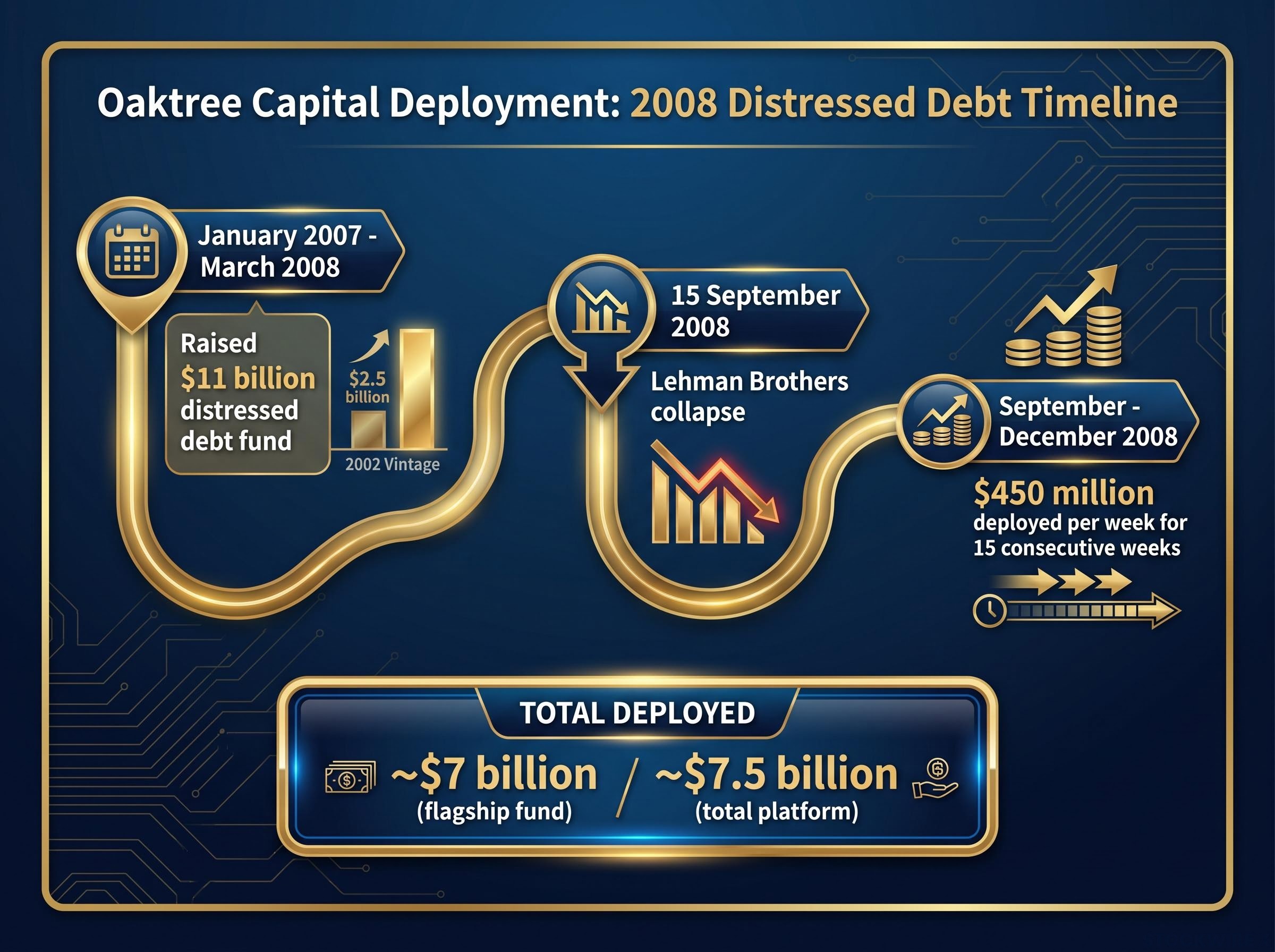

Between September and December 2008, Oaktree Capital Management committed roughly $450 million every week for 15 consecutive weeks. That was not a figure of speech. It was a rate of capital deployment that most institutional investors would struggle to execute in calm markets, let alone during the worst financial crisis since the Great Depression.

The collapse of Lehman Brothers on 15 September 2008 did not create Oaktree’s opportunity so much as trigger the plan they had already built. Behind the deployment sat an $11 billion distressed debt fund raised between January 2007 and March 2008, a 20-year credibility record with institutional investors, and a decision framework designed to function under genuine uncertainty rather than requiring its resolution.

Howard Marks’s investing strategy through that period remains one of the most documented examples of crisis capital deployment on record. This piece unpacks the specific logic Oaktree used, the behavioural record they built over two decades, and the psychological posture they maintained, so you can assess which elements are genuinely replicable and which required Oaktree’s specific institutional scale and timing.

What Oaktree actually did in the 15 weeks after Lehman

The timeline matters because it tells you something about the nature of the decision. Lehman Brothers filed for bankruptcy on 15 September 2008. Within days, Oaktree began deploying from its flagship distressed debt fund at a pace that left no room for deliberation in real time.

The key figures:

- $450 million per week, averaged across 15 consecutive weeks

- Approximately $7 billion deployed from the flagship distressed fund alone

- Roughly $7.5 billion when including purchases across the broader Oaktree platform (public accounts cluster around $6-7 billion depending on scope)

- The fund itself was $11 billion, raised between January 2007 and March 2008, compared to Oaktree’s prior largest distressed fund at just $2.5 billion (the 2002 vintage)

- Bruce Karsh led the operational execution. Marks was the philosophical architect; Karsh was the one committing capital in real time.

“Unless a second Great Depression lay ahead, acquisitions made at those prices should yield significant returns.” — Howard Marks, October 6, 2008 memo

That deployment rate tells you the decision to act had been resolved before the crisis arrived, not during it. At $450 million per week, there was no room for debate. The capital was pre-raised, the legal structures were in place, and the investment criteria were pre-committed. What looked from outside like a bold call made in the fog was, from inside, the execution phase of a plan set in motion years earlier.

When big ASX news breaks, our subscribers know first

The logic of acting when you cannot know the outcome

The most common misreading of Oaktree’s 2008 deployment is that Marks was confident the system would survive. He was not. He has been explicit that Oaktree had no usable historical data or analogous prior experience to draw on. The Great Depression, the closest historical reference, operated under different monetary regimes and regulatory structures. Real-time data was noisy and backward-looking. The range of outcomes, including systemic breakdown, was not knowable in probabilistic terms.

This is the formal distinction between risk and uncertainty. Risk describes situations where outcomes follow known probability distributions based on historical data; you can price it. Uncertainty describes genuinely novel environments where historical analogies are inadequate; you cannot price it, only navigate it. Oaktree was operating in the second regime.

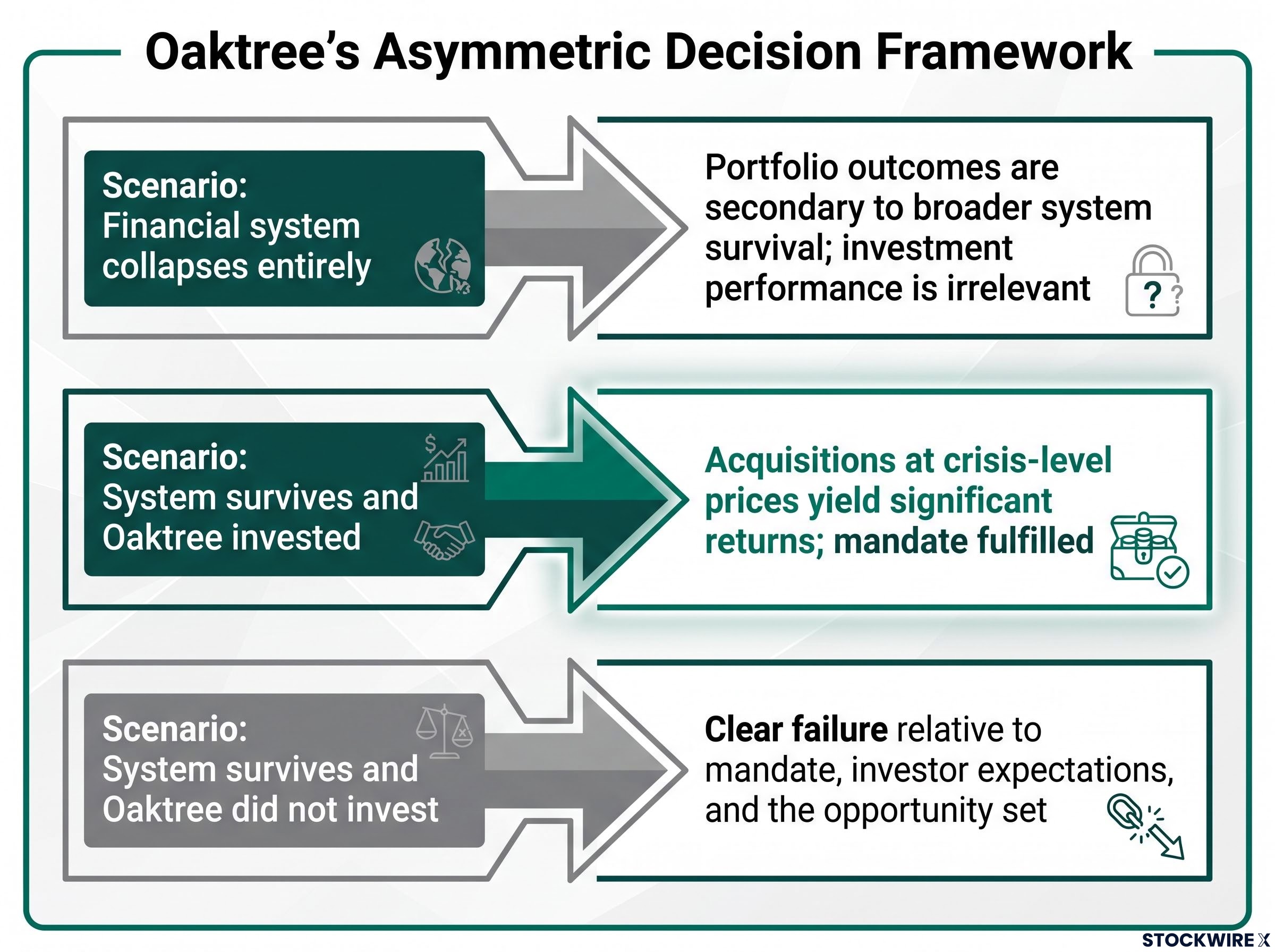

Rather than manufacturing certainty, Marks structured his thinking around an asymmetric framing, one that collapsed a paralysing question into a tractable decision. The logic works across three scenarios:

| Scenario | Implication for acting vs. not acting |

|---|---|

| Financial system collapses entirely | Portfolio outcomes are secondary to broader system survival; investment performance is irrelevant in this state of the world regardless of positioning |

| System survives and Oaktree invested | Acquisitions at crisis-level prices yield significant returns; mandate fulfilled |

| System survives and Oaktree did not invest | Clear failure relative to mandate, investor expectations, and the opportunity set Oaktree was specifically built to exploit |

The decision did not require confidence that the system would survive. It required only the recognition that failing to act in a survivable scenario was demonstrably worse than acting, while in the non-survivable scenario, the portfolio outcome was irrelevant either way.

During the pandemic, a Harvard epidemiologist described a three-tier model for decision-making under uncertainty: available data, analogies drawn from prior experience, and supposition. Marks applied this hierarchy explicitly to the Lehman moment, noting that data was unreliable and historical analogies were absent, leaving supposition as the only honest instrument. Treating that openly as a legitimate analytical input, rather than a confession of ignorance, is itself a disciplined epistemic stance.

How the margin of safety made the logic executable

The asymmetric framework was the reasoning; the instrument selection made it operational. Oaktree bought the senior-most debt of high-quality, recently leveraged-buyout companies, meaning the debt sat at the top of the capital structure with the strongest legal claims on assets. Their entry prices were sufficiently depressed that the positions would still have broken even had those businesses turned out to be worth as little as one-fifth or one-quarter of the price private equity had originally paid for them.

The thesis required only that companies avoided total annihilation, not that they recovered to prior valuations. That made the investment robust under extreme pessimism, not just optimism with a margin bolted on.

Oaktree’s distressed debt mandate is built on the same arithmetic that makes loss avoidance more powerful than equivalent gains: a position that breaks even in the worst survivable scenario and generates significant returns in the base case has a structural edge over one that requires a favourable outcome to avoid permanent capital impairment.

For any investor facing a novel environment, this is the transferable principle: when you cannot resolve uncertainty, the question shifts from “what will happen?” to “which error is worse if I am wrong, and in which state of the world does each error occur?”

Why trepidation is a calibration signal, not a weakness to manage

In his Taking the Temperature memo, Marks reviewed the five significant macro calls he made across roughly 26 years of investing. His consistent observation was that every one of those decisions carried genuine doubt at the moment it was made. The pattern was not confident action; it was committed action in the presence of uncertainty.

He recounted an exchange from the 1998 market disruptions, which included the Long-Term Capital Management collapse, the Russian ruble crisis, and Southeast Asian financial instability. A young portfolio manager was hesitant to commit capital. Marks urged him to act anyway, comparing the behaviour to a soldier advancing under fire.

The comparison was deliberate: the expectation was not that the fear would disappear, but that the professional would act through it because the mission required it.

Marks has acknowledged he is exposed to the same negative news flow as every other investor when markets are falling. He must consciously override that signal to reach a contrarian conclusion. Oaktree’s 25-year retrospective frames the firm’s approach plainly: risk control in good times, shifting to risk-bearing when potential rewards are greatest, with the explicit note that this shift is psychologically difficult by design.

When trepidation arrives, investors default to one of three modes:

The three failure modes Marks identifies, paralysis, performed certainty, and deliberate action through acknowledged anxiety, map directly onto the documented behavioural biases concentrated at the sell decision: loss aversion drives paralysis, recency bias and herd behaviour drive paralysis or performed certainty, and only a pre-committed process enables the third mode.

- Paralysis: the anxiety overwhelms the process, and no action is taken

- Performed certainty: the anxiety is suppressed and decisions are made without the caution the environment warrants

- Deliberate action through acknowledged anxiety: Oaktree’s model, where discomfort informs position-sizing and risk calibration rather than being ignored or surrendered to

Marks’s position is that anyone making major investment decisions without anxiety is probably miscalibrated. The absence of fear in genuinely dangerous situations is itself a warning sign.

For any investor managing a portfolio through a drawdown or dislocation, this reframes the question. It is not “how do I become more confident?” It is “am I using my discomfort as data, or am I defaulting to paralysis or performed certainty?”

Two decades of counter-intuitive behaviour that made $11 billion possible

The $11 billion fundraise looks, in isolation, like a stroke of timing. It was not. It was the withdrawal on 20 years of deposited trust.

Since its 1995 founding, Oaktree had managed capital through the 1991 downturn and the 2001-2002 credit dislocation. Those cycles gave investors direct evidence that Oaktree’s distressed strategy performed when it mattered most. But the credibility asset was built through something less obvious: Oaktree’s explicit policy of reducing fund sizes following strong performance periods.

This is the direct opposite of industry convention. Most asset managers raise their largest funds after their best returns, capitalising on the marketing window. Oaktree did the reverse. The logic was straightforward: strong prior returns indicate that assets have appreciated and future opportunity in those strategies has diminished. Raising more capital into a depleted opportunity set would dilute returns and erode the track record.

| Industry convention | Oaktree approach |

|---|---|

| Raise largest funds after strongest returns | Reduce fund sizes when opportunity is thin, even at cost to fee revenue |

| Fundraise when investor enthusiasm is highest | Raise crisis-ready capital while conditions are calm, before sentiment turns |

| Project confidence and certainty to investors | Communicate doubt openly when warranted |

| Deploy capital to justify management fees | Hold dry powder through extended periods, deploying only when pricing meets criteria |

| Align fund size with fee revenue targets | Align fund size with available opportunity, accepting reduced fees when opportunity is limited |

Over roughly 12-13 years, this behaviour communicated something that marketing alone cannot: when Oaktree signalled opportunity, it reflected genuine conviction rather than an asset-gathering motive. Karsh’s personal investing reputation reinforced the institutional credibility.

The implication for any investment professional building a practice is uncomfortable but precise: the behaviours that build durable credibility (smaller funds when returns are high, consistent philosophy through cycles) are exactly the behaviours that cut short-term revenue and require the most explanation to clients.

Reading market temperature without forecasting the future

Marks does not claim to predict crises. He claims to read the market’s temperature, and the distinction matters.

The temperature framework tracks three signals: risk appetite, credit standards, and investor behaviour. When the environment is characterised by too much trust and too little worry (loose lending, compressed spreads, aggressive deal structures), the temperature is elevated. When fear is extreme and prices reflect disaster scenarios, the temperature is depressed. Neither reading tells you when conditions will change. Both tell you how to position.

The temperature signals Marks tracked in 2007, compressed spreads, loosening covenants, and capital chasing yield into structurally weaker positions, are directly analogous to the fragile market conditions that institutional strategists at Morgan Stanley, J.P. Morgan, and Robeco are flagging in mid-2026, including narrow AI-linked leadership and private credit liquidity risk.

The $11 billion fundraise between January 2007 and March 2008 was a direct output of this framework. Markets were still functioning well enough to raise capital, but the temperature reading, specifically the reckless behaviour in credit markets, indicated a crisis was building. Marks did not know when it would arrive or how severe it would be. He knew the conditions that would create distressed opportunities were accumulating.

The temperature-reading process follows a sequence:

- Assess credit standards: are lenders loosening terms, extending duration, or accepting weaker covenants?

- Observe investor risk appetite: are capital allocators reaching for yield, compressing risk premiums, or ignoring structural risks?

- Evaluate pricing relative to historical norms: are spreads and yields consistent with the risk being assumed?

- Calibrate fund size and dry powder accordingly: accumulate reserves when temperature is elevated

- Pre-commit the legal and investor structure before conditions shift: raise capital while fundraising is socially acceptable

Positioning before the dislocation, not during it

Here is the structural asymmetry that most investors underestimate: the same conditions that create investment opportunity (fear, forced selling, distressed pricing) simultaneously make it nearly impossible to raise new capital or establish new investor relationships. Negative sentiment that drives prices to crisis levels also drives investors to redeem, cut risk, and freeze commitments.

This is a sequencing problem, not a courage problem. The decisive action is the preparation, not the deployment. The temperature framework tells you this is actionable today: the question is not “when will the next dislocation occur?” but “what does current credit behaviour, risk appetite, and pricing tell you about where you are in the cycle, and are you positioned to act or constrained?”

For investors seeking to apply the temperature-reading framework to today’s credit markets, our dedicated guide to current distressed credit conditions examines the K-shaped divergence now visible in leveraged loans, where stable headline indices mask severe distress in lower-rated debt that mirrors the early-stage conditions Marks identified before 2008.

The next major ASX story will hit our subscribers first

What the Oaktree framework demands from investors who want to apply it

The principles are easy to admire. They are difficult to execute. Each one carries a behavioural cost that most institutional cultures are not structured to absorb.

- Build credibility before you need it. Cost: reduced fee revenue during good years, and the requirement to explain counter-intuitive decisions to investors who see competitors raising larger funds.

- Position before the crisis, not during it. Cost: holding dry powder through extended bull markets while peers generate returns, creating social and professional pressure to deploy.

- Use market temperature, not point forecasts. Cost: accepting that you will be early, late, or wrong on timing, and that the framework provides direction without precision.

- Structure asymmetry rather than seeking comfort. Cost: accepting that the worst systemic scenarios genuinely cannot be hedged, and designing decisions around that honest acknowledgment.

- Treat trepidation as an input, not a weakness. Cost: institutional discomfort with admitting doubt, in cultures that reward projected certainty.

“You can do everything right and still be wrong. The job is to do everything right anyway.” — Howard Marks

Marks’s Taking the Temperature memo is structured around what he thought at the time, including uncertainty, doubt, and analytical limitations. Rather than presenting his successful calls as having been obvious in hindsight, he is careful to reconstruct the genuine ambiguity that surrounded each decision as it was made. The measure he applies is not whether every call produced the right result, but whether the reasoning behind each decision held up: grounded in mandate, anchored to pricing discipline, and consistent with frameworks established in advance rather than retrofitted afterwards.

The question for you is not whether these principles are theoretically appealing. It is which of these behavioural costs your own organisation or practice can genuinely sustain.

The preparation was the call

The $7 billion deployment was possible because of the $11 billion fund. The fund was possible because of the temperature-reading that prompted the raise. The raise was possible because of the credibility. The credibility was possible because of 20 years of behaviourally consistent decisions made at real financial cost: smaller funds when returns were high, open communication of doubt when certainty was expected, and patience through cycles when competitors were gathering assets.

The central insight is not complicated. Crisis alpha of this kind is not manufactured in the crisis. It is manufactured in the years of unglamorous, counter-intuitive preparation that most institutions find commercially uncomfortable.

This framework at full scale requires long time horizons, institutional patience, and genuine alignment between manager and investor incentives. Those cannot be shortcut. But the underlying principles (credibility, preparation, asymmetric structuring, temperature-reading, process discipline) are available to any investor willing to pay the behavioural cost.

The measure of the framework is whether the decision was defensible at the time it was made, not whether it produced 30% returns.

Marks’s standard asks you to evaluate your own process by the same measure. Not the outcome. The process.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.