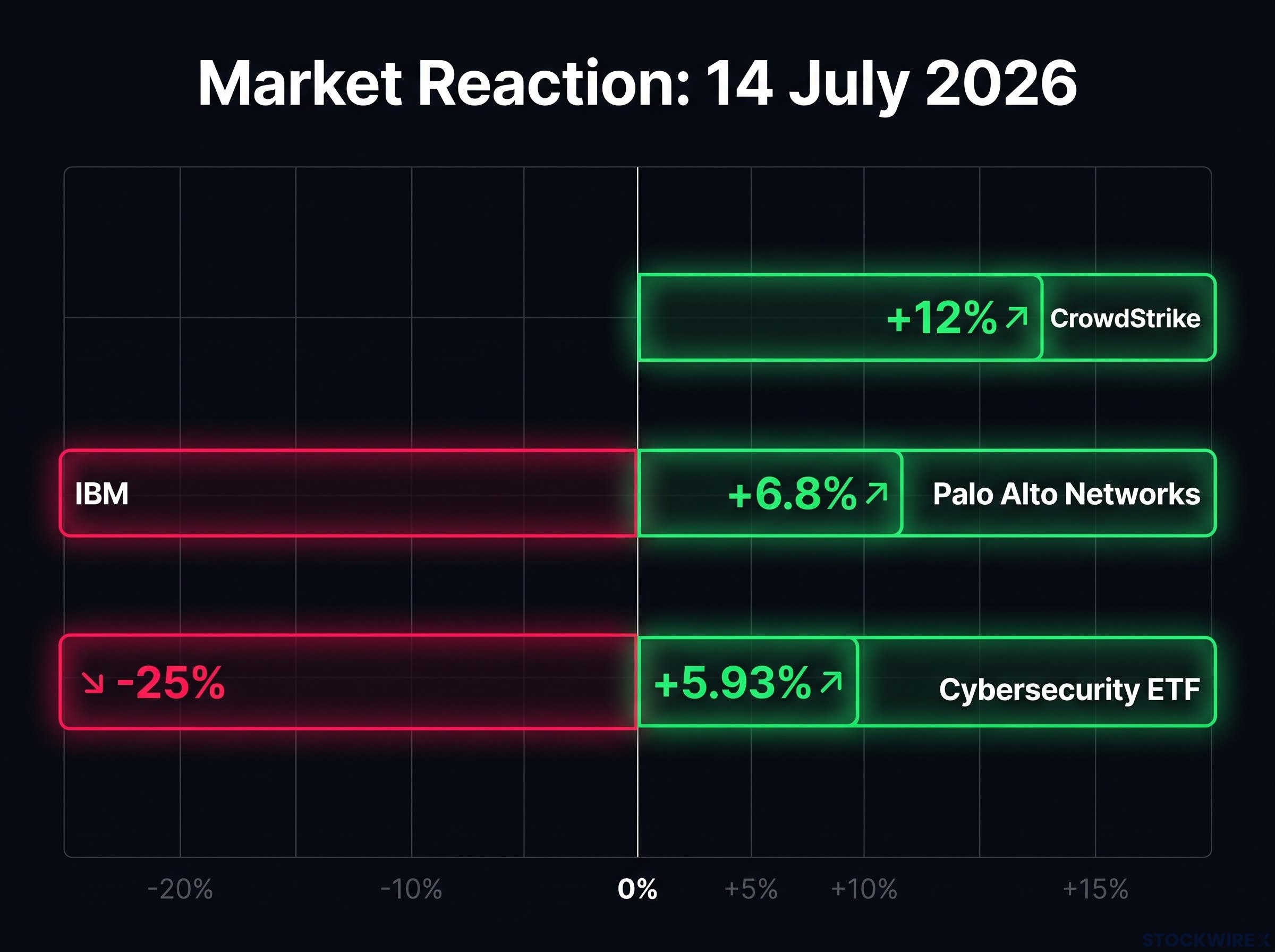

IBM recorded its most severe single-day share price fall ever when it shed roughly 25% of its value on 14 July 2026, a move that eclipsed the previous worst session in the company’s long trading history. The same results announcement that hammered IBM propelled CrowdStrike to a fresh all-time high and carried the cybersecurity sector up by close to 6% across the session.

The surface read is a disappointing quarterly result from a legacy technology provider. The more important read is what IBM’s management said about why: enterprises are not cutting technology budgets, they are redirecting them, and cybersecurity is where the money is going. That distinction carries direct portfolio implications across two sectors, not one.

Here is the full picture of what IBM actually reported, why the market reacted the way it did across both sectors, and how to use this type of cross-sector earnings event as an investment signal rather than noise.

IBM’s Q2 numbers and what actually missed

IBM’s preliminary second-quarter FY2026 results showed a company still growing revenue year over year, but growing at the wrong speed and in the wrong places.

| Metric | Reported | Year-over-year change | vs. consensus |

|---|---|---|---|

| Revenue | US$17.2 billion | Up approx. 1% | Below estimates |

| GAAP diluted EPS | US$2.27 | Down approx. 2% | Below estimates |

| Operating (non-GAAP) diluted EPS | US$2.93 | Up approx. 5% | Below estimates |

The segment breakdown tells you where the pressure sat:

- Software revenue grew approximately 5%.

- Consulting revenue was roughly flat, up approximately 1% at constant currency.

- Infrastructure revenue declined approximately 7%.

A company growing revenue year over year does not crater 25% over a single quarter unless investors believe the problem is structural, not temporary. That anxiety is exactly what IBM’s own commentary introduced.

The late-quarter IT budget squeeze that IBM described was more specific than a generalised slowdown: enterprises redirected funds into high-bandwidth memory and server hardware, deferring IBM’s highest-margin Transaction Processing software renewals and IBM Z mainframe upgrades rather than cancelling them outright.

When big ASX news breaks, our subscribers know first

A 25% drop that rewrote the record books

On 14 July 2026, IBM shares closed down approximately 25%, marking the steepest single-session loss in the company’s history and overtaking the previous record of 23.7% reached in the October 1987 market crash.

IBM’s approximately 25% single-session decline on 14 July 2026 surpassed its prior record of 23.7%, set during the October 1987 market crash.

A stock that has traded publicly for over a century does not set a new single-day loss record because of a revenue miss alone. What spooked the market was the forward-looking implication of IBM’s own commentary about how enterprise clients are changing their spending behaviour.

That distinction matters. A move of this magnitude is not automatically a signal to buy or sell. It is a flag that market participants repriced something they consider fundamental about the business, not just a quarterly number.

What the spending shift really means (and why IBM said it matters)

The financial results were the headline. Management’s explanation was the signal.

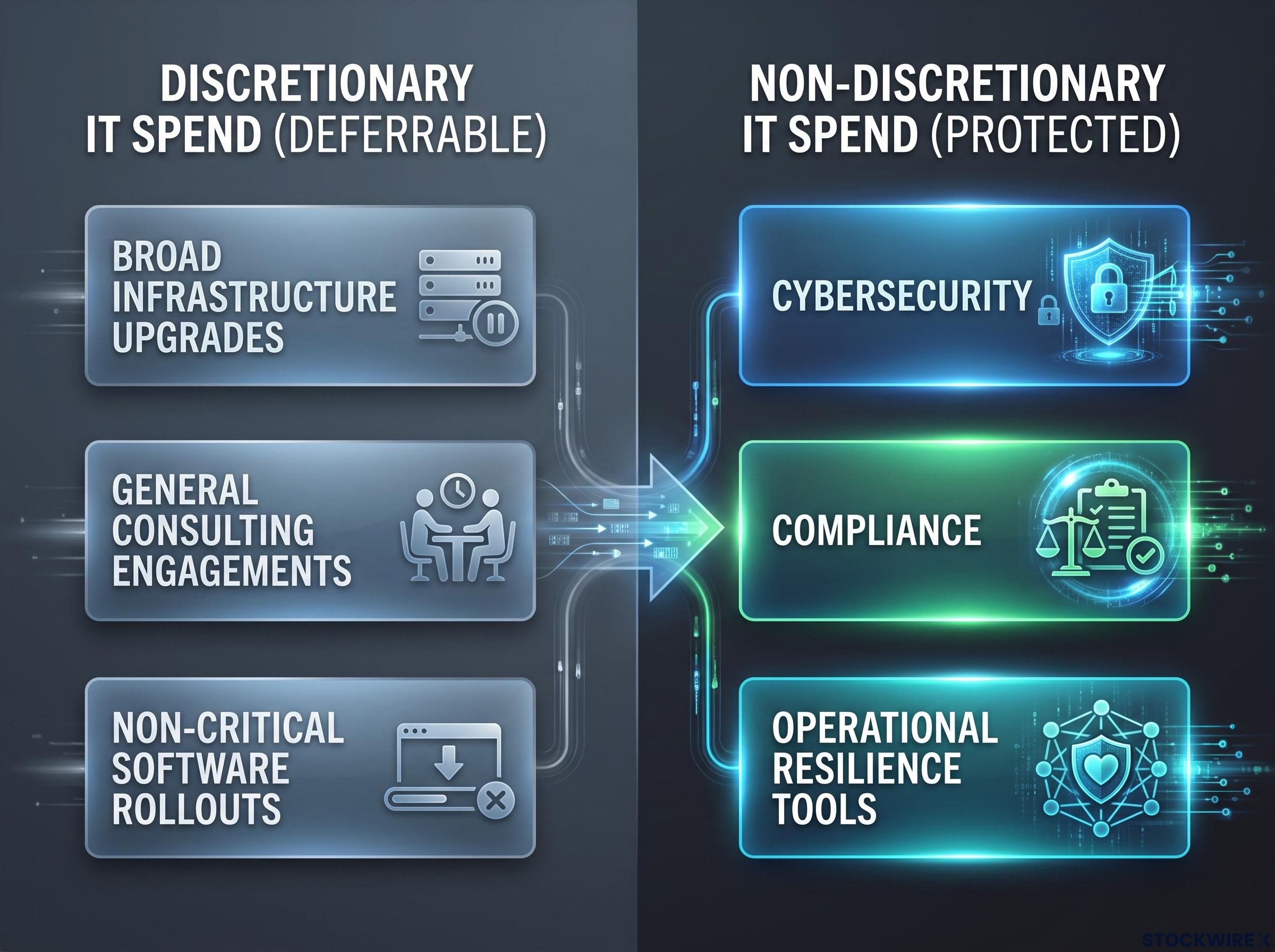

IBM pointed to a worsening in discretionary IT spending as a key source of pressure. Discretionary spending, in this context, refers to technology projects that are useful but not mission-critical: upgrades, expansions, and nice-to-have modernisations that enterprises can delay without immediate operational risk.

Management also noted that clients were grappling with what the company described as “rapidly evolving, industry-wide cybersecurity concerns.”

Earnings call commentary, particularly the Q&A session where management responses are unrehearsed, often reveals shifts in confidence through hedging language and metric switching that the prepared press release is designed to obscure.

“Rapidly evolving, industry-wide cybersecurity concerns.”

That language positions cybersecurity as non-discretionary, the kind of spending enterprises cannot defer even when budgets tighten. IBM presented this as an industry-wide condition rather than something peculiar to its own business, and indicated that softening discretionary budgets were likely to emerge as the dominant story across software companies more broadly.

The key categories to separate:

- Discretionary IT spend (deferrable): broad infrastructure upgrades, general consulting engagements, non-critical software rollouts.

- Non-discretionary IT spend (protected): cybersecurity, compliance, and operational resilience tools.

When a company of IBM’s scale and customer diversity says budgets are moving toward cybersecurity and away from general IT, that is enterprise-buyer-side confirmation of a spending thesis. You should read it as one.

How cybersecurity vendors went from bystanders to beneficiaries

IBM’s worst day became the cybersecurity sector’s best. The logic is straightforward: IBM told the market that enterprises are prioritising security spending above almost everything else, and the companies that specialise in security immediately benefited from that confirmation.

| Security name | Session gain (14 July 2026) | Context |

|---|---|---|

| CrowdStrike | +12% | Reached all-time high |

| Palo Alto Networks | +6.8% | Session outperformance |

| Cybersecurity ETF | +5.93% | Broad sector move |

Over the twelve months preceding the announcement, the BetaShares Global Cybersecurity ETF had already gained approximately 17%. For investors who entered at the 13 April 2026 low, returns had reached roughly 55% by the time of the report.

The fact that the cybersecurity sector was already outperforming before IBM’s announcement tells you this rally was confirmation, not speculation. IBM validated what dedicated security vendors had been signalling through their own results and guidance for months. That distinction matters when assessing whether the move reflects durable demand or just a sentiment spike.

AI cybersecurity stocks have benefited from a structural asymmetry between attackers and defenders: AI-accelerated vulnerability scanning has outpaced conventional patch cycles, making security spending non-deferrable at the enterprise level in a way that general IT modernisation projects are not.

Reading cross-sector earnings signals: a framework for investors

This kind of episode, where one company’s bad quarter lights up an adjacent sector, is not a one-off curiosity. It is a repeatable pattern, and there is a structured way to approach it.

The first step is separating two types of earnings commentary. “Demand is weak everywhere” is a broadly negative signal. “Clients are diverting money toward X” is a roadmap to beneficiaries. IBM’s commentary falls squarely into the second category: budgets are not disappearing, they are moving toward security.

The framework:

- Identify what management blames. Look for the specific problem or spending category management names as the pressure point. IBM named cybersecurity pressures and discretionary deferrals.

- Map which vendors solve that named problem. The companies positioned precisely in the priority category, here pure-play security vendors like CrowdStrike and Palo Alto Networks, are the logical beneficiaries.

- Check whether those vendors are already in an uptrend. If adjacent names are already outperforming, the earnings commentary is confirming an existing thesis, not creating a new one. Confirmation signals are stronger than surprises.

The valuation caution that belongs next to every demand signal

Cybersecurity leaders frequently trade at premium multiples. A positive demand signal accelerates price moves that may already reflect optimistic assumptions. That does not mean the demand thesis is wrong, but it does mean specific risks remain: multiple compression if interest rates rise, and earnings volatility if aggressive expectations are missed.

Validate the demand thesis first, then apply a valuation filter before acting. The two steps are sequential, not optional.

The next major ASX story will hit our subscribers first

What comes next for IBM, and what the market is pricing in now

The forward question for IBM is binary, and management has not answered it clearly yet.

- Cyclical pause: Discretionary IT spending normalises over the next few quarters, IBM’s software and infrastructure divisions recover, and the stock becomes a value or income opportunity at a lower base.

- Structural headwind: Enterprise buyers increasingly prefer specialist vendors over integrated suites, IBM’s budget share continues to shrink, and capital is better deployed elsewhere.

The divisions under pressure, software and infrastructure, were central to IBM’s growth narrative. Their underperformance, set against the simultaneous outperformance of dedicated security vendors, is the clearest evidence of spending rotation in enterprise IT this year.

The honest position is to hold that ambiguity explicitly. A record single-day decline is neither a buying opportunity nor a final verdict until the question of cyclical versus structural gets a clearer answer from subsequent quarters.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

IBM’s record day as a spending map, not just a stock story

IBM’s worst single-day loss in over a century of public trading is less meaningful as an IBM story than as a signal about where enterprise technology budgets are flowing. Cybersecurity absorbed budget from discretionary IT categories, and the market priced that shift in real time across two sectors simultaneously.

The cybersecurity rally that followed was not speculative noise. It was a logical market response to credible, enterprise-buyer-side confirmation of a spending shift that was already underway.

The IBM-driven spending rotation sits inside a larger macro context: enterprise technology spending reached a record 4.9% of US GDP in Q1 2026, surpassing both the dot-com era and the cloud buildout peak, with rewards concentrated in infrastructure and security layers rather than in broad application stocks.

The habit this event should build is straightforward: treat large-incumbent earnings commentary as an early-warning system for cross-sector spending rotation, apply valuation discipline before acting on the signal, and read the commentary before you read the stock price.