JPMorgan: 80% S&P Beat Rate Makes Iran Selloffs a Buy Signal

4 mins ago

On 13 July 2026, JPMorgan’s strategist desk published a note that handed two sectors many investors treat as interchangeable cyclicals, Energy and Banks, entirely opposite verdicts. Banks earned an overweight. Energy did not. The reasoning behind that split tells you more about where risk-reward actually sits in H2 2026 than any single macro forecast.

The backdrop matters. Global growth is solid but cooling. The Strait of Hormuz closure has repriced energy risk across every asset class that touches oil. For the first time since early 2025, the gap between eurozone and US earnings revisions has nearly closed. And equity leadership is expected to rotate away from the Magnificent 7 toward sectors where valuations leave room for error. JPMorgan’s mid-year stance is less about whether equities go up and more about where within equities the asymmetry is sitting.

Here is the specific reasoning behind three sector-level calls from Mislav Matejka, Head of Global and European Equity Strategy at JPMorgan, and what each one means for how you think about your own allocation through the second half of the year.

JPMorgan’s base case is solid but uneven global growth. US expansion ran above 3% early in the year and is cooling toward approximately 2% by year-end, with no outright recession call attached. The firm’s Asset Management arm characterises the trajectory as a manageable deceleration rather than a stall.

The Strait of Hormuz closure complicates the picture. The energy price shock has pushed headline inflation higher and narrowed central bank flexibility, but JPMorgan treats this as a temporary disruption with scope for normalisation in H2 2026, not a structural break.

Four data points from the Matejka note underpin the constructive lean:

That combination, growth softening but not breaking, inflation elevated but not runaway, tells you this is not a moment to rotate fully defensive or fully risk-on. It is a moment to pick within equities on the basis of valuation buffer and earnings trajectory. The investors who treat H2 2026 as a generic late-cycle retreat or a straightforward recovery will miss the sector-level differentiation where most of the return potential sits.

The near-term catalyst is specific. Matejka’s 13 July note flags that JPMorgan’s strategists expect the banking sector’s quarterly results to come in reassuringly during the current earnings season. That is not a vague macro view; it is a timing hook with a defined window.

The timing of JPMorgan’s overweight call is not incidental: the current bank earnings season is already delivering early Q2 2026 results with S&P 500 financials beating EPS estimates by 13%, giving the thesis an immediate empirical test before the ink on the strategist note is dry.

Earnings season catalyst: JPMorgan’s strategist desk anticipates that upcoming bank reporting results will provide investors with comfort, underpinning the overweight call in the current cycle.

The valuation case layers on top. Financials are flagged as more reasonably valued compared with expensive mega-cap growth stocks and carry less dependence on earnings perfection. In a market where the Magnificent 7 have absorbed enormous capital, banks offer cyclical exposure at a fraction of the valuation premium.

Three pillars support the thesis:

For an investor sitting on a portfolio still heavily weighted toward US mega-cap growth, this call reframes the rotation into financials. It is not a defensive retreat. It is a valuation-led move toward a sector with near-term earnings catalysts already in view.

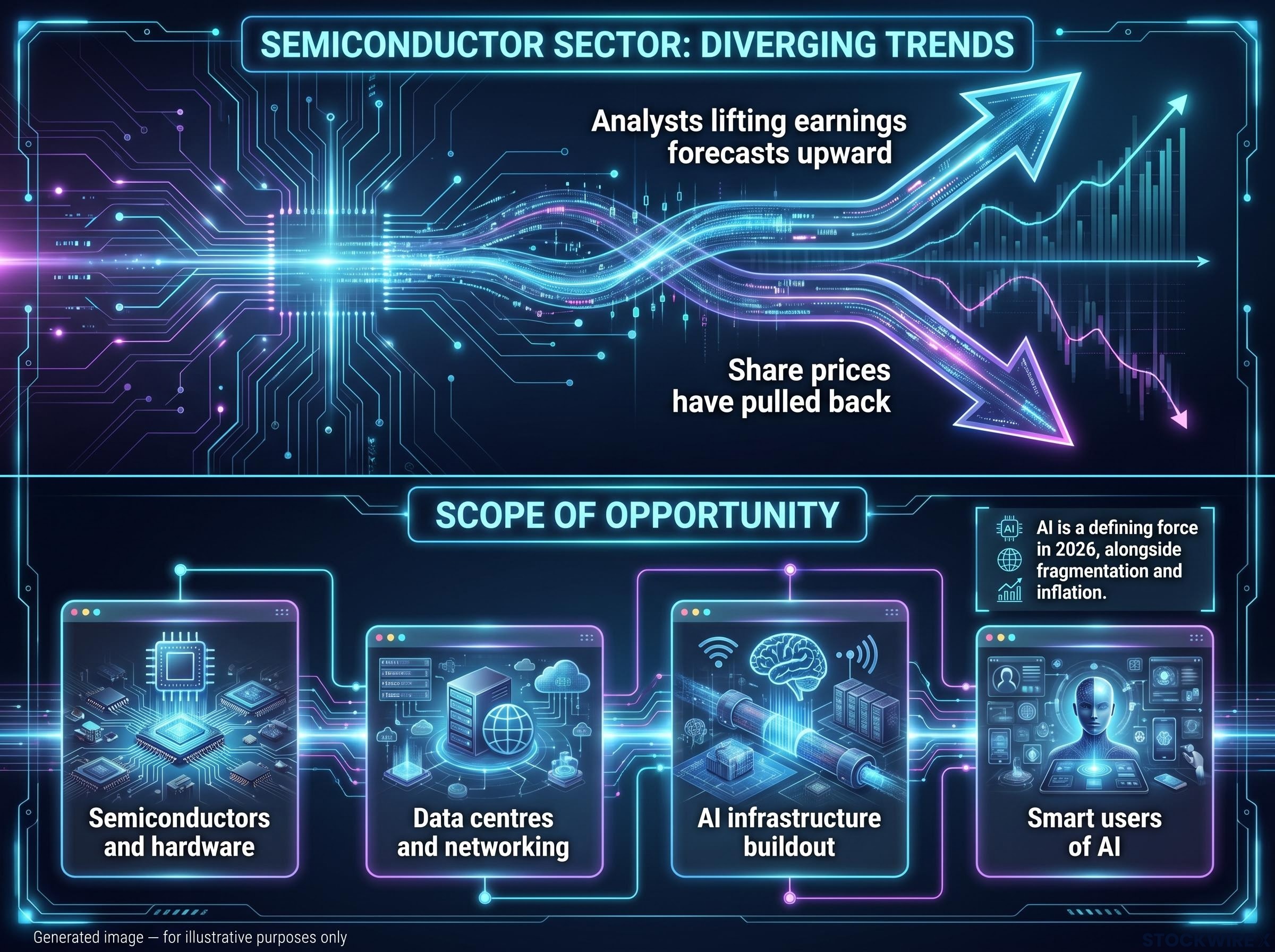

The pattern Matejka identifies is precise: analysts have been lifting their semiconductor earnings forecasts upward at the same time that share prices have pulled back. That divergence, professional analysts upgrading their fundamental view at the same moment short-term traders are selling, is the operative signal.

The dislocation: Analysts have continued revising semiconductor earnings estimates upward even as share prices have retreated, a gap JPMorgan views as signalling a potential entry point for investors willing to look through near-term noise.

JPMorgan’s broader research places this observation inside a structural thesis. Across the Private Bank, Wealth Management, and Global Research divisions, artificial intelligence is identified as one of three defining forces for markets in 2026 (alongside fragmentation and inflation). The semiconductor complex sits at the centre of that force.

AI infrastructure investment driving semiconductor earnings was already a documented trend before JPMorgan’s July note, with first-quarter results across the chip complex confirming that capital spending on data centres and networking was translating into measurable revenue upgrades across the supply chain.

The scope of the opportunity extends well beyond the largest chip names. JPMorgan’s strategists include:

Volatility is not something the call ignores. JPMorgan’s guidance accepts that the AI supply chain will remain volatile, and strategists advise siding with the structural earnings story rather than transient sentiment. The firm characterises the bigger risk as missing the upside rather than timing a bubble burst.

What the earnings-revision-versus-price divergence tells you is that the professional consensus on semiconductor fundamentals is strengthening at a moment when market pricing says otherwise. Historically, the revision trend has been the more reliable indicator of forward returns.

This is the most instructive of JPMorgan’s three calls because it challenges a reflex most investors carry: that a commodity price spike automatically makes energy equities attractive. Matejka’s diagnosis is specific. The energy sector has lost the valuation buffer it would need to absorb a drop in oil prices. A valuation margin of safety means the gap between where a stock trades and where it would trade if the commodity price dropped back to more normal levels. When that gap is wide, you have a cushion. When it is narrow, you are effectively making a leveraged bet that prices stay elevated.

If oil prices normalise in H2 2026, as JPMorgan’s Asset Management arm expects, current energy equity valuations that assume persistently high prices will face compression. The cushion is gone.

Oil price normalisation is the critical assumption buried inside JPMorgan’s energy caution: Brent surged from a pre-conflict baseline of $72-74 to a peak of $126 per barrel following the Strait of Hormuz closure, and even a partial reversal toward that baseline would compress energy equity valuations that are currently priced for persistence.

| Asset Category | Valuation Assessment | H2 Price Risk | Recommended Role |

|---|---|---|---|

| Traditional oil and gas equities | No valuation margin of safety | High (exposed to oil normalisation) | Caution / underweight |

| LNG, renewables, grid modernisation | Supported by structural demand | Lower (less tied to spot oil) | Selective hedge and transition exposure |

JPMorgan’s Private Bank favours gold and natural resources as geopolitical hedges, but steers that exposure toward LNG, renewables, and grid modernisation rather than conventional producers. The Wealth Management division frames commodities and infrastructure as inflation toolkit components, not growth bets.

An investor buying broad energy exposure today is effectively taking a leveraged view that oil prices stay elevated through year-end. That is the opposite of what JPMorgan’s macro team expects to happen.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The most underappreciated finding in the Matejka note sits outside the headline sector calls. Eurozone earnings revisions have turned positive and are drawing close to parity with their US counterparts for the first time since early 2025, with Matejka’s team forecasting robust double-digit EPS gains for the eurozone across full-year 2026.

Revision parity: The gap between eurozone and US earnings revisions has largely closed, with both now moving in similar directions, pointing to a widening of the global earnings recovery beyond a single region.

That convergence matters because eurozone earnings had largely gone sideways from 2022 onward with little meaningful progress. This is not an outlier bounce. It is a shift in the underlying earnings cycle, supported by three data points JPMorgan cites:

The eurozone earnings quality question adds an important caveat to the revision parity signal: STOXX 600 headline growth of 10-15% in 2026 is largely a commodity story, and strip out energy and basic materials and the underlying ex-commodity growth rate falls to approximately 5-6%, a gap that changes how the revision convergence should be interpreted.

The conditionality is explicit. The double-digit EPS projection from Matejka’s team is premised on the Iran conflict remaining contained and not flaring further across H2 2026. That is the primary downside risk to this part of the thesis.

For an investor running a predominantly US equity portfolio, this convergence changes the diversification case. International allocation is no longer just a valuation argument. It is an earnings momentum argument, and momentum has historically been a more durable basis for relative outperformance than valuation discount alone.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

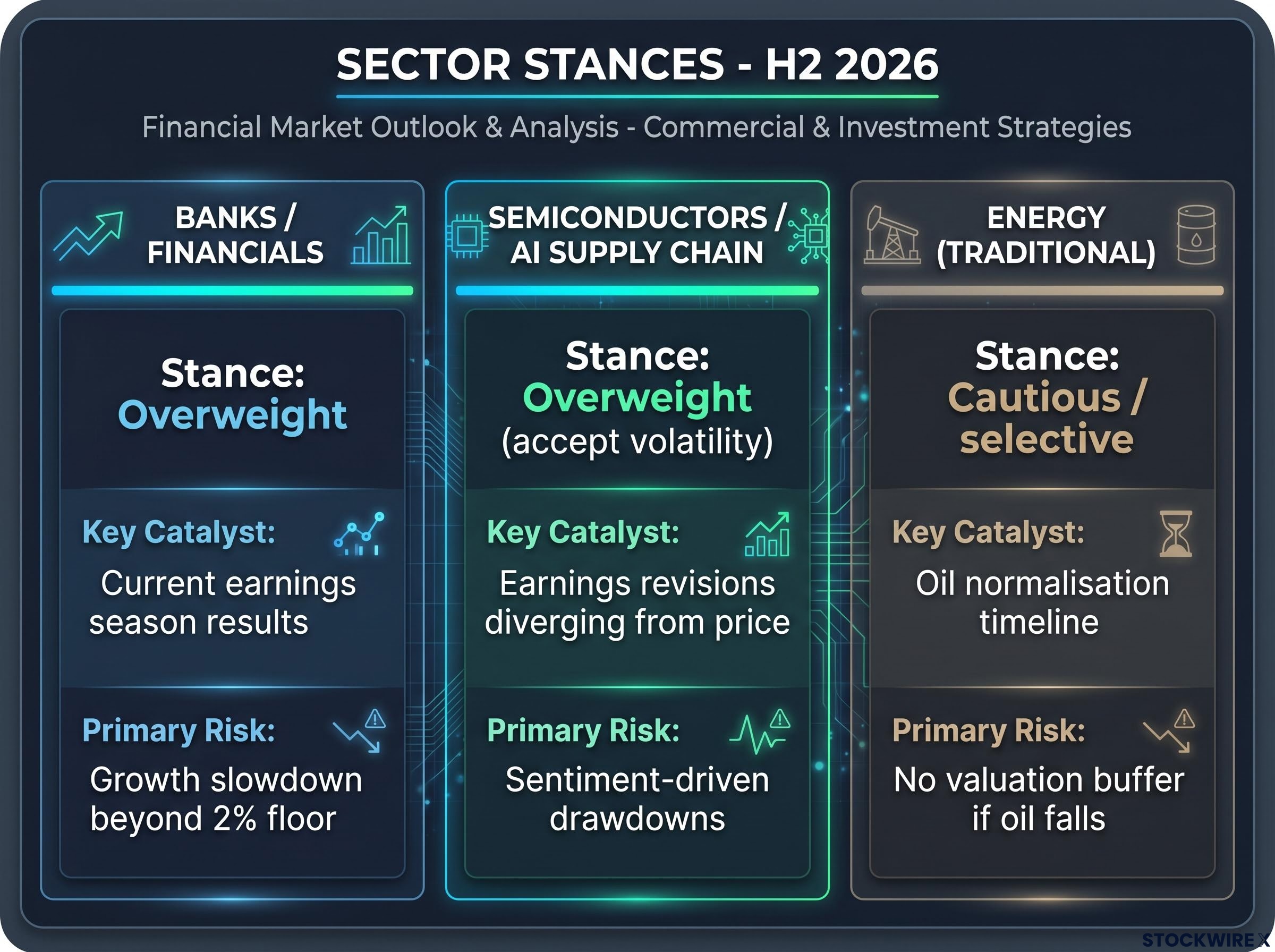

The three sector calls are not isolated recommendations. They share a single underlying logic: valuation buffer plus earnings revision momentum. Banks have both. Semiconductors have revision momentum plus a structural thesis that justifies riding through price volatility. Traditional energy has neither, which is why the call tilts toward transition assets instead.

| Sector | JPMorgan Stance | Key Catalyst | Primary Risk |

|---|---|---|---|

| Banks / Financials | Overweight | Current earnings season results | Growth slowdown beyond 2% floor |

| Semiconductors / AI supply chain | Overweight (accept volatility) | Earnings revisions diverging from price | Sentiment-driven drawdowns |

| Energy (traditional) | Cautious / selective | Oil normalisation timeline | No valuation buffer if oil falls |

For an investor holding all three sectors and deciding on relative sizing, the decision sequence runs in this order:

That framework is portable. It works beyond these three sectors because the underlying screen, valuation buffer plus revision momentum, applies anywhere an investor is choosing between competing allocation options.

The coherence of JPMorgan’s H2 2026 playbook comes from a single analytical thread: every sector call runs through the same two filters. Valuation buffer and earnings revision direction. That consistency means the framework remains useful even for investors who want to adapt the specific weightings to their own risk tolerance.

The single most important variable to monitor is the trajectory of the Iran conflict and oil prices. An escalation simultaneously weakens the Energy normalisation thesis, raises inflation risk for Financials margin assumptions, and introduces a risk-off sentiment headwind for Semiconductors. It is the scenario that breaks the most elements of the framework at once.

Four forward signals tell you whether the conditions justifying these sector tilts remain intact:

These statements reflect JPMorgan’s published views as of 13 July 2026 and are subject to change based on market developments and geopolitical conditions.

A thesis with clearly identified conditions and break points is more actionable than a directional call with no exit criteria. The sector tilts JPMorgan recommends are not permanent positions. They are conditional bets with defined signals that will tell you when the conditions have changed.

For investors wanting to see where institutional money is already moving in response to stretched AI valuations, our deep-dive into 2026 institutional capital flows tracks specific ETF price levels across energy, industrials, healthcare, and real estate that signal whether the reallocation away from mega-cap technology has staying power.

A valuation margin of safety is the gap between where a stock trades and where it would trade if its underlying commodity or earnings driver reverted to normal levels. JPMorgan flagged that traditional energy equities have lost this buffer, meaning any oil price normalisation would compress their valuations with no cushion to absorb the move.

JPMorgan's overweight on Banks rests on three pillars: financials trade at a discount to mega-cap tech, the macro environment still supports net interest margins and loan growth, and Q2 2026 bank earnings are already beating EPS estimates by 13%, giving the thesis an immediate empirical confirmation.

Analysts have been raising semiconductor earnings forecasts at the same time share prices have pulled back, a divergence JPMorgan views as a potential entry point. Historically, the earnings revision trend has been a more reliable indicator of forward returns than short-term price sentiment.

Energy equities have priced in persistently elevated oil following the Strait of Hormuz closure, but JPMorgan expects oil prices to normalise in H2 2026. With no valuation buffer remaining, any reversal toward pre-conflict Brent levels of around $72-74 per barrel would directly compress energy equity valuations.

Eurozone earnings revisions have closed the gap with US revisions for the first time since early 2025, with Matejka's team forecasting double-digit EPS gains for the eurozone across full-year 2026. This shifts the case for international diversification from a valuation argument to an earnings momentum argument, which has historically been a more durable basis for relative outperformance.