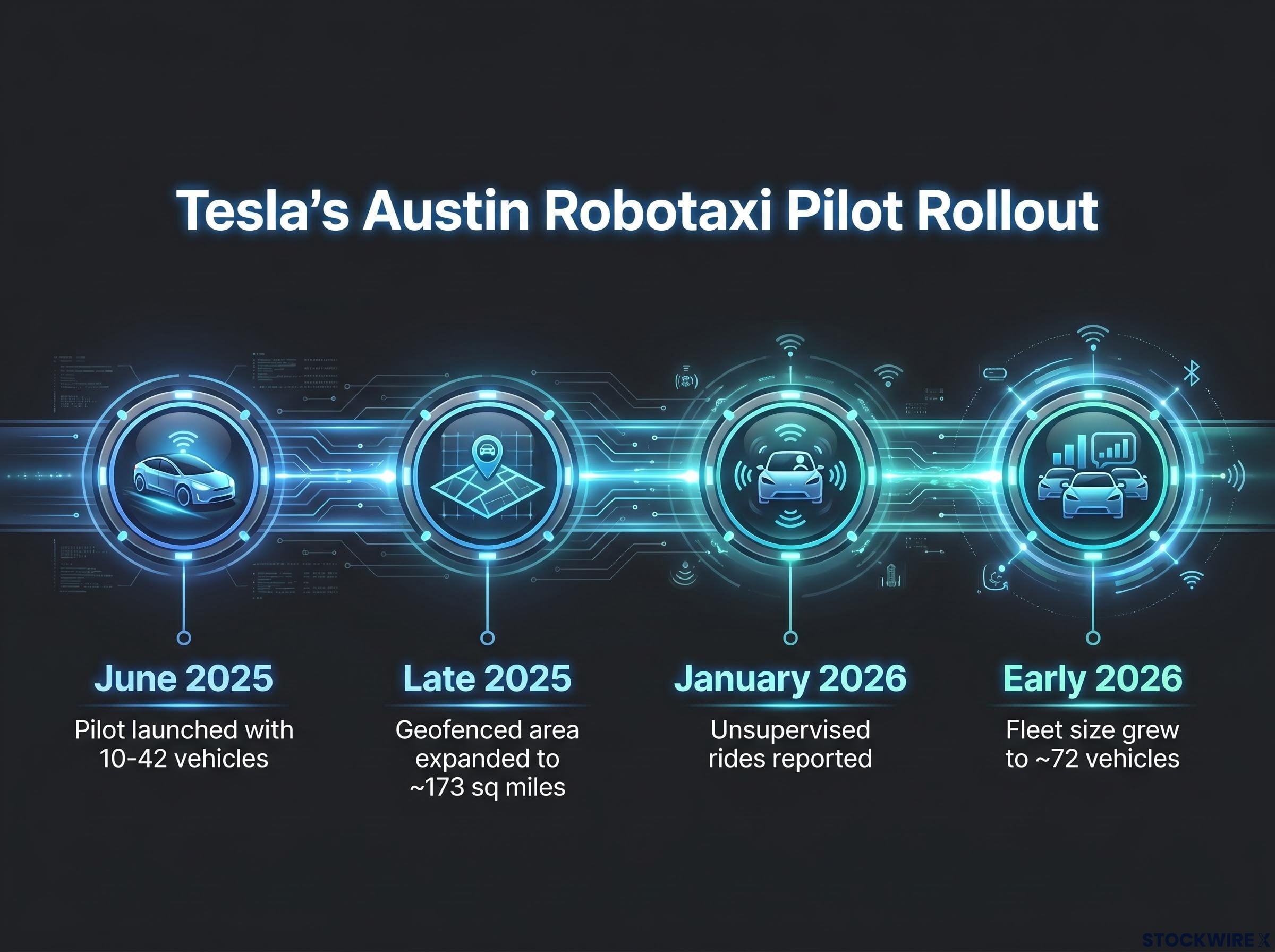

What the robotaxi rollout actually looks like on the ground today

The robotaxi service is the nearest-term of the three bets, which makes its current operational state the most actionable leading indicator for investors.

The timeline so far:

- June 2025: Tesla launched a limited robotaxi pilot in Austin, Texas, with approximately 10-42 vehicles and safety monitors present

- Late 2025: The geofenced service area expanded to approximately 173 square miles in Austin

- January 2026: Some unsupervised rides were reported in Austin

- Early 2026: Fleet size grew to approximately 72 vehicles according to operational trackers

JPMorgan’s upgrade references expansion to Dallas, Houston, and the Bay Area. However, Tesla’s own SEC filings continue to frame full autonomy and scaled Cybercab deployment in forward-looking terms.

The California DMV autonomous vehicle permit requirements, updated in April 2025, establish the specific safety standards and permit processes that any robotaxi operator must satisfy before scaling commercial deployment in the state, a regulatory hurdle directly relevant to Tesla’s Bay Area expansion plans.

Tesla’s Form 10-Q describes the company as “focused on … future autonomous capabilities through our purpose-built Robotaxi product, Cybercab,” without providing ridership statistics or confirming a fully commercial, unmonitored service.

For competitive context, Waymo operates commercially in Phoenix, San Francisco, and Los Angeles. No head-to-head metrics comparing the two services, such as trips per day or miles driven, have been published in verifiable sources. The gap between JPMorgan’s expansive characterisation and Tesla’s own regulatory filings is worth monitoring closely.

Understanding Tesla’s vertical integration advantage: why physical AI is the new valuation framework

The term “physical AI” has become the analytical framework that separates bulls from bears on Tesla. Understanding what it means in practice, rather than as marketing language, is the single most relevant concept for evaluating whether Tesla deserves a premium multiple.

Tesla’s vertical integration stack comprises four components:

- In-house chip design: Custom silicon including Dojo and HW4, developed specifically for autonomous driving workloads

- Proprietary FSD software: A full self-driving software stack trained on real-world driving data, continuously updated over the air

- Manufacturing at scale: Global production capacity that also serves as a live testing environment for Optimus

- Real-world data flywheel: Approximately 9 million vehicles operating globally and roughly 10 billion FSD miles driven, per JPMorgan’s upgrade note

Each of these layers reinforces the others. The manufacturing infrastructure produces the vehicles. The vehicles generate training data. The data improves the software. The software increases the value of the vehicle. Competitors without a comparable installed fleet face a structural disadvantage in replicating this cycle.

How the FSD data flywheel compounds over time

Each incremental mile driven feeds training data back into the FSD model, creating a compounding accuracy advantage. This is not a static moat; it widens with every vehicle sold and every mile logged.

Tesla’s $3.60 billion in FSD deferred revenue (Tesla Form 10-Q, Q1 2025) indicates a large base of vehicles already monetised through FSD purchases or subscriptions, with future software improvements yet to be delivered. That figure represents both an obligation to those customers and an opportunity to recognise revenue as capabilities are released.

JPMorgan’s framework argues that this combination of hardware, software, data, and manufacturing integration justifies assessing Tesla on long-duration earnings potential rather than near-term GAAP multiples. Physical AI, in this context, refers to companies operating at the intersection of robotics, autonomous systems, and manufacturing, where the data advantage compounds over time in ways that asset-light competitors cannot easily replicate.

Physical AI competition extends well beyond Tesla’s own deployments; China operates approximately 2 million industrial robots, generating a compounding real-world training data advantage that widens with every additional hour of operation and sits outside the semiconductor and software scorecard most analysts use to assess the US-China technology contest.

The entry point question: where JPMorgan sees near-term risk and what investors should weigh

JPMorgan raised its target 228% but still rates the stock Neutral. That is the most important signal in the entire note.

The core tension: A 228% price target increase paired with a Neutral rating signals that JPMorgan views the long-term thesis as sound but the near-term risk-reward at current prices as balanced.

The bank’s own caveats explain the restraint. JPMorgan acknowledged that current valuation multiples are elevated relative to near-term earnings, with most new addressable markets not expected to materialise at scale until 2029 or later. The EPS inflection point is projected beyond 2028, meaning near-term GAAP earnings do not support the current share price.

Scenario-based valuation is the only framework that makes analytical sense when a stock’s current price reflects a future that does not yet exist; point estimates and trailing multiples collapse under the weight of the uncertainty embedded in a 2027-2030 EPS inflection that has not yet been earned.

Four risk factors warrant attention:

- Margin pressure: Automotive gross margins have declined from historical peaks due to price reductions and mix shifts, documented in Tesla’s 2024 Form 10-K and 2025 quarterly filings

- Execution risk: FSD, robotaxi, Optimus, and energy storage all remain unproven at commercial scale

- Regulatory and technological uncertainty: Full autonomy faces an unclear regulatory pathway that could delay or limit the revenue streams embedded in aggressive models

- Near-term index rotation: JPMorgan flagged that selling pressure from investors rotating to higher-growth opportunities could push Tesla lower in the short term, potentially creating a more attractive entry point

For investors deciding whether to add, hold, or wait, JPMorgan’s own risk language provides the most honest framing: the long-term thesis may prove correct, but the near-term price may improve if rotation creates a pullback.

What it would take to get from $475 to a buy: the milestones that matter

Rather than treating the upgrade as a binary signal, investors can monitor three specific milestone categories over the next 12-18 months:

- Robotaxi regulatory approvals and fleet scale: Formal municipal or state permits for a fully commercial, unmonitored service, combined with measurable fleet growth beyond the current Austin pilot

- Optimus Gen 3 commercial orders: The Gen 3 reveal is slated for 2026, with meaningful commercial volumes projected by analysts for 2027-2028. Signed third-party orders would validate the factory-first strategy.

- FSD third-party licensing announcement: No executed licensing agreement with a named automaker has been disclosed as of mid-2026. A signed commercial deal would confirm an entirely new revenue category.

JPMorgan’s own EPS trajectory, approximately $7.50 by 2030, means investors have a multi-year window in which execution signals matter more than quarterly earnings beats. The Neutral rating itself signals that a pullback toward $380-$400 would materially improve the risk-reward.

| Metric | 2025 (estimate) | 2028 (projected) | 2030 (projected) |

|---|---|---|---|

| Revenue | $95 billion | Growth driven by new business lines | $203 billion |

| EPS | Below inflection point | Inflection projected beyond 2028 | ~$7.50 |

| Price target | — | — | $475 (December 2027 target) |

A new analytical lens, not a green light

JPMorgan’s upgrade is best understood as an institutional validation of Tesla’s long-duration investment thesis, not a near-term buy recommendation. The modest implied upside from $418 to $475 and the Neutral rating both signal that risk-reward is balanced at current prices.

Investors considering increased exposure may benefit from monitoring the three milestone categories outlined above before acting. If even one of Tesla’s three long-horizon bets, robotaxi, Optimus, or FSD licensing, delivers at scale ahead of schedule, the $475 target could prove conservative.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in this analysis are sourced from JPMorgan’s research note and are subject to market conditions and various risk factors. Past performance does not guarantee future results.