Why JPMorgan’s 2026 Sector Calls Split Banks and Energy Apart

3 mins ago

JPMorgan’s strategy team told clients on 13 July to treat Iran-driven equity selloffs as entry points, not warnings. The recommendation, led by strategist Mislav Matejka, arrived with specific earnings data behind it, and that data is worth examining on its own merits.

The call landed mid-earnings season. Q1 2026 results already show roughly 80% of S&P 500 companies beating estimates, and full-year EPS forecasts have been revised upward across every major global region. That earnings momentum is doing the heavy lifting in JPMorgan’s framework: the bank argues geopolitical shocks of this type are transient by nature, and the underlying profit cycle is resilient enough to absorb them.

Here is what the numbers behind the recommendation actually tell you, and what they do not. The specific figures, their verification status, the conditional logic holding the thesis together, and the signals worth watching as earnings season unfolds from here.

Mislav Matejka and JPMorgan’s strategy team published their buy-the-dip recommendation on 13 July 2026, directed specifically at Iran-related equity market volatility. This position is not a recent change of heart. JPMorgan first adopted it around the second half of March 2026, and the July note refines the argument with updated evidence and sharper framing.

The core logic runs through a single framing: geopolitical shocks create temporary dislocations, not structural damage, and the current earnings cycle is strong enough to absorb them.

According to the note, the bank believes that pullbacks caused by geopolitical developments of this kind represent opportunities for investors to add exposure rather than signals to reduce it. J.P. Morgan Asset Management reinforces the view by noting that asset prices and the dollar have reacted relatively modestly to Iran developments, suggesting fundamentals, not geopolitics, are anchoring markets.

But this is not an unconditional green light. The call depends explicitly on the conflict avoiding severe disruption to energy infrastructure, with the Strait of Hormuz remaining open. That containment assumption is the load-bearing wall. If it holds, the thesis holds. If it cracks, JPMorgan’s own framework requires reassessment. Understanding exactly where the thesis breaks down is what separates following the recommendation from understanding it.

The earnings data is what gives JPMorgan’s call weight beyond sentiment. Start with the most concrete and independently verified figure: roughly 80% of S&P 500 companies beat first-quarter estimates in Q1 2026, according to LSEG I/B/E/S data.

The Q1 2026 earnings season delivered a blended S&P 500 growth rate of 27.1%, nearly double the 13.1% analyst forecast from quarter-end, with an aggregate earnings surprise of 20.7% that was almost three times the five-year average, providing the foundation on which upward EPS revisions through July have been built.

That beat rate alone would be notable. What makes it more so is the revision trajectory underneath it. Q1 2026 EPS growth expectations were revised upward from 12.7% to 13.9% as the Iran situation unfolded. Earnings estimates moving higher into a geopolitical shock, rather than lower, is directionally unusual and is the specific dynamic JPMorgan is pointing to.

FactSet Earnings Insight data for Q1 2026 recorded a positive EPS surprise rate of 84% across reporting S&P 500 companies, corroborating the broader beat-rate trend that underpins the buy-the-dip thesis and confirming that upward EPS revisions were broad-based rather than confined to a single sector.

The 13 July note then builds forward. Headline Q2 2026 earnings growth projections for U.S. companies run at around 22% year-over-year, with eurozone companies sitting closer to 12%. JPMorgan regards these figures as superficially large, but the bank places greater analytical weight on the median EPS growth reading of roughly 8% across both regions, treating it as a more grounded gauge that is less distorted by a small cluster of outsized performers at the top.

JPMorgan strategists described the median 8% growth figure as “very achievable,” according to the 13 July note.

That distinction matters for you directly. If the earnings bar the market actually needs to clear is 8%, not 22%, the fundamental anchor supporting the buy-the-dip thesis is considerably more durable than the headline consensus number suggests.

| Metric | Figure | Region | Verification status |

|---|---|---|---|

| Q1 2026 beat rate | ~80% | U.S. (S&P 500) | Confirmed (LSEG I/B/E/S) |

| Q1 2026 EPS growth revision | 12.7% → 13.9% | U.S. (S&P 500) | Confirmed (LSEG I/B/E/S) |

| Consensus Q2 2026 EPS growth | ~22% YoY | U.S. | From July 13 note; unverified externally |

| Consensus Q2 2026 EPS growth | ~12% YoY | Eurozone | From July 13 note; unverified externally |

| Median Q2 EPS growth | ~8% | U.S. and eurozone | From July 13 note; unverified externally |

The bank’s strategists noted that full-year 2026 EPS projections have continued rising across every region, with the improvement broad-based rather than driven solely by U.S. technology or energy sectors. Multiple independent data sources corroborate the direction of that trend.

Equity markets have developed a pattern over the past decade: absorb the geopolitical shock, reprice modestly, then refocus on fundamentals once the initial volatility passes. JPMorgan explicitly references this dynamic. The bank’s strategists contend that investors have become progressively better at recognising geopolitical disruptions as short-lived, with the Iran situation specifically seen as one where both parties carry substantial economic and political reasons to keep the conflict contained rather than allow it to spiral.

The historical record supporting equity resilience during conflict is substantial: the S&P 500 has delivered a positive one-year return after conflict onset in roughly 73% of cases since 1959, with a median gain near 9.7%, reinforcing why institutional strategists frame geopolitical shocks as temporary dislocations rather than structural breaks.

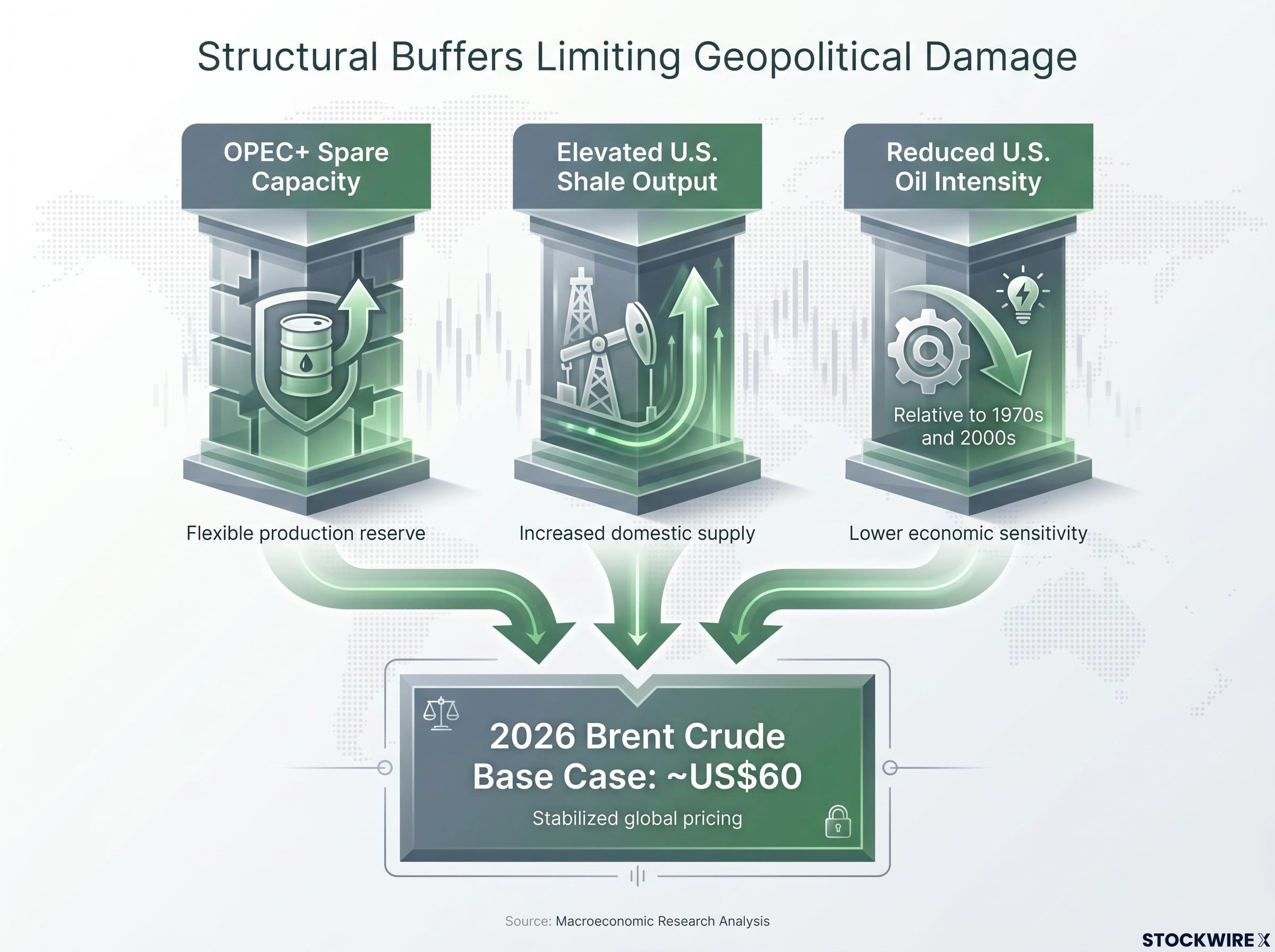

But the pattern is not just behavioural. It rests on structural buffers in global energy markets that make a supply-driven crisis less damaging than it would have been in previous decades:

Under the containment base case, JPMorgan expects Brent crude to average approximately US$60 for 2026 (a figure not independently confirmed but consistent with the bank’s broader framework). Even under a sustained conflict scenario, the bank’s more likely macro outcome is inflationary pressure rather than deep recession, an environment where earnings hold up with margin compression but do not collapse.

Two conditions would materially challenge JPMorgan’s call: severe disruption to energy infrastructure or a prolonged closure of the Strait of Hormuz. Under either scenario, the bank’s own framework does not suggest staying the course. It requires reassessment. The containment assumption is not a footnote; it is the foundation.

The earnings story is not just strong. It is structurally better distributed than it was, and that distribution is a core reason JPMorgan treats the buy-the-dip call as more durable this time.

Broadening market leadership, in plain terms, means earnings and price gains are spreading across more sectors and geographies rather than concentrating in a handful of megacap technology names. The valuation data supports this. The forward price-to-earnings premium of the Magnificent Seven over the broader S&P 500 has narrowed from approximately 1.7x to approximately 1.2x, according to JPMorgan’s research (this figure has not been independently confirmed externally).

That compression is not just a valuation story. It signals that the market’s earnings base has become less dependent on a small number of names that a single piece of bad news could disrupt, which directly strengthens the case for treating geopolitical dips as temporary rather than structural.

JPMorgan reinforces this by expressing a stated preference for international, emerging-market, and eurozone equities, not just U.S. megacaps. Morgan Stanley has offered a parallel observation, noting improving earnings growth and valuations in cyclical sectors:

Market leadership rotation away from US megacap technology is supported by valuation spreads between US Tech and international developed markets that are near multi-decade extremes, with MSCI EAFE trading at roughly a 50-55% forward P/E discount to the S&P 500 IT sector, which is the structural context behind JPMorgan’s stated preference for international and eurozone equities.

With full-year 2026 EPS revisions moving upward across all global regions, the geographic breadth of the earnings cycle gives markets more shock absorbers. For your own portfolio, the question this raises is whether your sector and geographic distribution positions you to benefit from the pattern JPMorgan is identifying, or whether concentration in a narrowing set of names leaves you more exposed than the broader market.

JPMorgan’s buy-the-dip framework is not risk-free, and the bank’s own published materials say so explicitly. The call comes with caveats that define the boundaries of the thesis, and those boundaries matter.

What strong earnings protect against:

What they do not protect against:

Treasury yield dynamics represent the policy error risk that JPMorgan names explicitly: with the 10-year yield at 4.66-4.67% and headline CPI accelerating from 2.9% in January to 3.8% in April 2026, the Fed lacks the rate-cut flexibility that historically served as the circuit breaker limiting geopolitical shock damage to corporate earnings.

JPMorgan’s materials name three specific risk factors that could reprice risk assets more severely: prolonged conflict, policy missteps, and sharper-than-expected inflation. The bank also emphasises that such views may not fit every investor’s risk tolerance, and that position sizing, diversification, and liquidity management remain non-negotiable regardless of the macro view.

Those caveats are not boilerplate for you. They define the specific conditions under which the dominant institutional recommendation of the moment stops applying. Knowing them is what separates informed positioning from trend-following.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

JPMorgan’s thesis is live and testable. The remainder of Q2 2026 earnings season is the real-time examination of whether the fundamental anchor holds. Three signals are worth tracking as results arrive over the next four to six weeks:

These three signals together form a real-time scorecard. Tracking them does not require waiting for the next JPMorgan note. It requires watching the same incoming data the strategists are watching.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. These statements are speculative and subject to change based on market developments and company performance.

JPMorgan's buy the dip strategy, led by strategist Mislav Matejka, recommends treating Iran-related equity selloffs as entry points rather than warnings, arguing that geopolitical shocks are transient and the current earnings cycle is strong enough to absorb them.

Roughly 80% of S&P 500 companies beat Q1 2026 estimates according to LSEG I/B/E/S data, Q1 EPS growth expectations were revised upward from 12.7% to 13.9% during the Iran situation, and full-year 2026 EPS projections have risen across every major global region.

JPMorgan's own framework requires reassessment if the conflict causes severe disruption to energy infrastructure or a prolonged closure of the Strait of Hormuz; the containment assumption is the load-bearing condition of the entire call.

JPMorgan treats the median EPS growth of roughly 8% across U.S. and eurozone companies as a more grounded target because it is less distorted by a small cluster of outsized performers, making the fundamental bar the market needs to clear considerably more achievable than the headline consensus implies.

Three real-time signals matter: whether the Q2 2026 beat rate stays near 80%, whether full-year EPS revisions continue trending upward across global regions, and whether Brent crude remains near JPMorgan's base case of approximately US$60, which serves as a proxy for the containment assumption holding.